Unit 4: FinalAccounts of a Sole Trader

Preparation of Income statement – Trading Account and Profit and Loss Account; Preparation of

Balance Sheet; Treatment of adjustments - Closing Stock, Outstanding Expenses, Prepaid or Unexpired

Expenses, Accrued Income, Unearned Income, Income Received in Advance, Depreciation, Interest on

Capital, Interest on Drawings, Interest on Loan, Bad Debt, Provision for Bad and Doubtful Debts.

---------------------------------------------------------------------------------------------------------------------------

4.1 Introduction to final accounts

Business entities raise funds, acquire assets and incur various expenses for the purpose of carrying on

business operations and earning income from such operations. These transactions are first recorded in

the journal and then classified under common heads in the ledger. Preparation of trial balance from

ledger balances helps to verify the arithmetical accuracy of entries made in the books of accounts, but

it is not the end in itself. The business entities are interested in knowing periodically the results of

business operations carried on and the financial soundness of the business. In other words, they want to

know the profitability and the financial position of the business. These can be ascertained by preparing

the final accounts or financial statements. The final accounts are usually prepared at the end of the

accounting period on the basis of balances of ledger accounts shown by the trial balance.

The final accounts or financial statements include the following:

a. Income Statement or Trading and Profit and Loss Account and

b. Position Statement or Balance Sheet.

The purposes of preparing the financial statements are:

i. To ascertain the financial performance of an enterprise and

ii. To ascertain the financial position of an enterprise.

The income statement and balance sheet are prepared for these purposes respectively. Income statement

gives the manner in which the profit or loss for an accounting period is arrived at. The revenues earned

and expenses incurred to earn the revenues during the period are shown in the income statement under

appropriate heads as per matching principle. All the nominal accounts and accounts relating to goods

during an accounting period are to be considered only in the relevant accounting period and are not to

be carried forward. Moreover, only these items are to be compared for determining the financial

performance. Hence, at the close of the accounting period, all nominal accounts (i.e. expenses, losses,

revenues, gains, purchases, purchases returns, sales and sales returns) are to be closed by transferring

to the income statement or trading and profit and loss account.

While transferring the items, it is desirable that the results of buying and selling of goods and the results

of overall operations and financial performance are given separately. Hence, income statement is

divided into two parts. The first part, i.e., trading account shows the results of buying and selling and

the second part shows the results of overall financial performance. The second part may also be

presented in such a manner to give the operating results and overall financial performance separately.

All the direct expenses and items relating to goods are transferred to trading account which is the first

part of income statement. All indirect expenses and losses and indirect incomes and gains are transferred

to profit and loss account along with the net result of trading account.

2.

4.2 Trading account

Tradingrefers to buying and selling of goods with the intention of making profit. The trading account

is a nominal account which shows the result of buying and selling of goods for an accounting period.

According to J. R. Batliboi, “The trading account shows the results of buying and selling of goods. In

preparing this account, the general establishment charges are ignored and only the transactions in goods

are included.”

Trading account is prepared to find out the difference between the revenue from sales and cost of goods

sold. Cost of goods sold refers to directly related cost. Direct cost includes the purchase price of goods

purchased and all other expenses which are incurred to bring the goods to the business premises or

godown and to make these ready for sale. All the goods purchased during the accounting period may

not be sold during the same accounting period. Hence, it is necessary to calculate the cost of goods sold

during the period. Matching principle is applied here. Hence, the cost of stock not sold must be

deducted, i.e., value of closing stock must be deducted. But if there is any opening stock of goods that

will be sold during the accounting period, it is to be added to the cost of purchases made during the

period. If there is cost of goods manufactured, it must also be added to find out the cost of goods sold.

Cost of goods sold = Opening stock + Net purchases + Direct expenses – Closing stock

If the amount of sales exceeds the cost of goods sold, the difference is gross profit. On the other hand,

the excess of cost of goods sold over the amount of sales results in gross loss.

Sales – Cost of goods sold = Gross profit

Sales – Gross profit = Cost of goods sold

4.2.1 Need for preparation of trading account

Preparation of trading account serves the following purposes:

(i) Provides information about gross profit or gross loss

It shows the gross profit or gross loss of the business for an accounting year. This helps the

businesspersons to find out gross profit ratio by expressing the gross profit as a percentage of sales. It

helps to compare and analyse with the ratios of the previous years. Thus, it provides data for

comparison, analysis and planning for a future period.

(ii) Provides an opportunity to safeguard against possible losses

If the ratio of gross profit has decreased in comparison to the preceding years, effective measures can

be taken to safeguard against future losses. For example, the sale price of goods may be increased, or

steps may be taken to analyse and control the direct expenses.

(iii) Provides information about direct expenses and direct incomes

All the expenses incurred on the purchase of goods are direct expenses. They are recorded in the trading

account. Trading account also shows sales revenue, which is a direct income. With the help of trading

account, percentage of such expenses on sales revenue can be calculated and compared with similar

ratios of the previous years. Thus, it enables the management to have control over the direct expenses.

4.2.2 Preparation of trading account

Trading account is a nominal account. The opening stock, net purchases and all expenses relating to

purchase of goods are shown on the debit side and the net sales and closing stock are shown on the

credit side of it.

A) Items shown on the debit side of the trading account

The following are the items shown on the debit side of the trading account:

(i) Opening stock

The stock of goods remaining unsold at the end of the previous year is the opening stock of the current

year. This item will not be there in a newly started business. It will not appear if it is adjusted with

purchases. As opening stock would have been sold during the year, the cost of opening stock is included

in trading account.

(ii) Purchases and purchases returns

Goods which have been bought for resale are termed as purchases. Goods purchased which are returned

to suppliers are termed as purchases returns or returns outward. Purchases include both cash purchases

3.

and credit purchases.Net purchases, i.e., purchases minus purchases returns are shown in the debit side

of the trading account.

(iii) Direct expenses

All the expenses incurred on the purchase of goods and for bringing the goods to the go down or place

of business and to make them to saleable condition are known as direct expenses. They are debited to

trading account. Direct expenses include the following:

(a) Carriage inwards or Freight inwards

Amount paid for transporting the goods purchased to the godown or business premises is called carriage

inwards or carriage on purchases or freight inwards.

(b) Wages

Amount paid to workers who are directly engaged in loading, unloading and handling of goods

purchased is known as wages.

(c) Dock Charges

These are the charges levied for shipping the cargo while entering or leaving docks. When they are paid

on import of goods, they are treated as direct expenses.

(d) Octroi

This is a tax levied by the local authority when the purchased goods enter the municipal limits.

(e) Import duty

Taxes paid on import of goods are known as import duties.

(f) Royalty

This is the amount paid to the owner of a mine or a patent for using owner’s right. When the royalty is

based on cost of production or output, it is treated as a direct expense.

(g) Coal, gas, fuel and power

Cost incurred towards coal, gas and fuel to make the goods saleable is also considered as direct

expenses.

(iv) Cost of goods manufactured

If the sole proprietor is also engaged in manufacture of goods, a separate account, namely,

manufacturing account is to be prepared in which expenses incurred for manufacture of goods will be

entered. Examples of such expenses are raw materials, coal, gas, fuel, water, power, factory rent,

packaging, factory lighting, royalty on manufactured goods, etc. The total cost of goods manufactured

is transferred to the debit side of trading account.

B) Items shown on the credit side of the trading account

Following are the items shown on the credit side of the trading account:

(a) Sales and Sales returns

Both cash and credit sales of goods will be included in sales. The sales account will show credit balance

whereas the sales returns account will show debit balance. The amount of net sales is shown on the

credit side of the trading account by deducting sales returns from sales.

(b) Closing stock

The goods remaining unsold at the end of the accounting period are known as closing stock. They are

valued at cost price or net realisable value (market price) whichever is lower as per Accounting Standard

2 (Revised).

4.

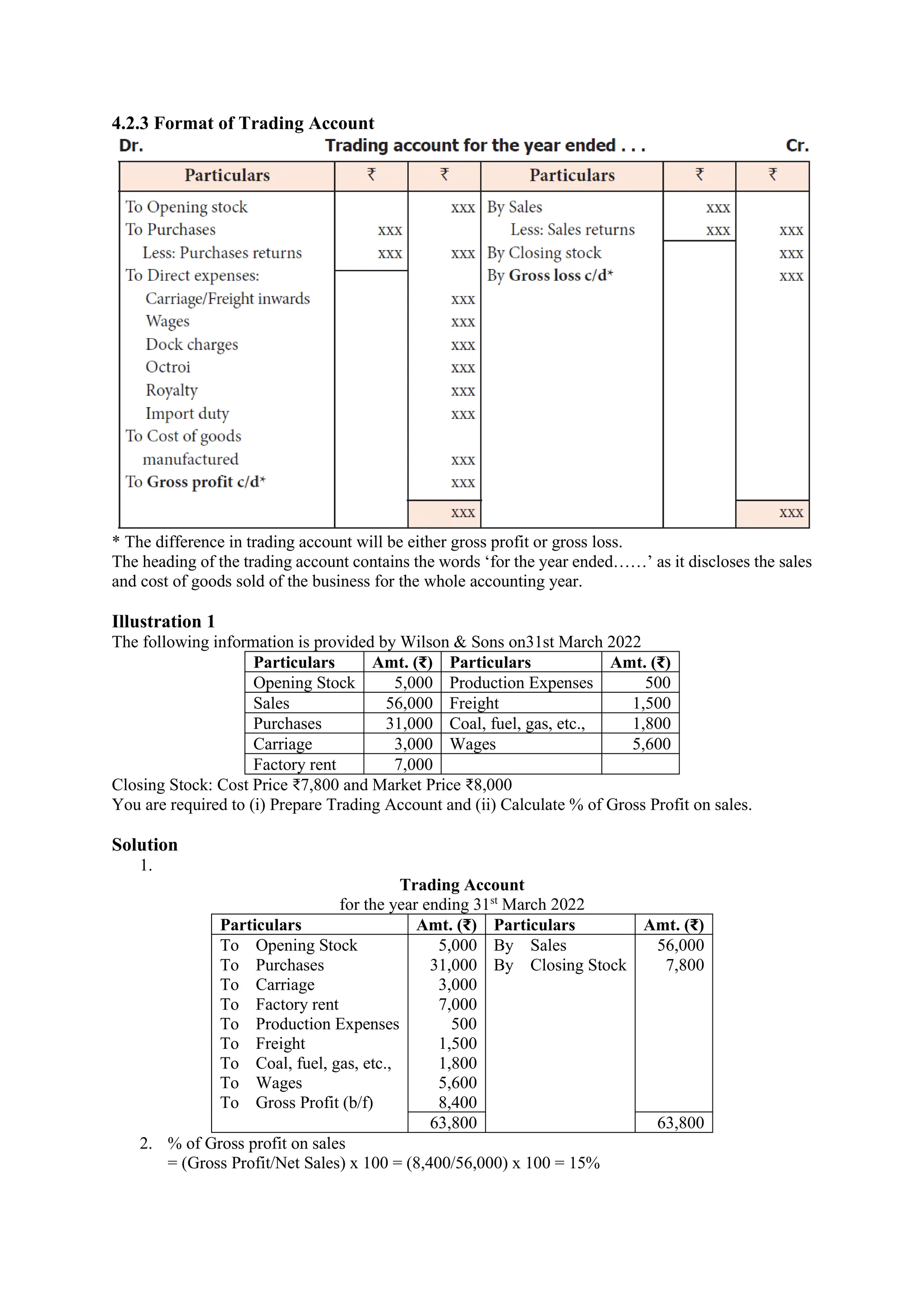

4.2.3 Format ofTrading Account

* The difference in trading account will be either gross profit or gross loss.

The heading of the trading account contains the words ‘for the year ended……’ as it discloses the sales

and cost of goods sold of the business for the whole accounting year.

Illustration 1

The following information is provided by Wilson & Sons on31st March 2022

Particulars Amt. (₹) Particulars Amt. (₹)

Opening Stock 5,000 Production Expenses 500

Sales 56,000 Freight 1,500

Purchases 31,000 Coal, fuel, gas, etc., 1,800

Carriage 3,000 Wages 5,600

Factory rent 7,000

Closing Stock: Cost Price ₹7,800 and Market Price ₹8,000

You are required to (i) Prepare Trading Account and (ii) Calculate % of Gross Profit on sales.

Solution

1.

Trading Account

for the year ending 31st

March 2022

Particulars Amt. (₹) Particulars Amt. (₹)

To Opening Stock 5,000 By Sales 56,000

To Purchases 31,000 By Closing Stock 7,800

To Carriage 3,000

To Factory rent 7,000

To Production Expenses 500

To Freight 1,500

To Coal, fuel, gas, etc., 1,800

To Wages 5,600

To Gross Profit (b/f) 8,400

63,800 63,800

2. % of Gross profit on sales

= (Gross Profit/Net Sales) x 100 = (8,400/56,000) x 100 = 15%

5.

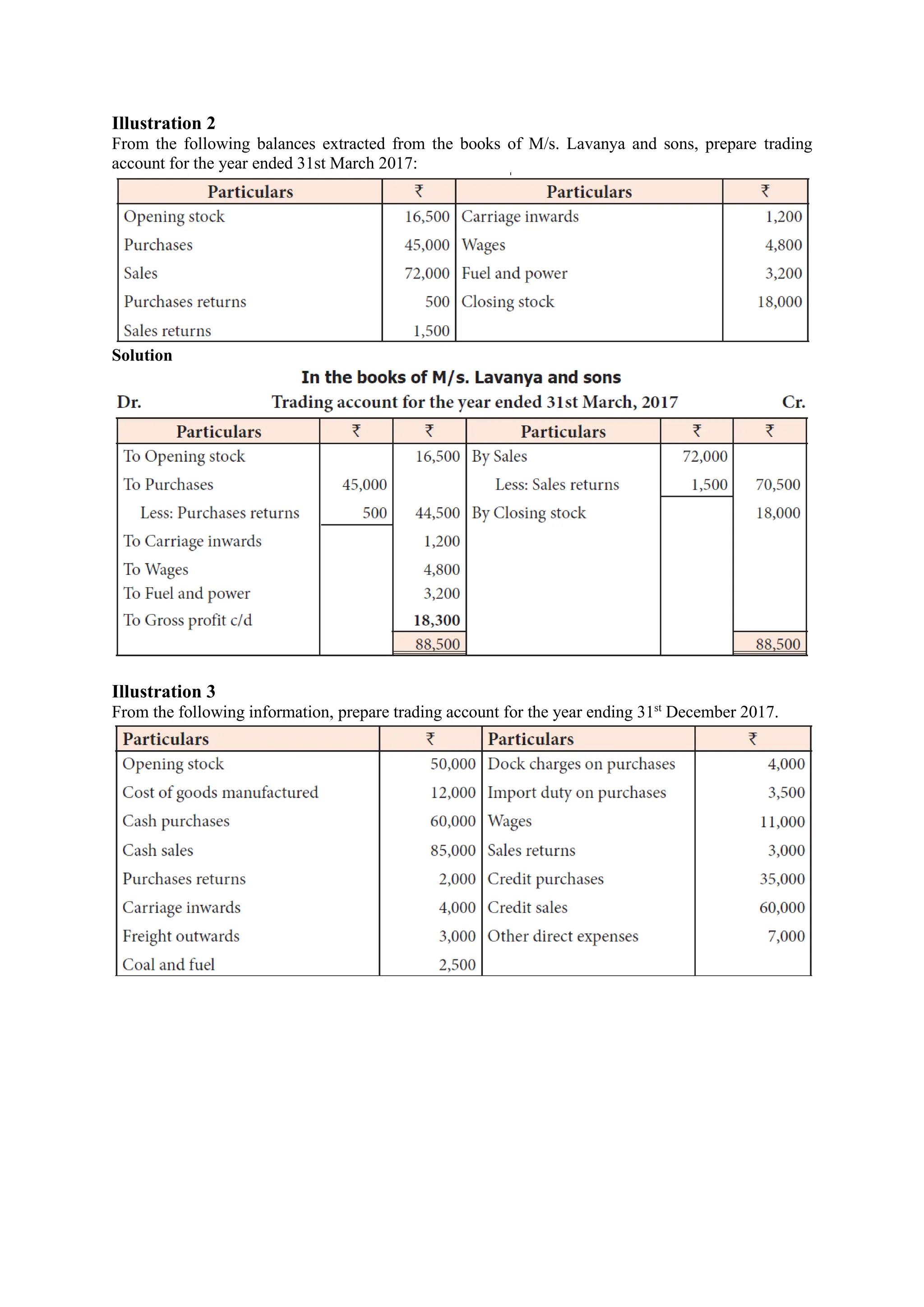

Illustration 2

From thefollowing balances extracted from the books of M/s. Lavanya and sons, prepare trading

account for the year ended 31st March 2017:

Solution

Illustration 3

From the following information, prepare trading account for the year ending 31st

December 2017.

6.

Solution

Classwork

Problem 1

Prepare TradingAccount of M/s Robin Pandey & Sons for the year ending 31st

March 2022 from the

following information.

Particulars Amt. (₹) Particulars Amt. (₹)

Purchases 79,800 Sales Return 1,400

Sales 1,05,900 Carriage outwards 2,300

Salaries 7,600 Carriage inwards ,1900

Wages 11,000 Purchase Returns 2,300

Rent 1,700 Insurance 800

Freight 1,900 Bad debts 1,500

Production Expenses 780 Dock Charges paid 1,800

Stock (opening) 11,500 Trading Expenses 7,000

Closing Stock at the end was ₹15,700.

[Answer: Gross Profit: ₹13,820]

Note: Salaries, Rent, Carriage Outwards, Insurance, Bad debts and Trading Expenses are shown in the

profit & loss account, as these are indirect expenses. In Trading Account only direct expenses are

shown.

Self-Assessment

Q. No. 1

From the following balances of M/s Simran, prepare Trading Account for the year ended 31st

March

2022.

Particulars Amt. (₹) Particulars Amt. (₹)

Stock (01.04.2021) 5,700 Carriage Inwards 7,500

Purchases 1,11,000 Carriage Outwards 9,700

Sales 2,26,000 Rent and Taxes 1,380

7.

Return Outwards 4,000Production Expenses 4,380

Return Inward 5,000 Coal, Fuel, Gas, etc., 7,380

Salaries 11,700 Lighting and Heating (office) 2,380

Wages 6,900 Import Duty 1,340

Closing Stock at the end was ₹7,900

[Answer: Gross Profit: ₹88,700]

4.3 Profit and Loss Account

Profit and loss account is the second part of income statement. It is a nominal account in nature. A

business entity is interested in knowing not only the gross profit or loss but also the net profit earned,

or net loss incurred during the year. Hence, profit and loss account is prepared to ascertain the net profit

or net loss during the year. Profit and loss account contains all the items of indirect expenses and losses

and indirect incomes and gains in addition to gross profit or gross loss pertaining to the accounting

period. The difference is net profit or net loss. According to Prof. Carter, “A Profit and Loss Account

is an account into which all gains and losses are collected, in order to ascertain the excess of gains over

the losses or vice-versa”.

4.3.1 Need for preparing profit and loss account

Profit and loss account is prepared for the following purposes:

(i) Ascertainment of net profit or net loss

The profit and loss account discloses the net profit available to the proprietor or net loss to be borne by

him. Ascertainment of profitability helps in planning for the growth and efficiency of a business

enterprise. Inter-firm comparison and intra-firm comparison of profit and loss account items help in

assessing efficiency in comparison with other enterprises and other departments of the same enterprise

respectively.

(ii) Comparison of profit

The net profit of the current year can be compared with the profit of the previous years. It helps to know

whether the business is conducted efficiently or not.

(iii) Control on expenses

Profit and loss account helps in comparing various expenses with the expenses of the previous years.

The percentage of individual expenses to net sales can be calculated and compared with

the similar ratios of previous years. Such a comparison will be helpful in taking effective steps for

controlling unnecessary expenses.

(iv) Helpful in the preparation of balance sheet

A balance sheet can be prepared only after ascertaining the net profit or loss through profit and loss

account. Net profit or loss is shown in the balance sheet. Thus, it facilitates preparation of balance sheet.

4.3.2 Preparation of profit and loss account

The amount of gross profit or gross loss brought down from the trading account is the first item in the

profit and loss account. All the indirect expenses and losses are debited to profit and loss account.

Indirect expenses include office and administrative expenses, selling expenses, distribution expenses,

etc. As the profit and loss account is a nominal account, all the indirect expenses and losses are shown

on the debit side and all the indirect incomes and gains are shown on the credit side.

Items shown on the debit side of profit and loss account are as follows:

(i) Gross loss

If trading account discloses gross loss, it is shown on the debit side of the profit and loss account.

(ii) Indirect expenses

Expenses which are not connected with purchase of goods are indirect expenses, i.e., expenses incurred

in administration, office, selling and distribution of goods are indirect expenses.

(a) Office and administrative expenses

Expenses incurred for office and administration such as salary of office employees, office rent, lighting,

postage, printing, legal charges, audit fee, depreciation and maintenance of office equipment, etc. are

classified as office and administrative expenses.

8.

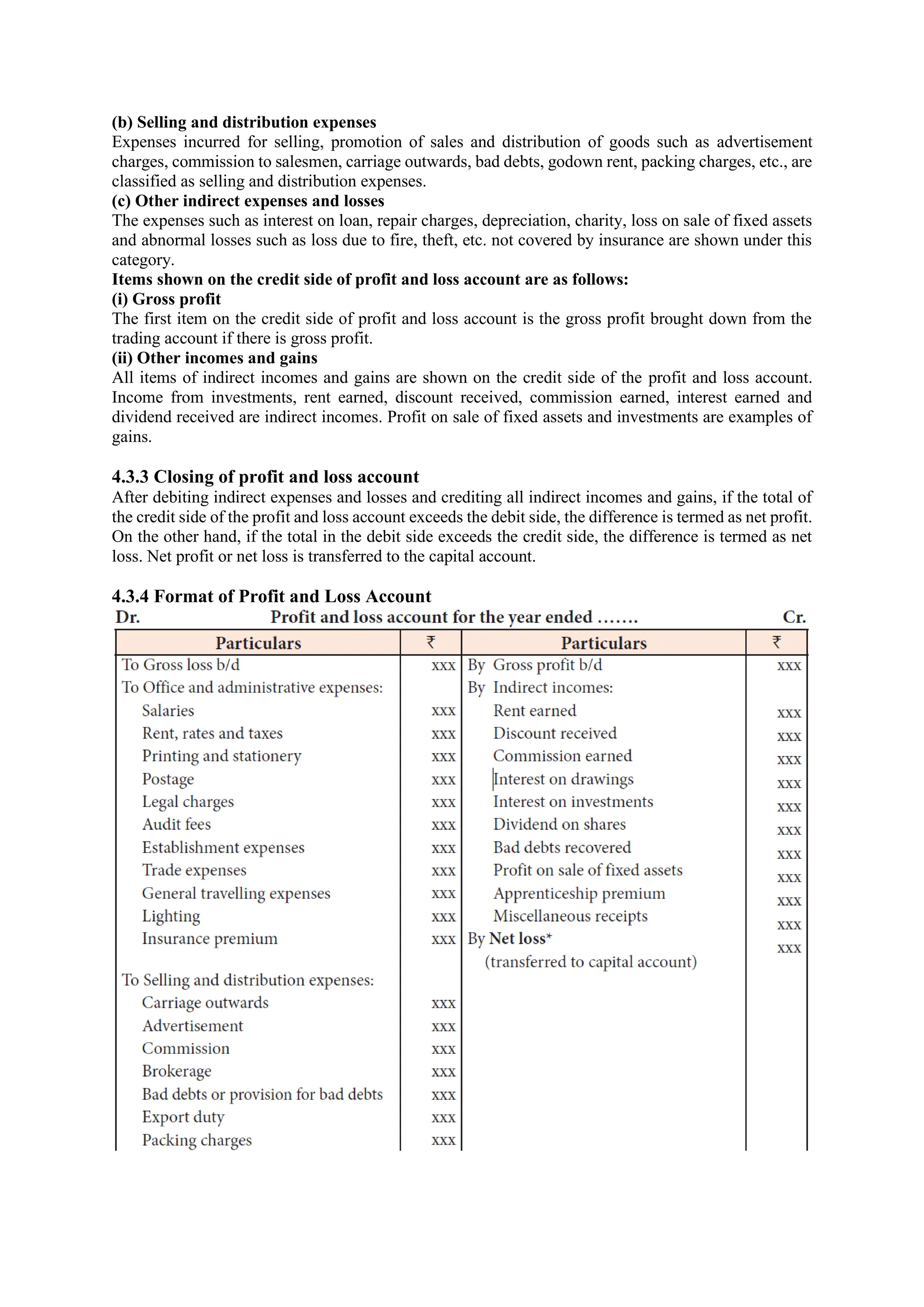

(b) Selling anddistribution expenses

Expenses incurred for selling, promotion of sales and distribution of goods such as advertisement

charges, commission to salesmen, carriage outwards, bad debts, godown rent, packing charges, etc., are

classified as selling and distribution expenses.

(c) Other indirect expenses and losses

The expenses such as interest on loan, repair charges, depreciation, charity, loss on sale of fixed assets

and abnormal losses such as loss due to fire, theft, etc. not covered by insurance are shown under this

category.

Items shown on the credit side of profit and loss account are as follows:

(i) Gross profit

The first item on the credit side of profit and loss account is the gross profit brought down from the

trading account if there is gross profit.

(ii) Other incomes and gains

All items of indirect incomes and gains are shown on the credit side of the profit and loss account.

Income from investments, rent earned, discount received, commission earned, interest earned and

dividend received are indirect incomes. Profit on sale of fixed assets and investments are examples of

gains.

4.3.3 Closing of profit and loss account

After debiting indirect expenses and losses and crediting all indirect incomes and gains, if the total of

the credit side of the profit and loss account exceeds the debit side, the difference is termed as net profit.

On the other hand, if the total in the debit side exceeds the credit side, the difference is termed as net

loss. Net profit or net loss is transferred to the capital account.

4.3.4 Format of Profit and Loss Account

9.

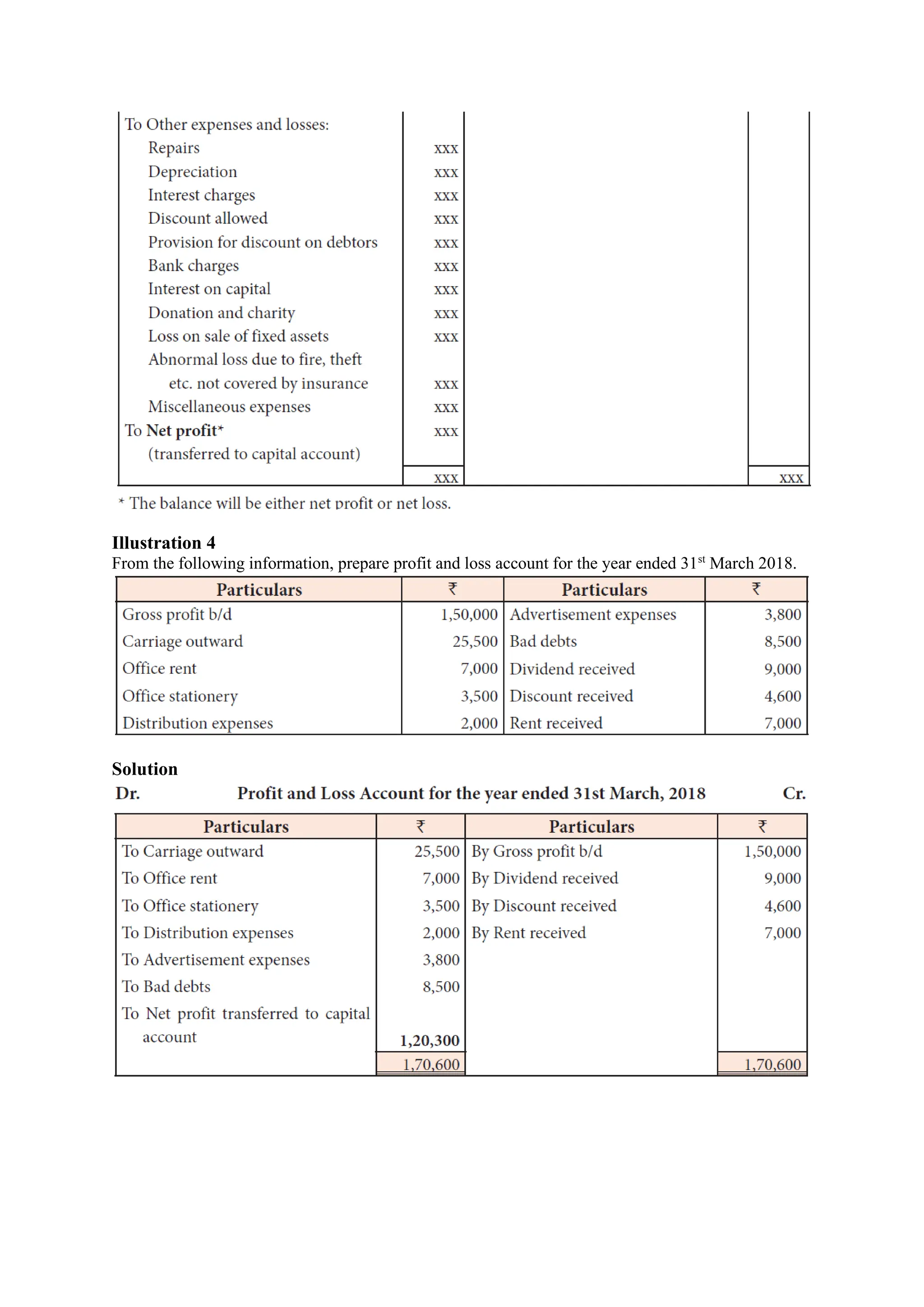

Illustration 4

From thefollowing information, prepare profit and loss account for the year ended 31st

March 2018.

Solution

10.

Illustration 5

From thefollowing information, prepare profit and loss account for the year ended 31st

December 2017.

Solution

Note: Carriage inwards will not appear in profit and loss account as it is a direct expense.

Classwork

Problem 2

Sh. Sunder Lal is a proprietor of a business. The following are the extracts from his trial balance. Prepare

profit and loss account of the year ending 31st

March 2022.

Particulars Amt. (₹) Particulars Amt. (₹)

Interest (Dr.) 570 Bad debts 770

Salaries 14,690 Interest on investment 240

Stationery & Printing 2,310 Rent 2,340

Audit fees 1,590 Depreciation 490

General expenses 670 Gross profit 40,770

Commission received 1,230

[Answer: To Net Profit (b/f): 18,810]

11.

Problem 3

From thefollowing information, prepare Trading and Profit and Loss Account for the year ending 31st

March 2023.

Particulars Amt. (₹) Particulars Amt. (₹)

Salaries 2,000 Purchases 23,000

Wages 7,000 Stock (1.4.2022) 11,000

Carriage 3,400 Factory rent 4,000

Bad debts 700 Audit fees 3,200

Plant & Machinery 46,000 Depreciation 6,200

Sales 55,000 Freight 700

Drawings 3,000 Sales return 900

Return outwards 500 Land and Building 70,000

Closing Stock is valued at ₹19,000

[Answer: To Gross Profit b/d ₹24,500; To Net Profit ₹12,400]

Self-Assessment

Q. No. 2

From the following information, prepare profit and loss account for the year ending 31st December

2021.

[Answer: Net Loss ₹1,02,000]

Q. No. 3

From the following balances obtained from the books of Mr. Ganesh, prepare trading and profit and

loss account.

Closing stock on December 31.12.2017 was ₹4,500

[Answer: Gross profit: ₹14,000; Net profit: ₹4,200]

4.4 Balance sheet

Balance sheet is a statement which gives the position of assets and liabilities on a particular date. Assets

are the resources owned by the business. Liabilities are the claims against the business. After

ascertaining the net profit or net loss of the business enterprise, a businessperson would like to know

the financial position of the business. For this purpose, balance sheet is prepared which contains

amounts of all the assets and liabilities of the business enterprise as on a particular date. The statement

so prepared is called ‘balance sheet’ because it gives the balances of ledger accounts which are still

12.

there, after theclosure of all nominal accounts by transferring to the trading and profit and loss account.

Balances of all the personal and real accounts are grouped into assets and liabilities. In the balance

sheet, liabilities are shown on the left-hand side and assets on the right-hand side.

According to J.R. Batliboi, “A Balance Sheet is a statement prepared with a view to measure the exact

financial position of a business on a certain fixed date.”

4.4.1 Need for preparing a balance sheet

The purposes of preparing a balance sheet are as follows:

a) The main purpose of preparing a balance sheet is to ascertain the true financial position of the

business at a particular point of time.

b) It helps in comparing the cost of various assets of the business such as the amount of closing

stock, amount due from debtors, amount of fictitious assets, etc. Moreover, as assets and liabilities

of similar nature are grouped and presented in balance sheet, a comparative study of these assets

and liabilities is facilitated. It helps in comparing the various liabilities of the business.

c) It helps in finding out the solvency position of the firm. The firm’s solvency position is favourable

if the assets exceed the external liabilities. The firm’s solvency position is not favourable it the

external liabilities exceed the assets.

4.4.2 Characteristics of balance sheet

The following are the characteristics of a balance sheet:

a) A balance sheet is a part of the final accounts. However, the balance sheet is a statement and not

an account. It has no debit or credit sides and as such the words ‘To’ and ‘By’ are not used before

the names of the accounts shown therein.

b) A balance sheet is a summary of the personal and real accounts, which have balances. Personal

and real accounts having debit balances are shown on the right-hand side known as assets side,

whereas personal and real accounts having credit balances are shown on the left hand side known

as liabilities side.

c) The totals of the two sides of the balance sheet must be equal. If the totals are not equal, it indicates

existence of error. It must satisfy the accounting equation, ie., Assets = Capital + Liabilities,

following the dual aspect concept.

d) Balance sheet is prepared on a particular date and not for a fixed period. It discloses the financial

position of a business on a particular date. It gives the balances only for the date on which it is

prepared.

e) It shows the financial position of the business according to the going concern concept.

4.4.3 Grouping and Marshalling of assets and liabilities in a balance sheet

The assets and liabilities shown in the balance sheet are grouped and presented in a particular order.

The term ‘grouping’ means showing the items of similar nature under a common heading. For example,

the amount due from various customers will be shown under the head ‘Sundry debtors.’ Similarly, under

the head ‘Current assets’, the balance of cash, bank, debtors, stock and other current assets will be

shown.

‘Marshalling’ is the arrangement of various assets and liabilities in a proper order. Marshalling can be

made in one of the following two ways:

(a) In the order of liquidity

According to this method, an asset which is most easily convertible into cash, i.e., cash in hand is shown

first and then will follow those assets which are comparatively less easily convertible, so that the least

liquid asset i.e., goodwill is shown last. In the same way, the liabilities which are to be paid at the

earliest will be shown first. In other words, current liabilities are shown first, then fixed or long-term

liabilities and finally the proprietor’s capital.

(b) In the order of permanence

This method is exactly the reverse of the first method. Asset, which is more permanent, i.e., goodwill

is shown first followed by assets which are less permanent. Similarly, those liabilities which are to be

paid last will be shown first. In other words, the proprietor’s capital is shown first, then fixed or long-

term liabilities and lastly the current liabilities. Joint stock companies are required under the Companies

Act to prepare their balance sheet in the order of permanence.

13.

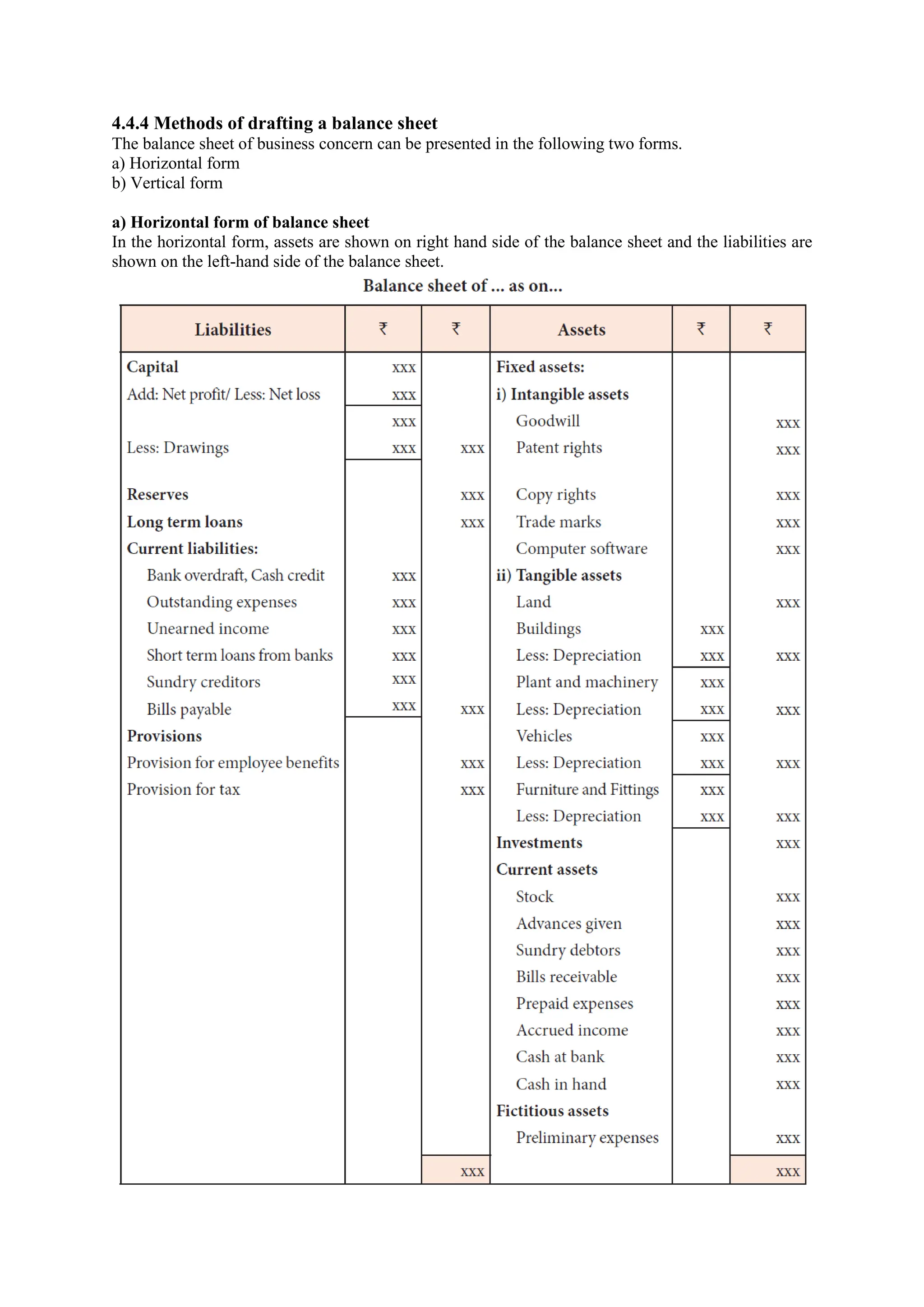

4.4.4 Methods ofdrafting a balance sheet

The balance sheet of business concern can be presented in the following two forms.

a) Horizontal form

b) Vertical form

a) Horizontal form of balance sheet

In the horizontal form, assets are shown on right hand side of the balance sheet and the liabilities are

shown on the left-hand side of the balance sheet.

14.

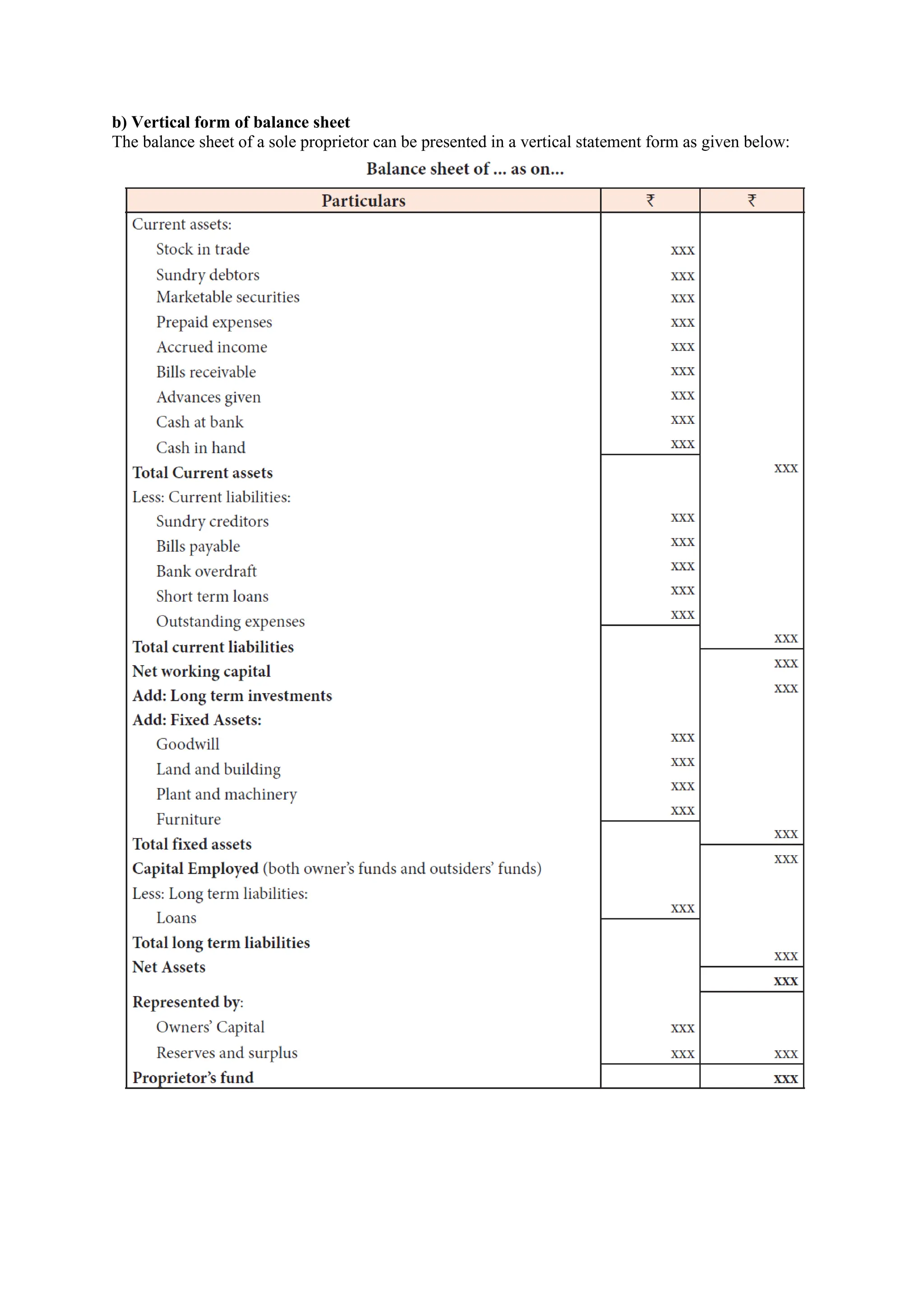

b) Vertical formof balance sheet

The balance sheet of a sole proprietor can be presented in a vertical statement form as given below:

15.

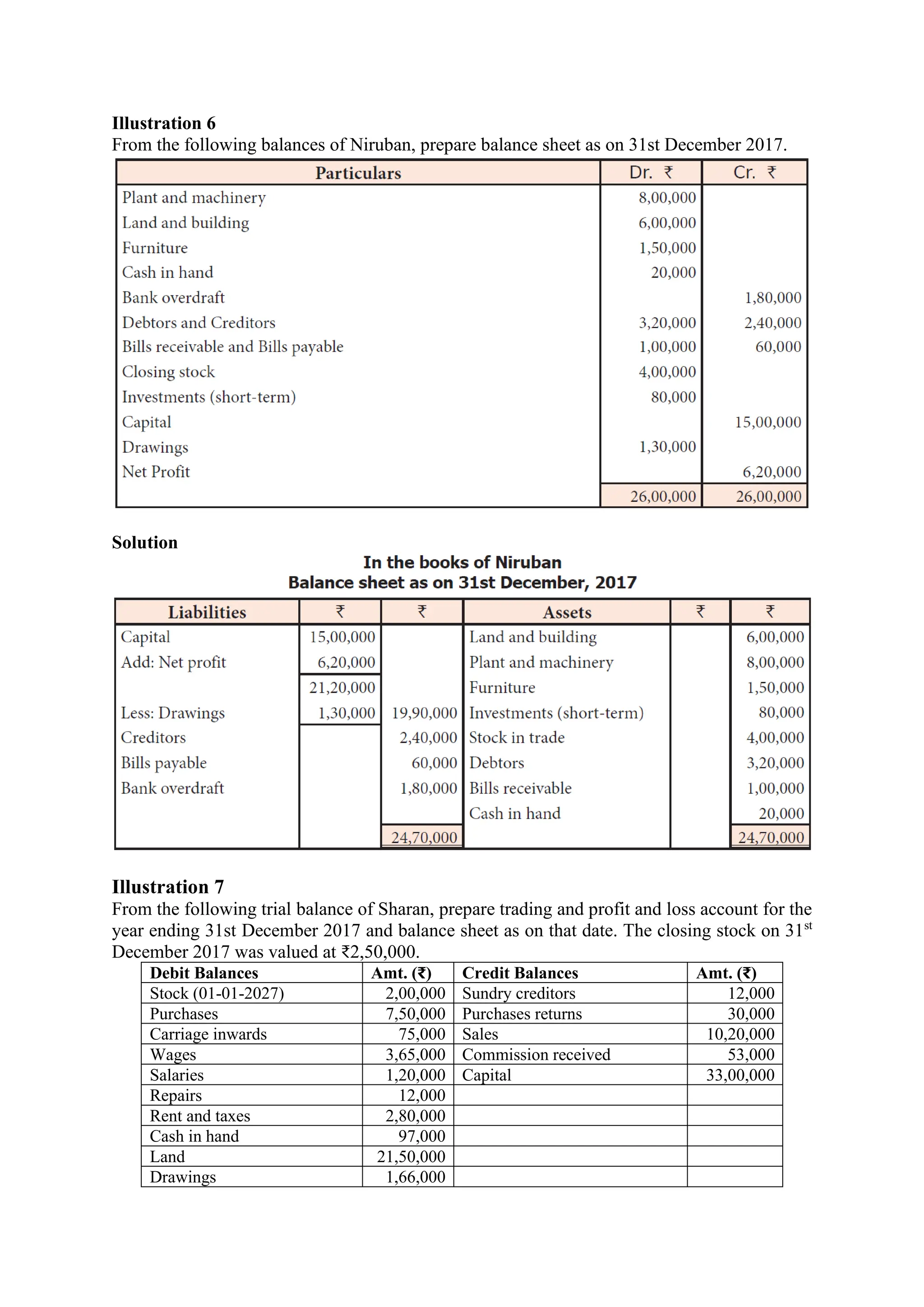

Illustration 6

From thefollowing balances of Niruban, prepare balance sheet as on 31st December 2017.

Solution

Illustration 7

From the following trial balance of Sharan, prepare trading and profit and loss account for the

year ending 31st December 2017 and balance sheet as on that date. The closing stock on 31st

December 2017 was valued at ₹2,50,000.

Debit Balances Amt. (₹) Credit Balances Amt. (₹)

Stock (01-01-2027) 2,00,000 Sundry creditors 12,000

Purchases 7,50,000 Purchases returns 30,000

Carriage inwards 75,000 Sales 10,20,000

Wages 3,65,000 Commission received 53,000

Salaries 1,20,000 Capital 33,00,000

Repairs 12,000

Rent and taxes 2,80,000

Cash in hand 97,000

Land 21,50,000

Drawings 1,66,000

16.

Bank deposits 2,00,000

44,15,00044,15,000

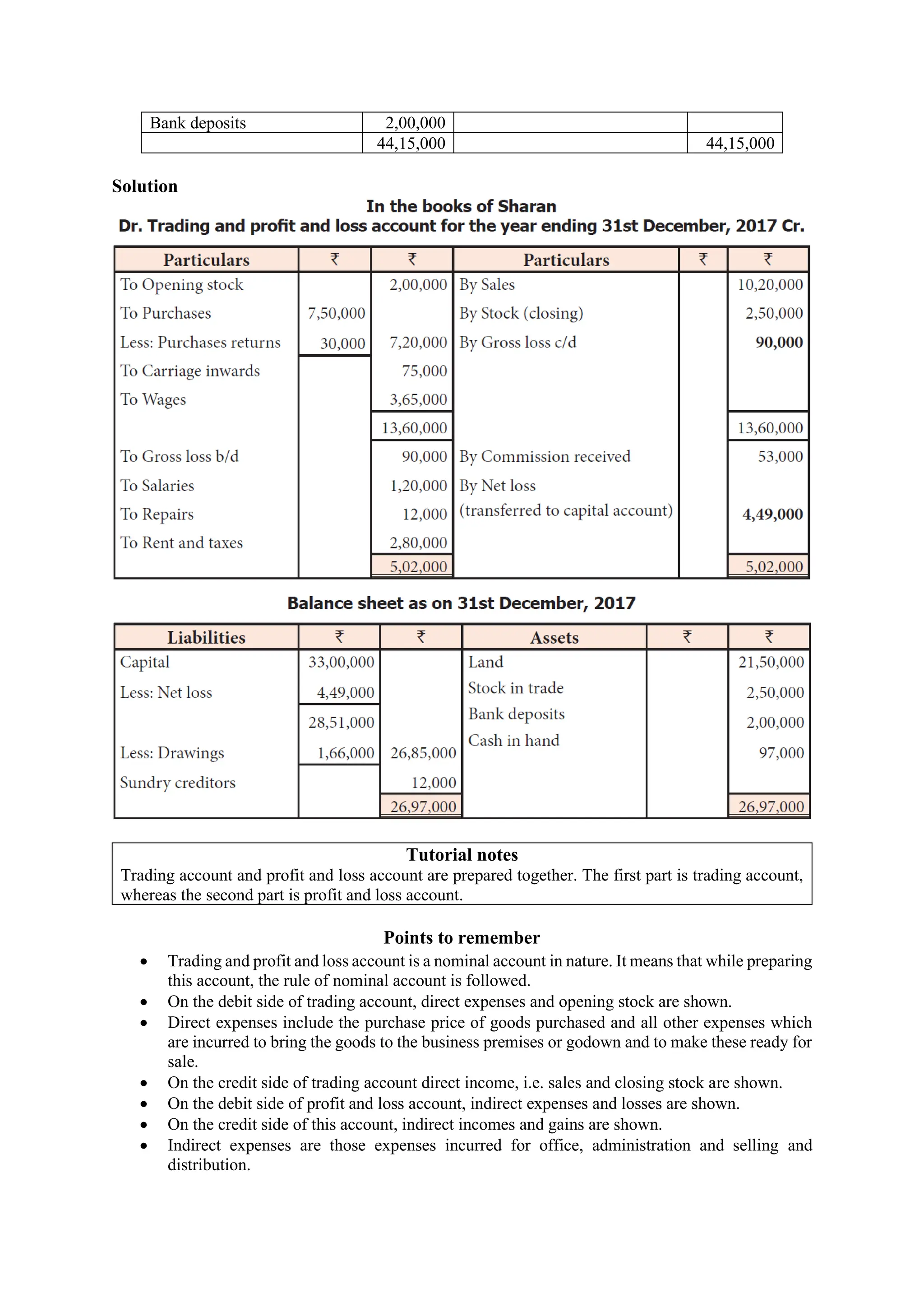

Solution

Tutorial notes

Trading account and profit and loss account are prepared together. The first part is trading account,

whereas the second part is profit and loss account.

Points to remember

• Trading and profit and loss account is a nominal account in nature. It means that while preparing

this account, the rule of nominal account is followed.

• On the debit side of trading account, direct expenses and opening stock are shown.

• Direct expenses include the purchase price of goods purchased and all other expenses which

are incurred to bring the goods to the business premises or godown and to make these ready for

sale.

• On the credit side of trading account direct income, i.e. sales and closing stock are shown.

• On the debit side of profit and loss account, indirect expenses and losses are shown.

• On the credit side of this account, indirect incomes and gains are shown.

• Indirect expenses are those expenses incurred for office, administration and selling and

distribution.

17.

• Indirect incomesand gains are the incomes or gains which are not directly related to the

operation of business enterprise. For example, interest received on the deposits in the bank.

• Balance sheet is a statement and not an account. On the left side liabilities including capital and

on the right side the assets are shown in the balance sheet.

• Assets are the resources owned by a business entity. Liabilities are claims against the business

or the amounts owed by business to outsiders and owners.

Classwork

Problem 4

Complete the following account by filling the amount of missing figures:

Particulars Amount Particulars Amount

To Opening Stock (20% on sales By Sales 5,00,000

To Purchases (300% of opening stock) By Closing Stock

To Wages (2% of sales)

To Factory Expenses (4% of purchases)

To Coal, Gas, and Water

(50% of wages, and factory expenses)

To Freight (10% of closing stock)

To Gross Profit

6,00,000 6,00,000

[Answer: Gross profit: ₹1,57,000]

Problem 5:

From the following Trail Balance prepare Trading and Profit and Loss account for the year ending 31st

March 2024 and a balance sheet as on that date:

Particulars Amt. (₹) Dr. Amt. (₹) Cr.

Purchases 37,500

Stock (opening) 15,000

Drawings 5,500

Returns Inwards 1,350

Trade Expenses 445

Wages 3,500

Salaries 2,800

Travelling Expenses 330

Advertising Expenses 210

Rent, Rates and Insurance 1,400

Bad Debts 200

Discount 150

Premises 3,000

Plant and Machinery 5,000

Fixtures and Fittings 2,500

Sundry Debtors 21,250

Cash in hand 515

Capital 17,500

Sales 62,500

Returns Outwards 650

Creditors 15,000

Bank Overdraft 5,000

1,00,650 1,00,650

Closing Stock was ₹21,000

[Answer: Gross profit: ₹26,800; Net profit: ₹21,265; Balance Sheet Total: ₹53,265]

18.

Problem 6:

From thefollowing Trial Balance extracted from the books of Sh. Golul Nath as on 31st

March, 2023,

prepare Trading and Profit and Loss Account for the year ending and Balance Sheet as on that date.

Debit Balance Amt. (₹) Credit Balance Amt. (₹)

Cash at Bank 1,400 Creditors 68,000

Cash in hand 3,000 Sales 1,46,000

Rent and Rates 1,200 Purchases Returns 2,000

Stock 18,000 Commission Received 4,000

Discount Allowed 400 Capital Account 55,000

Purchases 1,09,000 Rent Received 2,000

Carriage Outwards 3,600

Plant and Machinery 22,000

Returns 6,000

Carriage on Purchases 1,000

Fixture and Fittings 12,000

Audit Fees 3,000

Salaries 6,000

Bills Receivable 12,000

Drawings 12,000

Wages 18,000

Sundry Debtors 40,000

Commission 8,400

2,77,000 2,77,000

Closing Stock: ₹29,000

[Answer: Gross profit: ₹25,000; Net profit: ₹8,400; Balance Sheet Total: ₹1,19,400]

Problem 7:

Sh. Ram Gopal is a sole trader and his trial balance as on 31st

March 2023 is as under:

Particulars Amt. (₹) Dr. Amt. (₹) Cr.

Stock (31-03-2023) 12,000

Account Payable 6,000

Furniture 3,000

Purchases (After adjusting stock) 1,00,000

Returns Inwards 6,000

Salaries 11,000

Cash 1,000

Life Insurance Premium 1,500

Bank (Overdraft) 5,000

Sales 1,70,000

Carriage Inwards 2,500

Returns Outwards 8,000

Investments 15,000

Dividend Received 2,000

Rent 4,400

Commission 2,400

Unproductive Wages 400

Printing and Stationery 1,000

Postage 300

Accounts Receivable 7,000

Royalties 5,000

Bad Debts 800

Rent Received 2,500

19.

Premises 50,000

Insurance 1,800

Drawings14,900

Discount 1,000 3,000

Capital 44,500

2,41,000 2,41,000

You are asked to prepare Trading and Profit and Loss Account for the year ending and Balance Sheet

as on that date.

Hint: - 1. Life Insurance Premium is treated as Drawings

2. Closing Stock is given as balance in the trial balance, so it will be shown in Balance Sheet

only

[Answer: Gross profit: ₹64,500; Net profit: ₹48,900; Balance Sheet Total: ₹88,000]

Self-Assessment

Q. No. 4

From the following balance prepare Trading and Profit and Loss Account for the year ending 31st

March

2023, and Balance sheet as on that date:

Particulars Amt. (₹) Dr. Amt. (₹) Cr.

Purchases 36,000

Stock (01.04.2022) 12,500

Sales 59,000

Sales Returns 1,000

Purchase Returns 1,500

Creditors 5,500

Book-debts 10,300

Furniture 2,500

Freight and Duty 1,000

Carriage Outwards 250

Rent and Insurance 1,750

Advertisement 700

Stationery Expenses 400

Office Expenses 200

Telephone Expenses 400

Bad Debts Recovered 200

General Reserve 300

Salaries 3,650

Productive Wages 7,000

Leasehold Property 12,500

Cash in hand 600

Bank balance 12,750

Capital 45,000

Income Tax 8,000

1,11,500 1,11,500

Closing Stock ₹11,900.

[Answer: Gross profit: ₹14,900; Net profit: ₹7,750; Balance Sheet Total: ₹50,550]

Q. No. 5

Prepare Trading, Profit and Loss Account from the following

Trail Balance

Particulars Amt. (₹) Dr. Amt. (₹) Cr.

David’s Drawings & Capital 5,000 40,000

Leasehold land 25,000

20.

Freehold premises 20,000

Goodwill7,000

Trademark 13,000

Plant and Machinery 15,000

Fixture and Fittings 2,000

Stock at Commencement 18,000

Bills Receivable and Payable 4,000 6,000

Sundry Debtors and Creditors 16,000 24,000

Purchases and Sales 80,000 1,50,000

Returns 1,000 2,000

Carriage in 1,500

Carriage out 500

Fright and duty 1,200

Manufacturing Wages 22,000

Coal, Fuel & Gas 800

Factory Expenses 4,500

Salaries 18,000

Rates and Taxes 6,000

Commission 2,500

Interest 3,000

Discount 6,000

Stationery 4,000

Trading Expenses 500

Cash in hand 1,800

Bank Overdraft 700

2,70,000 2,70,000

Closing Stock at the end of the year ₹20,000

[Answer: Gross profit: ₹43,000; Net profit: ₹18,700; Balance Sheet Total: ₹1,22,700]

4.5 Balance Sheet with Adjustments

4.5.1 Meaning and Need/Importance of Adjustments

In accounting we follow the Accrual Concept, and according to this concept there may be some incomes

and expenses which are still to be brought into the books of accounts. So, it is compulsory to adjust

these items in the Final Accounts, to get the true and fair picture of this business. If there is any item

which is not correctly stated in Trading, Profit & Loss Account or in the Balance Sheet, then these

records will not show the real Profit or Loss and financial position of the business.

Need or Importance of Adjustments

1. To know the actual profits of the business

2. To know the actual financial position of the business

3. To know the actual value of assets and liabilities

4. To record the unrecorded assets and liabilities

5. To record the outstanding expenses and incomes

6. To rectify the errors

7. To make the provision for bad debts, provision for

tax and depreciation

4.5.2 Accounting Treatment of Adjustment Entries

1. Treatment of Opening Stock

Generally opening stock is shown as first item in the

Trading Account (Debit side) when it is given in the trial

balance but sometimes opening stick is given in the

adjustments, in such a case it will not take place in Trading

Opening

Stock

If given in

trail balance

Trading A/c

(Debit Side)

If given in

adjextments

No Use

ignore

21.

Account or BalanceSheet, because it is already adjusted and given in the question only for information

purpose.

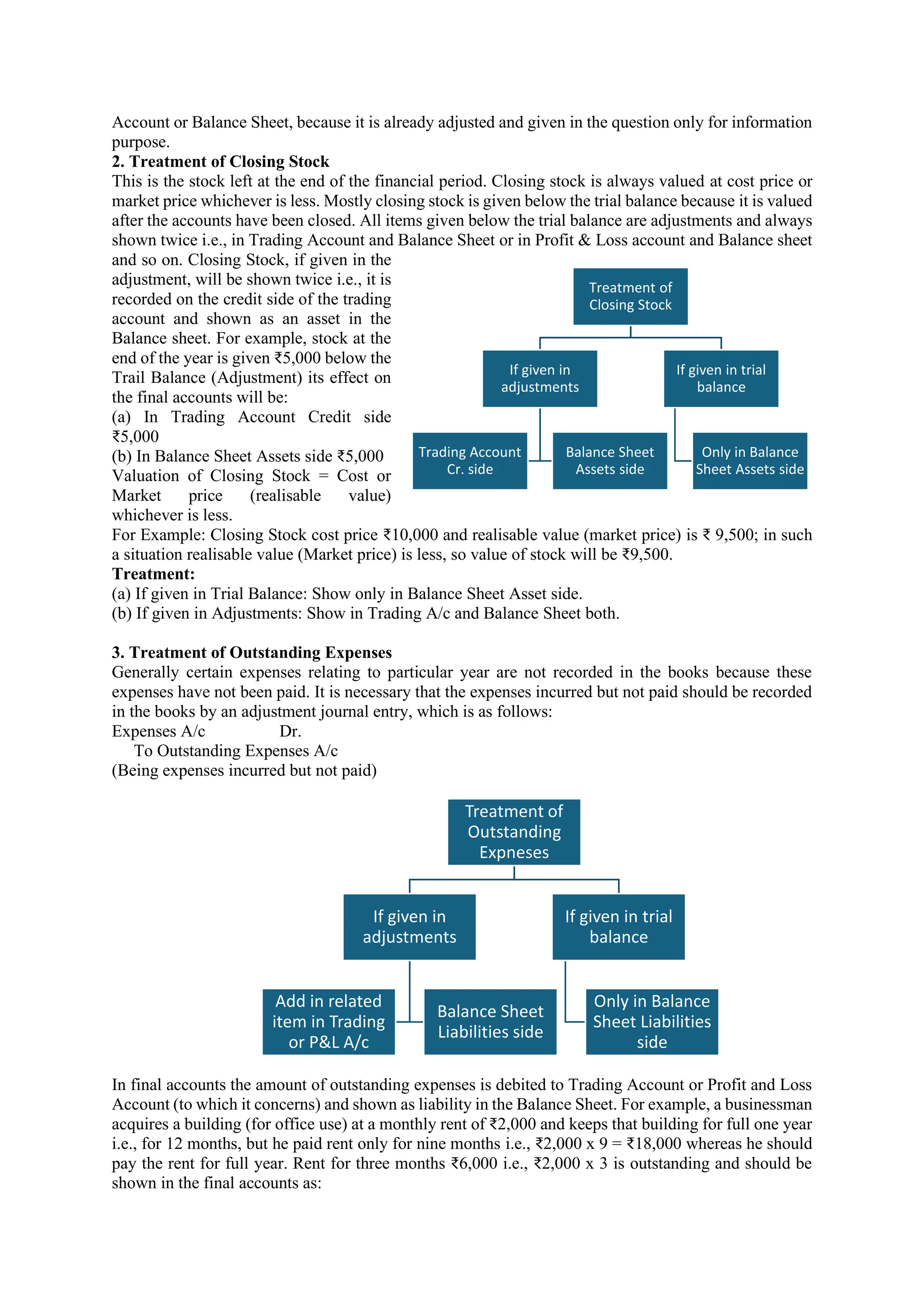

2. Treatment of Closing Stock

This is the stock left at the end of the financial period. Closing stock is always valued at cost price or

market price whichever is less. Mostly closing stock is given below the trial balance because it is valued

after the accounts have been closed. All items given below the trial balance are adjustments and always

shown twice i.e., in Trading Account and Balance Sheet or in Profit & Loss account and Balance sheet

and so on. Closing Stock, if given in the

adjustment, will be shown twice i.e., it is

recorded on the credit side of the trading

account and shown as an asset in the

Balance sheet. For example, stock at the

end of the year is given ₹5,000 below the

Trail Balance (Adjustment) its effect on

the final accounts will be:

(a) In Trading Account Credit side

₹5,000

(b) In Balance Sheet Assets side ₹5,000

Valuation of Closing Stock = Cost or

Market price (realisable value)

whichever is less.

For Example: Closing Stock cost price ₹10,000 and realisable value (market price) is ₹ 9,500; in such

a situation realisable value (Market price) is less, so value of stock will be ₹9,500.

Treatment:

(a) If given in Trial Balance: Show only in Balance Sheet Asset side.

(b) If given in Adjustments: Show in Trading A/c and Balance Sheet both.

3. Treatment of Outstanding Expenses

Generally certain expenses relating to particular year are not recorded in the books because these

expenses have not been paid. It is necessary that the expenses incurred but not paid should be recorded

in the books by an adjustment journal entry, which is as follows:

Expenses A/c Dr.

To Outstanding Expenses A/c

(Being expenses incurred but not paid)

In final accounts the amount of outstanding expenses is debited to Trading Account or Profit and Loss

Account (to which it concerns) and shown as liability in the Balance Sheet. For example, a businessman

acquires a building (for office use) at a monthly rent of ₹2,000 and keeps that building for full one year

i.e., for 12 months, but he paid rent only for nine months i.e., ₹2,000 x 9 = ₹18,000 whereas he should

pay the rent for full year. Rent for three months ₹6,000 i.e., ₹2,000 x 3 is outstanding and should be

shown in the final accounts as:

Treatment of

Closing Stock

If given in

adjustments

Trading Account

Cr. side

Balance Sheet

Assets side

If given in trial

balance

Only in Balance

Sheet Assets side

Treatment of

Outstanding

Expneses

If given in

adjustments

Add in related

item in Trading

or P&L A/c

Balance Sheet

Liabilities side

If given in trial

balance

Only in Balance

Sheet Liabilities

side

22.

Profit and LossAccount

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

To Rent 18,000

Add: Outstanding 6,000 24,000

Balance Sheet

Liabilities Amt. (₹) Assets Amt. (₹)

Outstanding Rent 6,000

If outstanding expenses is given in the trial balance it will be shown as liability in the Balance Sheet

only. Outstanding expenses can be named as expenses due, unpaid, expenses incurred but unpaid etc.,

Treatment:

1. If given in Trial Balance: It will be shown only in liabilities side of Balance Sheet.

2. If given in adjustments:

(i) Add in related item and

(ii) Show in liabilities side of Balance Sheet

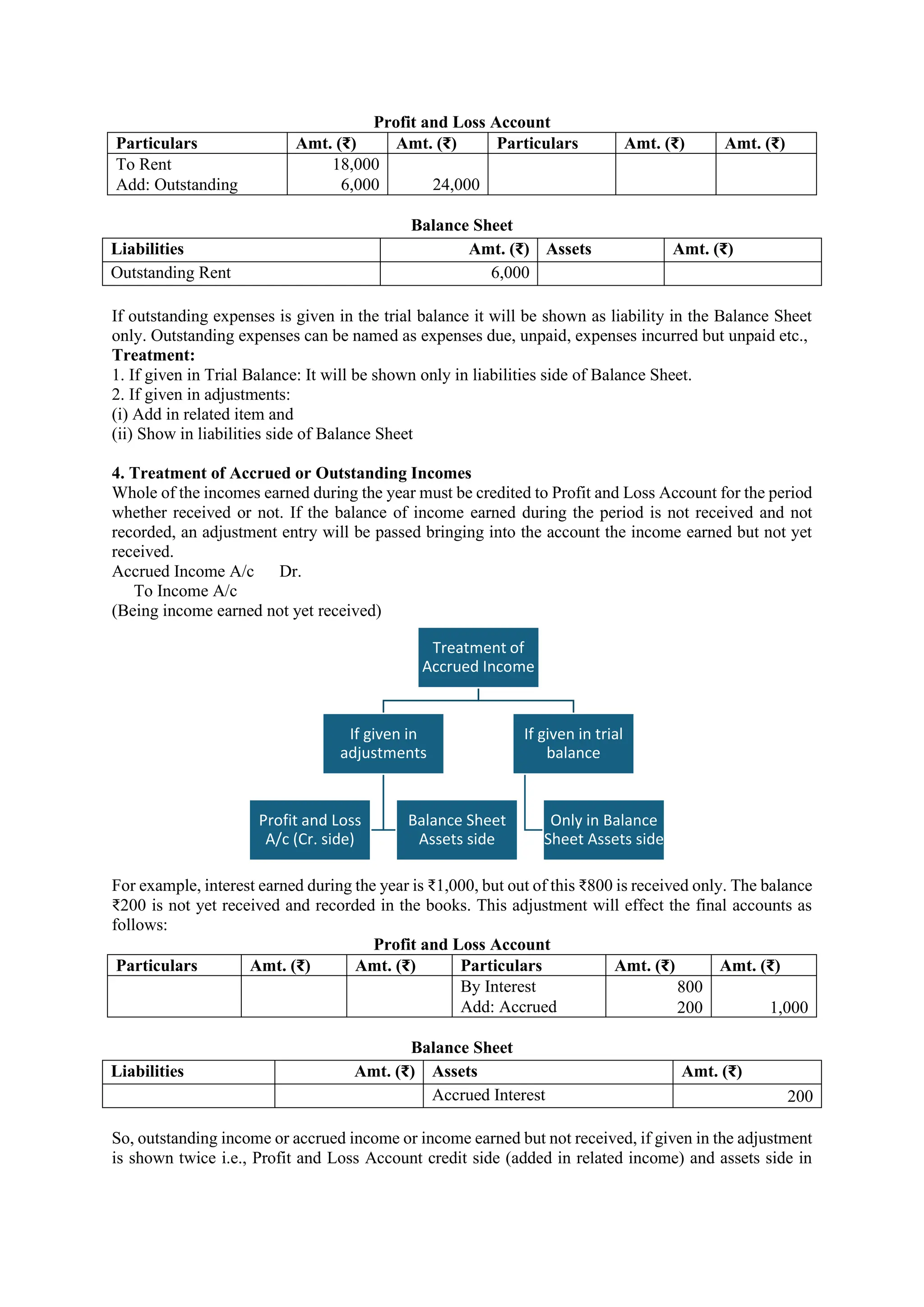

4. Treatment of Accrued or Outstanding Incomes

Whole of the incomes earned during the year must be credited to Profit and Loss Account for the period

whether received or not. If the balance of income earned during the period is not received and not

recorded, an adjustment entry will be passed bringing into the account the income earned but not yet

received.

Accrued Income A/c Dr.

To Income A/c

(Being income earned not yet received)

For example, interest earned during the year is ₹1,000, but out of this ₹800 is received only. The balance

₹200 is not yet received and recorded in the books. This adjustment will effect the final accounts as

follows:

Profit and Loss Account

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

By Interest 800

Add: Accrued 200 1,000

Balance Sheet

Liabilities Amt. (₹) Assets Amt. (₹)

Accrued Interest 200

So, outstanding income or accrued income or income earned but not received, if given in the adjustment

is shown twice i.e., Profit and Loss Account credit side (added in related income) and assets side in

Treatment of

Accrued Income

If given in

adjustments

Profit and Loss

A/c (Cr. side)

Balance Sheet

Assets side

If given in trial

balance

Only in Balance

Sheet Assets side

23.

Balance Sheet. IfAccrued income is given in the trial balance, it will be shown as an asset in the Balance

Sheet only.

Treatment:

1. If given in Trial Balance: Show in Assets side of Balance Sheet only

2. If given in adjustment: 1. Cr. Side of P&L A/c and 2. B/S Assets side.

5. Treatment of Prepaid, Carry Forward or Unexpired Expenses

Expenses paid but not due or expenses paid in advance or pre-paid expenses are those expenses which

are paid during the year but belong to the subsequent year. Expenses related to next year not shown in

the books of this year, but if those are already included in the expenses of current year, then with the

help of following journal entries these will be adjusted:

Prepaid Expenses A/c Dr.

To Expenses A/c

(Being prepaid expenses adjusted)

For example, a trader’s financial year is from 1st

April 2019 to 31st

March 2020. He paid for insurance

₹400 for one year on 1st

July 2019. As the insurance is paid for one year, it expires on 30th

June 2020,

but the accounting year ends on 31st

March 2020 so for the 3 months i.e., 1st

July 2019 to 30th

June 2020

it is paid in advance i.e., ₹100 (for 3 months only). It will effect the final accounts as follows:

Profit and Loss Account

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

To Insurance Premium 400

Less: Paid in Advance 100 300

Balance Sheet

Liabilities Amt. (₹) Assets Amt. (₹)

Insurance Premium paid in advance 100

Treatment:

1. If given in Trial Balance: Show asset side of Balance Sheet only.

2. If given in adjustment: 1. Less from related item in Trading or P&L A/c; 2. Asset side of B/S.

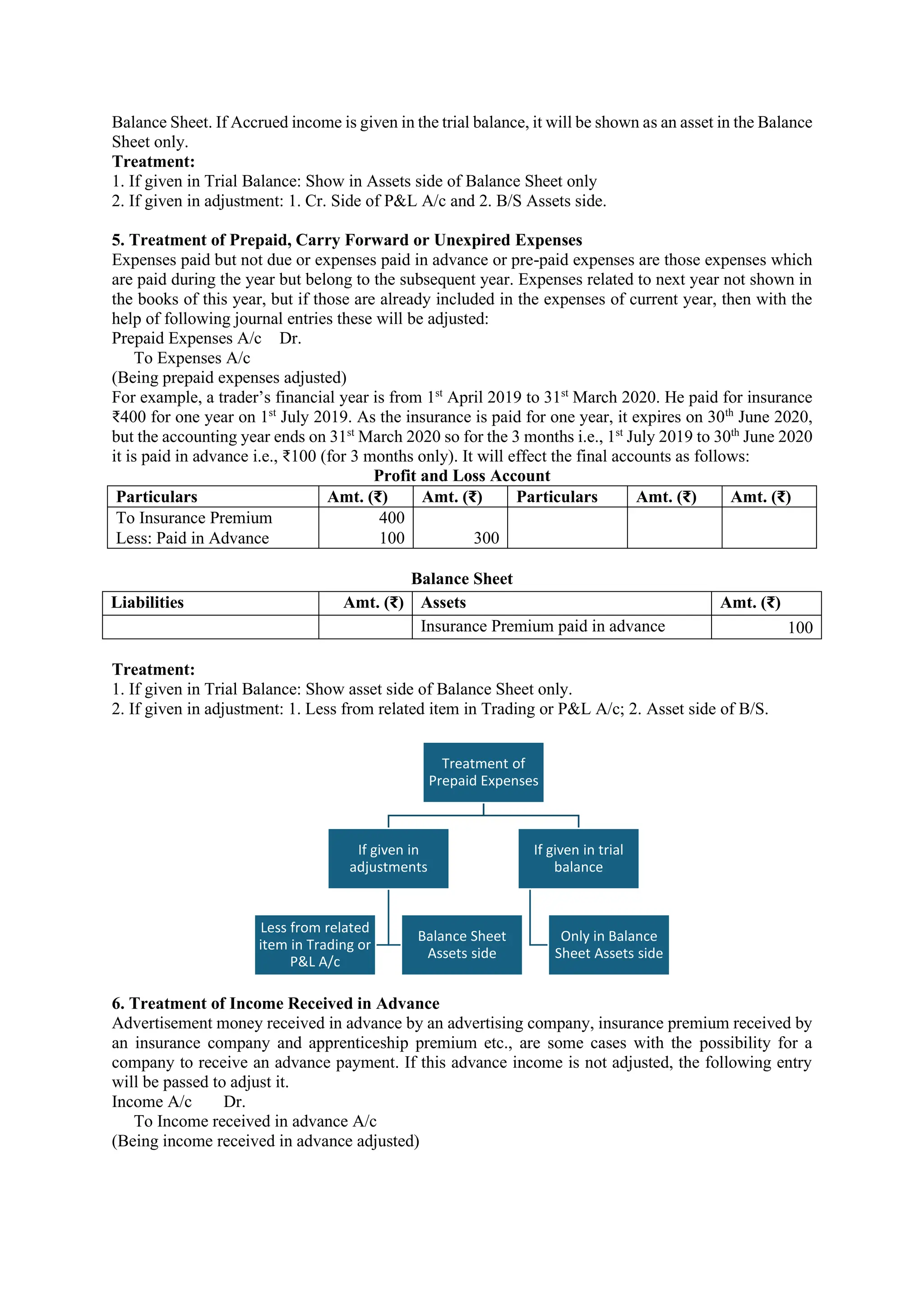

6. Treatment of Income Received in Advance

Advertisement money received in advance by an advertising company, insurance premium received by

an insurance company and apprenticeship premium etc., are some cases with the possibility for a

company to receive an advance payment. If this advance income is not adjusted, the following entry

will be passed to adjust it.

Income A/c Dr.

To Income received in advance A/c

(Being income received in advance adjusted)

Treatment of

Prepaid Expenses

If given in

adjustments

Less from related

item in Trading or

P&L A/c

Balance Sheet

Assets side

If given in trial

balance

Only in Balance

Sheet Assets side

24.

This income (receivedin advance) when given as adjustment, it will be deducted from particular income

in P&L A/c and shown as liability in the Balance Sheet. If advance income is given in the Trial Balance,

it will be shown as liability in the balance sheet.

Treatment:

1. If given in Trial Balance: Show in Liabilities side of Balance Sheet only.

2. If given in adjustment: 1. Deduct from related item and 2. Show on the liabilities side of B/S.

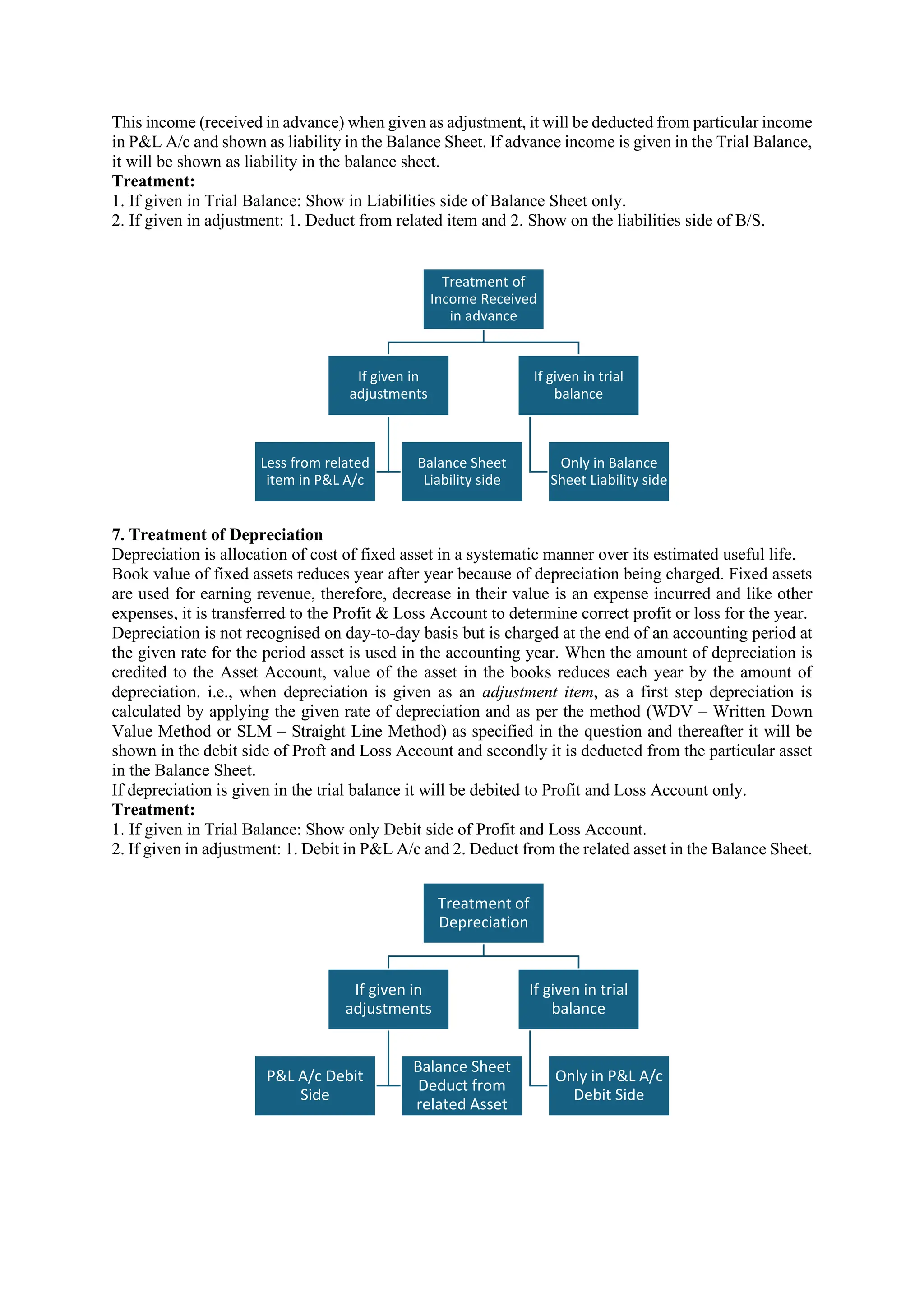

7. Treatment of Depreciation

Depreciation is allocation of cost of fixed asset in a systematic manner over its estimated useful life.

Book value of fixed assets reduces year after year because of depreciation being charged. Fixed assets

are used for earning revenue, therefore, decrease in their value is an expense incurred and like other

expenses, it is transferred to the Profit & Loss Account to determine correct profit or loss for the year.

Depreciation is not recognised on day-to-day basis but is charged at the end of an accounting period at

the given rate for the period asset is used in the accounting year. When the amount of depreciation is

credited to the Asset Account, value of the asset in the books reduces each year by the amount of

depreciation. i.e., when depreciation is given as an adjustment item, as a first step depreciation is

calculated by applying the given rate of depreciation and as per the method (WDV – Written Down

Value Method or SLM – Straight Line Method) as specified in the question and thereafter it will be

shown in the debit side of Proft and Loss Account and secondly it is deducted from the particular asset

in the Balance Sheet.

If depreciation is given in the trial balance it will be debited to Profit and Loss Account only.

Treatment:

1. If given in Trial Balance: Show only Debit side of Profit and Loss Account.

2. If given in adjustment: 1. Debit in P&L A/c and 2. Deduct from the related asset in the Balance Sheet.

Treatment of

Income Received

in advance

If given in

adjustments

Less from related

item in P&L A/c

Balance Sheet

Liability side

If given in trial

balance

Only in Balance

Sheet Liability side

Treatment of

Depreciation

If given in

adjustments

P&L A/c Debit

Side

Balance Sheet

Deduct from

related Asset

If given in trial

balance

Only in P&L A/c

Debit Side

25.

Note:

1. If itis instructed to charge depreciation @10% then the depreciation is calculated ignoring time

factor. But if it is instructed to charge depreciation @10% p.a. then depreciation is calculated

with the time factor into consideration.

Example: Plant costing ₹2,00,000 and accounts are prepared for 6 months then the depreciation

will be:

a. ₹20,000 if the rate of depreciation is 10% and

b. ₹10,000 if the rate of depreciation is 10% p.a.

2. It is better to ignore depreciation on sale of assets if the date of transaction is not given.

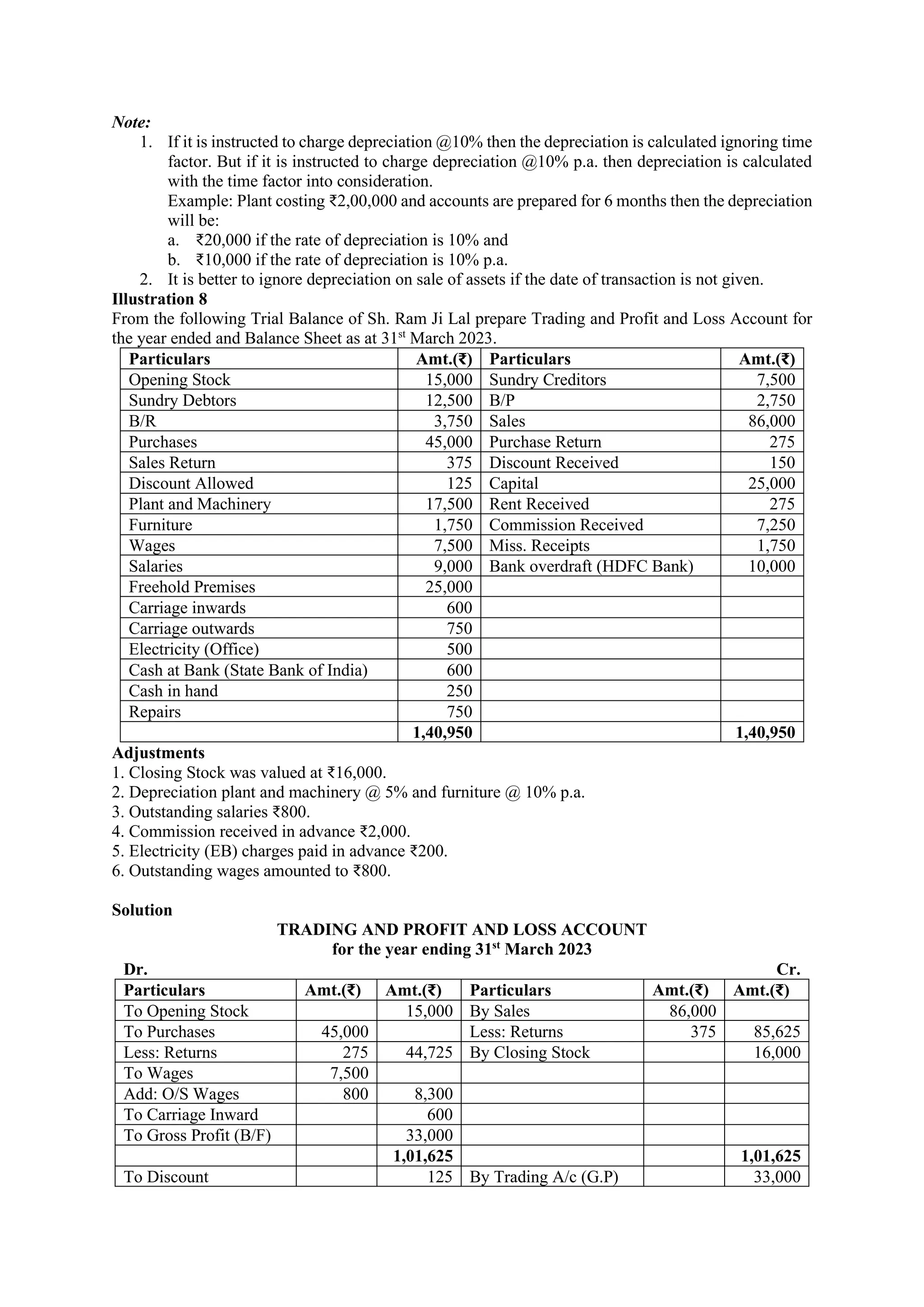

Illustration 8

From the following Trial Balance of Sh. Ram Ji Lal prepare Trading and Profit and Loss Account for

the year ended and Balance Sheet as at 31st

March 2023.

Particulars Amt.(₹) Particulars Amt.(₹)

Opening Stock 15,000 Sundry Creditors 7,500

Sundry Debtors 12,500 B/P 2,750

B/R 3,750 Sales 86,000

Purchases 45,000 Purchase Return 275

Sales Return 375 Discount Received 150

Discount Allowed 125 Capital 25,000

Plant and Machinery 17,500 Rent Received 275

Furniture 1,750 Commission Received 7,250

Wages 7,500 Miss. Receipts 1,750

Salaries 9,000 Bank overdraft (HDFC Bank) 10,000

Freehold Premises 25,000

Carriage inwards 600

Carriage outwards 750

Electricity (Office) 500

Cash at Bank (State Bank of India) 600

Cash in hand 250

Repairs 750

1,40,950 1,40,950

Adjustments

1. Closing Stock was valued at ₹16,000.

2. Depreciation plant and machinery @ 5% and furniture @ 10% p.a.

3. Outstanding salaries ₹800.

4. Commission received in advance ₹2,000.

5. Electricity (EB) charges paid in advance ₹200.

6. Outstanding wages amounted to ₹800.

Solution

TRADING AND PROFIT AND LOSS ACCOUNT

for the year ending 31st

March 2023

Dr. Cr.

Particulars Amt.(₹) Amt.(₹) Particulars Amt.(₹) Amt.(₹)

To Opening Stock 15,000 By Sales 86,000

To Purchases 45,000 Less: Returns 375 85,625

Less: Returns 275 44,725 By Closing Stock 16,000

To Wages 7,500

Add: O/S Wages 800 8,300

To Carriage Inward 600

To Gross Profit (B/F) 33,000

1,01,625 1,01,625

To Discount 125 By Trading A/c (G.P) 33,000

26.

To Salaries 9,000By Discount 150

Add: O/S Salaries 800 9,800 By Rent 275

To Electricity 500 By Commission 7,250

Less: Prepaid 200 300 Less: Advance 2,000 5,250

To Carriage outward 750 By Miss. receipts 1,750

To Repairs 750

To Depreciation

Plant & Machinery 875

Furniture 175 1,050

To Net Profit (B/F) 27,650

40,425 40,425

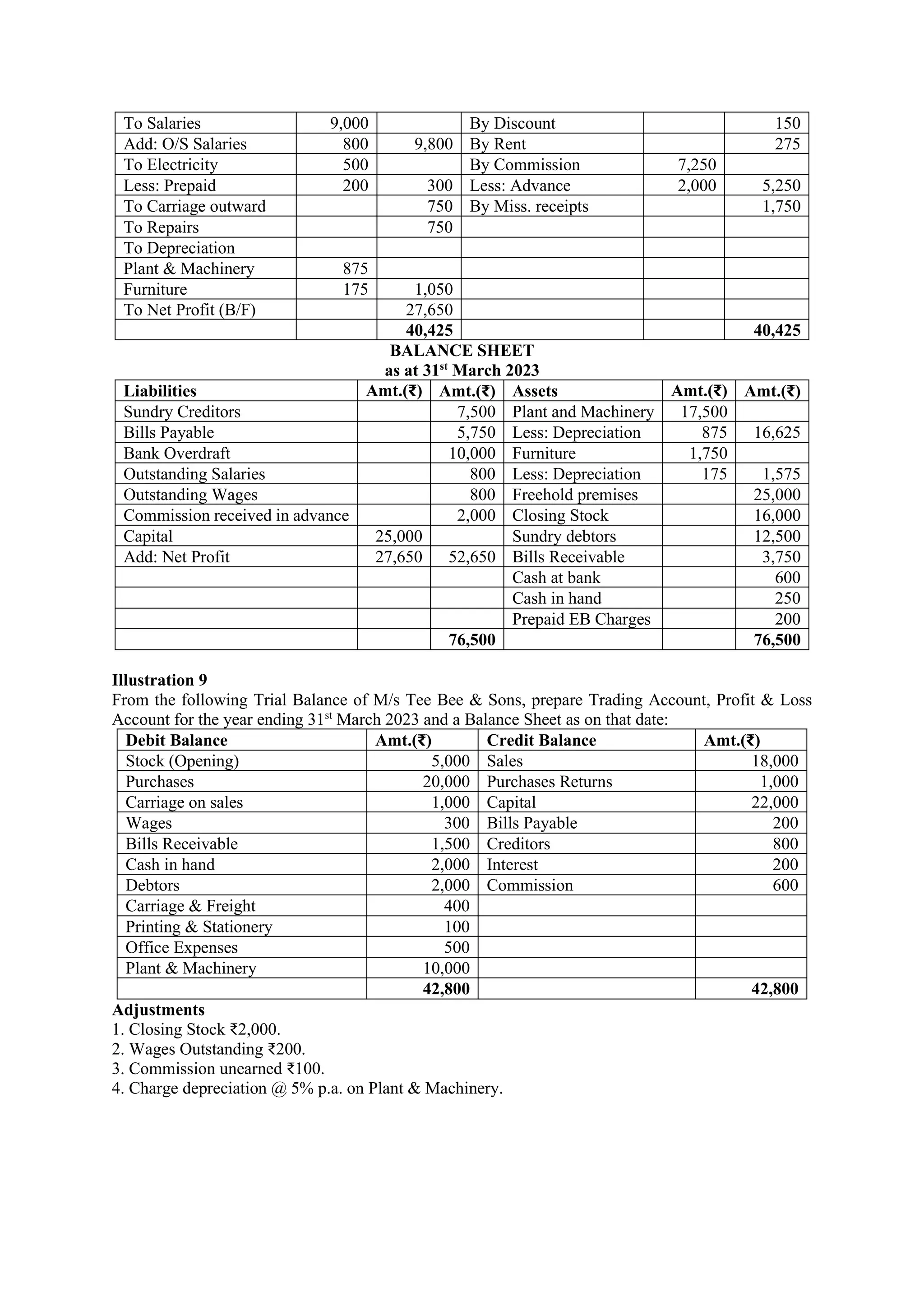

BALANCE SHEET

as at 31st

March 2023

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Sundry Creditors 7,500 Plant and Machinery 17,500

Bills Payable 5,750 Less: Depreciation 875 16,625

Bank Overdraft 10,000 Furniture 1,750

Outstanding Salaries 800 Less: Depreciation 175 1,575

Outstanding Wages 800 Freehold premises 25,000

Commission received in advance 2,000 Closing Stock 16,000

Capital 25,000 Sundry debtors 12,500

Add: Net Profit 27,650 52,650 Bills Receivable 3,750

Cash at bank 600

Cash in hand 250

Prepaid EB Charges 200

76,500 76,500

Illustration 9

From the following Trial Balance of M/s Tee Bee & Sons, prepare Trading Account, Profit & Loss

Account for the year ending 31st

March 2023 and a Balance Sheet as on that date:

Debit Balance Amt.(₹) Credit Balance Amt.(₹)

Stock (Opening) 5,000 Sales 18,000

Purchases 20,000 Purchases Returns 1,000

Carriage on sales 1,000 Capital 22,000

Wages 300 Bills Payable 200

Bills Receivable 1,500 Creditors 800

Cash in hand 2,000 Interest 200

Debtors 2,000 Commission 600

Carriage & Freight 400

Printing & Stationery 100

Office Expenses 500

Plant & Machinery 10,000

42,800 42,800

Adjustments

1. Closing Stock ₹2,000.

2. Wages Outstanding ₹200.

3. Commission unearned ₹100.

4. Charge depreciation @ 5% p.a. on Plant & Machinery.

27.

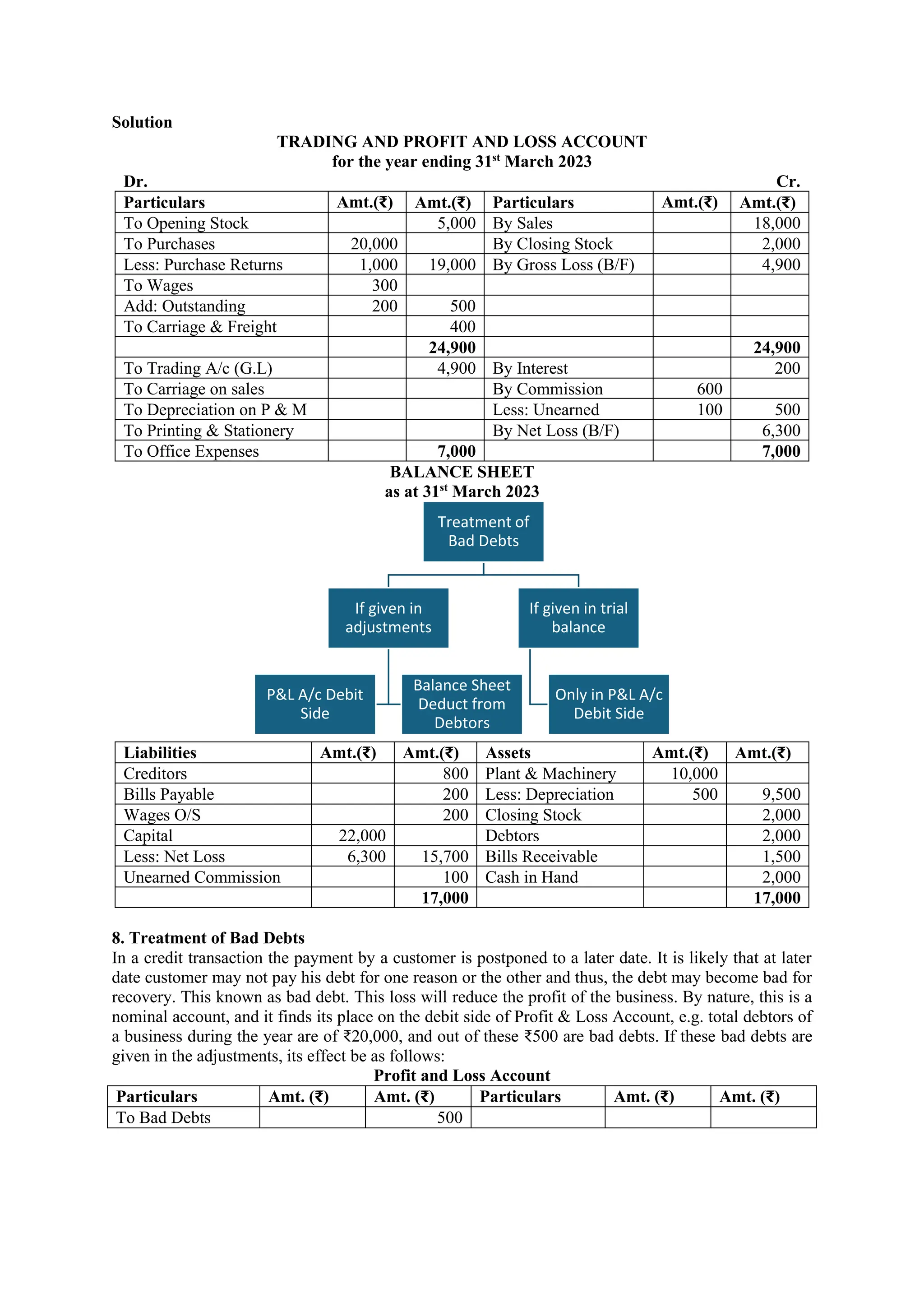

Solution

TRADING AND PROFITAND LOSS ACCOUNT

for the year ending 31st

March 2023

Dr. Cr.

Particulars Amt.(₹) Amt.(₹) Particulars Amt.(₹) Amt.(₹)

To Opening Stock 5,000 By Sales 18,000

To Purchases 20,000 By Closing Stock 2,000

Less: Purchase Returns 1,000 19,000 By Gross Loss (B/F) 4,900

To Wages 300

Add: Outstanding 200 500

To Carriage & Freight 400

24,900 24,900

To Trading A/c (G.L) 4,900 By Interest 200

To Carriage on sales By Commission 600

To Depreciation on P & M Less: Unearned 100 500

To Printing & Stationery By Net Loss (B/F) 6,300

To Office Expenses 7,000 7,000

BALANCE SHEET

as at 31st

March 2023

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Creditors 800 Plant & Machinery 10,000

Bills Payable 200 Less: Depreciation 500 9,500

Wages O/S 200 Closing Stock 2,000

Capital 22,000 Debtors 2,000

Less: Net Loss 6,300 15,700 Bills Receivable 1,500

Unearned Commission 100 Cash in Hand 2,000

17,000 17,000

8. Treatment of Bad Debts

In a credit transaction the payment by a customer is postponed to a later date. It is likely that at later

date customer may not pay his debt for one reason or the other and thus, the debt may become bad for

recovery. This known as bad debt. This loss will reduce the profit of the business. By nature, this is a

nominal account, and it finds its place on the debit side of Profit & Loss Account, e.g. total debtors of

a business during the year are of ₹20,000, and out of these ₹500 are bad debts. If these bad debts are

given in the adjustments, its effect be as follows:

Profit and Loss Account

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

To Bad Debts 500

Treatment of

Bad Debts

If given in

adjustments

P&L A/c Debit

Side

Balance Sheet

Deduct from

Debtors

If given in trial

balance

Only in P&L A/c

Debit Side

28.

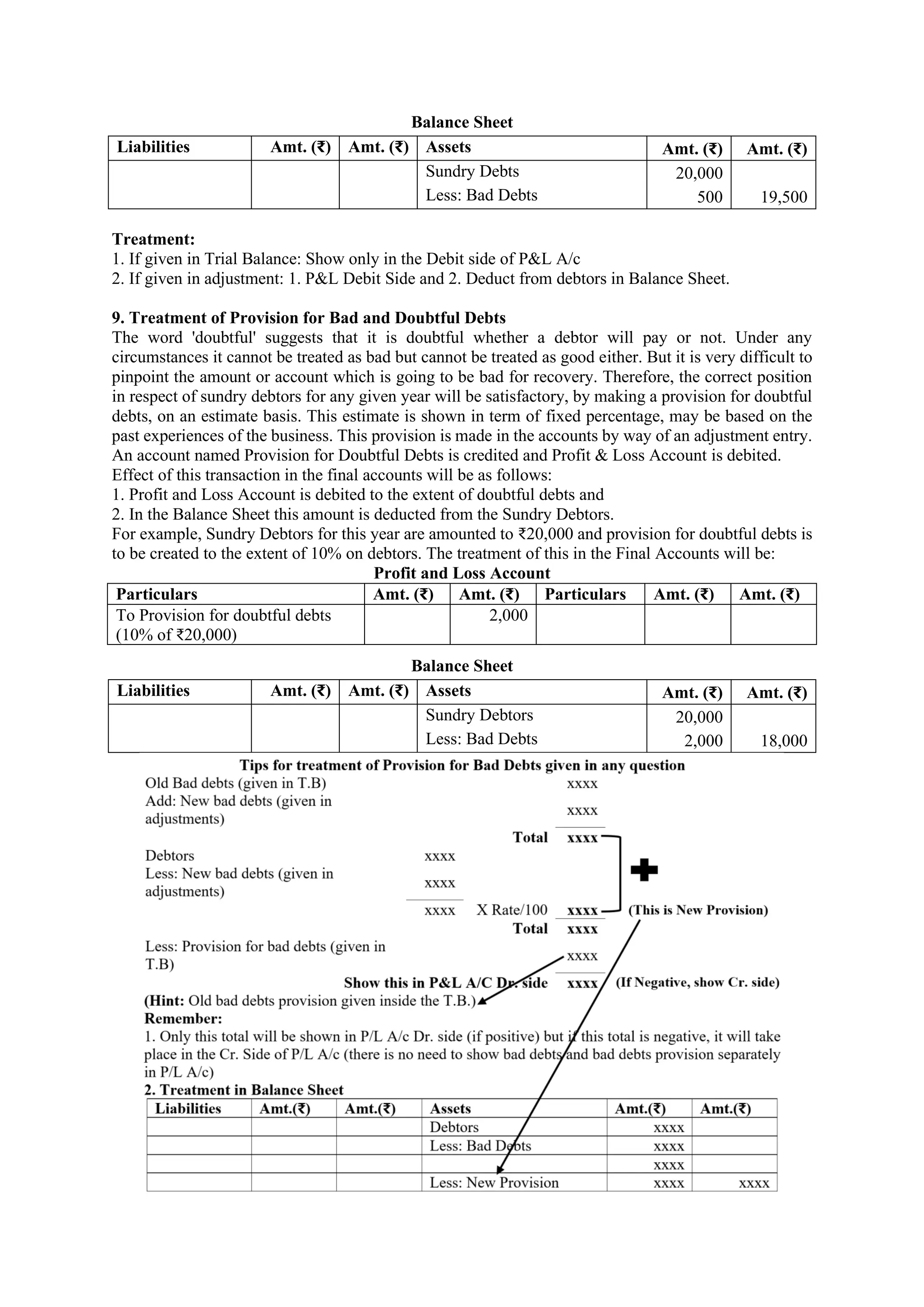

Balance Sheet

Liabilities Amt.(₹) Amt. (₹) Assets Amt. (₹) Amt. (₹)

Sundry Debts 20,000

Less: Bad Debts 500 19,500

Treatment:

1. If given in Trial Balance: Show only in the Debit side of P&L A/c

2. If given in adjustment: 1. P&L Debit Side and 2. Deduct from debtors in Balance Sheet.

9. Treatment of Provision for Bad and Doubtful Debts

The word 'doubtful' suggests that it is doubtful whether a debtor will pay or not. Under any

circumstances it cannot be treated as bad but cannot be treated as good either. But it is very difficult to

pinpoint the amount or account which is going to be bad for recovery. Therefore, the correct position

in respect of sundry debtors for any given year will be satisfactory, by making a provision for doubtful

debts, on an estimate basis. This estimate is shown in term of fixed percentage, may be based on the

past experiences of the business. This provision is made in the accounts by way of an adjustment entry.

An account named Provision for Doubtful Debts is credited and Profit & Loss Account is debited.

Effect of this transaction in the final accounts will be as follows:

1. Profit and Loss Account is debited to the extent of doubtful debts and

2. In the Balance Sheet this amount is deducted from the Sundry Debtors.

For example, Sundry Debtors for this year are amounted to ₹20,000 and provision for doubtful debts is

to be created to the extent of 10% on debtors. The treatment of this in the Final Accounts will be:

Profit and Loss Account

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

To Provision for doubtful debts

(10% of ₹20,000)

2,000

Balance Sheet

Liabilities Amt. (₹) Amt. (₹) Assets Amt. (₹) Amt. (₹)

Sundry Debtors 20,000

Less: Bad Debts 2,000 18,000

29.

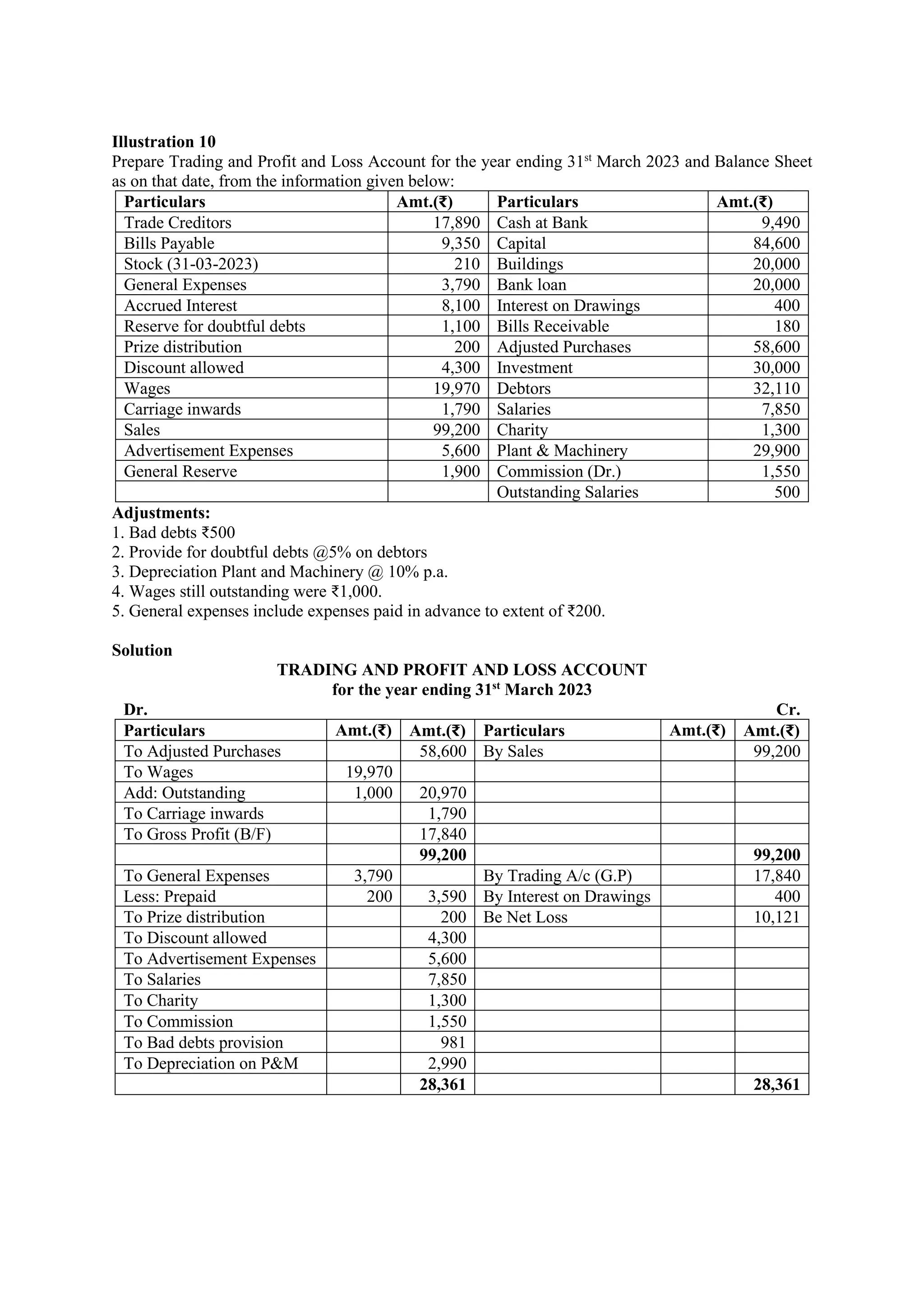

Illustration 10

Prepare Tradingand Profit and Loss Account for the year ending 31st

March 2023 and Balance Sheet

as on that date, from the information given below:

Particulars Amt.(₹) Particulars Amt.(₹)

Trade Creditors 17,890 Cash at Bank 9,490

Bills Payable 9,350 Capital 84,600

Stock (31-03-2023) 210 Buildings 20,000

General Expenses 3,790 Bank loan 20,000

Accrued Interest 8,100 Interest on Drawings 400

Reserve for doubtful debts 1,100 Bills Receivable 180

Prize distribution 200 Adjusted Purchases 58,600

Discount allowed 4,300 Investment 30,000

Wages 19,970 Debtors 32,110

Carriage inwards 1,790 Salaries 7,850

Sales 99,200 Charity 1,300

Advertisement Expenses 5,600 Plant & Machinery 29,900

General Reserve 1,900 Commission (Dr.) 1,550

Outstanding Salaries 500

Adjustments:

1. Bad debts ₹500

2. Provide for doubtful debts @5% on debtors

3. Depreciation Plant and Machinery @ 10% p.a.

4. Wages still outstanding were ₹1,000.

5. General expenses include expenses paid in advance to extent of ₹200.

Solution

TRADING AND PROFIT AND LOSS ACCOUNT

for the year ending 31st

March 2023

Dr. Cr.

Particulars Amt.(₹) Amt.(₹) Particulars Amt.(₹) Amt.(₹)

To Adjusted Purchases 58,600 By Sales 99,200

To Wages 19,970

Add: Outstanding 1,000 20,970

To Carriage inwards 1,790

To Gross Profit (B/F) 17,840

99,200 99,200

To General Expenses 3,790 By Trading A/c (G.P) 17,840

Less: Prepaid 200 3,590 By Interest on Drawings 400

To Prize distribution 200 Be Net Loss 10,121

To Discount allowed 4,300

To Advertisement Expenses 5,600

To Salaries 7,850

To Charity 1,300

To Commission 1,550

To Bad debts provision 981

To Depreciation on P&M 2,990

28,361 28,361

30.

BALANCE SHEET

as at31st

March 2023

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Outstanding Salaries 500 Buildings 20,000

Trade Creditors 17,890 Plant & Machinery 29,900

Bills Payable 9,350 Less: Depreciation 2,990 26,910

Bank Loan 20,000 Investments 30,000

General Reserves 1,900 Closing Stock 210

Outstanding wages 1,000 Bills Receivable 180

Capital 84,600 Debtors 32,110

Less: Net Loss 10,121 74,479 Less: Bad Debts 500

31,610

Less: New Provision 1,581 30,029

Cash at Bank 9,490

Accrued Interest 8,100

Prepaid General Expenses 200

1,25,119 1,25,119

Working Notes:

Calculation of Provision for Bad Debts

Old Bad debts (given in T.B) Nil

Add: New bad debts (given in adjustments) 500

Total 500

Debtors 21,110

Less: New bad debts (given in adjustments) 500

31,610 X 5/100 1,581 (This is New Provision)

Total 2,081

Less: Provision for bad debts (given in T.B) 1,100

Show this in P&L A/C Dr. side 981

Treatment in Balance Sheet

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Debtors 32,110

Less: Bad Debts 500

31,610

Less: New Provision 1,581 30,029

Note:

Adjusted Purchases

Adjusted purchases means that Opening Stock, Returns Outwards and Closing Stock have been adjusted

in the purchases. As a result, Adjusted Purchases Account and Closing Stock are shown in Trial

Balance. Thus, Closing Stock, if given in the Trial Balance, means that Opening Stock, Closing Stock

and Purchases Return are adjusted in the purchases. As a result, Opening Stock and Purchases Return

are not shown in the Trial Balance and instead Adjusted Purchases and Closing Stock are shown therein.

Adjusted Purchases = Opening Stock + Purchases (Net) – Closing Stock.

[or]

Adjusted Purchases = Opening Stock + Purchases – Purchases Return – Closing Stock

Adjusted purchases are transferred in the debit of Trading Account while Closing Stock is shown as an

asset in the Balance Sheet under Current Assets.

31.

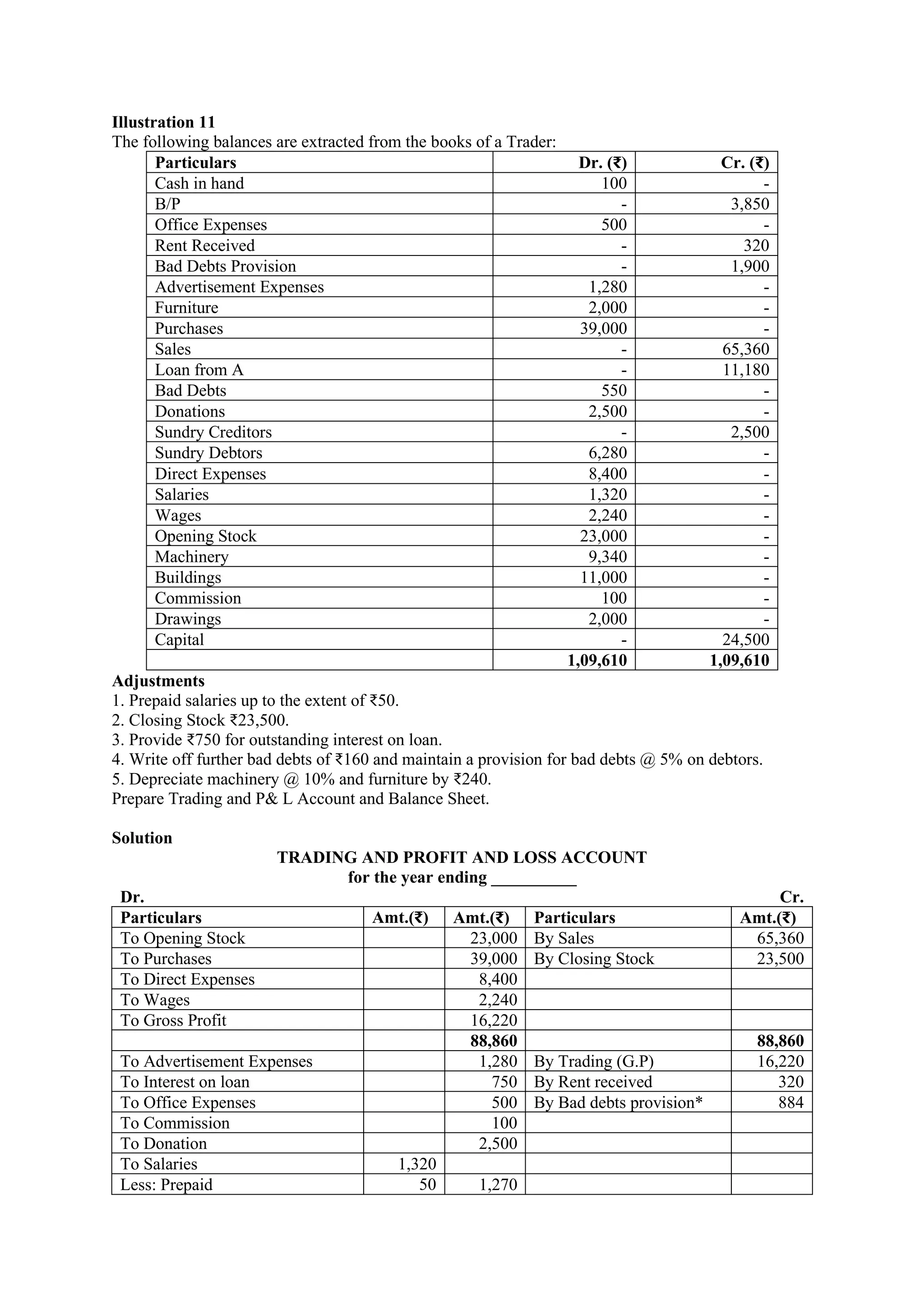

Illustration 11

The followingbalances are extracted from the books of a Trader:

Particulars Dr. (₹) Cr. (₹)

Cash in hand 100 -

B/P - 3,850

Office Expenses 500 -

Rent Received - 320

Bad Debts Provision - 1,900

Advertisement Expenses 1,280 -

Furniture 2,000 -

Purchases 39,000 -

Sales - 65,360

Loan from A - 11,180

Bad Debts 550 -

Donations 2,500 -

Sundry Creditors - 2,500

Sundry Debtors 6,280 -

Direct Expenses 8,400 -

Salaries 1,320 -

Wages 2,240 -

Opening Stock 23,000 -

Machinery 9,340 -

Buildings 11,000 -

Commission 100 -

Drawings 2,000 -

Capital - 24,500

1,09,610 1,09,610

Adjustments

1. Prepaid salaries up to the extent of ₹50.

2. Closing Stock ₹23,500.

3. Provide ₹750 for outstanding interest on loan.

4. Write off further bad debts of ₹160 and maintain a provision for bad debts @ 5% on debtors.

5. Depreciate machinery @ 10% and furniture by ₹240.

Prepare Trading and P& L Account and Balance Sheet.

Solution

TRADING AND PROFIT AND LOSS ACCOUNT

for the year ending __________

Dr. Cr.

Particulars Amt.(₹) Amt.(₹) Particulars Amt.(₹)

To Opening Stock 23,000 By Sales 65,360

To Purchases 39,000 By Closing Stock 23,500

To Direct Expenses 8,400

To Wages 2,240

To Gross Profit 16,220

88,860 88,860

To Advertisement Expenses 1,280 By Trading (G.P) 16,220

To Interest on loan 750 By Rent received 320

To Office Expenses 500 By Bad debts provision* 884

To Commission 100

To Donation 2,500

To Salaries 1,320

Less: Prepaid 50 1,270

32.

To Depreciation onMachinery 934

To Depreciation on Furniture 240

To Net Profit 9,850

17,424 17,424

BALANCE SHEET

as at _________

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Capital 24,500 Buildings 11,000

Add: Net Profit 9,850 Machinery 9,340

34,350 Less: Depreciation 934 8,406

Less: Drawings 2,000 32,350 Furniture 2,000

B/P 3,850 Less: Depreciation 240 1,760

Loan from A 11,180 Closing Stock 23,500

Add: Interest 750 11,930 Debtor (6,280-160-306) 5,814

Sundry Creditors 2,500 Prepaid salaries 50

Cash in Hand 100

50,630 50,630

Working Notes:

Calculation of Provision for Bad Debts

Old Bad debts (given in T.B) 550

Add: New bad debts (given in adjustments) 160

Total 710

Debtors 6,280

Less: New bad debts (given in adjustments) 160

6,120 X 5/100 306 (This is New Provision)

Total 1,016

Less: Provision for bad debts (given in T.B) 1,900

Show this in P&L A/C Cr. side 884 (Negative Balance)

Treatment in Balance Sheet

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Debtors 6,280

Less: New Bad Debts 160

6,120

Less: New Provision 306 5,814

10. Treatment of Interest on Capital

The amount brought by a trader in known as capital, he expects some type of return. Net Profit can be

the first type and second is interest on capital, which he will be taking from his business. Interest on

capital is therefore generally given to proprietor who has invested his money in the business and interest

is treated as trade expenses.

Journal entry for this interest on capital will be:

Interest on Capital A/c Dr.

To Capital A/c

(Being interest on capital credited to capital account)

Final accounts will be effected as follows, if interest on capital is given in adjustment

Profit and Loss Account

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

To interest on Capital 2,500

33.

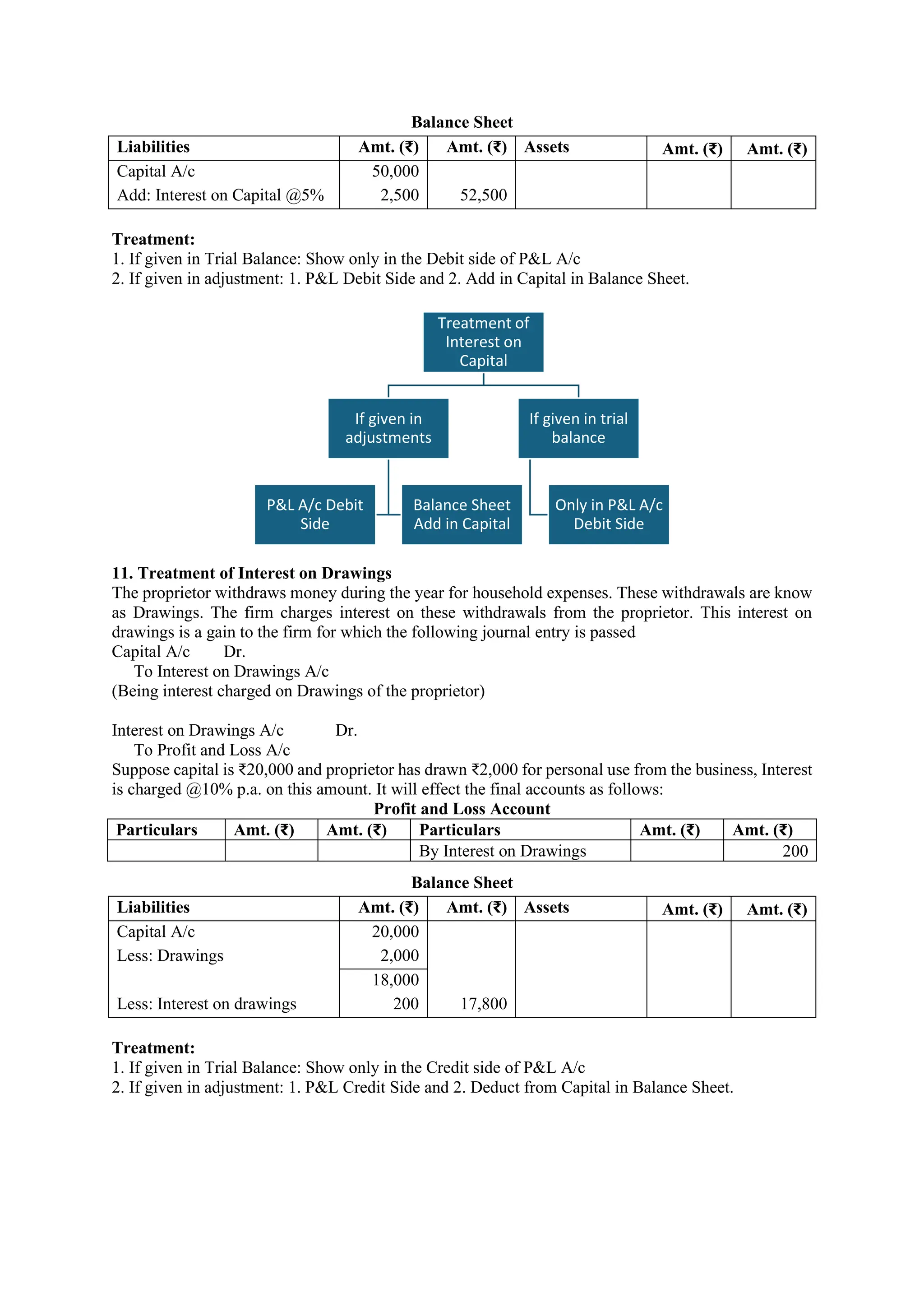

Balance Sheet

Liabilities Amt.(₹) Amt. (₹) Assets Amt. (₹) Amt. (₹)

Capital A/c 50,000

Add: Interest on Capital @5% 2,500 52,500

Treatment:

1. If given in Trial Balance: Show only in the Debit side of P&L A/c

2. If given in adjustment: 1. P&L Debit Side and 2. Add in Capital in Balance Sheet.

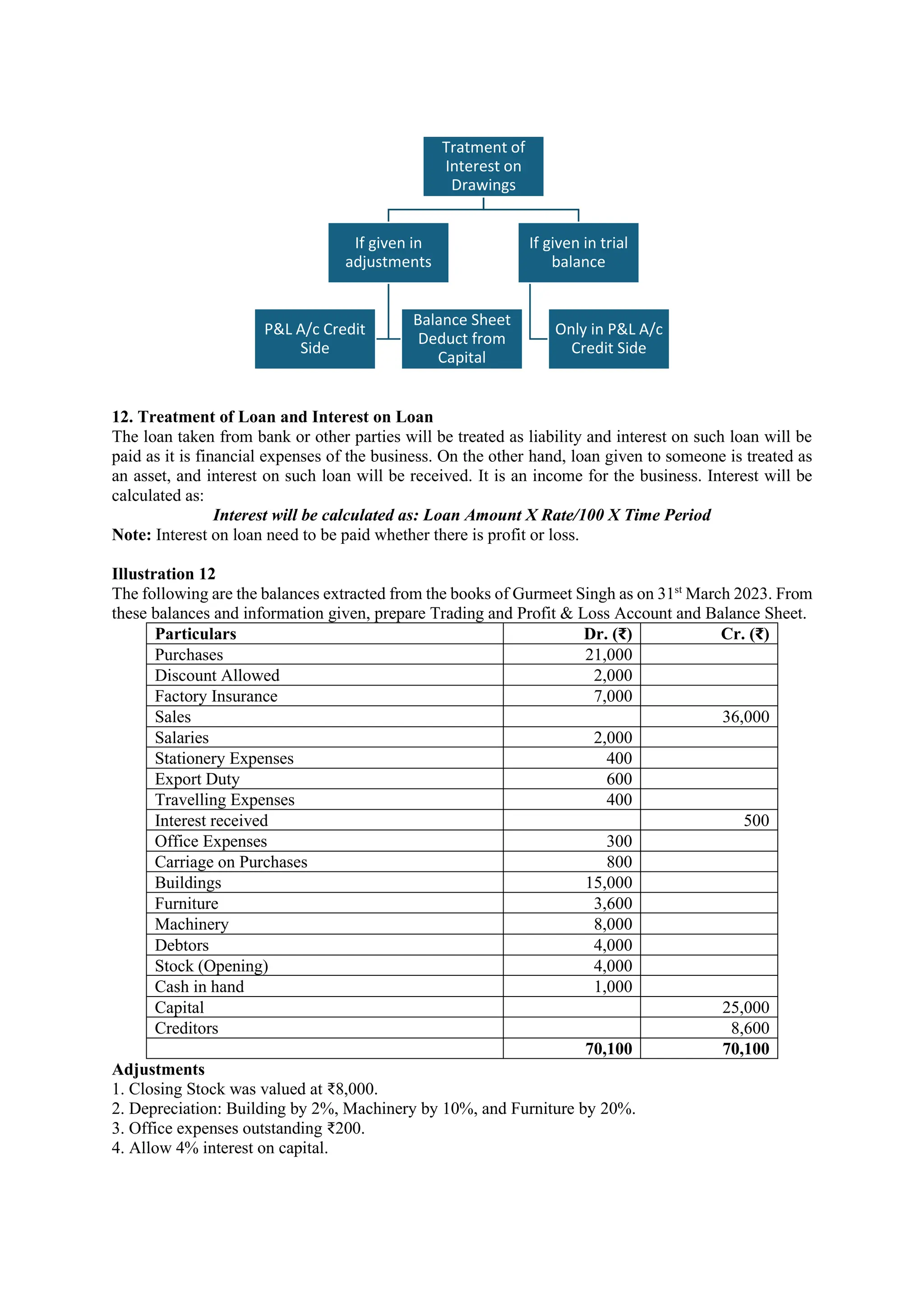

11. Treatment of Interest on Drawings

The proprietor withdraws money during the year for household expenses. These withdrawals are know

as Drawings. The firm charges interest on these withdrawals from the proprietor. This interest on

drawings is a gain to the firm for which the following journal entry is passed

Capital A/c Dr.

To Interest on Drawings A/c

(Being interest charged on Drawings of the proprietor)

Interest on Drawings A/c Dr.

To Profit and Loss A/c

Suppose capital is ₹20,000 and proprietor has drawn ₹2,000 for personal use from the business, Interest

is charged @10% p.a. on this amount. It will effect the final accounts as follows:

Profit and Loss Account

Particulars Amt. (₹) Amt. (₹) Particulars Amt. (₹) Amt. (₹)

By Interest on Drawings 200

Balance Sheet

Liabilities Amt. (₹) Amt. (₹) Assets Amt. (₹) Amt. (₹)

Capital A/c 20,000

Less: Drawings 2,000

18,000

Less: Interest on drawings 200 17,800

Treatment:

1. If given in Trial Balance: Show only in the Credit side of P&L A/c

2. If given in adjustment: 1. P&L Credit Side and 2. Deduct from Capital in Balance Sheet.

Treatment of

Interest on

Capital

If given in

adjustments

P&L A/c Debit

Side

Balance Sheet

Add in Capital

If given in trial

balance

Only in P&L A/c

Debit Side

34.

12. Treatment ofLoan and Interest on Loan

The loan taken from bank or other parties will be treated as liability and interest on such loan will be

paid as it is financial expenses of the business. On the other hand, loan given to someone is treated as

an asset, and interest on such loan will be received. It is an income for the business. Interest will be

calculated as:

Interest will be calculated as: Loan Amount X Rate/100 X Time Period

Note: Interest on loan need to be paid whether there is profit or loss.

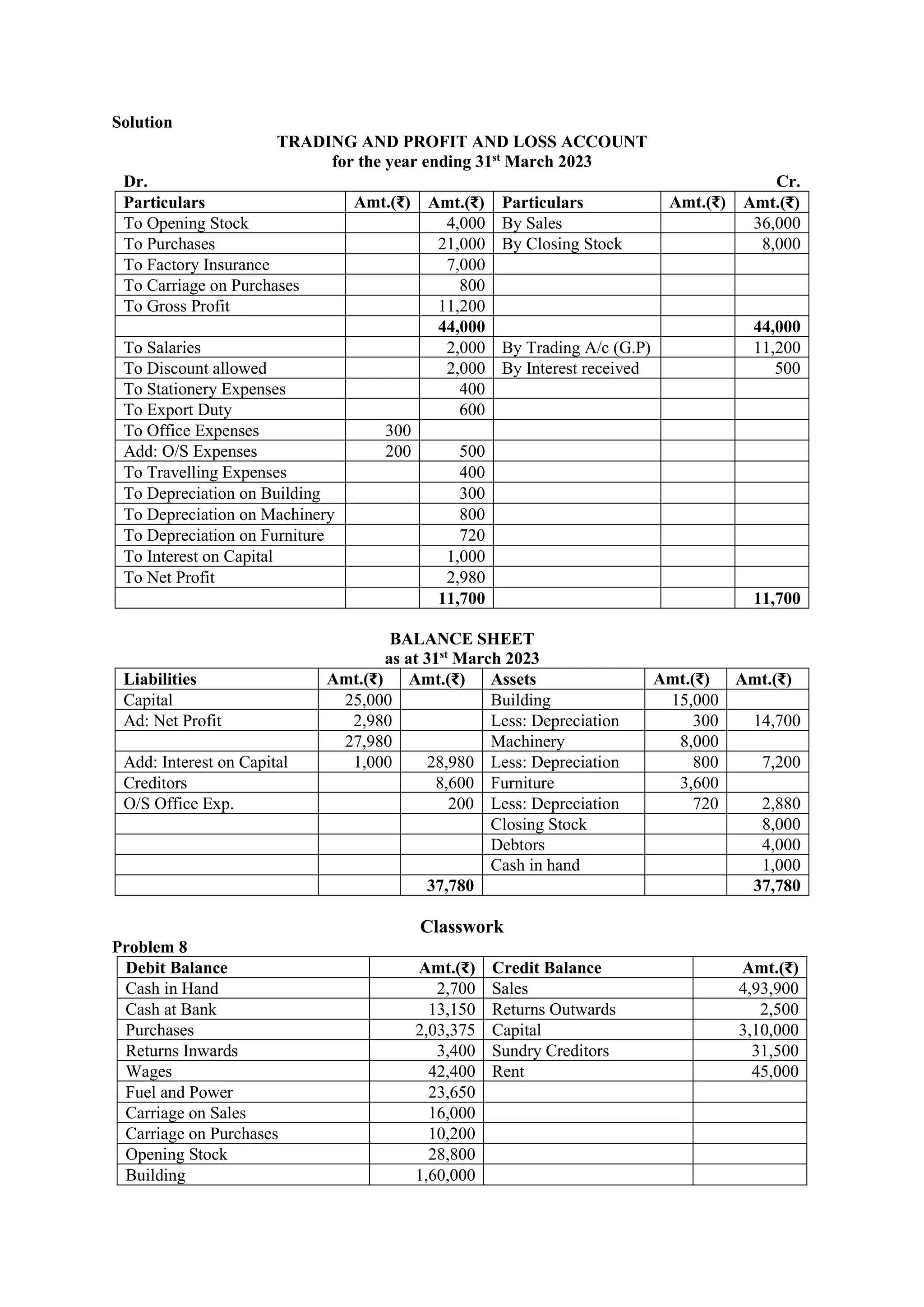

Illustration 12

The following are the balances extracted from the books of Gurmeet Singh as on 31st

March 2023. From

these balances and information given, prepare Trading and Profit & Loss Account and Balance Sheet.

Particulars Dr. (₹) Cr. (₹)

Purchases 21,000

Discount Allowed 2,000

Factory Insurance 7,000

Sales 36,000

Salaries 2,000

Stationery Expenses 400

Export Duty 600

Travelling Expenses 400

Interest received 500

Office Expenses 300

Carriage on Purchases 800

Buildings 15,000

Furniture 3,600

Machinery 8,000

Debtors 4,000

Stock (Opening) 4,000

Cash in hand 1,000

Capital 25,000

Creditors 8,600

70,100 70,100

Adjustments

1. Closing Stock was valued at ₹8,000.

2. Depreciation: Building by 2%, Machinery by 10%, and Furniture by 20%.

3. Office expenses outstanding ₹200.

4. Allow 4% interest on capital.

Tratment of

Interest on

Drawings

If given in

adjustments

P&L A/c Credit

Side

Balance Sheet

Deduct from

Capital

If given in trial

balance

Only in P&L A/c

Credit Side

35.

Solution

TRADING AND PROFITAND LOSS ACCOUNT

for the year ending 31st

March 2023

Dr. Cr.

Particulars Amt.(₹) Amt.(₹) Particulars Amt.(₹) Amt.(₹)

To Opening Stock 4,000 By Sales 36,000

To Purchases 21,000 By Closing Stock 8,000

To Factory Insurance 7,000

To Carriage on Purchases 800

To Gross Profit 11,200

44,000 44,000

To Salaries 2,000 By Trading A/c (G.P) 11,200

To Discount allowed 2,000 By Interest received 500

To Stationery Expenses 400

To Export Duty 600

To Office Expenses 300

Add: O/S Expenses 200 500

To Travelling Expenses 400

To Depreciation on Building 300

To Depreciation on Machinery 800

To Depreciation on Furniture 720

To Interest on Capital 1,000

To Net Profit 2,980

11,700 11,700

BALANCE SHEET

as at 31st

March 2023

Liabilities Amt.(₹) Amt.(₹) Assets Amt.(₹) Amt.(₹)

Capital 25,000 Building 15,000

Ad: Net Profit 2,980 Less: Depreciation 300 14,700

27,980 Machinery 8,000

Add: Interest on Capital 1,000 28,980 Less: Depreciation 800 7,200

Creditors 8,600 Furniture 3,600

O/S Office Exp. 200 Less: Depreciation 720 2,880

Closing Stock 8,000

Debtors 4,000

Cash in hand 1,000

37,780 37,780

Classwork

Problem 8

Debit Balance Amt.(₹) Credit Balance Amt.(₹)

Cash in Hand 2,700 Sales 4,93,900

Cash at Bank 13,150 Returns Outwards 2,500

Purchases 2,03,375 Capital 3,10,000

Returns Inwards 3,400 Sundry Creditors 31,500

Wages 42,400 Rent 45,000

Fuel and Power 23,650

Carriage on Sales 16,000

Carriage on Purchases 10,200

Opening Stock 28,800

Building 1,60,000

36.

Freehold Land 50,000

Machinery1,00,000

Salaries 75,000

Furniture 37,500

General Expenses 15,000

Insurance Premium 3,000

Drawings 26,225

Sundry Debtors 72,500

8,82,900 8,82,900

Taking into account the following adjustments, prepare Trading and Profit & Loss Account and Balance

Sheet as on March 31, 2023.

1. Stock in hand on March 31, 2023, was ₹34,000.

2. Machinery is to be depreciated at the rate of 10% and furniture @ 20%.

3. Salaries for the month of March 2023 amounted to ₹7,500 were outstanding.

4. Insurance includes a premium of ₹850 on a policy expiring on September 30, 2023.

5. Further bad debts are ₹3,625. Create a provision @ 5% on debtors.

6. Rent receivable ₹5,000.

[Answer: Gross profit: ₹2,18,575; Net profit: ₹1,27,931; Balance Sheet Total: ₹4,50,706]

Problem 9

From the following information, you are required to prepare Trading and Profit & Loss Account and

Balance Sheet.

Particulars Amt.(₹) Particulars Amt.(₹)

Raman’s Capital 2,28,800 Stock 1.4.2023 38,500

Raman’s Drawings 13,200 Wages 35,200

Plant and Machinery 99,000 Sundry Creditors 44,000

Freehold Property 66,000 Postages and Telegram 1,540

Purchases 1,10,000 Insurance 1,760

Purchases Return 1,100 Gas and Fuel 2,970

Salaries 13,200 Bad Debts 660

Office Expenses 2,750 Office Rent 2,860

Office Furniture 5,500 Freight 9,900

Discount allowed 1,320 Loose Tools 2,200

Sundry Debtors 29,260 Factory Lighting 1,100

Loan to Mr. Kumar at 10% p.a. balance on

1.4.2023 44,000

Provision for bad and doubtful

debts 880

Cash at Bank 29,260 Interest on loan to Mr. Kumar 1,100

Bills Payable 5,500 Cash on hand 2,640

Sales 2,31,440

Adjustments

1. Stock on 1.3.2023 was valued at ₹72,600.

2. A new machine was installed during the year costing ₹15,400 but it was not recorded in the books as

no payment was made for it. Wages ₹1,100 paid for its erection have been debited to wage account.

3. Depreciation on plant and machinery by 33⅓%; furniture by 10%; Freehold property by 5%.

4. Loose tools were valued at ₹1,760 on 31.3.2023

5. Of the sundry debtors ₹600 are bad and should be written off.

6. Maintain a provision of 5% on sundry debtors for doubtful debts.

[Answer: Gross profit: ₹1,08,570; Net profit: ₹44,880; Balance Sheet Total: ₹3,25,380]

Problem 10

The following balances were extracted from the books of Shri R. Lal on March 31, 2017:

Particulars Amt.(₹) Particulars Amt.(₹)

Capital 1,00,000 Rent (Cr.) 2,100

37.

Drawings 17,600 Railwayfreight on sales 16,940

Purchases 80,000 Carriage inwards 2,310

Sales 1,40,370 Office expenses 1,340

Purchases Return 2,820 Printing and Stationery 600

Stock on April 01, 2016 11,460 Postage and Telegram 820

Bad debts 1,400 Sundry debtors 62,070

Doubtful debts reserve April 01, 2016 3,240 Sundry creditors 18,920

Rates and Insurance 1,300 Cash in bank 12,400

Discount (Cr.) 190 Cash in hand 2,210

Bills receivable 1,240 Office furniture 3,500

Sales returns 4,240 Salaries and Commission 9,870

Wages 6,280 Additions to buildings 7,000

Buildings 25,000

Prepare the trading and profit and loss account and a balance sheet as on 31st

March 2017 after keeping

in view the following adjustments:

1. Depreciate old buildings by ₹625 and addition to buildings at 2% and office furniture at 5%.

2. Write-off further bad debts ₹570.

3. Increase the bad debts reserve to 6% of debtors.

4. On March 31, 2017, ₹570 are outstanding for salary.

5. Rent receivable ₹200 on March 31, 2017.

6. Interest on capital at 5% to be charged.

7. Unexpired insurance ₹240.

8. Stock was valued at ₹14,920 on March 31, 2017.

[Answer: Gross profit: ₹53,190; Net profit: ₹16,060; Balance Sheet Total: ₹1,22,950]

Problem 11

From the following Trail Balance of Ramesh, you are required to prepare Trading, Profit and Loss

Account and a Balance Sheet as on that date:

Particulars Dr. (₹) Cr. (₹)

Purchases 1,30,295 --

Sales -- 1,80,500

Cash in hand 500 --

Cash at bank 9,500 --

Stock on 1st

April 2023 40,000 --

Wages 22,525 --

Sales Return 2,400 --

Purchases Return -- 195

Repairs 1,675 --

Debtors 30,000 --

Creditors -- 30,305

Bad Debts 2,310 --

Discount Allowed 800 --

Discount Received -- 530

Capital -- 37,500

Interest on Loan 600 --

Salaries 8,000 --

Postage and Courier 800 --

Freight inwards 500 --

Insurance 1,000 --

Donation 125 --

Rent 2,000 --

Machinery 16,000 --

12% Loan -- 20,000

38.

2,69,030 2,69,030

Adjustments:

1. Purchasesincludes a machine purchased on 1st

October 2023 for ₹4,000 and wages include ₹2,000

paid for its installation.

2. Provide for depreciation on Machinery @ 10%.

3. Stock on 31st

March 2024 was worth ₹40,925.

4. Salaries unpaid ₹800 and rent is paid up to 30th

June 2024.

5. Write off further bad debts ₹400 and create a provision of 5% on debtors for doubtful debts.

6. Prepaid insurance ₹300.

[Answer: Gross profit: ₹31,900; Net profit: ₹9,440; Balance Sheet Total: ₹99,845]

Problem 12

From the following Trial Balance of Sunil as on 31st

March 2024 prepare Trading and Profit and Loss

Account for the year ended 31st

March 2024 and Balance Sheet as at that date.

Particulars Dr. (₹) Cr. (₹)

Capital -- 8,00,000

Drawings 1,80,000 --

Sales -- 15,50,000

Purchases 8,26,000 --

Stock (1st

April 2023) 4,20,000 --

Returns Outwards -- 16,000

Carriage Inwards 12,000 --

Wages 40,000 --

Power 60,000 --

Machinery 5,00,000 --

Furniture 1,40,000 --

Rent 2,20,000 --

Salary 1,50,000 --

Insurance 36,000 --

Bank Loan -- 2,50,000

Debtors 2,06,000 --

Creditors -- 1,89,000

Cash in Hand 15,000 --

28,05,000 28,05,000

Adjustments:

1. Closing Stock ₹6,40,000.

2. Wages outstanding ₹24,000.

3. Interest rate on Bank Loan is 8%.

4. Bad Debts ₹6,000.

5. Provision for Doubtful Debts to be 5%.

6. Rent is paid for 11months.

7. Insurance premium is paid per annum, ended 31st

May 2024.

8. Loan from the bank was taken on 1st

October 2023.

9. Provide Depreciation on machinery @ 10% and on furniture @ 5%.

[Answer: Gross profit: ₹8,24,000; Net profit: ₹3,21,000; Balance Sheet Total: ₹14,34,000]

Self-Assessment

Q. No. 6

Prepare the trading profit and loss account of M/s Mohit Traders as on 31st

March 2023. Prepare Trading

and Profit and Loss Account and Balance Sheet as on that date:

Debit Balance Amt.(₹) Credit Balance Amt.(₹)

Opening Stock 24,000 Sales 4,00,000

Purchases 1,60,000 Return outwards 2,000

39.

Cash in hand16,000 Capital 1,50,000

Cash at bank 32,000 Creditors 64,000

Returns inwards 4,000 Bills payable 20,000

Wages 22,000 Commission received 4,000

Fuel and Power 18,000

Carriage inwards 6,000

Insurance 8,000

Buildings 1,00,000

Plant 80,000

Patents 30,000

Salaries 28,000

Furniture 12,000

Drawings 18,000

Rent 2,000

Debtors 80,000

6,40,000 6,40,000

Adjustments:

1. Salaries outstanding ₹12,000.

2. Wages outstanding ₹6,000.

3. Commission is accrued ₹2,400.

4. Depreciation on building 5% and plant 3%.

5. Insurance paid in advance ₹700.

6. Closing stock ₹12,000.

[Answer: Gross profit: ₹1,74,000; Net profit: ₹1,23,700; Balance Sheet Total: ₹3,57,700]

Q. No. 7

Following are the balances extracted from the books of Narain on 31st

March 2024.

Particulars Amt.(₹) Particulars Amt.(₹)

Narain’s Capital 3,00,000 Sales 15,00,000

Narain’s Drawings 50,000 Sales Return 20,000

Furniture and Fittings 26,000 Discount (Dr.) 16,000

Bank Overdraft 42,000 Discount (Cr.) 20,000

Creditors 1,38,000 Insurance 20,000

Building 2,00,000 General Expenses 40,000

Stock on 1st

April 2023 2,20,000 Salaries 90,000

Debtors 1,80,000 Commission (Dr.) 22,000

Rent from tenants 10,000 Carriage on Purchases 18,000

Purchases 11,00,000 Bad Debts written off 8,000

Adjustments:

1. Closing Stock at cost as on 31st

March 2024 was ₹2,00,600, whereas its Net Realisable Value (Market

Value) was ₹2,05,000.

2. Depreciation: Building by ₹3,000 and Furniture and Fittings by ₹2,500.

3. Make a provision of 5% on debtors for doubtful debts.

4. Carry forward ₹2,000 for unexpired insurance.

5. Outstanding Salary was ₹15,000.

Prepare Trading and Profit & Loss Account and Balance Sheet as at that date.

[Answer: Gross profit: ₹3,42,600; Net profit: ₹1,49,100; Balance Sheet Total: ₹5,94,100]

Hints: 1. Closing Stock will be taken at ₹2,00,600, being lower of Cost and Net Realisable Value

(Market Value) following the Prudence Concept.

2. ₹2,000 out of Insurance Expenses are Prepaid Insurance.

40.

Q. No. 8

PrepareTrading and Profit & Loss Account for the year ended 31st

March 2024 and Balance Sheet as

at that date from the following balances taken from the books of Vijay on 31st

March 2024 after giving

effect to the following adjustments:

i. Stock as on 31st

March 2024 was valued at ₹2,30,000.

ii. Write off further ₹1,800 as Bad Debts and maintain the Provision for Doubtful Debts at 5%.