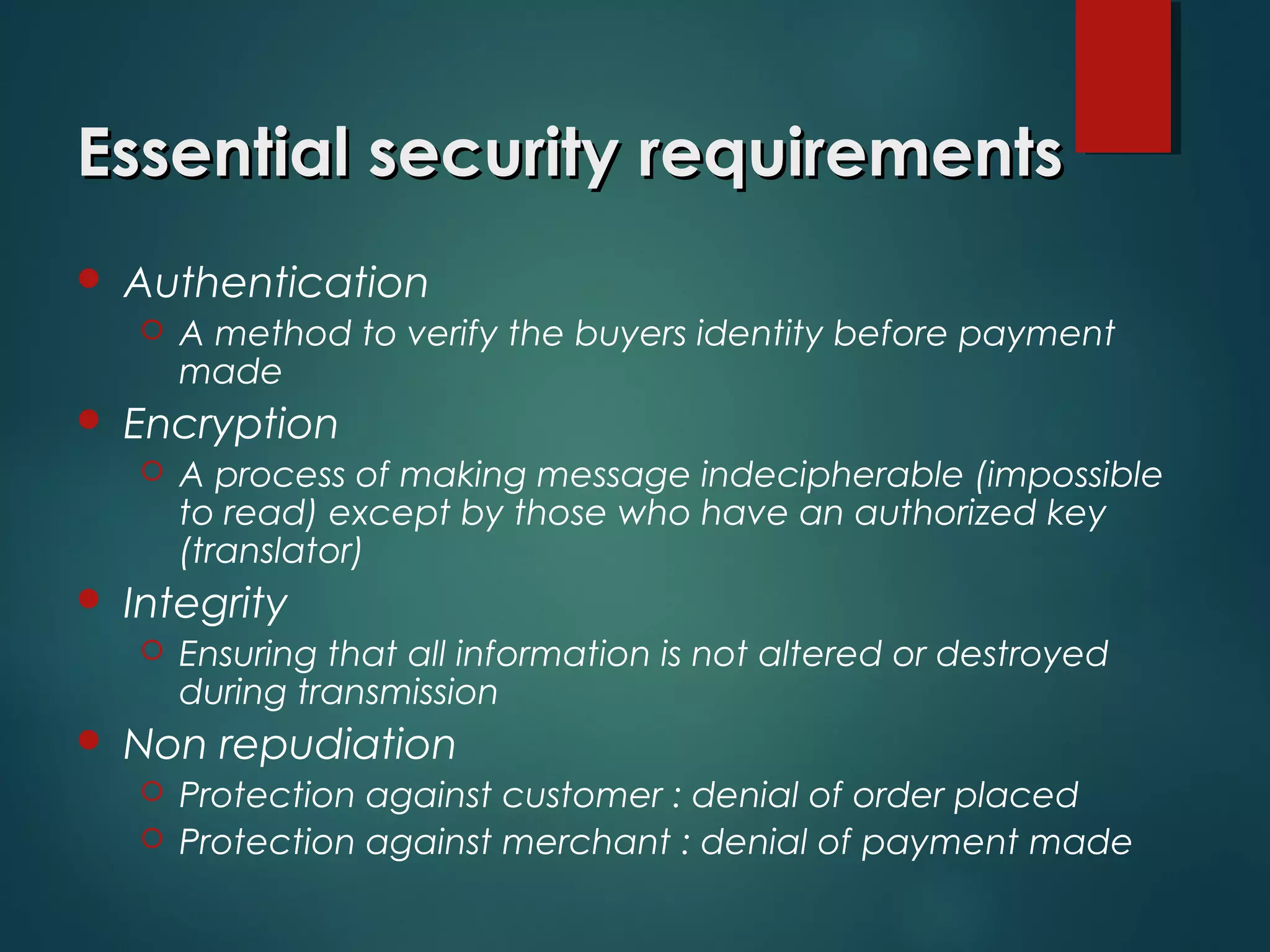

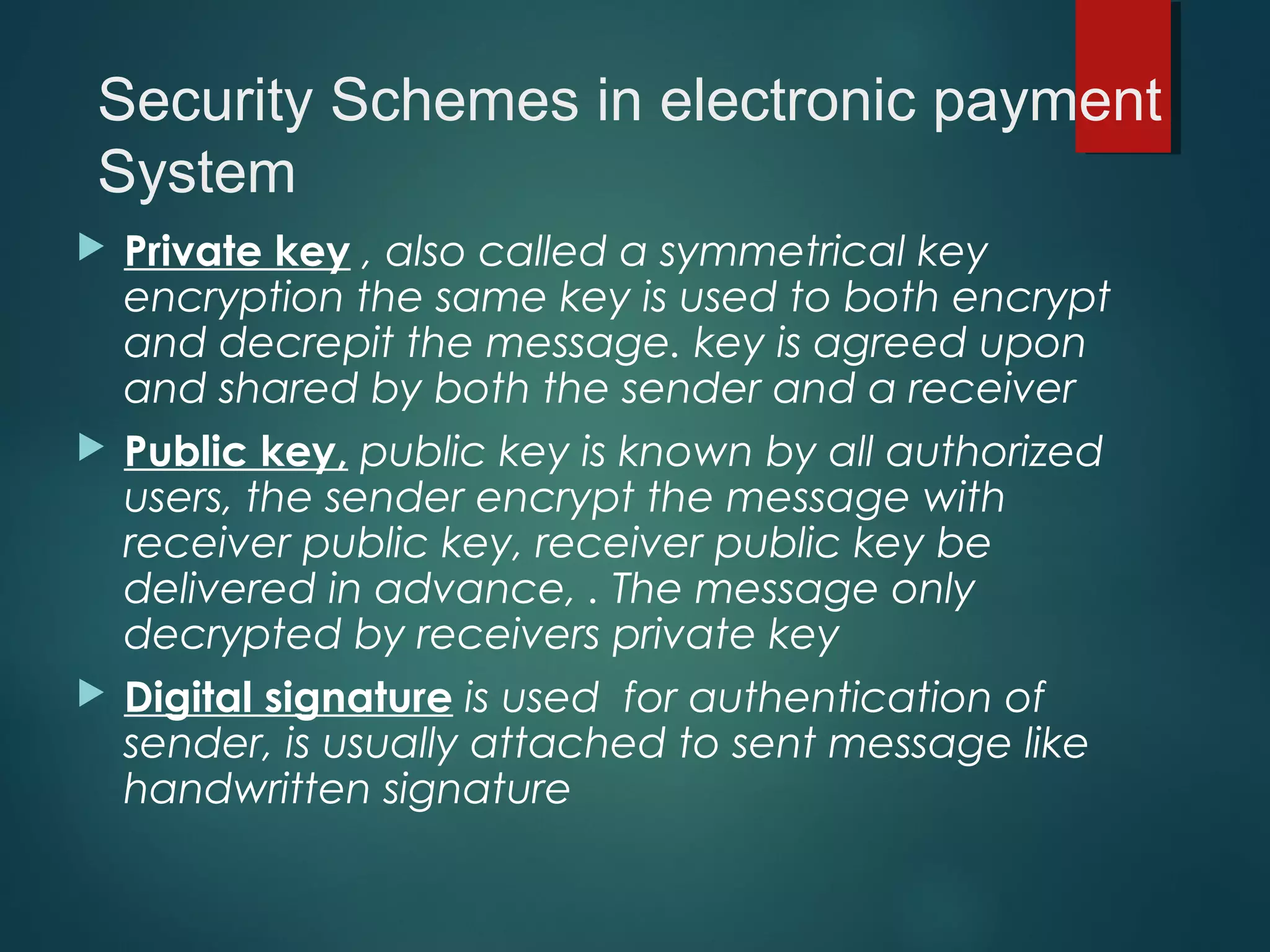

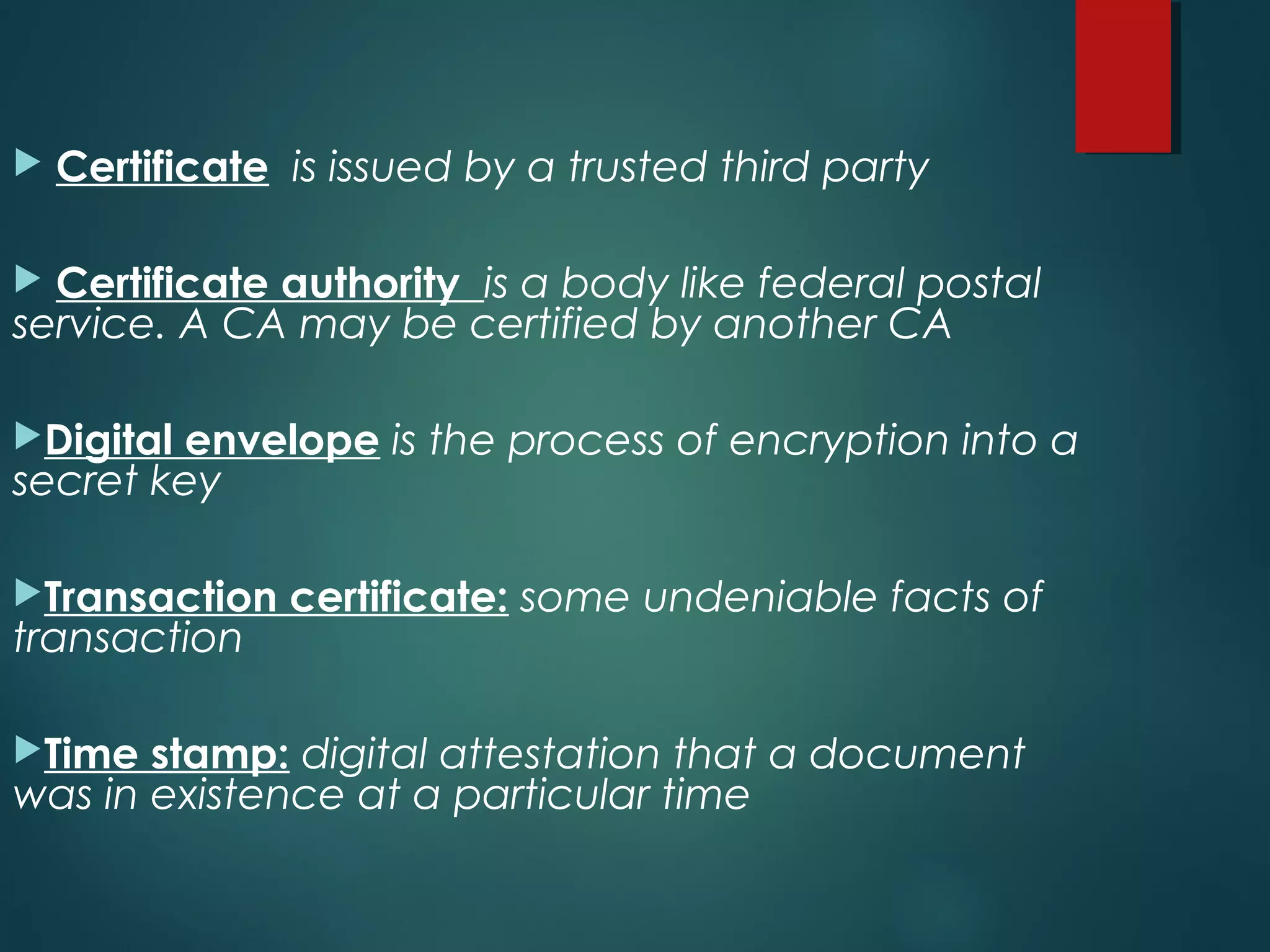

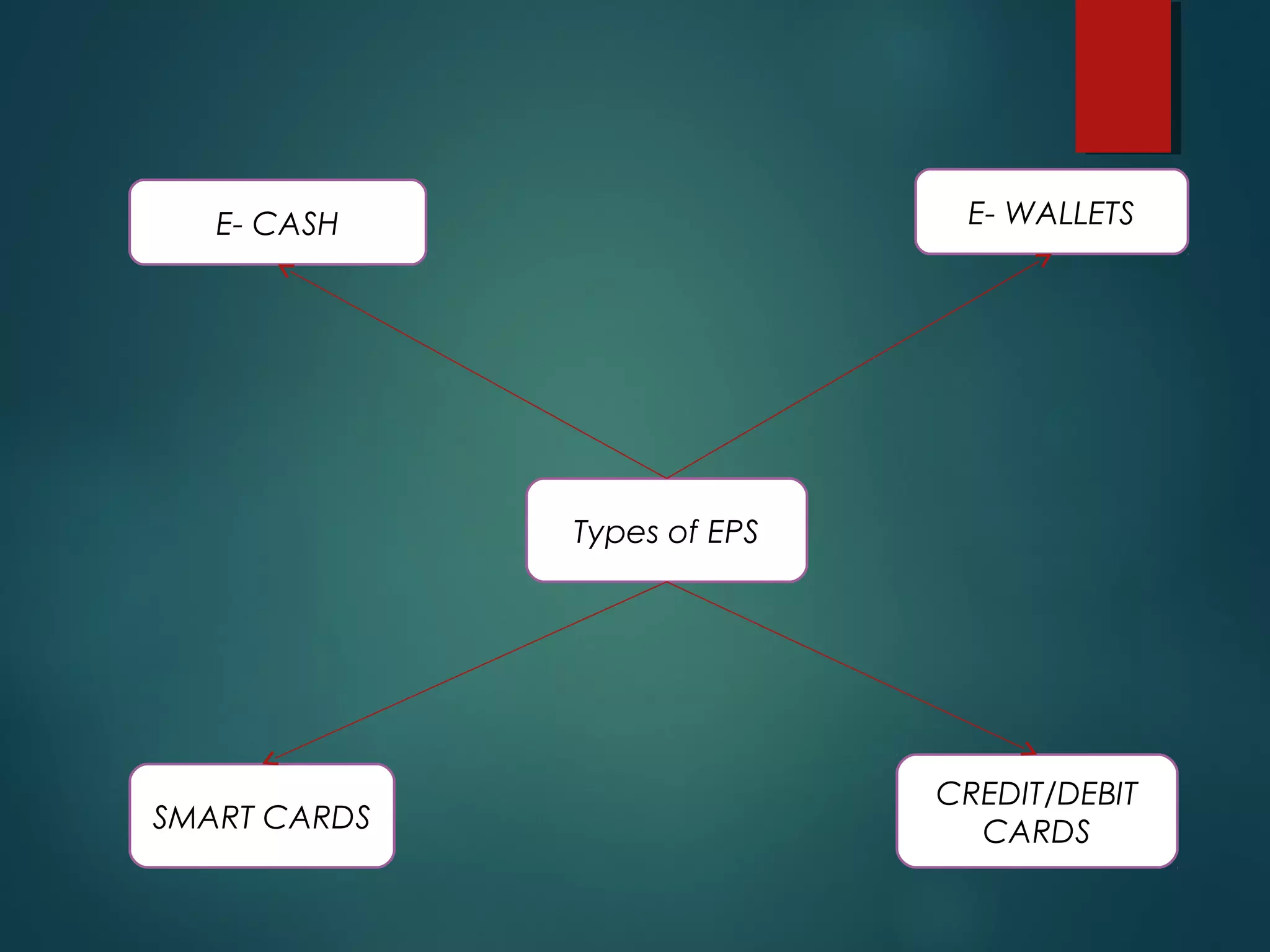

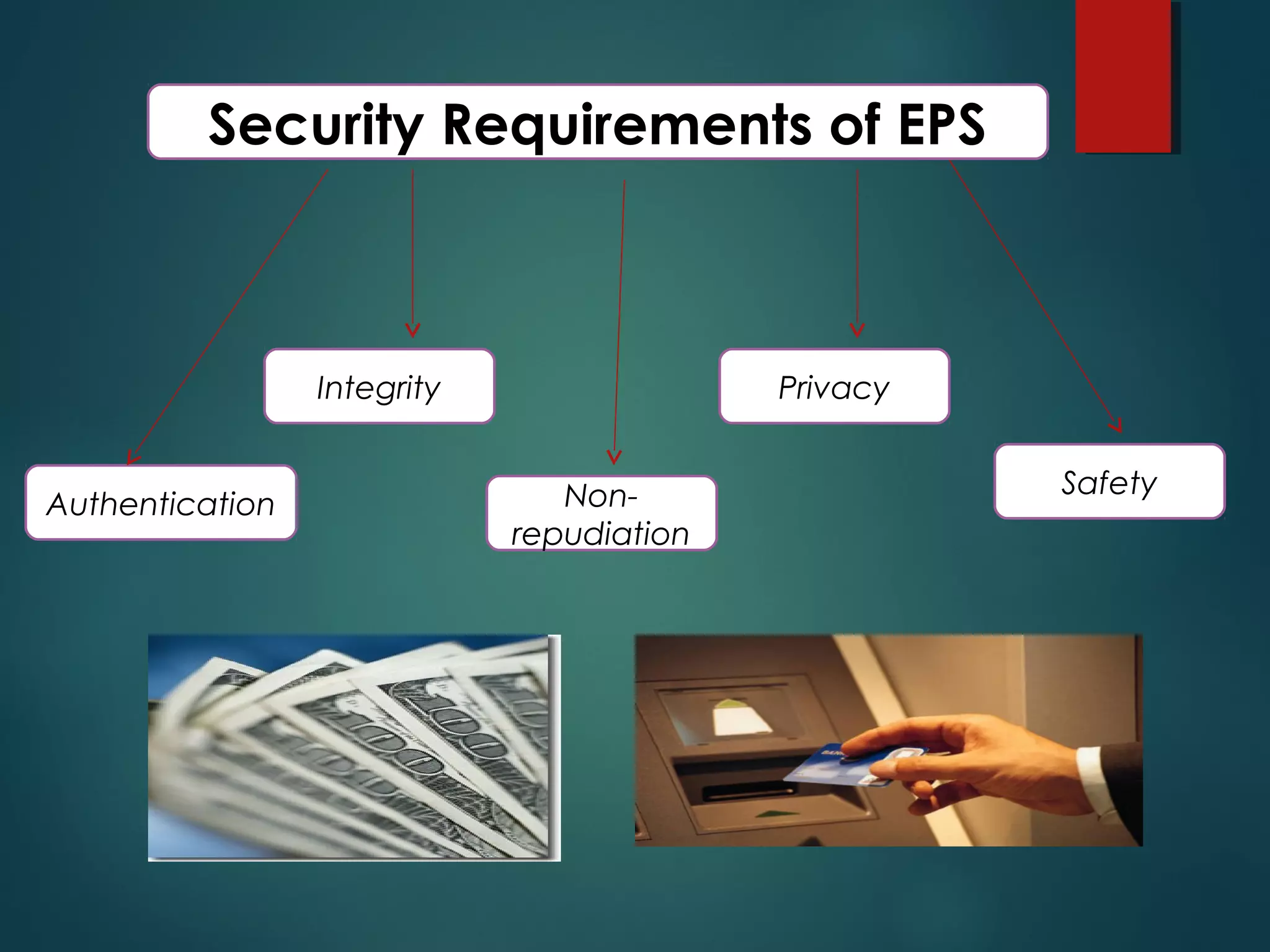

Electronic payment systems allow customers to make online payments for purchases. There are various methods of electronic payment including e-cash, smart cards, and credit/debit cards. Electronic payment systems provide authentication of users, encryption of data, integrity of information, and non-repudiation of transactions. Common types of electronic payment systems are e-cash, e-wallets, smart cards, and credit/debit cards. While electronic payment systems offer benefits like convenience and expense tracking, they also pose risks such as restrictions, hacking, lack of anonymity, and reliance on internet access.