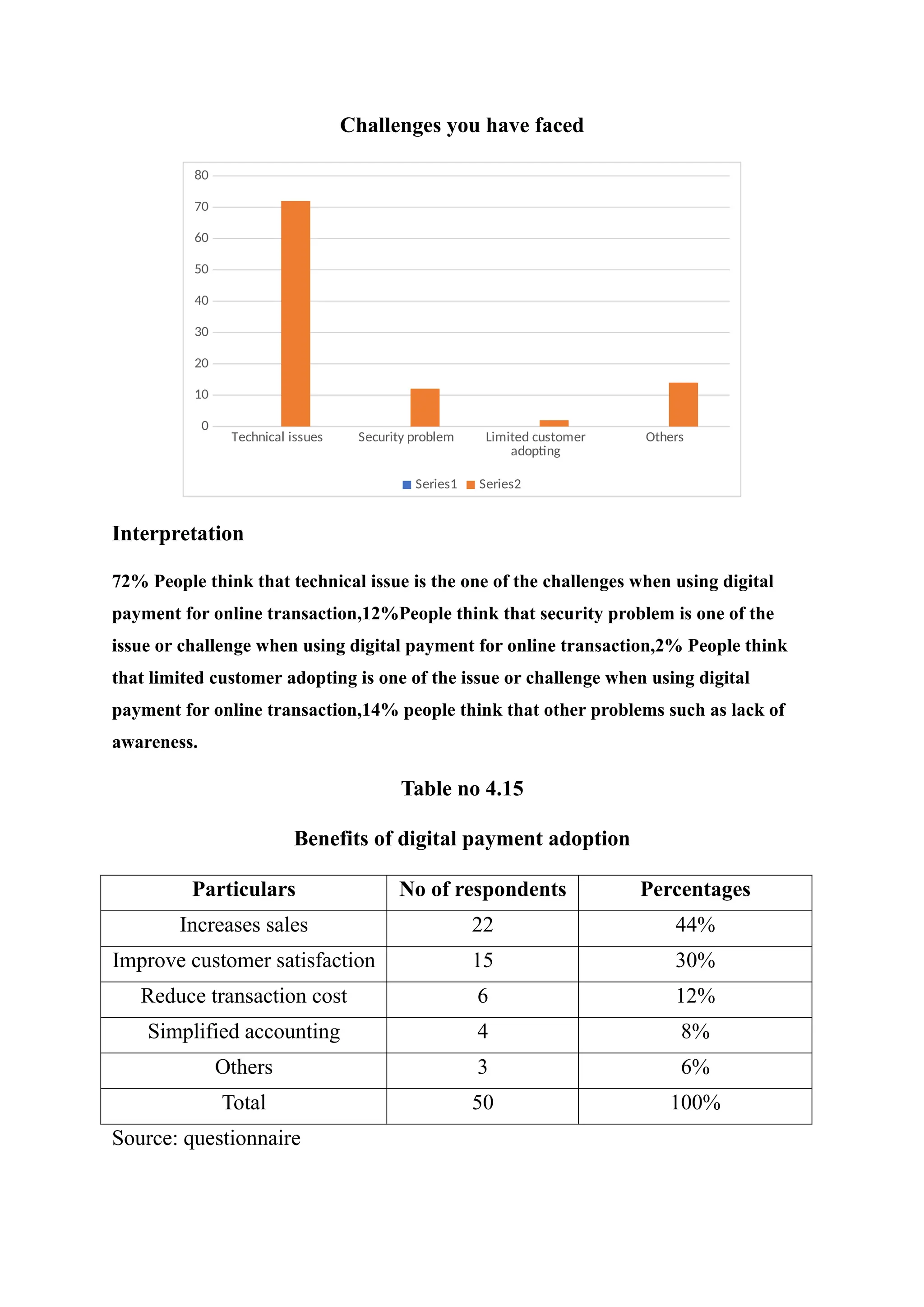

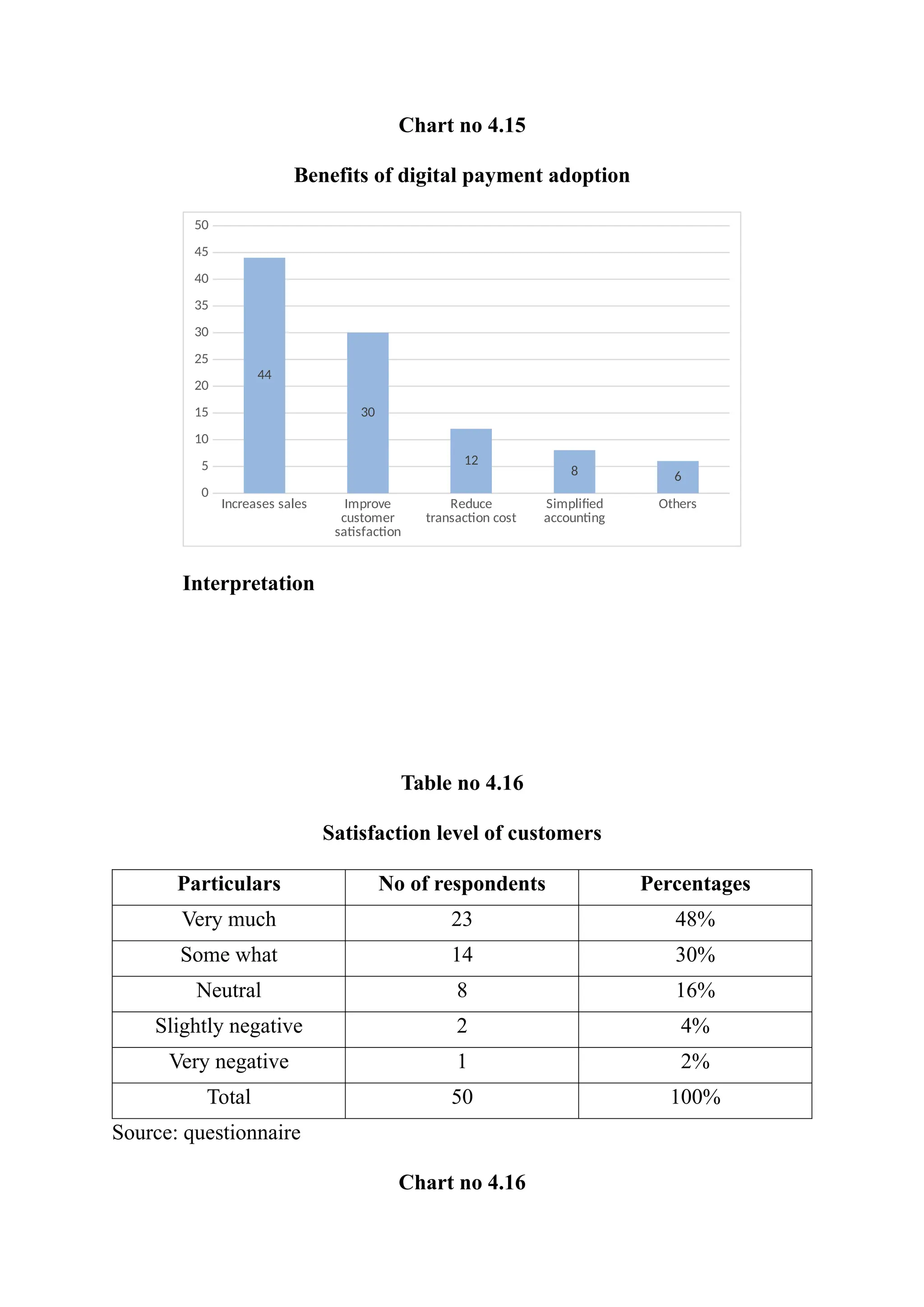

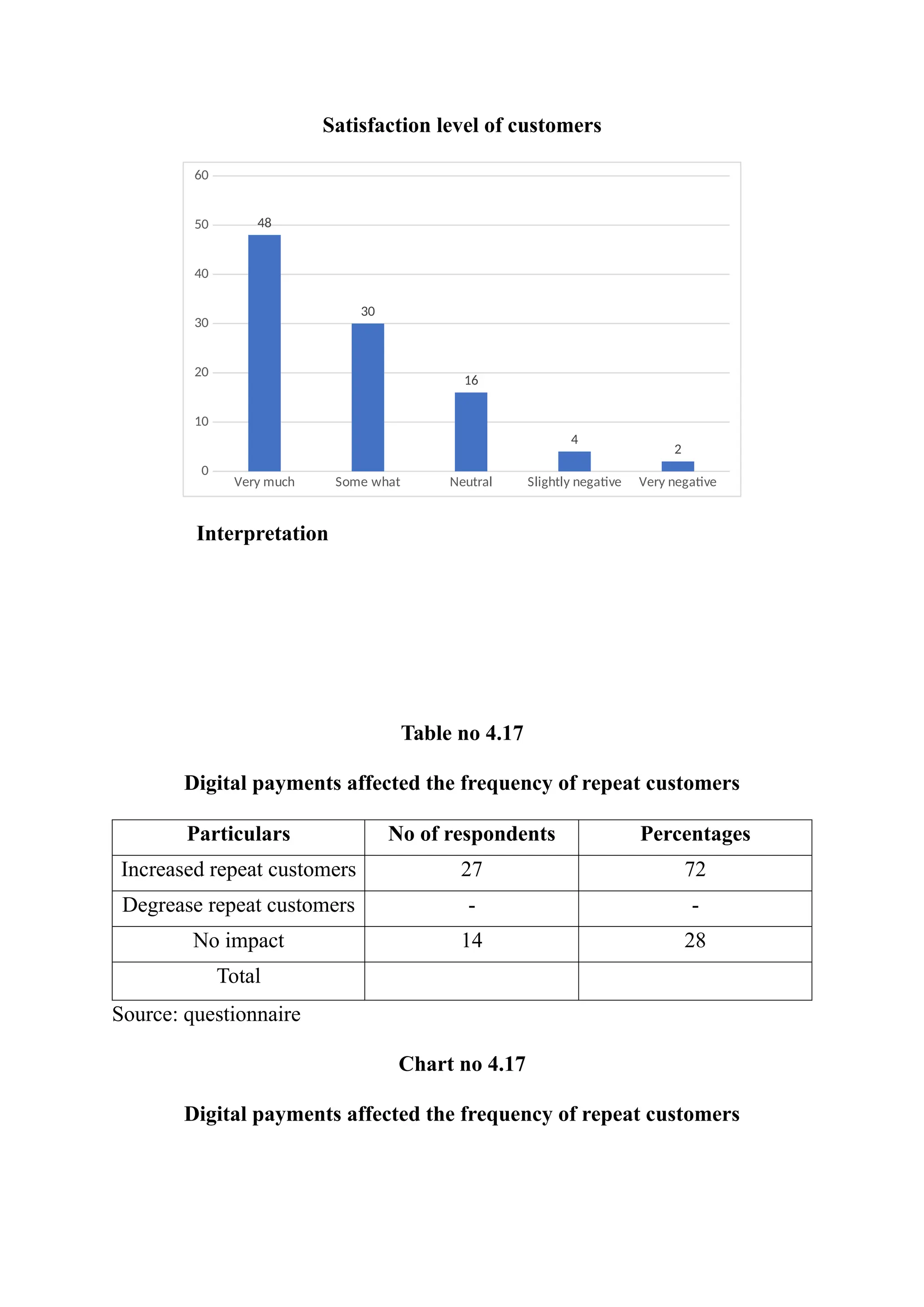

The document is a project report by Anusree V P from Calicut University Teacher Education Centre, focusing on the impact of digital payment systems on small businesses. It includes an introduction to digital payments, objectives of the study, methodology, and a review of literature regarding the adoption of digital payments, particularly in India. The research investigates various factors such as sales, revenue, customer satisfaction, and the challenges faced by small traders in adopting these technologies.