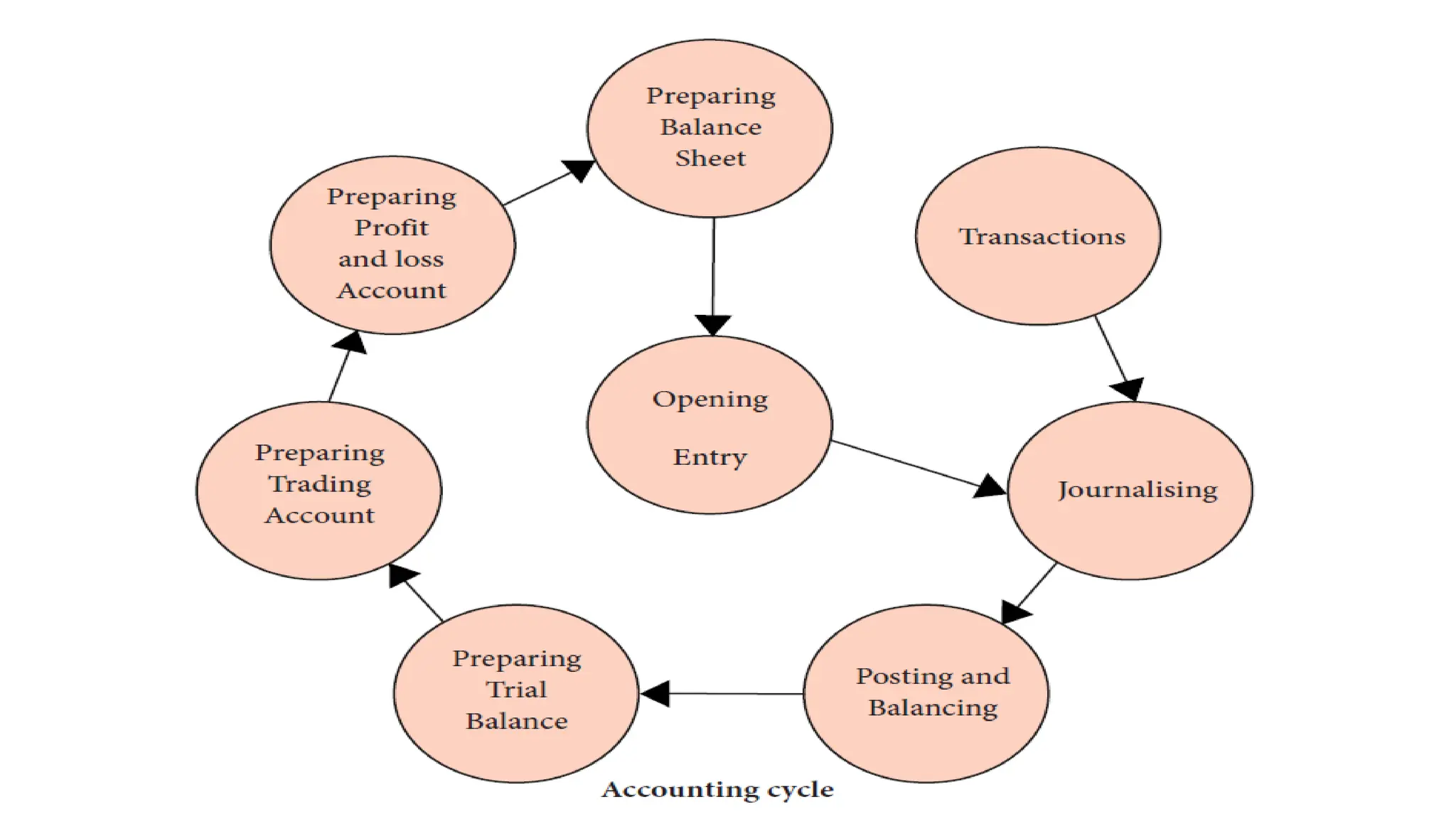

Journal

Journal is thebook of original entry in which business transactions are

recorded in chronological order, that is, in the order of occurrence.

Transactions are recorded for the first time in the journal. Entries are

made in the journal based on source documents.

Record of business transactions in the journal is known as Journal

entry. The process of recording the transactions in journal is called as

journalising.

3

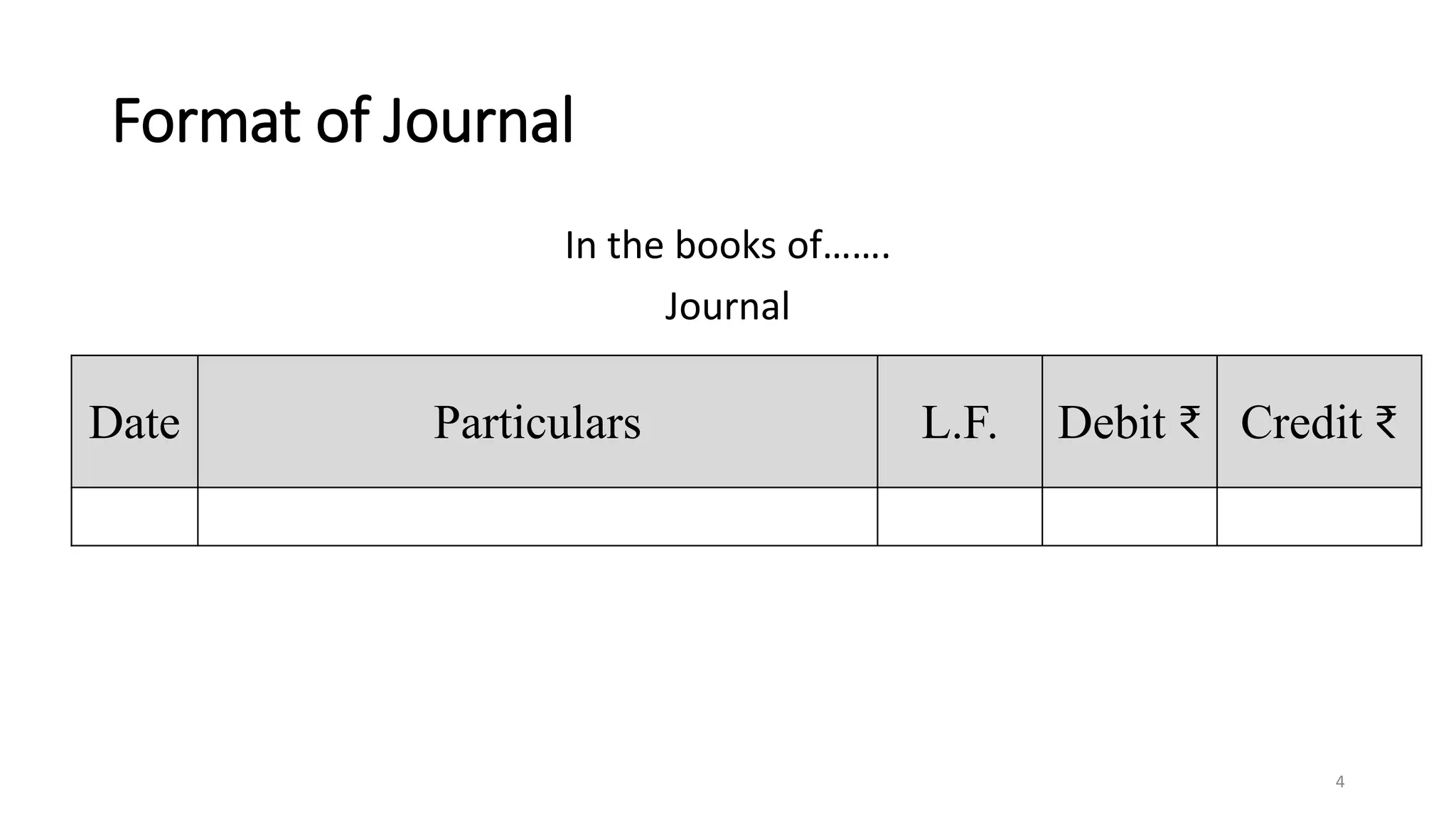

4.

Format of Journal

Inthe books of…….

Journal

4

Date Particulars L.F. Debit ₹ Credit ₹

5.

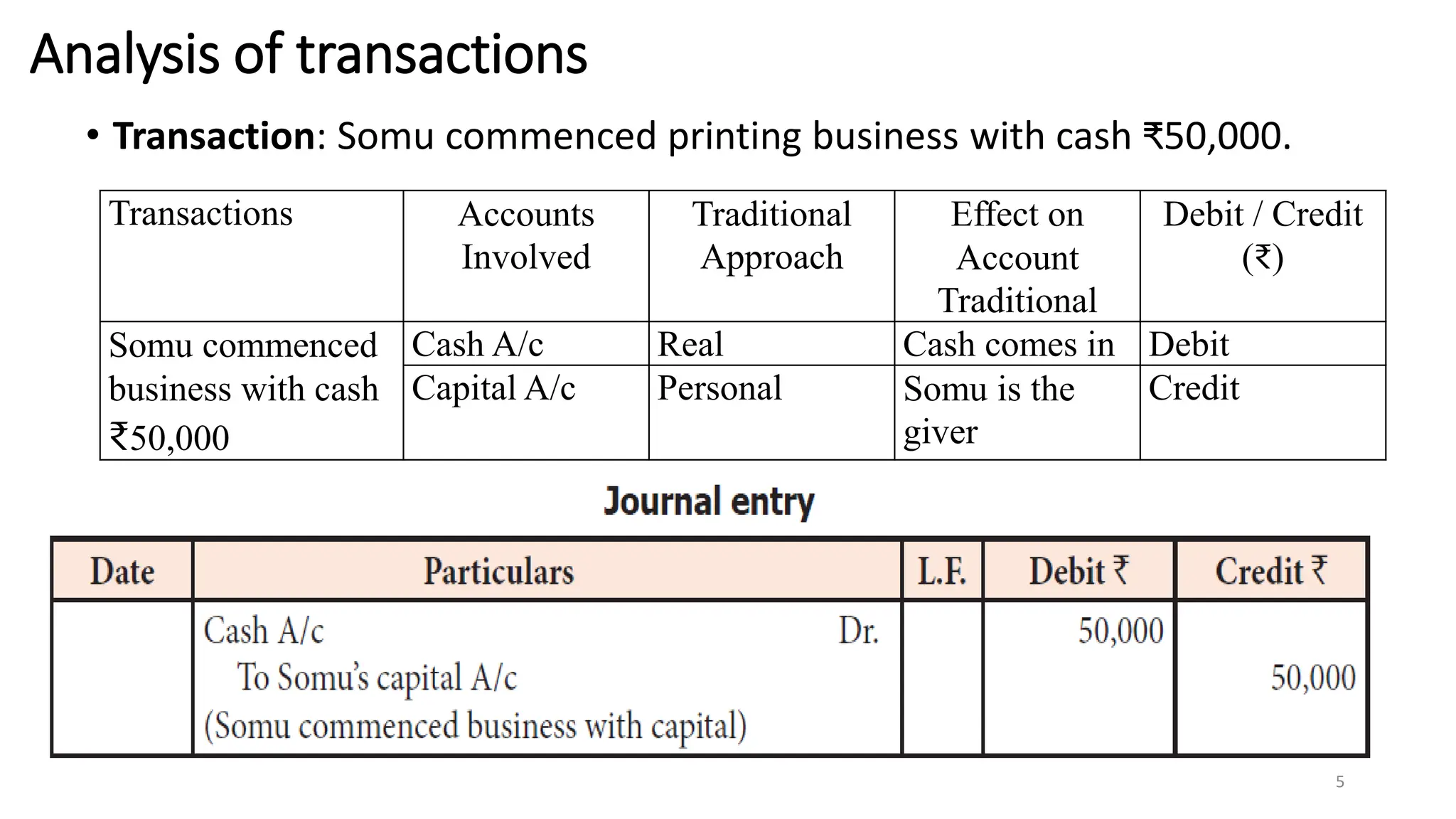

Analysis of transactions

•Transaction: Somu commenced printing business with cash ₹50,000.

5

Transactions Accounts

Involved

Traditional

Approach

Effect on

Account

Traditional

Debit / Credit

(₹)

Somu commenced

business with cash

₹50,000

Cash A/c Real Cash comes in Debit

Capital A/c Personal Somu is the

giver

Credit

6.

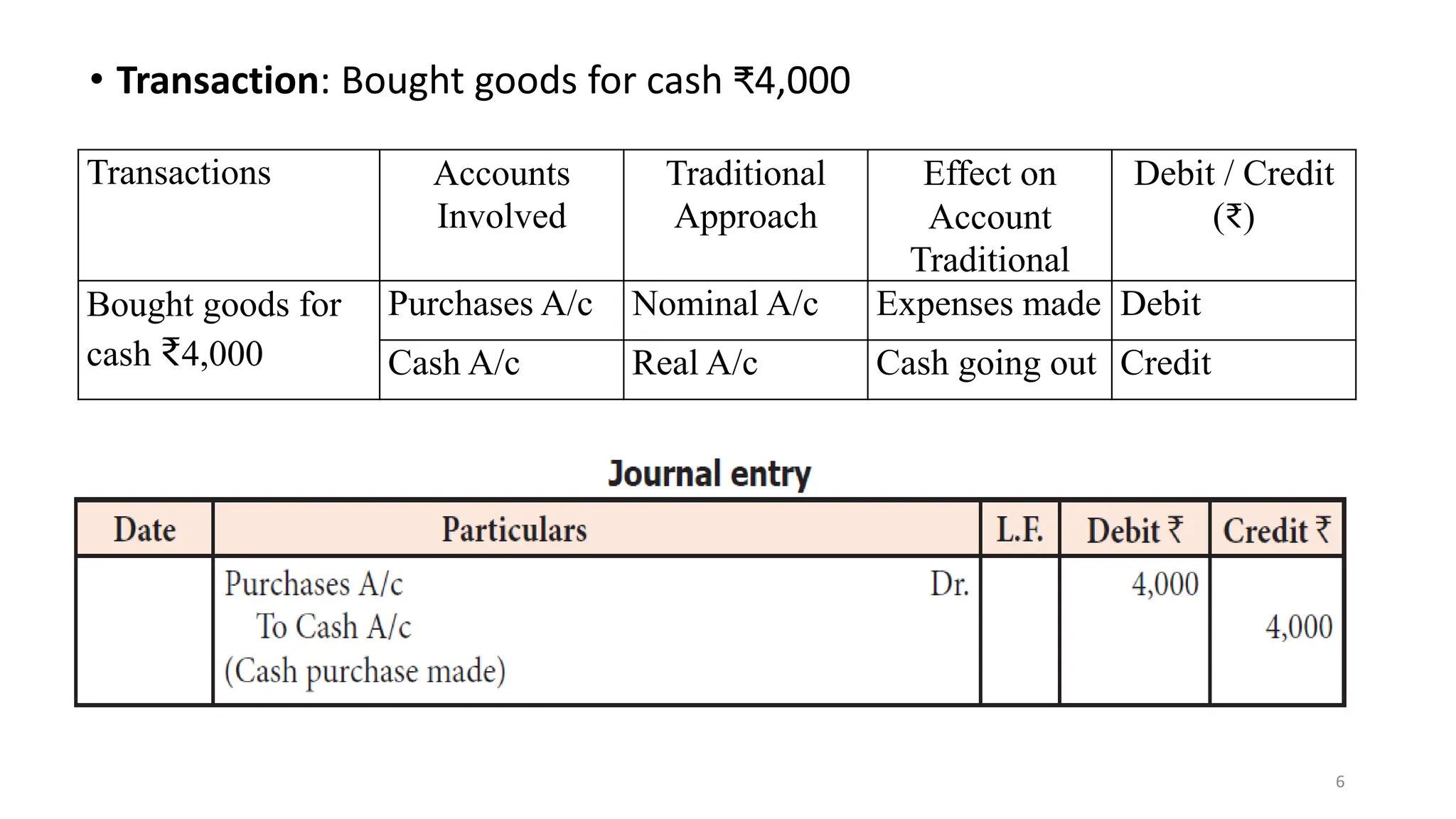

• Transaction: Boughtgoods for cash ₹4,000

6

Transactions Accounts

Involved

Traditional

Approach

Effect on

Account

Traditional

Debit / Credit

(₹)

Bought goods for

cash ₹4,000

Purchases A/c Nominal A/c Expenses made Debit

Cash A/c Real A/c Cash going out Credit

7.

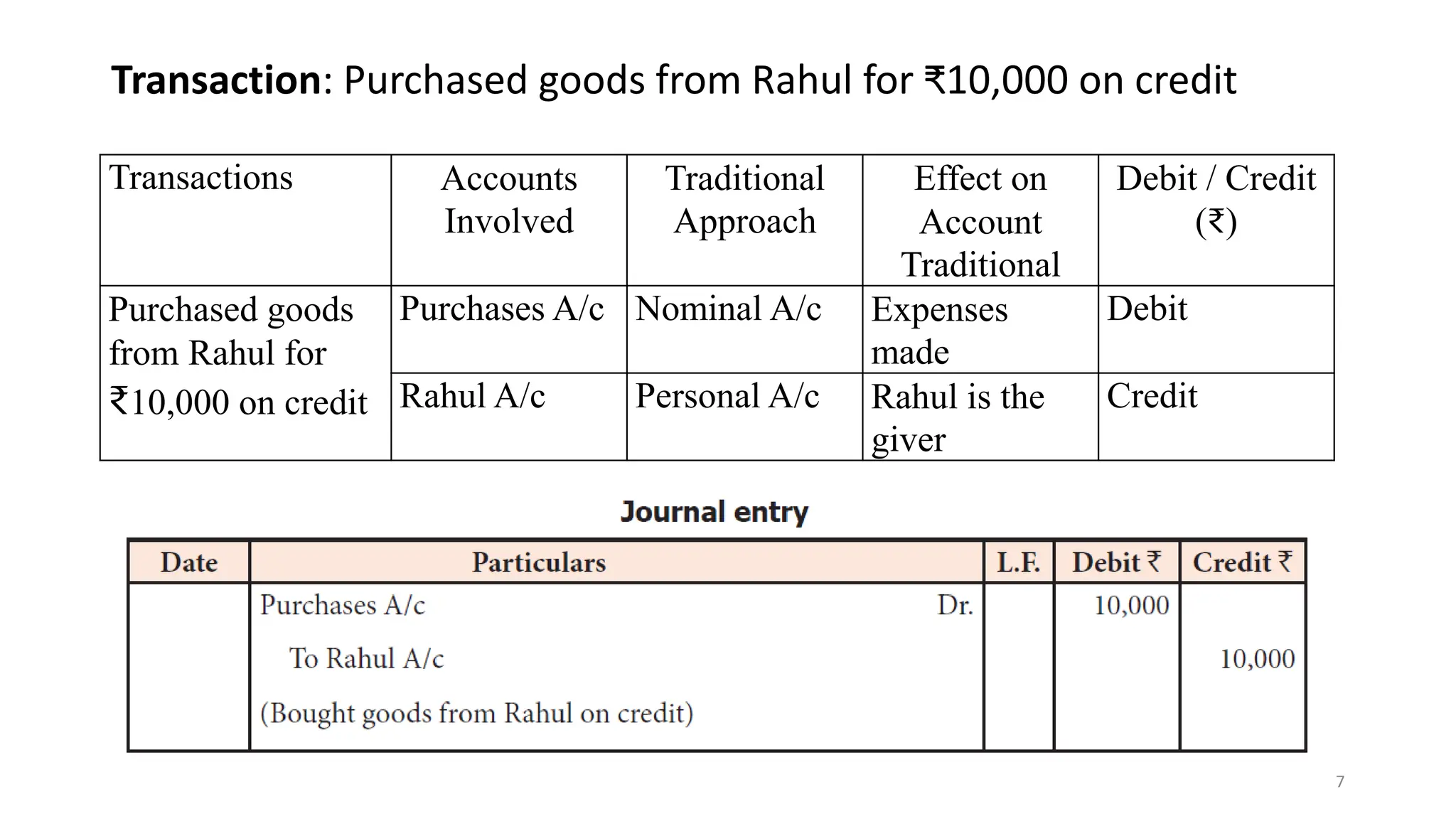

Transaction: Purchased goodsfrom Rahul for ₹10,000 on credit

Transactions Accounts

Involved

Traditional

Approach

Effect on

Account

Traditional

Debit / Credit

(₹)

Purchased goods

from Rahul for

₹10,000 on credit

Purchases A/c Nominal A/c Expenses

made

Debit

Rahul A/c Personal A/c Rahul is the

giver

Credit

7

8.

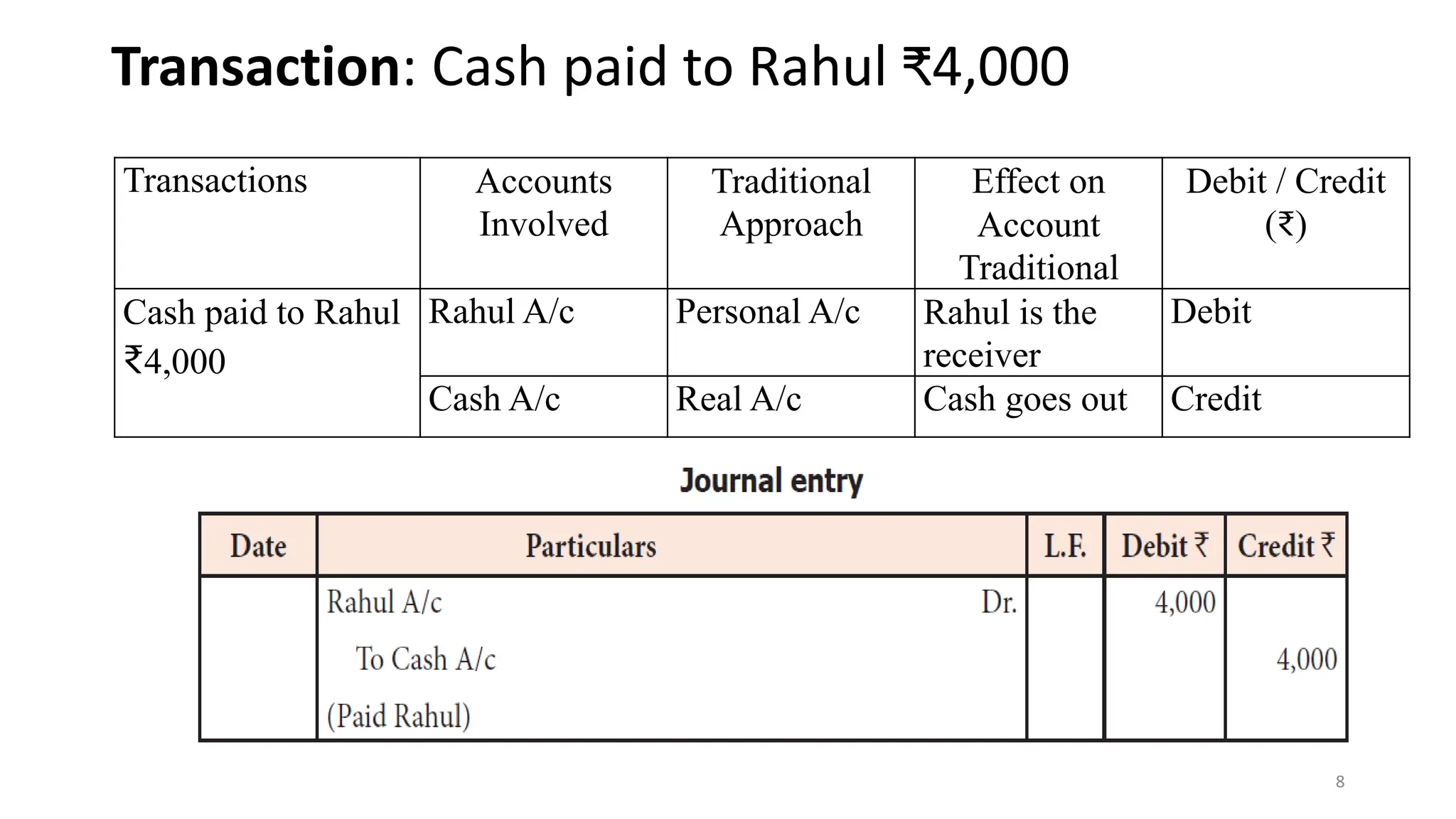

Transaction: Cash paidto Rahul ₹4,000

Transactions Accounts

Involved

Traditional

Approach

Effect on

Account

Traditional

Debit / Credit

(₹)

Cash paid to Rahul

₹4,000

Rahul A/c Personal A/c Rahul is the

receiver

Debit

Cash A/c Real A/c Cash goes out Credit

8

9.

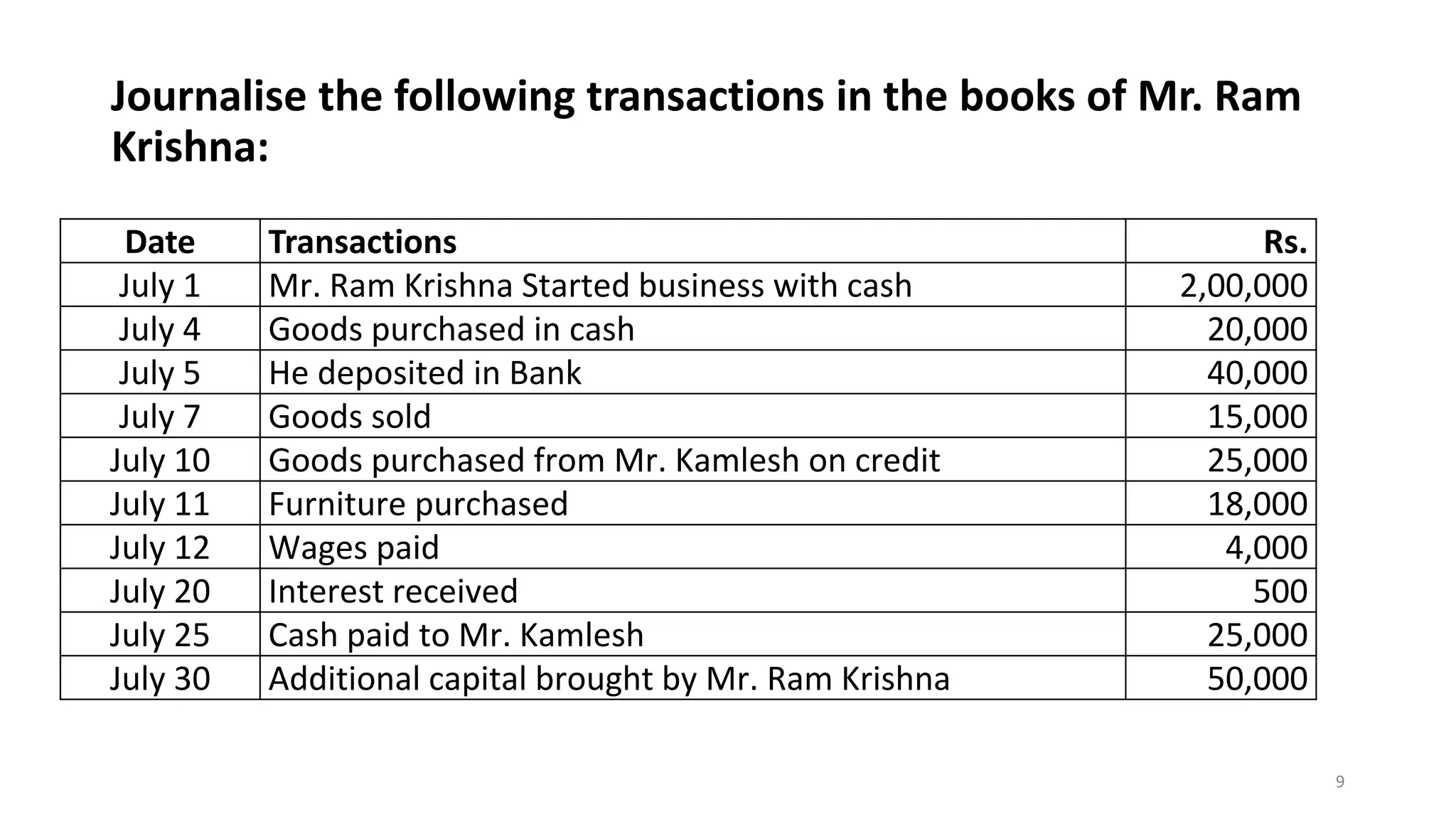

Journalise the followingtransactions in the books of Mr. Ram

Krishna:

Date Transactions Rs.

July 1 Mr. Ram Krishna Started business with cash 2,00,000

July 4 Goods purchased in cash 20,000

July 5 He deposited in Bank 40,000

July 7 Goods sold 15,000

July 10 Goods purchased from Mr. Kamlesh on credit 25,000

July 11 Furniture purchased 18,000

July 12 Wages paid 4,000

July 20 Interest received 500

July 25 Cash paid to Mr. Kamlesh 25,000

July 30 Additional capital brought by Mr. Ram Krishna 50,000

9

10.

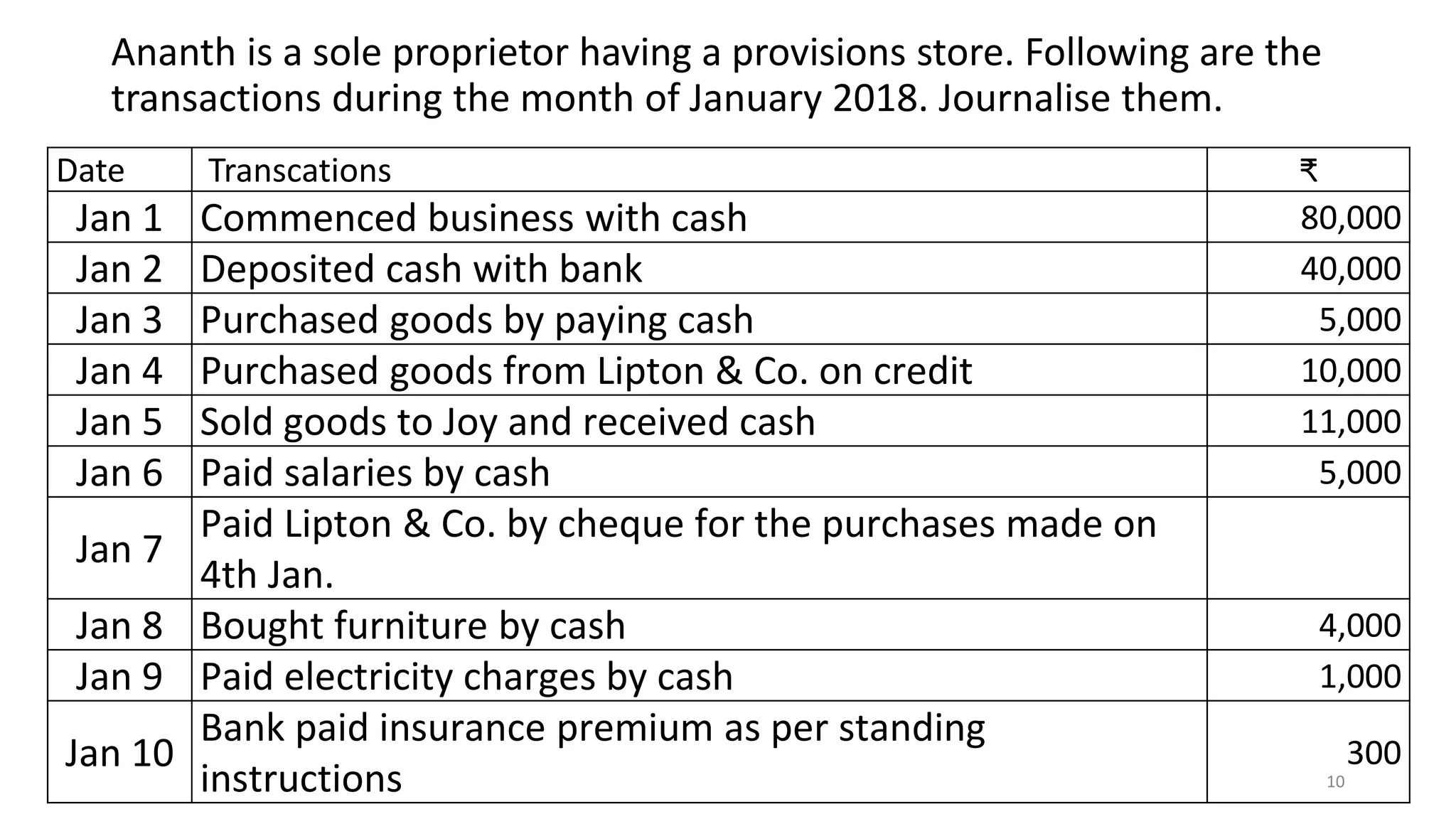

Ananth is asole proprietor having a provisions store. Following are the

transactions during the month of January 2018. Journalise them.

Date Transcations ₹

Jan 1 Commenced business with cash 80,000

Jan 2 Deposited cash with bank 40,000

Jan 3 Purchased goods by paying cash 5,000

Jan 4 Purchased goods from Lipton & Co. on credit 10,000

Jan 5 Sold goods to Joy and received cash 11,000

Jan 6 Paid salaries by cash 5,000

Jan 7

Paid Lipton & Co. by cheque for the purchases made on

4th Jan.

Jan 8 Bought furniture by cash 4,000

Jan 9 Paid electricity charges by cash 1,000

Jan 10

Bank paid insurance premium as per standing

instructions

300

10

11.

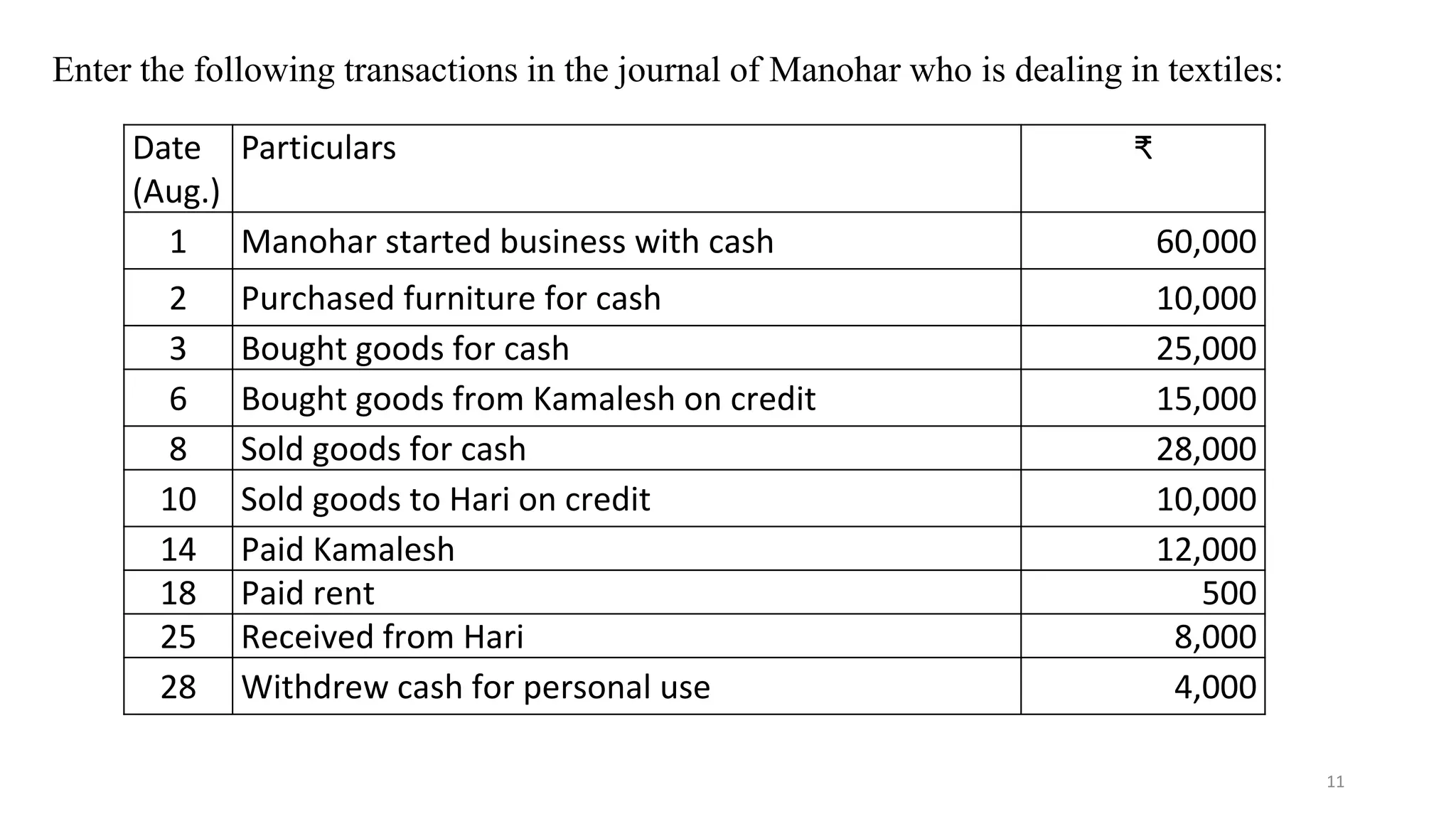

11

Enter the followingtransactions in the journal of Manohar who is dealing in textiles:

Date

(Aug.)

Particulars ₹

1 Manohar started business with cash 60,000

2 Purchased furniture for cash 10,000

3 Bought goods for cash 25,000

6 Bought goods from Kamalesh on credit 15,000

8 Sold goods for cash 28,000

10 Sold goods to Hari on credit 10,000

14 Paid Kamalesh 12,000

18 Paid rent 500

25 Received from Hari 8,000

28 Withdrew cash for personal use 4,000

12.

12

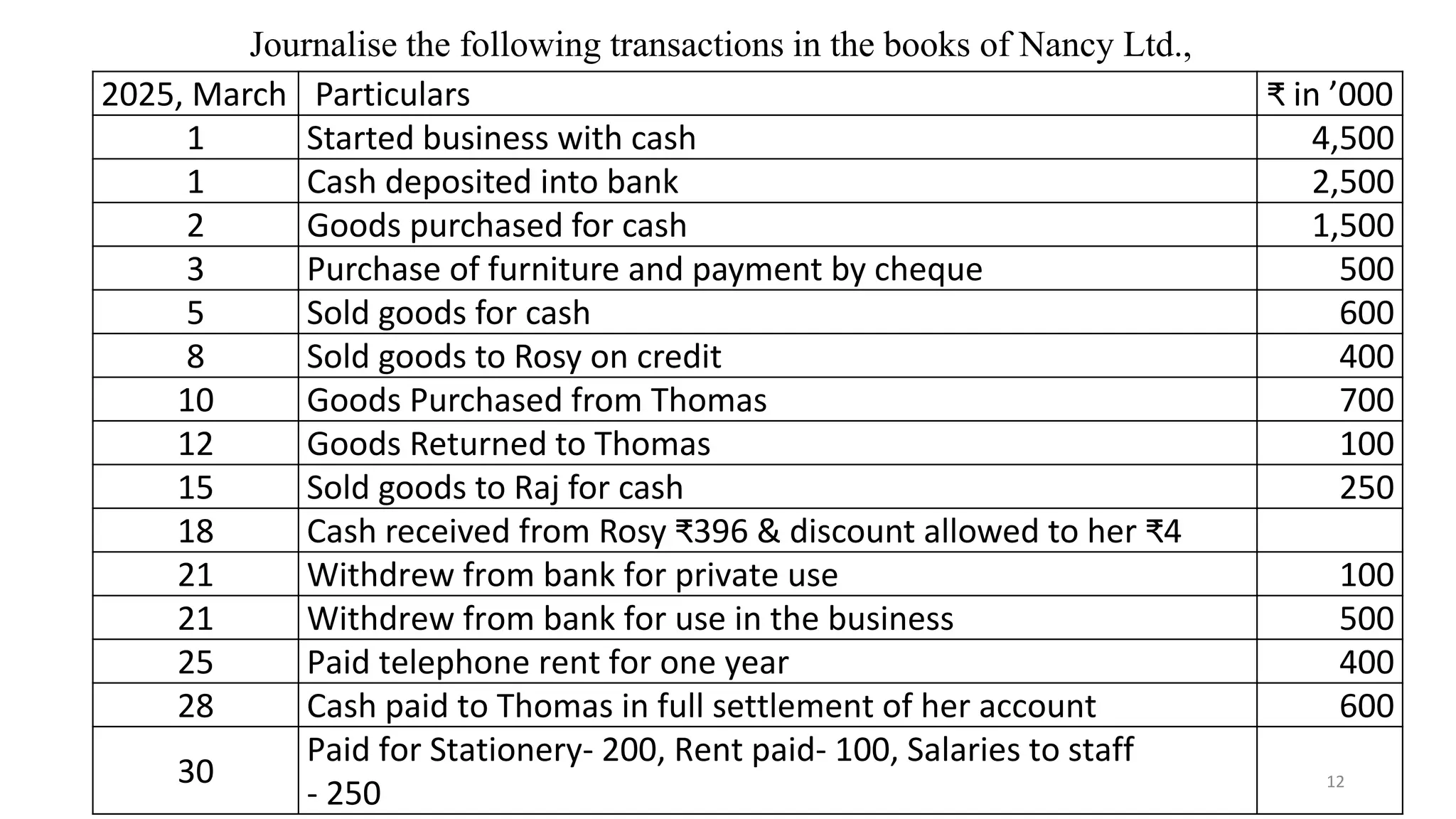

Journalise the followingtransactions in the books of Nancy Ltd.,

2025, March Particulars ₹ in ’000

1 Started business with cash 4,500

1 Cash deposited into bank 2,500

2 Goods purchased for cash 1,500

3 Purchase of furniture and payment by cheque 500

5 Sold goods for cash 600

8 Sold goods to Rosy on credit 400

10 Goods Purchased from Thomas 700

12 Goods Returned to Thomas 100

15 Sold goods to Raj for cash 250

18 Cash received from Rosy ₹396 & discount allowed to her ₹4

21 Withdrew from bank for private use 100

21 Withdrew from bank for use in the business 500

25 Paid telephone rent for one year 400

28 Cash paid to Thomas in full settlement of her account 600

30

Paid for Stationery- 200, Rent paid- 100, Salaries to staff

- 250

13.

13

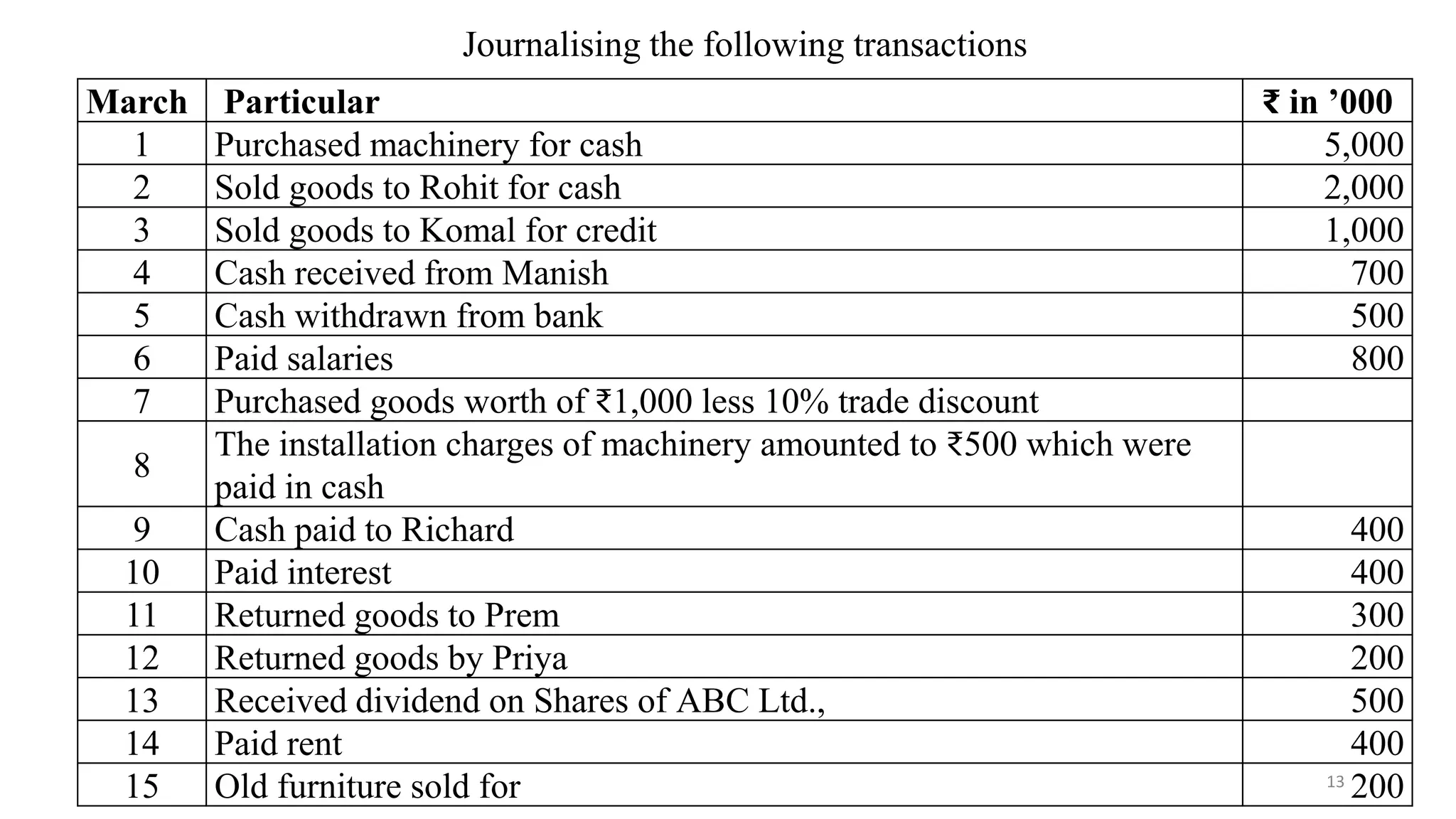

Journalising the followingtransactions

March Particular ₹ in ’000

1 Purchased machinery for cash 5,000

2 Sold goods to Rohit for cash 2,000

3 Sold goods to Komal for credit 1,000

4 Cash received from Manish 700

5 Cash withdrawn from bank 500

6 Paid salaries 800

7 Purchased goods worth of ₹1,000 less 10% trade discount

8

The installation charges of machinery amounted to ₹500 which were

paid in cash

9 Cash paid to Richard 400

10 Paid interest 400

11 Returned goods to Prem 300

12 Returned goods by Priya 200

13 Received dividend on Shares of ABC Ltd., 500

14 Paid rent 400

15 Old furniture sold for 200

14.

14

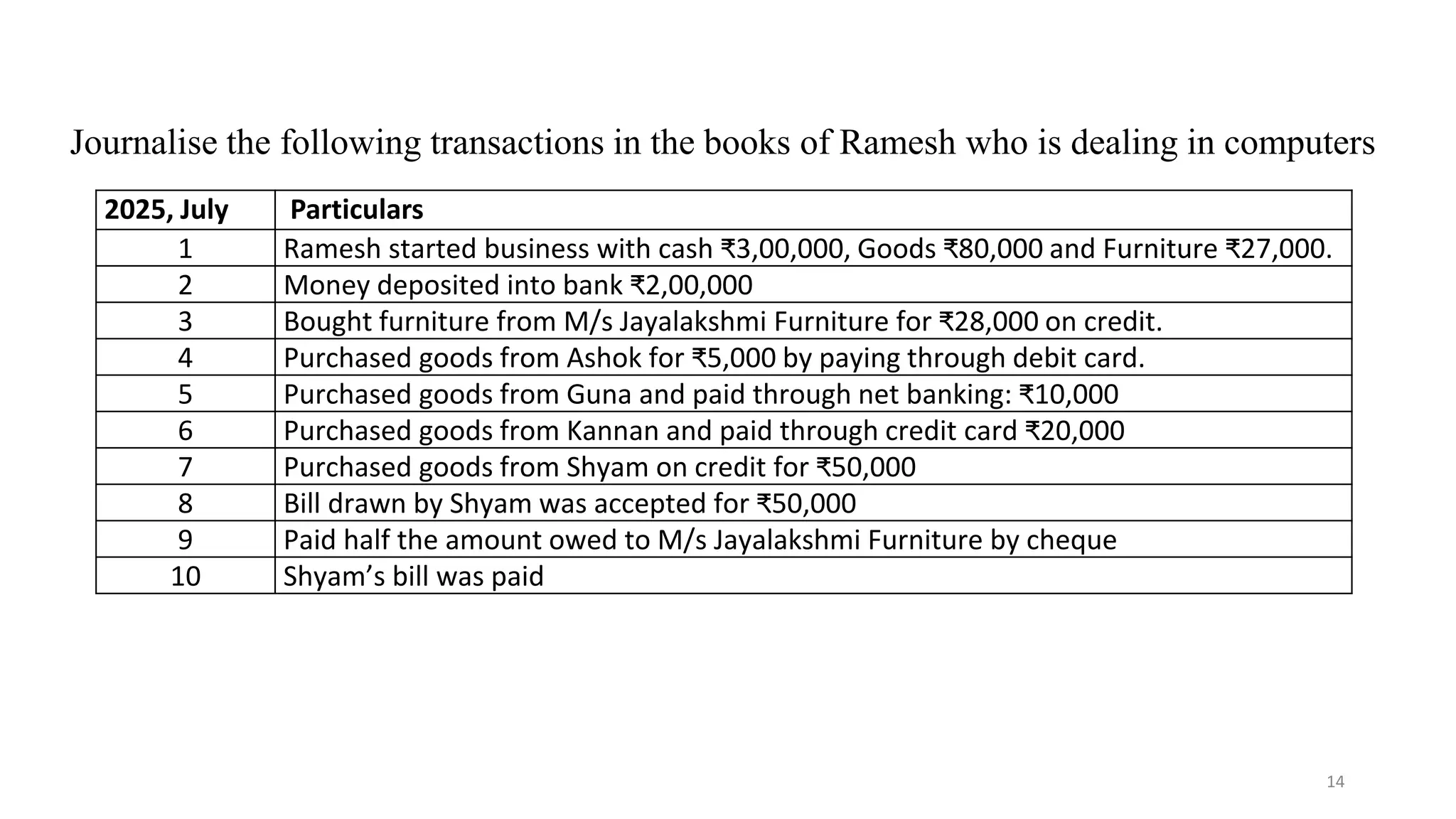

Journalise the followingtransactions in the books of Ramesh who is dealing in computers

2025, July Particulars

1 Ramesh started business with cash ₹3,00,000, Goods ₹80,000 and Furniture ₹27,000.

2 Money deposited into bank ₹2,00,000

3 Bought furniture from M/s Jayalakshmi Furniture for ₹28,000 on credit.

4 Purchased goods from Ashok for ₹5,000 by paying through debit card.

5 Purchased goods from Guna and paid through net banking: ₹10,000

6 Purchased goods from Kannan and paid through credit card ₹20,000

7 Purchased goods from Shyam on credit for ₹50,000

8 Bill drawn by Shyam was accepted for ₹50,000

9 Paid half the amount owed to M/s Jayalakshmi Furniture by cheque

10 Shyam’s bill was paid

15.

15

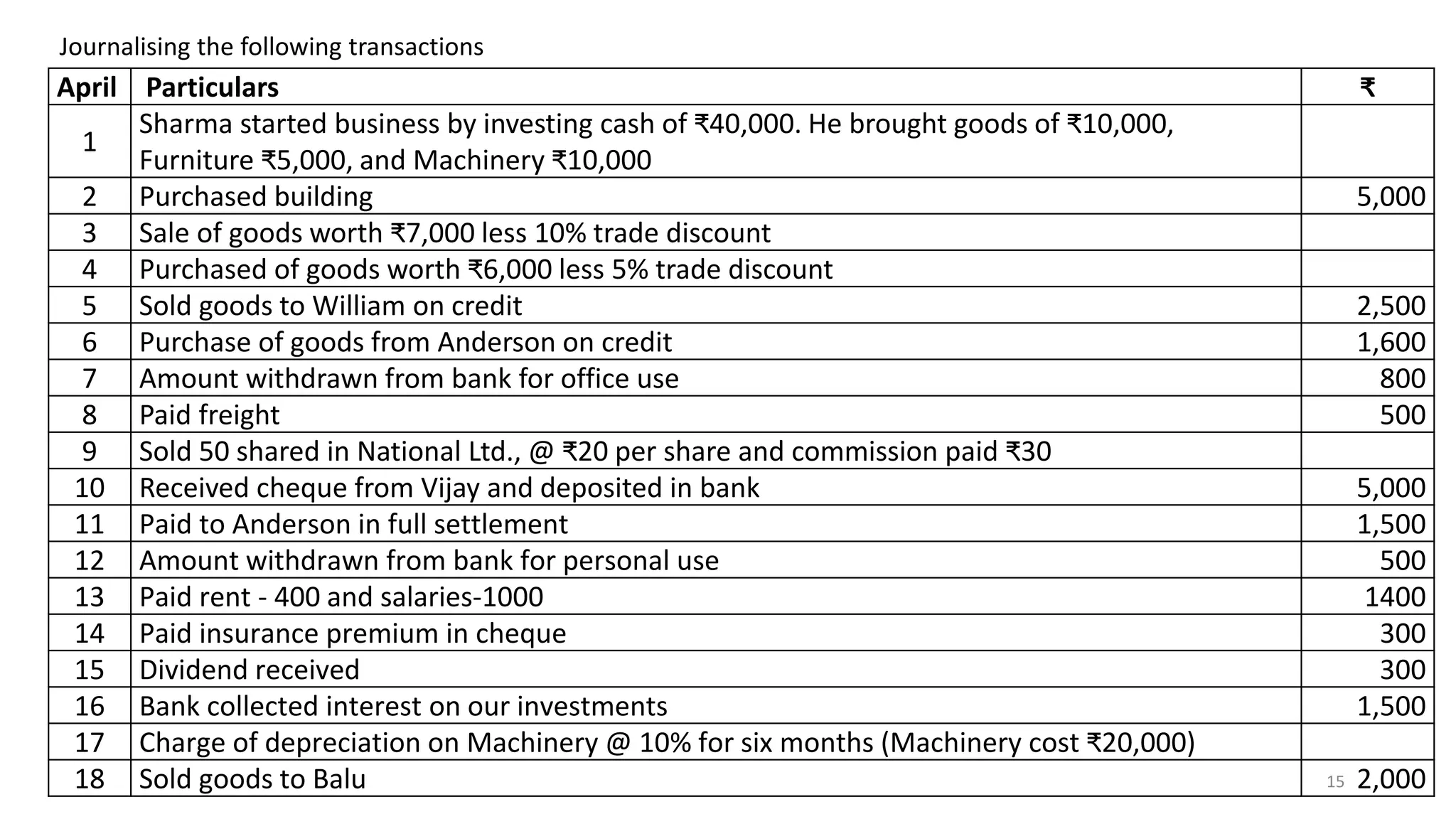

Journalising the followingtransactions

April Particulars ₹

1

Sharma started business by investing cash of ₹40,000. He brought goods of ₹10,000,

Furniture ₹5,000, and Machinery ₹10,000

2 Purchased building 5,000

3 Sale of goods worth ₹7,000 less 10% trade discount

4 Purchased of goods worth ₹6,000 less 5% trade discount

5 Sold goods to William on credit 2,500

6 Purchase of goods from Anderson on credit 1,600

7 Amount withdrawn from bank for office use 800

8 Paid freight 500

9 Sold 50 shared in National Ltd., @ ₹20 per share and commission paid ₹30

10 Received cheque from Vijay and deposited in bank 5,000

11 Paid to Anderson in full settlement 1,500

12 Amount withdrawn from bank for personal use 500

13 Paid rent - 400 and salaries-1000 1400

14 Paid insurance premium in cheque 300

15 Dividend received 300

16 Bank collected interest on our investments 1,500

17 Charge of depreciation on Machinery @ 10% for six months (Machinery cost ₹20,000)

18 Sold goods to Balu 2,000

16.

Ledger: Introduction

• Ledgeraccount is a summary statement of all the transactions relating to a person, asset, liability, expense or

income which has taken place during a given period of time and it shows their net effect.

• Quick information about a particular account

• Control over business transactions

• Trial balance can be prepared

• Helps to prepare financial statements

16

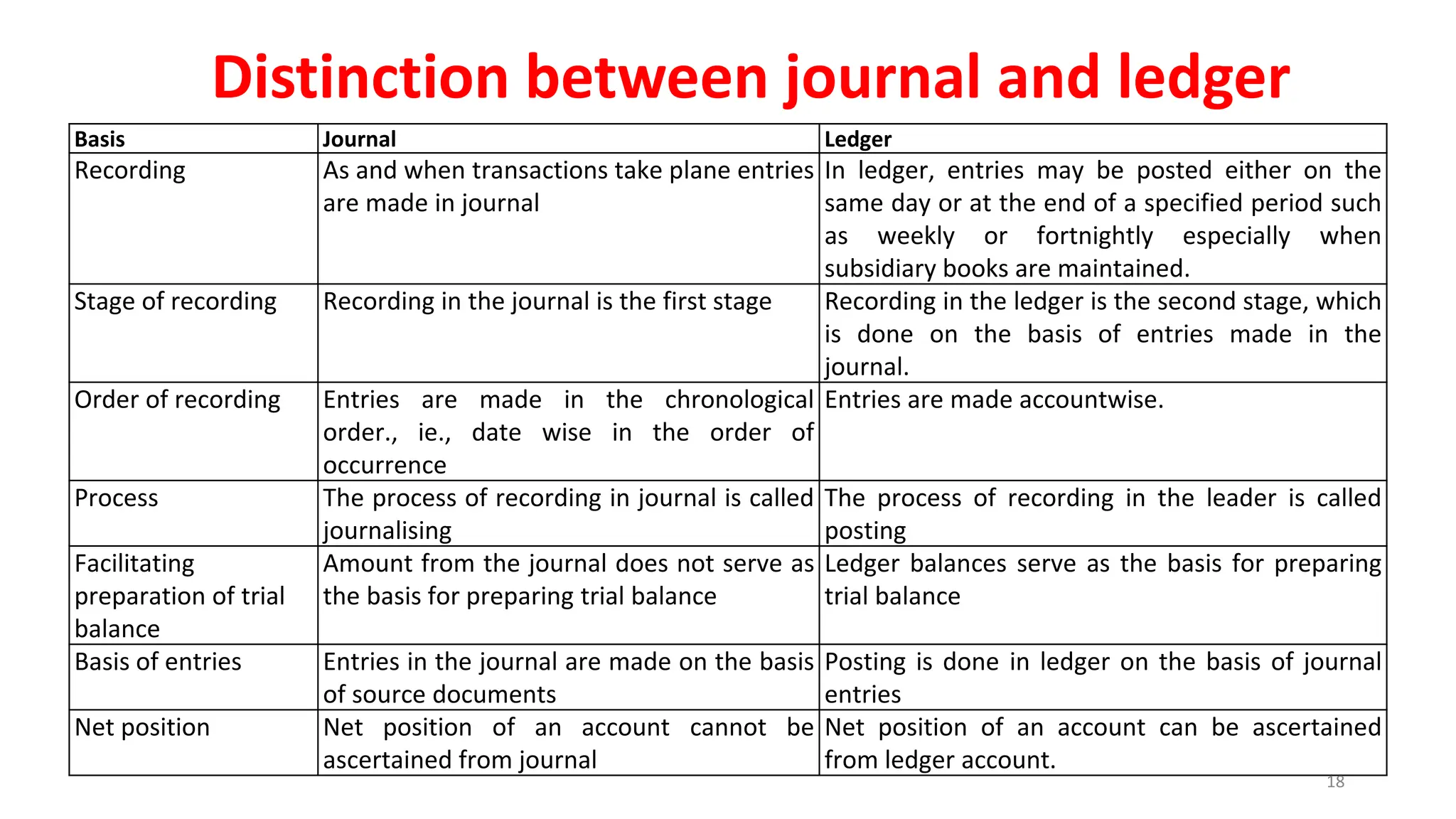

Distinction between journaland ledger

Basis Journal Ledger

Recording As and when transactions take plane entries

are made in journal

In ledger, entries may be posted either on the

same day or at the end of a specified period such

as weekly or fortnightly especially when

subsidiary books are maintained.

Stage of recording Recording in the journal is the first stage Recording in the ledger is the second stage, which

is done on the basis of entries made in the

journal.

Order of recording Entries are made in the chronological

order., ie., date wise in the order of

occurrence

Entries are made accountwise.

Process The process of recording in journal is called

journalising

The process of recording in the leader is called

posting

Facilitating

preparation of trial

balance

Amount from the journal does not serve as

the basis for preparing trial balance

Ledger balances serve as the basis for preparing

trial balance

Basis of entries Entries in the journal are made on the basis

of source documents

Posting is done in ledger on the basis of journal

entries

Net position Net position of an account cannot be

ascertained from journal

Net position of an account can be ascertained

from ledger account.

18

19.

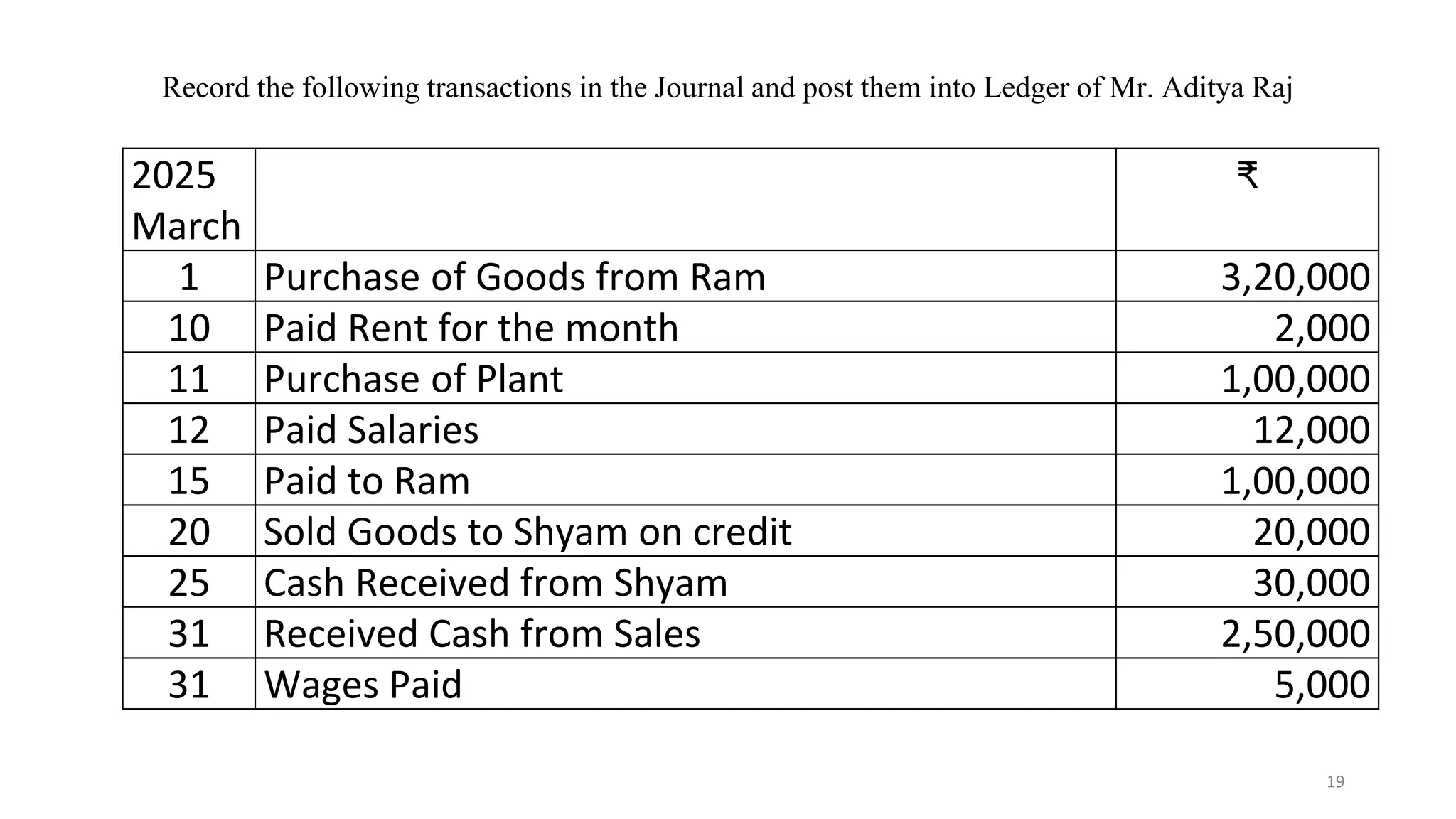

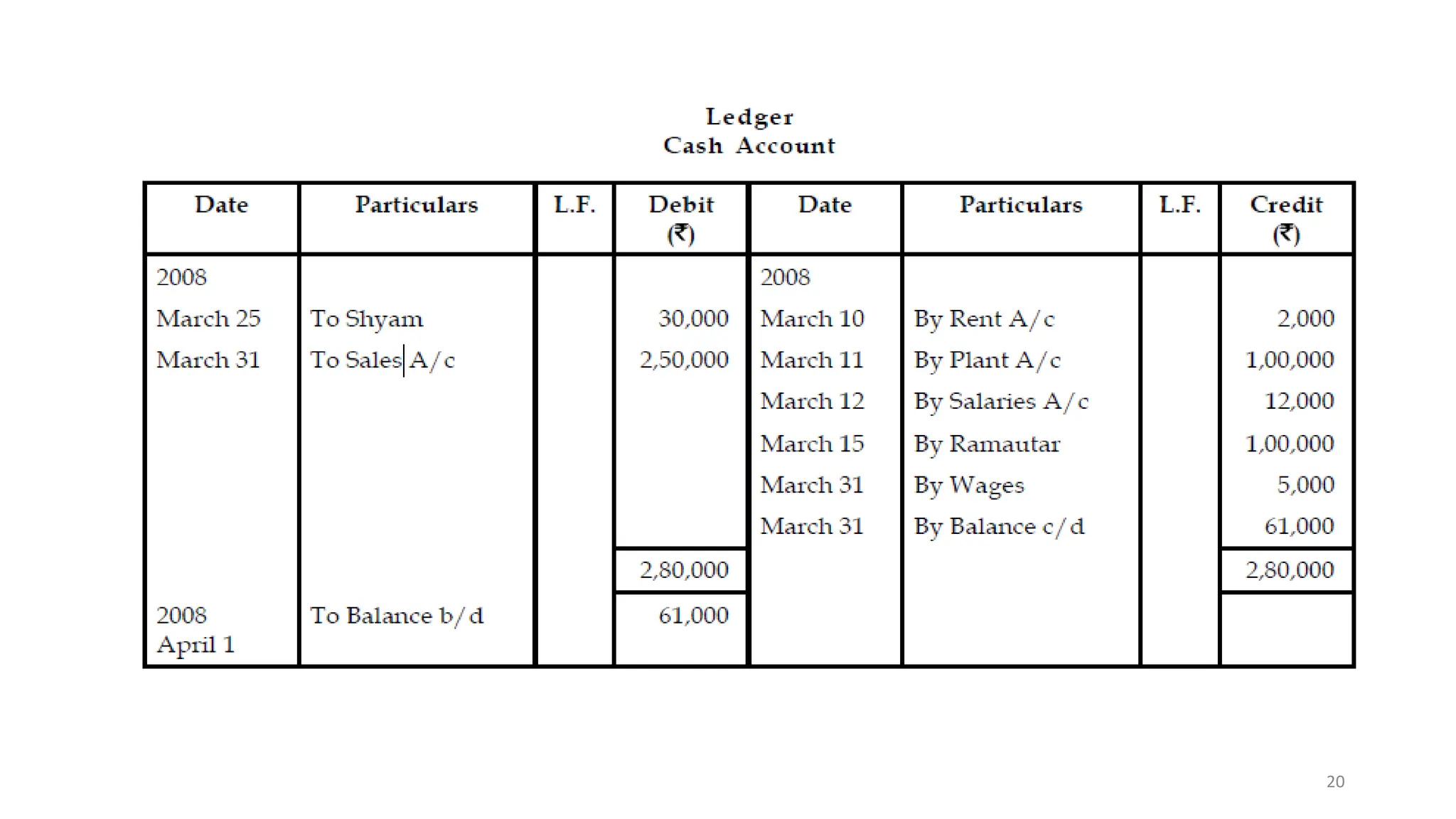

Record the followingtransactions in the Journal and post them into Ledger of Mr. Aditya Raj

2025

March

₹

1 Purchase of Goods from Ram 3,20,000

10 Paid Rent for the month 2,000

11 Purchase of Plant 1,00,000

12 Paid Salaries 12,000

15 Paid to Ram 1,00,000

20 Sold Goods to Shyam on credit 20,000

25 Cash Received from Shyam 30,000

31 Received Cash from Sales 2,50,000

31 Wages Paid 5,000

19

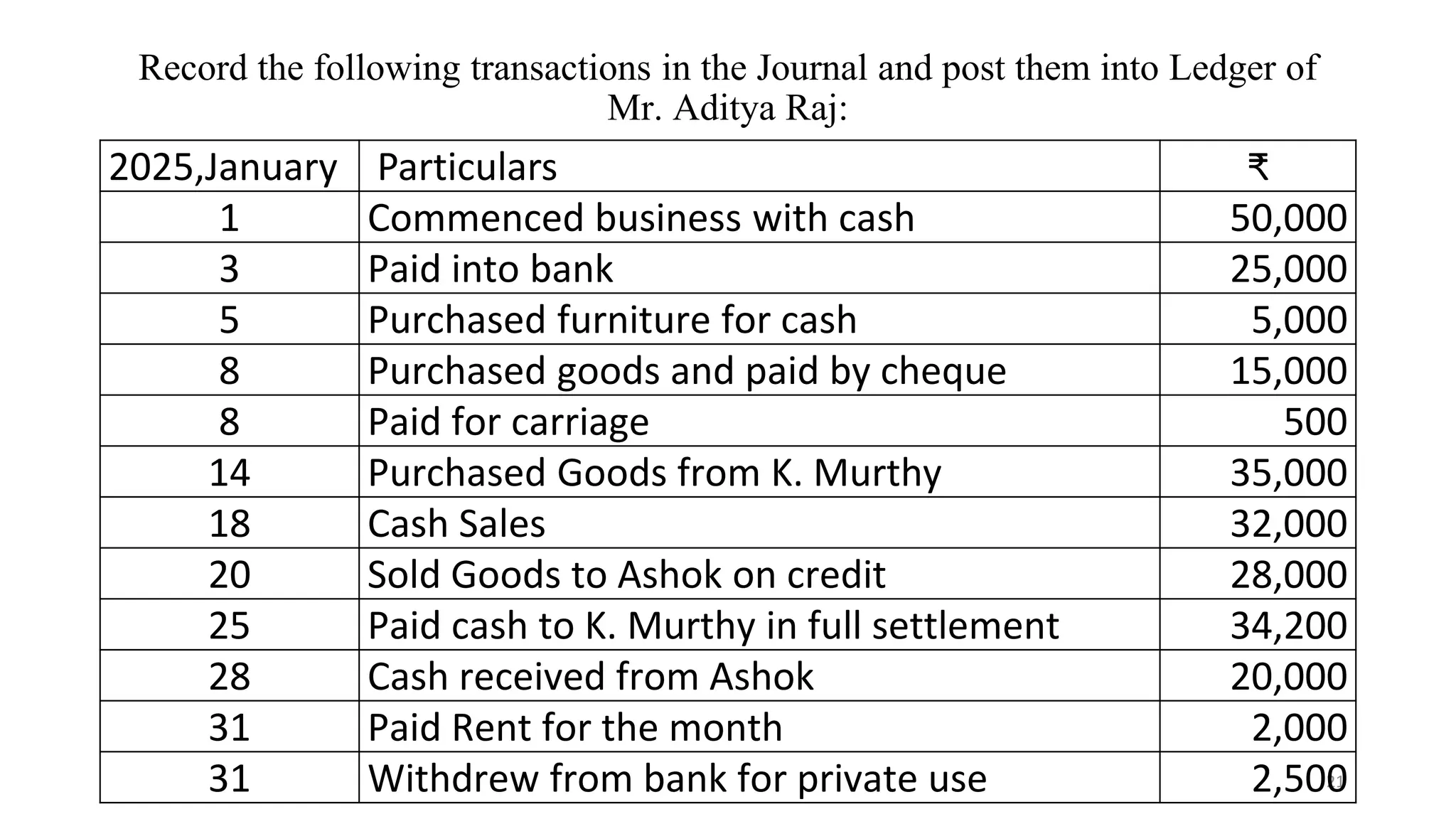

Record the followingtransactions in the Journal and post them into Ledger of

Mr. Aditya Raj:

21

2025,January Particulars ₹

1 Commenced business with cash 50,000

3 Paid into bank 25,000

5 Purchased furniture for cash 5,000

8 Purchased goods and paid by cheque 15,000

8 Paid for carriage 500

14 Purchased Goods from K. Murthy 35,000

18 Cash Sales 32,000

20 Sold Goods to Ashok on credit 28,000

25 Paid cash to K. Murthy in full settlement 34,200

28 Cash received from Ashok 20,000

31 Paid Rent for the month 2,000

31 Withdrew from bank for private use 2,500

22.

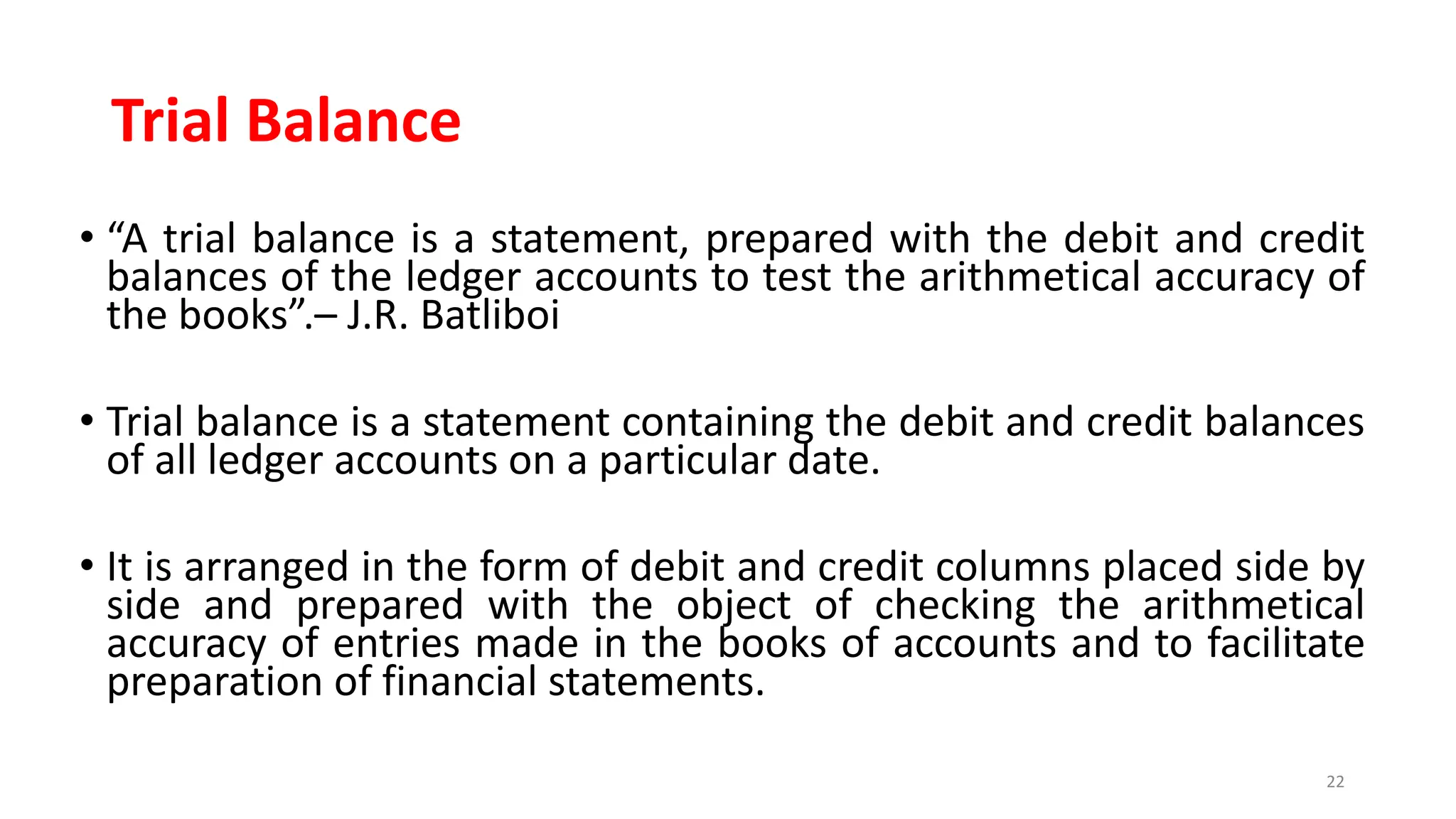

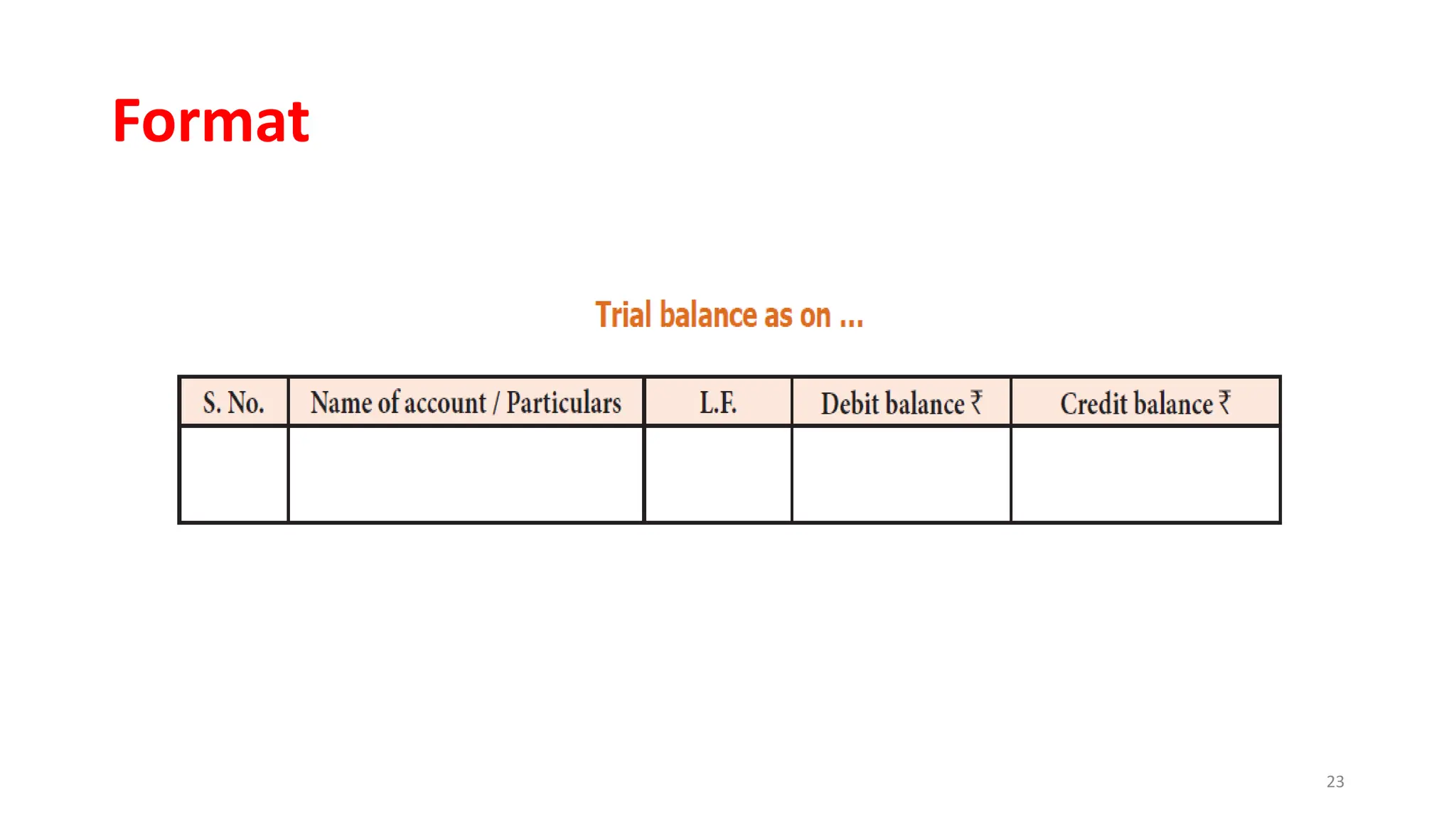

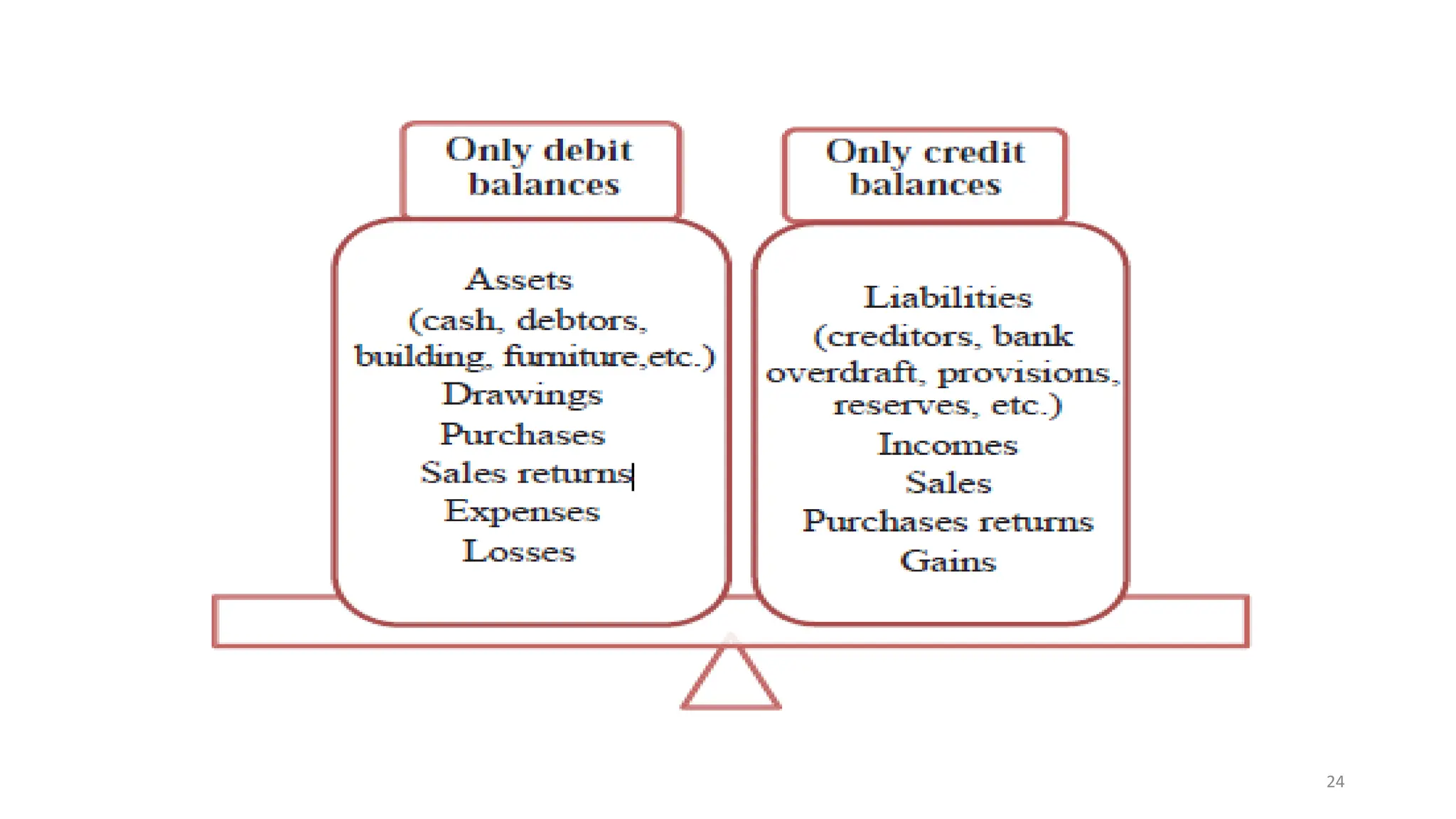

Trial Balance

• “Atrial balance is a statement, prepared with the debit and credit

balances of the ledger accounts to test the arithmetical accuracy of

the books”.– J.R. Batliboi

• Trial balance is a statement containing the debit and credit balances

of all ledger accounts on a particular date.

• It is arranged in the form of debit and credit columns placed side by

side and prepared with the object of checking the arithmetical

accuracy of entries made in the books of accounts and to facilitate

preparation of financial statements.

22

25

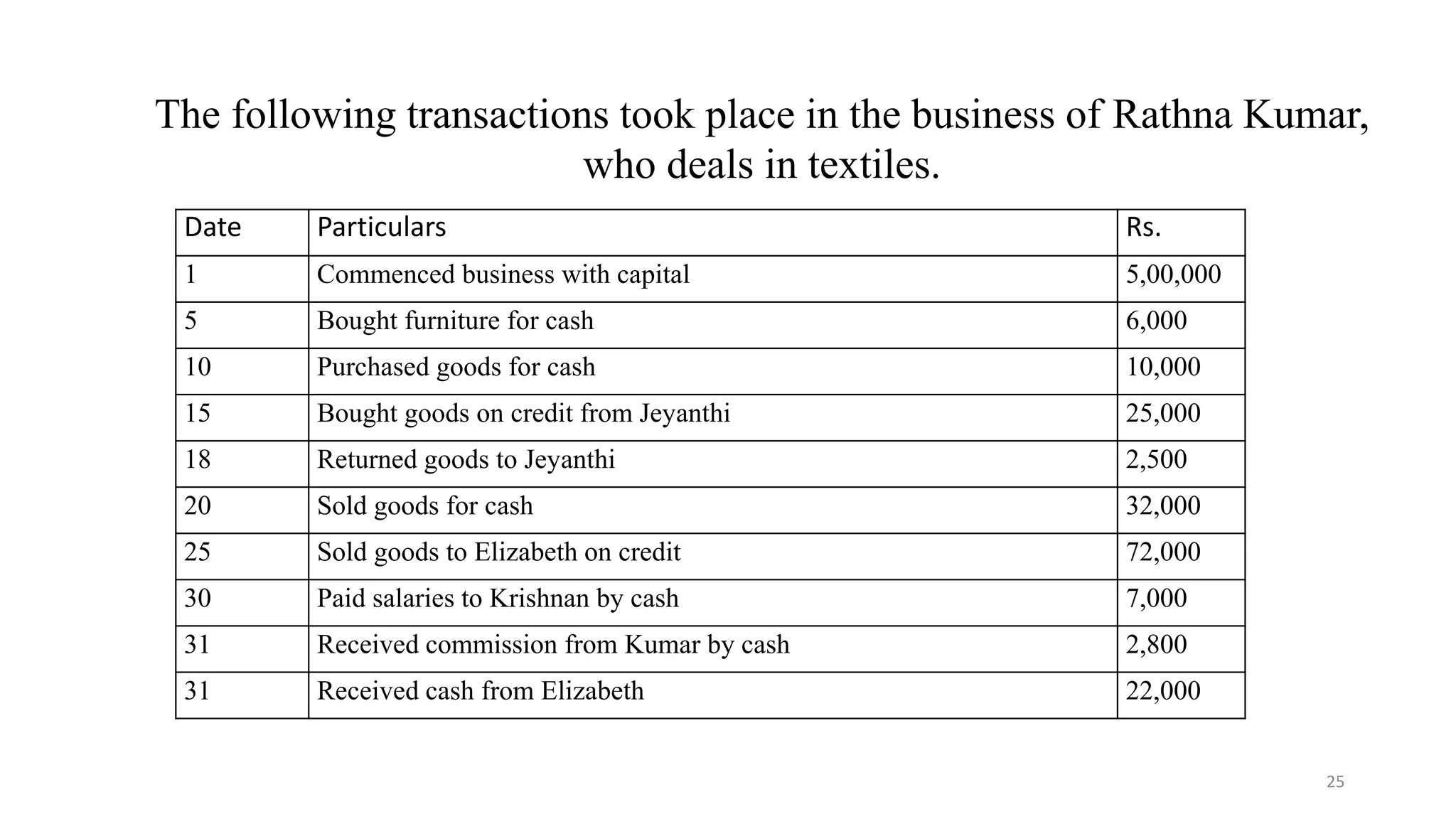

The following transactionstook place in the business of Rathna Kumar,

who deals in textiles.

Date Particulars Rs.

1 Commenced business with capital 5,00,000

5 Bought furniture for cash 6,000

10 Purchased goods for cash 10,000

15 Bought goods on credit from Jeyanthi 25,000

18 Returned goods to Jeyanthi 2,500

20 Sold goods for cash 32,000

25 Sold goods to Elizabeth on credit 72,000

30 Paid salaries to Krishnan by cash 7,000

31 Received commission from Kumar by cash 2,800

31 Received cash from Elizabeth 22,000