The document discusses social networking sites and provides statistics about key players and markets in 2010. It summarizes user numbers, revenues, and rankings of top social networking sites like Facebook, Twitter, Myspace, and LinkedIn. It also provides data on the top social networking markets and sites in India and average time spent on different Indian sites. Finally, it discusses revenue models, an external environment analysis, factors for success, and analyzing competitiveness of social media companies.

Introduction Websites focusedon building online communities of people having shared interests. Social networks have common themes of information sharing, person-to-person interaction and creation of shared & collaborative content. The industry has been successful in getting a large number of people at one place, but not very successful in monetization. Two-thirds of the world’s Internet population visit a social network or blogging site and the sector now accounts for almost 20% of all internet time.

3.

Some Statistics(2010) Accordingto a study by Nielson Company, 89 per cent of 15-20 year olds in India access a social networking site everyday and 60 per cent of them spend at least half an hour on social networking each day The world now spends around 22 percent of all time online on social networks and blog sites The average visitor spends 66% more time on these sites than a year ago 9 out of every 10 U.S. Internet user now visiting a social network in a month CNN's international readership found that 43% of online news sharing occurs via social media networks and tools The number of users registered for virtual world sites broke the 1 billion mark during 2010

4.

Some Statistics (2010)BlackPlanet users spent 3.6 minutes more on the site than the average Facebook visitor MyYearbook and Tagged users spent around 3 minutes more than the average MySpace visitor Facebook witnesses more than 65 billion page views par month More than 14 million photos* are uploaded on Facebook and 8 million photos on myspace daily . *source: www.facebook.com

5.

Key Players FacebookFounded: 2004 No. of users: 600 million Revenue: US$800 million Alexa Rank: 2 Revenue from: Banner ads, referral marketing, partnerships, branding elements , virtual currency

6.

Key Players TwitterFounded: 2006 No. of users: 1 90 million Revenue: US $150 million (projected 2010) Alexa Rank: 9 Revenue from: verified accounts, advertisements (promoted trends)

7.

Key Players MyspaceFounded: 2003 No. of users: 100+ million Revenue: US$385 million (2009 est.) Alexa Rank: 68 Revenue from: advertisements, Google AdSense

8.

Key Players LinkedInFounded: 2002 No. of users: 100+ million Revenue: US $161.4 million (Jan. – Sep. 2010) Alexa Rank: 18 Revenue from: premium accounts, hiring services, advertisements, partnerships, Google AdSense

9.

Key Players OrkutFounded: 2004 No. of users: 120 million Alexa Rank: 106 Revenue from: advertisements

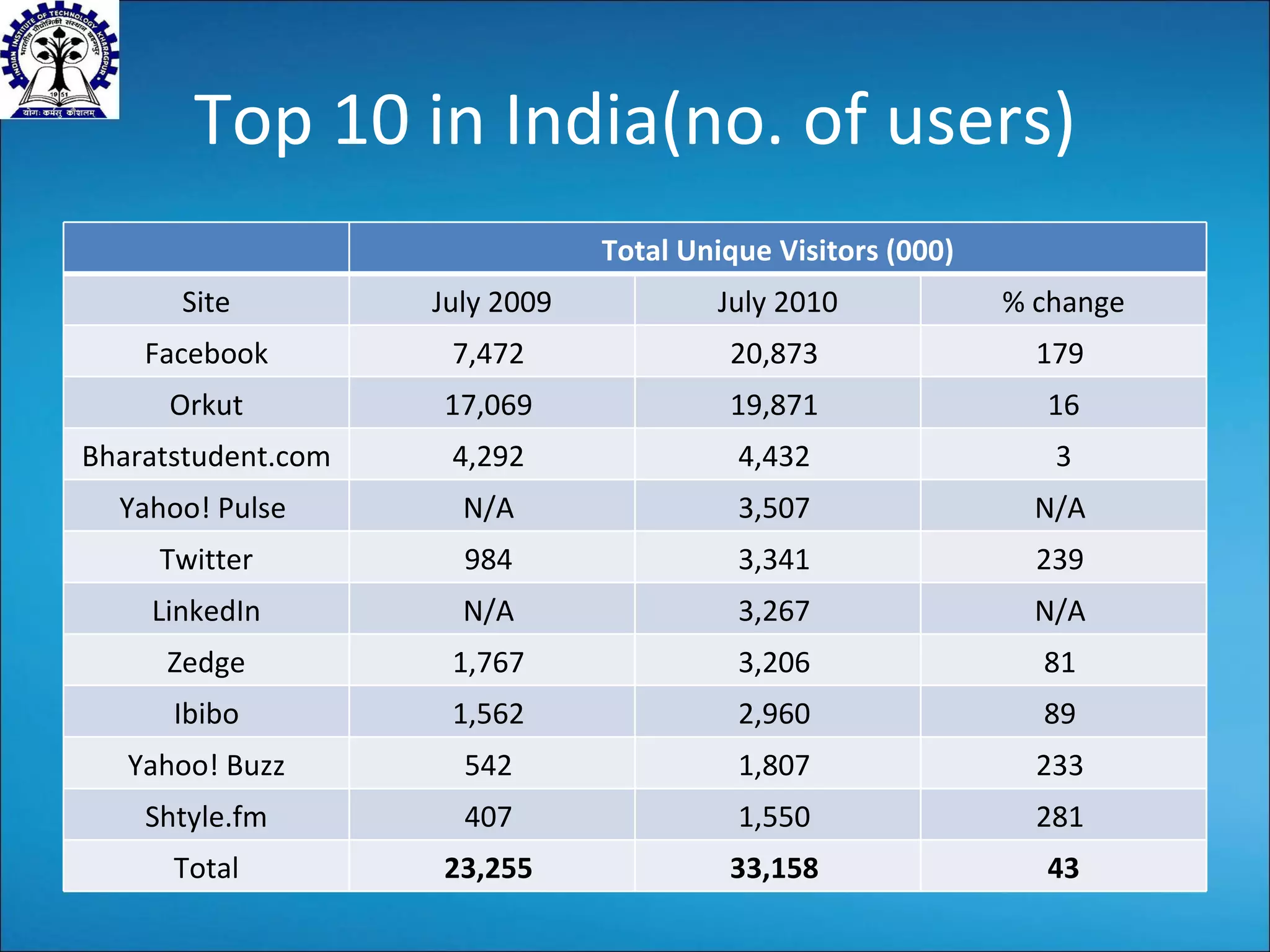

Top 10 inIndia(no. of users) Total Unique Visitors (000) Site July 2009 July 2010 % change Facebook 7,472 20,873 179 Orkut 17,069 19,871 16 Bharatstudent.com 4,292 4,432 3 Yahoo! Pulse N/A 3,507 N/A Twitter 984 3,341 239 LinkedIn N/A 3,267 N/A Zedge 1,767 3,206 81 Ibibo 1,562 2,960 89 Yahoo! Buzz 542 1,807 233 Shtyle.fm 407 1,550 281 Total 23,255 33,158 43

12.

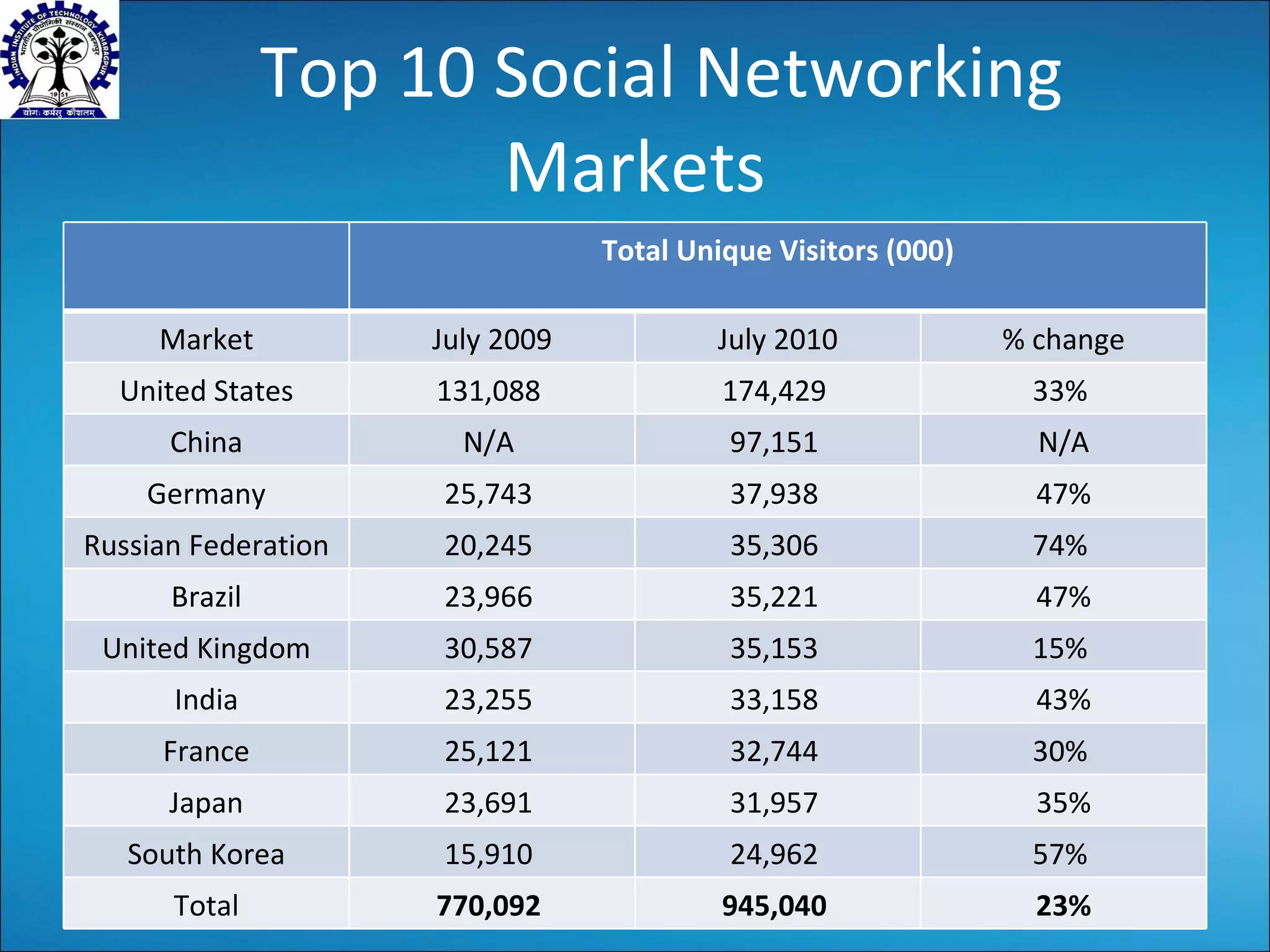

Top 10 SocialNetworking Markets Total Unique Visitors (000) Market July 2009 July 2010 % change United States 131,088 174,429 33% China N/A 97,151 N/A Germany 25,743 37,938 47% Russian Federation 20,245 35,306 74% Brazil 23,966 35,221 47% United Kingdom 30,587 35,153 15% India 23,255 33,158 43% France 25,121 32,744 30% Japan 23,691 31,957 35% South Korea 15,910 24,962 57% Total 770,092 945,040 23%

Revenue Models PremiumServices: example- LinkedIn Advertisements Cost per click (CPC) Cost per action (CPA) Cost per thousand viewers (CPM) Micropayments: small payments for upgrades Partnerships: create profiles for partners. example-twilight, Apple iTunes with Facebook, Simply Hired on LinkedIn Branding elements with applications: example- Living Social application on Facebook Virtual Currency: online applications(games). Real money for virtual goods. Annual revenue of two year old firm Zynga estimated $100 million in 2009 Virtual Gifts: more than $1 billion for US users in 2009 Surveys: pay members to participate and profit from selling access to its successful audience. Example: LinkedIn

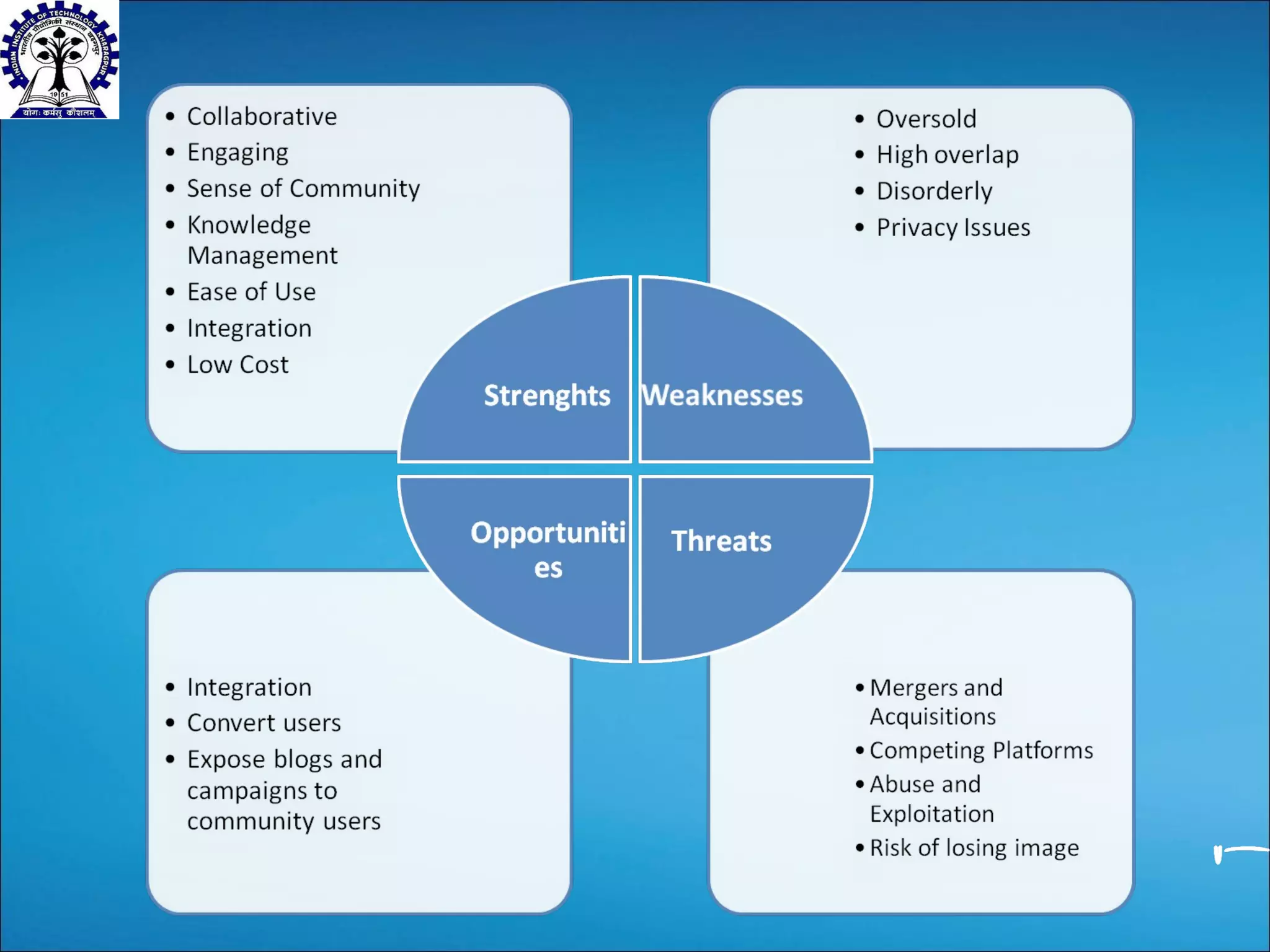

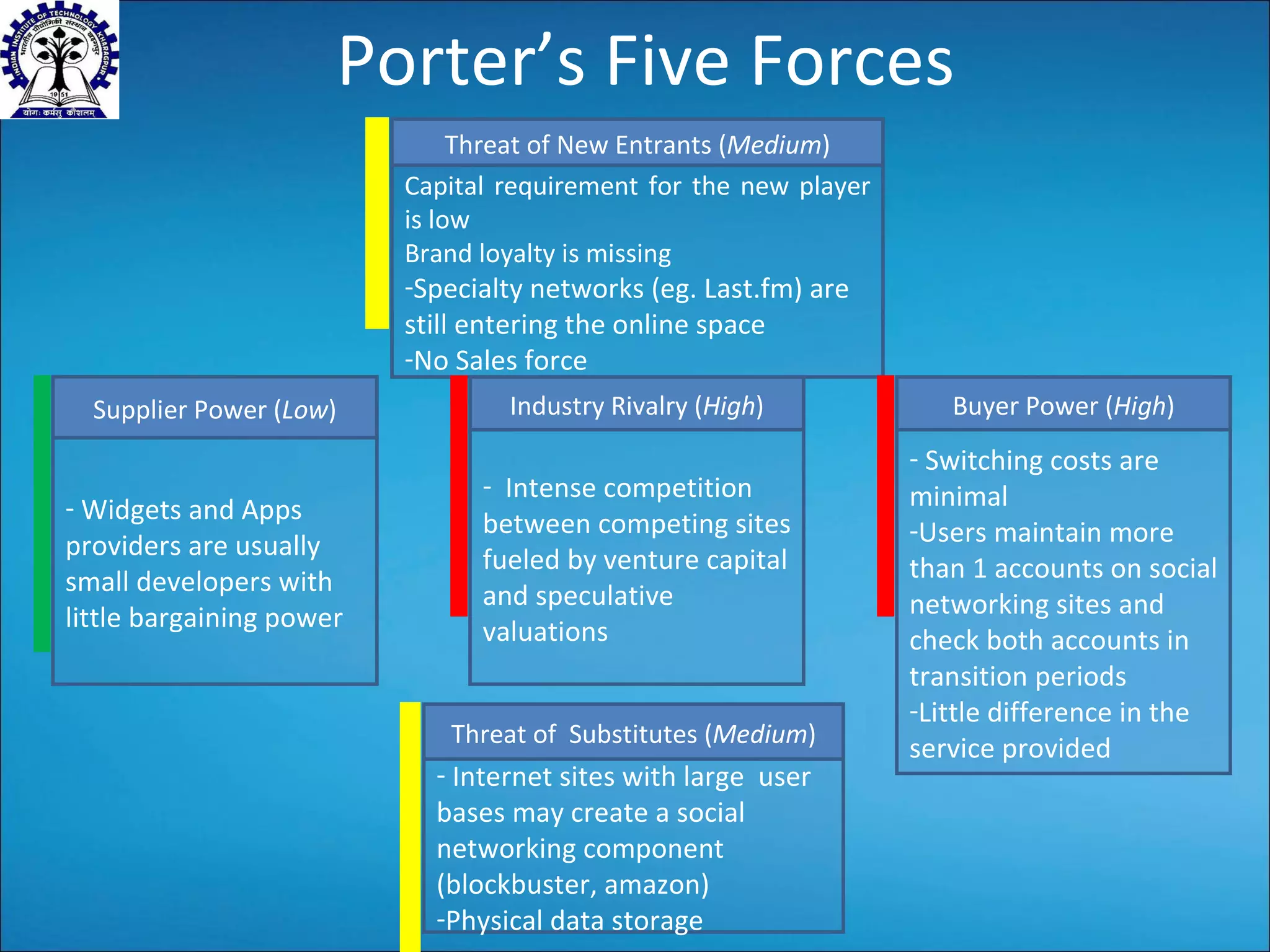

Porter’s Five ForcesThreat of New Entrants ( Medium ) Capital requirement for the new player is low Brand loyalty is missing Specialty networks (eg. Last.fm) are still entering the online space No Sales force Buyer Power ( High ) Switching costs are minimal Users maintain more than 1 accounts on social networking sites and check both accounts in transition periods Little difference in the service provided Threat of Substitutes ( Medium ) Internet sites with large user bases may create a social networking component (blockbuster, amazon) Physical data storage Supplier Power ( Low ) Widgets and Apps providers are usually small developers with little bargaining power Industry Rivalry ( High ) Intense competition between competing sites fueled by venture capital and speculative valuations

26.

Possible Success Factorsfor the industry Design – Ease of use, Attractiveness etc. Target Market – Some sites target niches, some target goegraphies Activity Focus – Target market can be connecting people over relationships, or over shared interests User Engagement – Site needs to retain user minutes Transactions – Innovative features like applications Privacy –privacy filters and controls Entry Barriers – Easy sign ups Trust – Different outlooks to Trust. Localization – Local content, languages etc.

27.

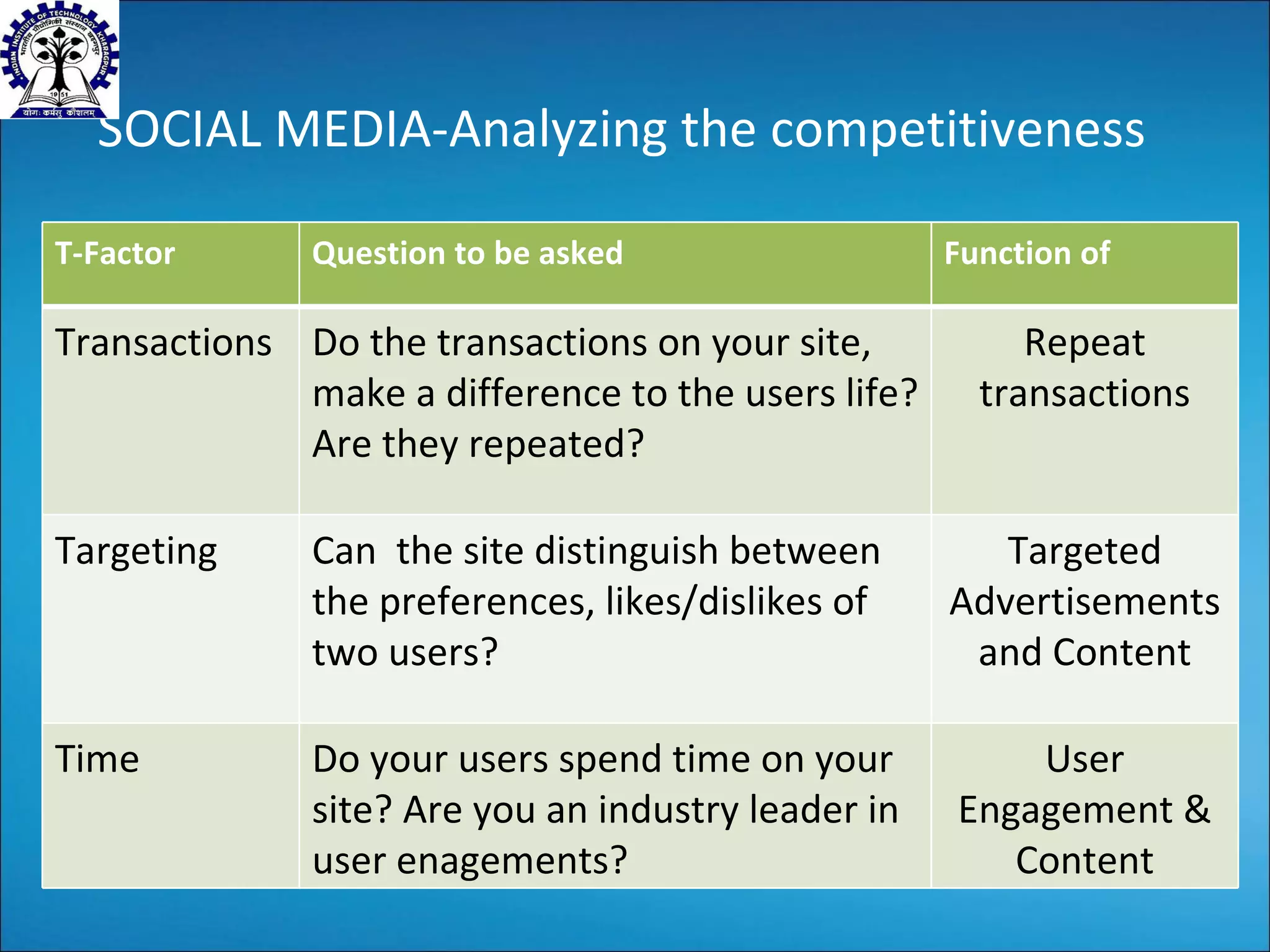

SOCIAL MEDIA-Analyzing thecompetitiveness T-Factor Question to be asked Function of Transactions Do the transactions on your site, make a difference to the users life? Are they repeated? Repeat transactions Targeting Can the site distinguish between the preferences, likes/dislikes of two users? Targeted Advertisements and Content Time Do your users spend time on your site? Are you an industry leader in user enagements? User Engagement & Content

#28 The 3T’s framework : 1) Orkut didn’t personalize (failure on the Targeting front. FB lets users even pick the kind of ‘real-time’ information they want to see. Eg. ‘I want to see more photo updates from friends. I want to less of relationship updates from friends, etc.’ MySpace didn’t innovate fast enough Active users are the audience based on which a site can be monetized. Facebook concentrates on building this.

#29 JP Morgan Report: Digital strategy is not working . MySpace revenue was flat Y/Y and FIM OI declined to $7M from $47M in Q2 FY08. MySpace continues to face challenges monetizing its large audience. We see more headwinds ahead as remnant inventory pricing is declining and competition makes it more difficult to reach meaningful profitability. Additionally, we are concerned that economics of search will worsen significantly when the deal with Google ends in Q4 FY10 creating additional pressure on profitability

#30 JP Morgan Report: Digital strategy is not working . MySpace revenue was flat Y/Y and FIM OI declined to $7M from $47M in Q2 FY08. MySpace continues to face challenges monetizing its large audience. We see more headwinds ahead as remnant inventory pricing is declining and competition makes it more difficult to reach meaningful profitability. Additionally, we are concerned that economics of search will worsen significantly when the deal with Google ends in Q4 FY10 creating additional pressure on profitability