Meaning of Amalgamation

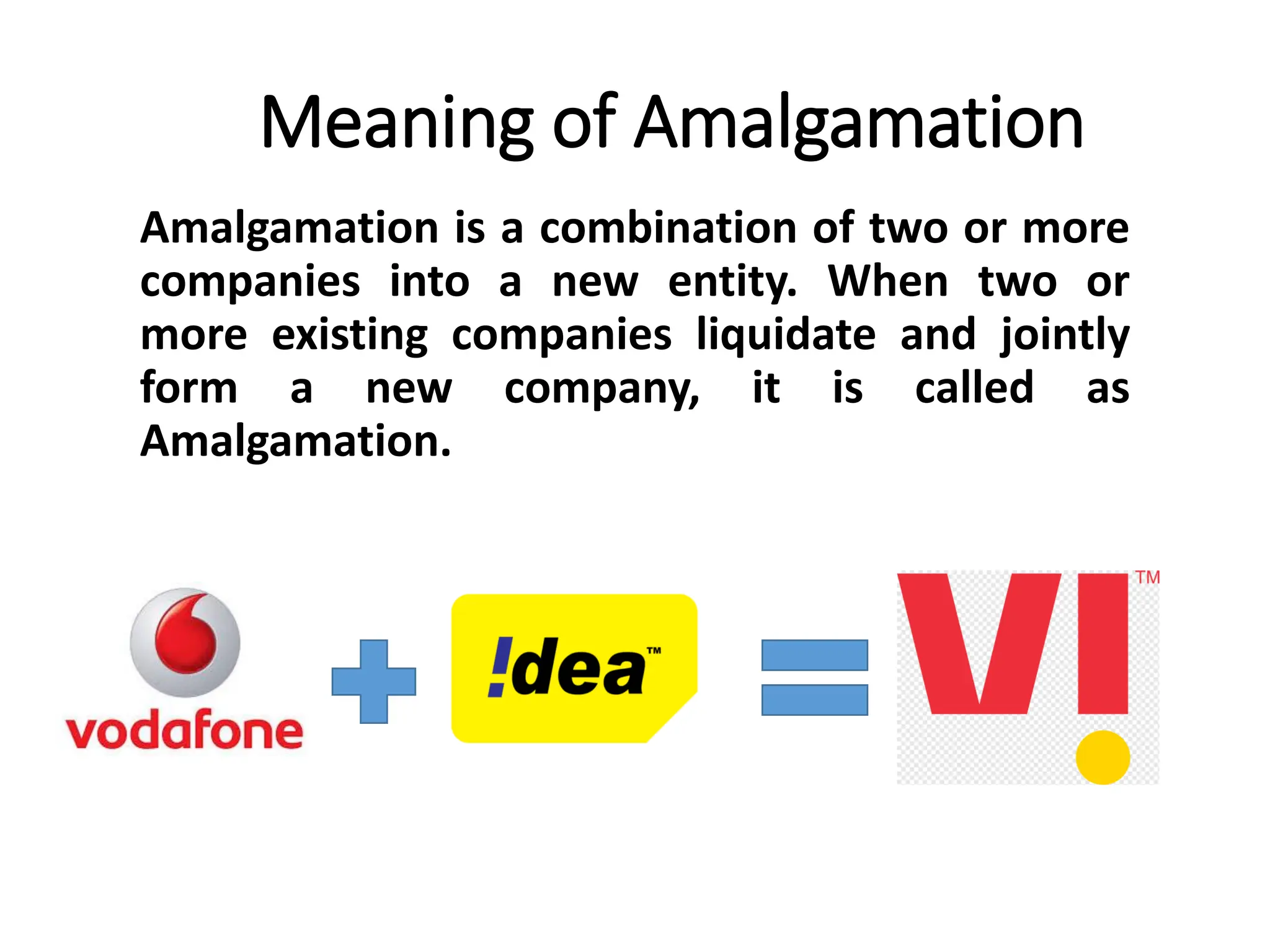

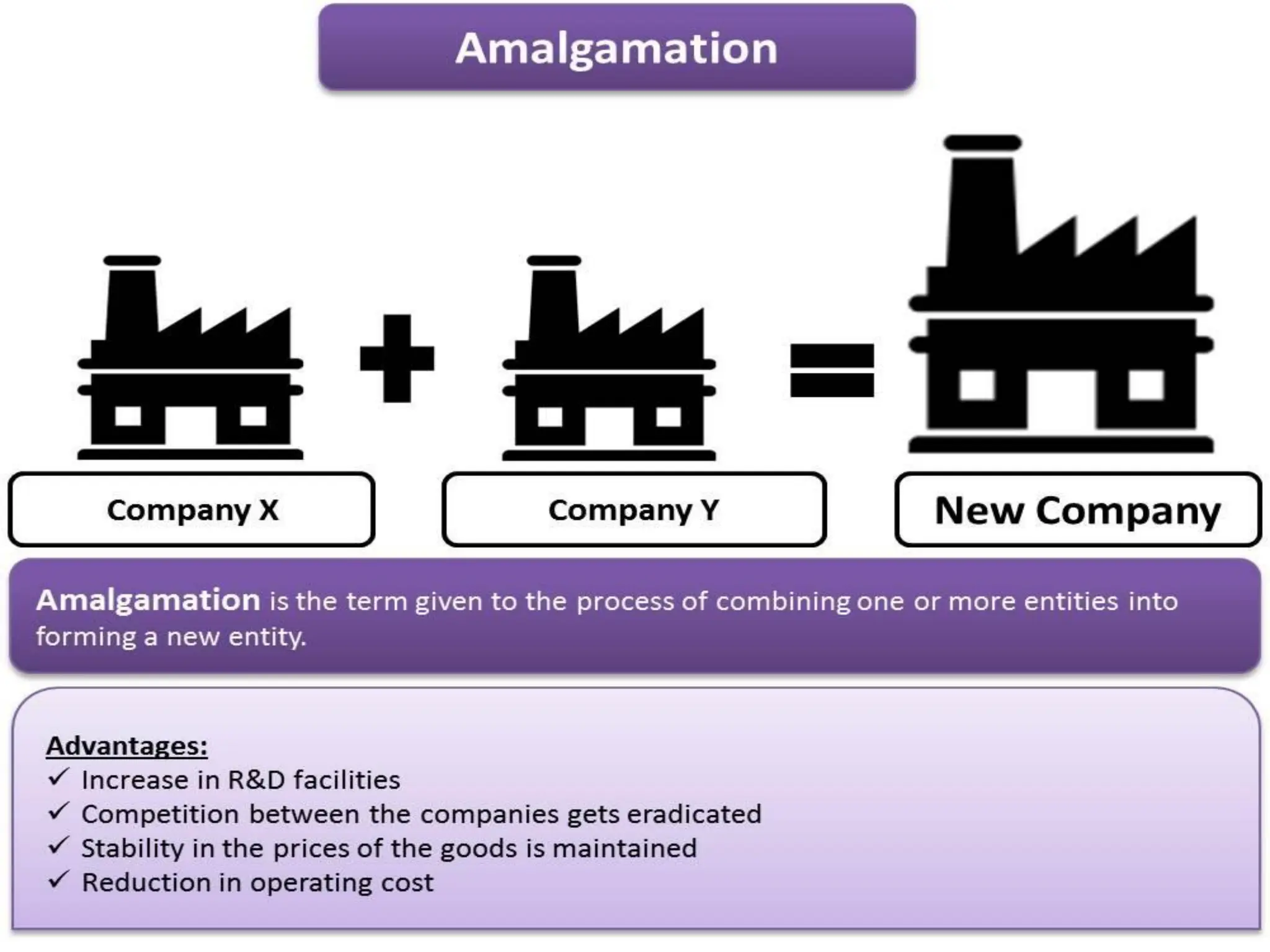

Amalgamationis a combination of two or more

companies into a new entity. When two or

more existing companies liquidate and jointly

form a new company, it is called as

Amalgamation.

4.

Amalgamation….

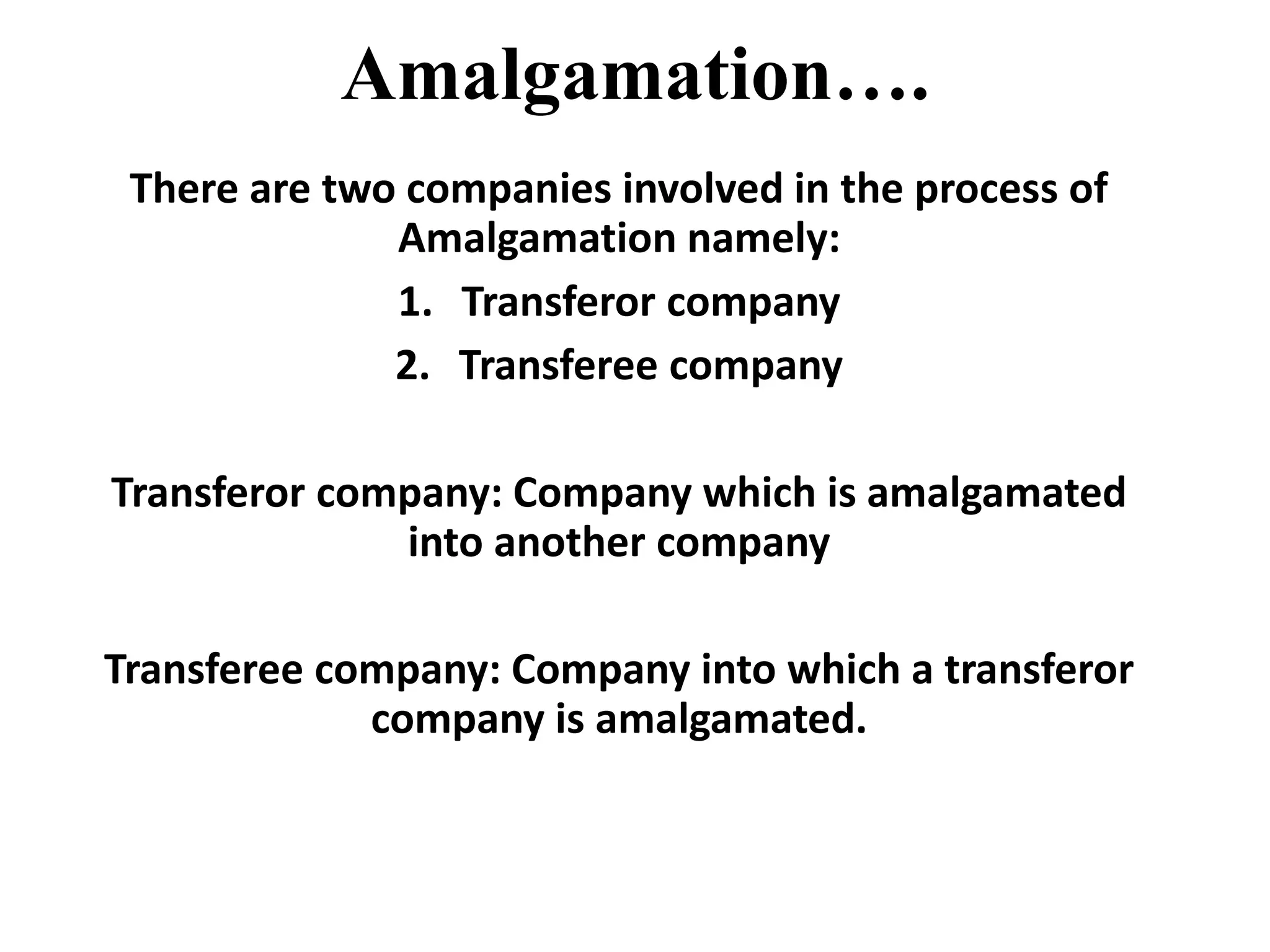

There are twocompanies involved in the process of

Amalgamation namely:

1. Transferor company

2. Transferee company

Transferor company: Company which is amalgamated

into another company

Transferee company: Company into which a transferor

company is amalgamated.

5.

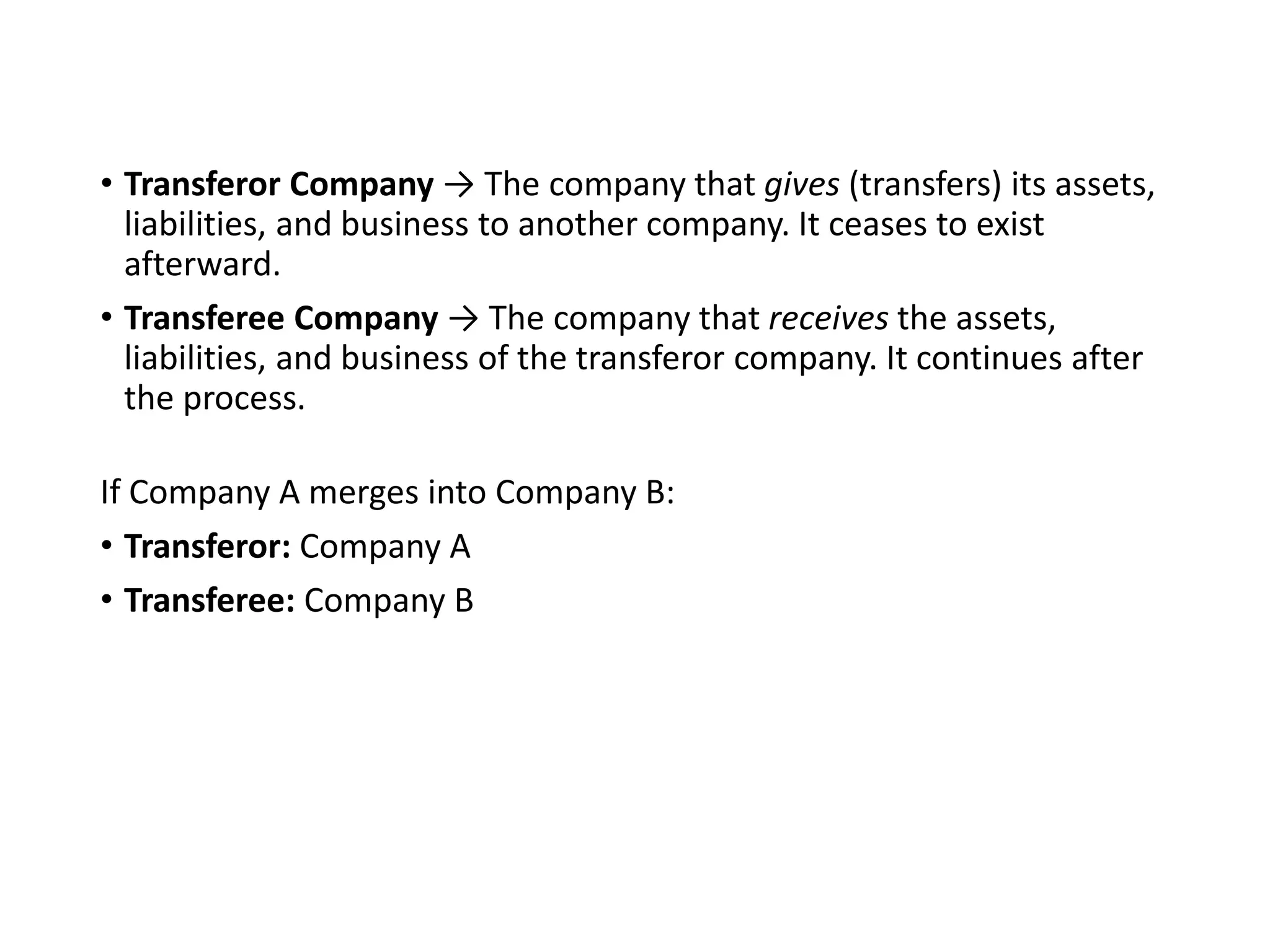

• Transferor Company→ The company that gives (transfers) its assets,

liabilities, and business to another company. It ceases to exist

afterward.

• Transferee Company → The company that receives the assets,

liabilities, and business of the transferor company. It continues after

the process.

If Company A merges into Company B:

• Transferor: Company A

• Transferee: Company B

6.

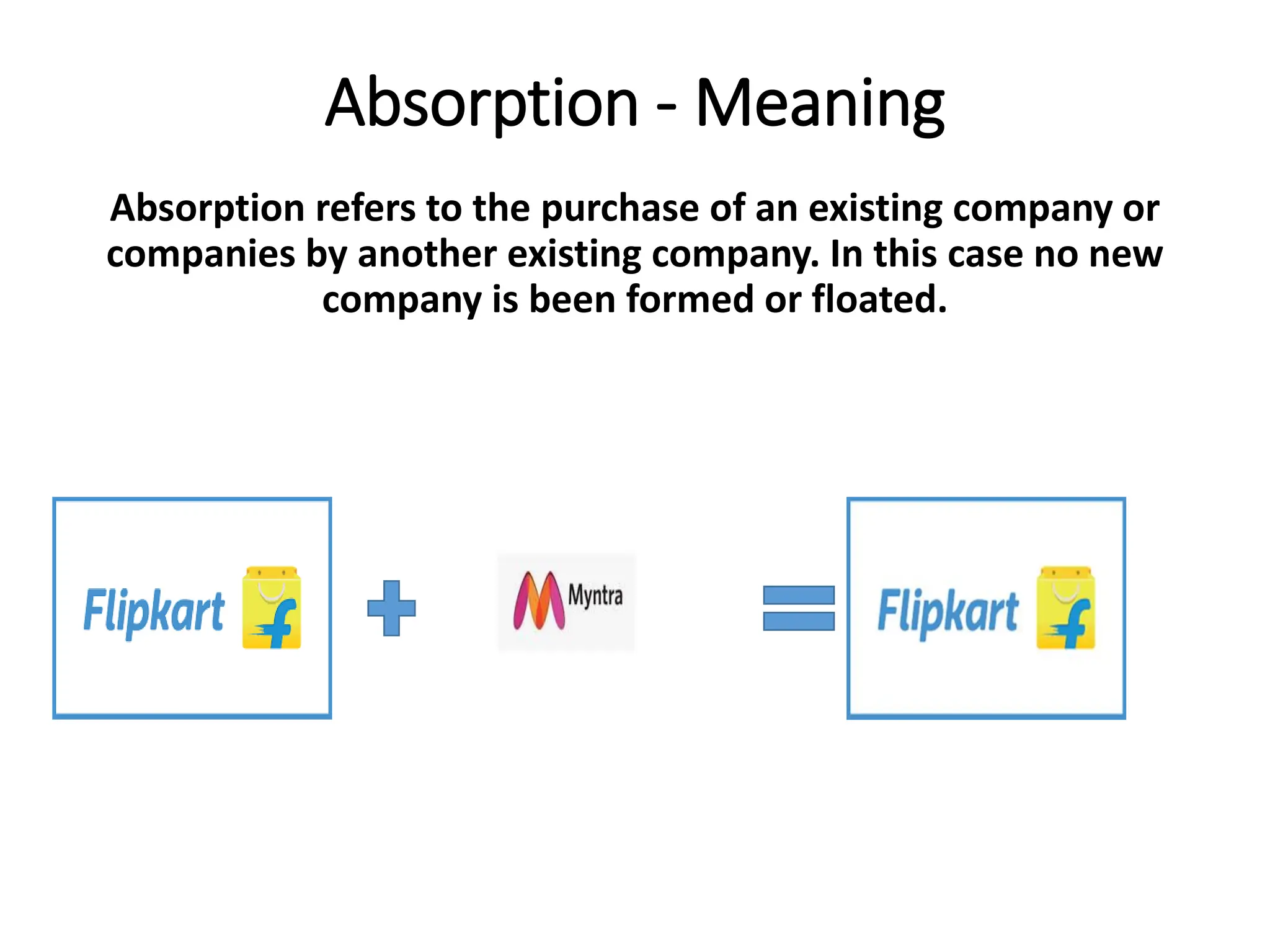

Absorption - Meaning

Absorptionrefers to the purchase of an existing company or

companies by another existing company. In this case no new

company is been formed or floated.

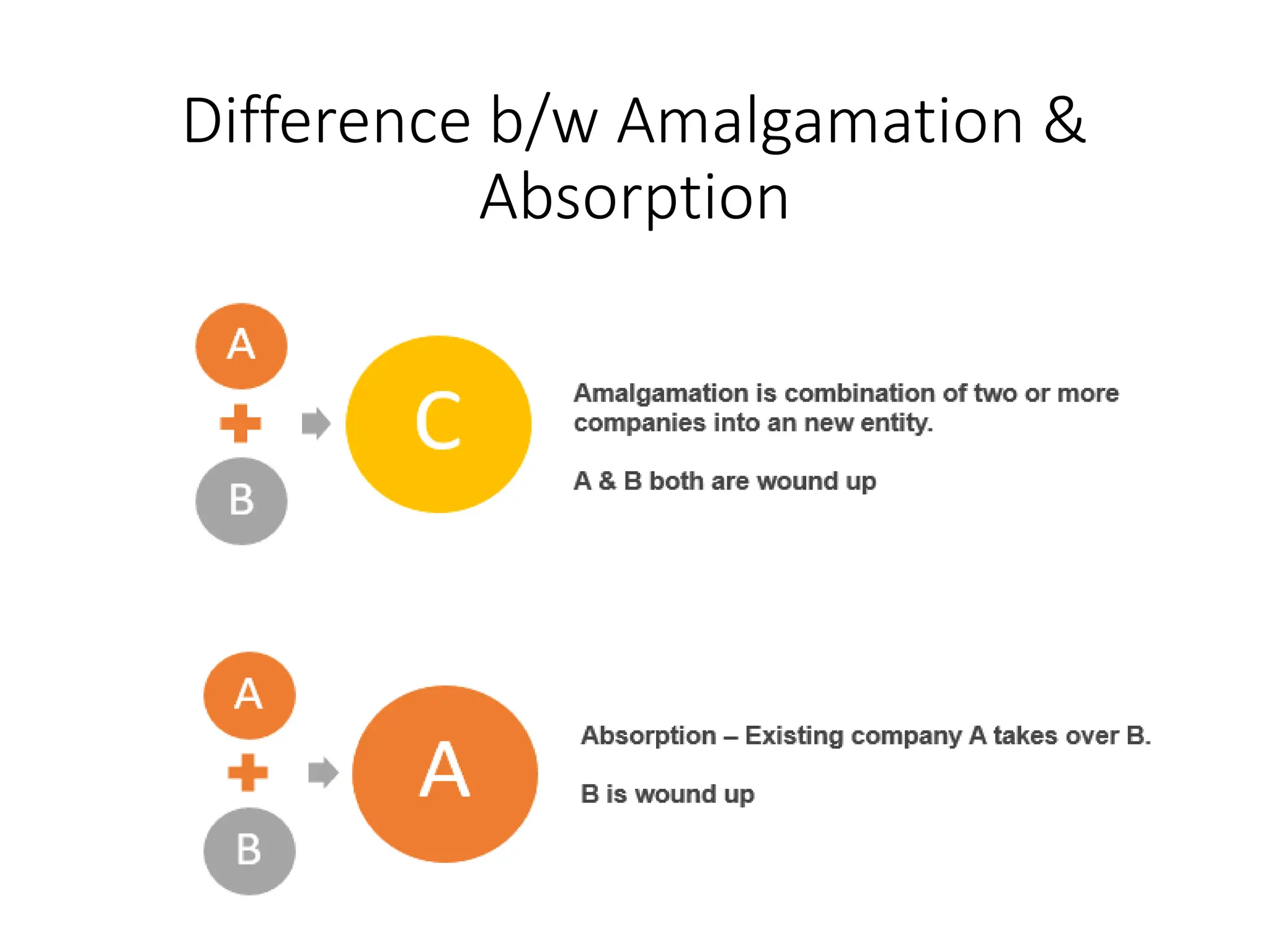

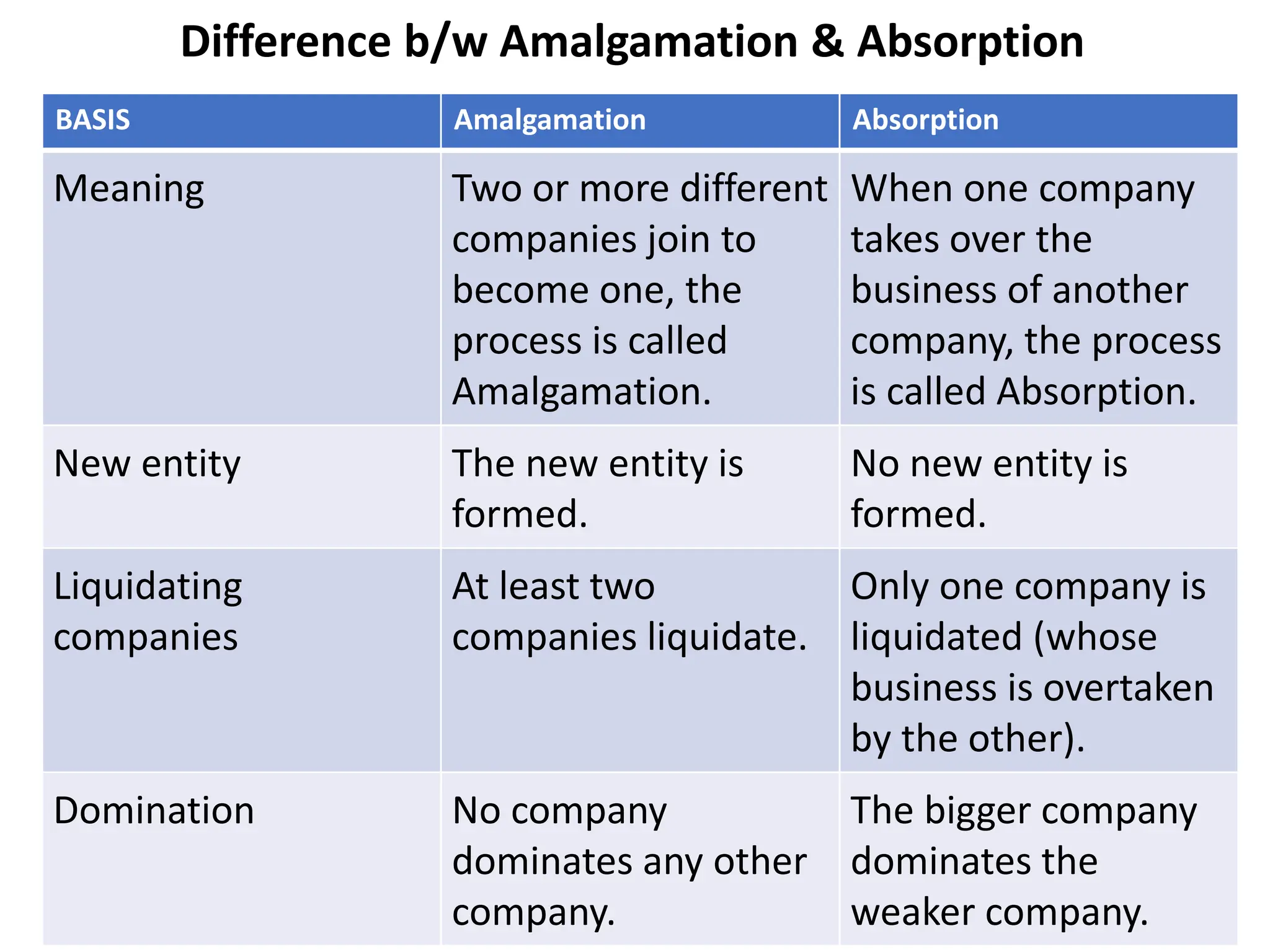

Difference b/w Amalgamation& Absorption

BASIS Amalgamation Absorption

Meaning Two or more different

companies join to

become one, the

process is called

Amalgamation.

When one company

takes over the

business of another

company, the process

is called Absorption.

New entity The new entity is

formed.

No new entity is

formed.

Liquidating

companies

At least two

companies liquidate.

Only one company is

liquidated (whose

business is overtaken

by the other).

Domination No company

dominates any other

company.

The bigger company

dominates the

weaker company.

10.

Types of Amalgamation

Accordingto Accounting Standard 14 issued by ICAI

amalgamation are of two types:

Amalgamation in the nature of Merger

Amalgamation in the nature of Purchase.

11.

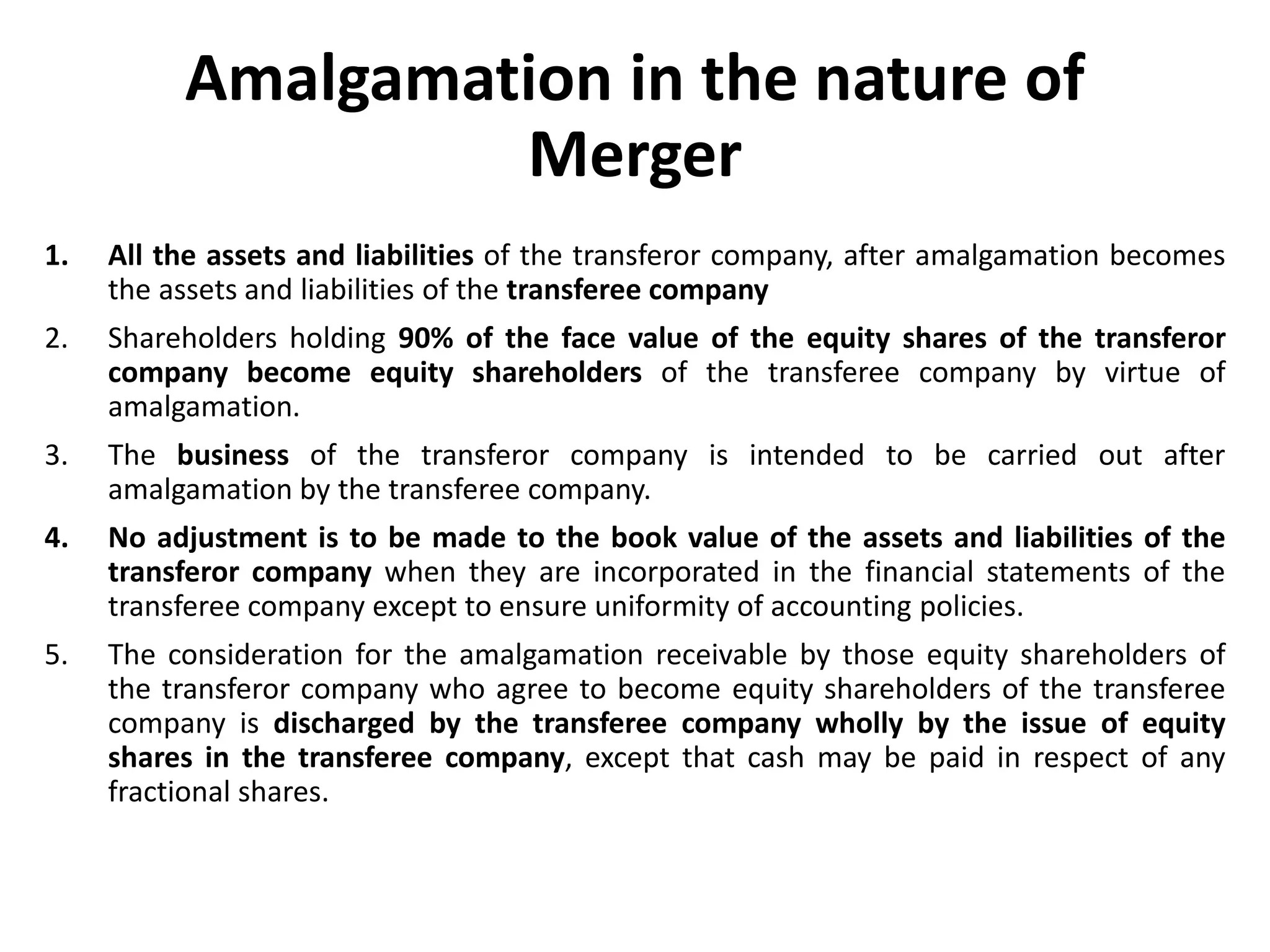

Amalgamation in thenature of

Merger

1. All the assets and liabilities of the transferor company, after amalgamation becomes

the assets and liabilities of the transferee company

2. Shareholders holding 90% of the face value of the equity shares of the transferor

company become equity shareholders of the transferee company by virtue of

amalgamation.

3. The business of the transferor company is intended to be carried out after

amalgamation by the transferee company.

4. No adjustment is to be made to the book value of the assets and liabilities of the

transferor company when they are incorporated in the financial statements of the

transferee company except to ensure uniformity of accounting policies.

5. The consideration for the amalgamation receivable by those equity shareholders of

the transferor company who agree to become equity shareholders of the transferee

company is discharged by the transferee company wholly by the issue of equity

shares in the transferee company, except that cash may be paid in respect of any

fractional shares.

12.

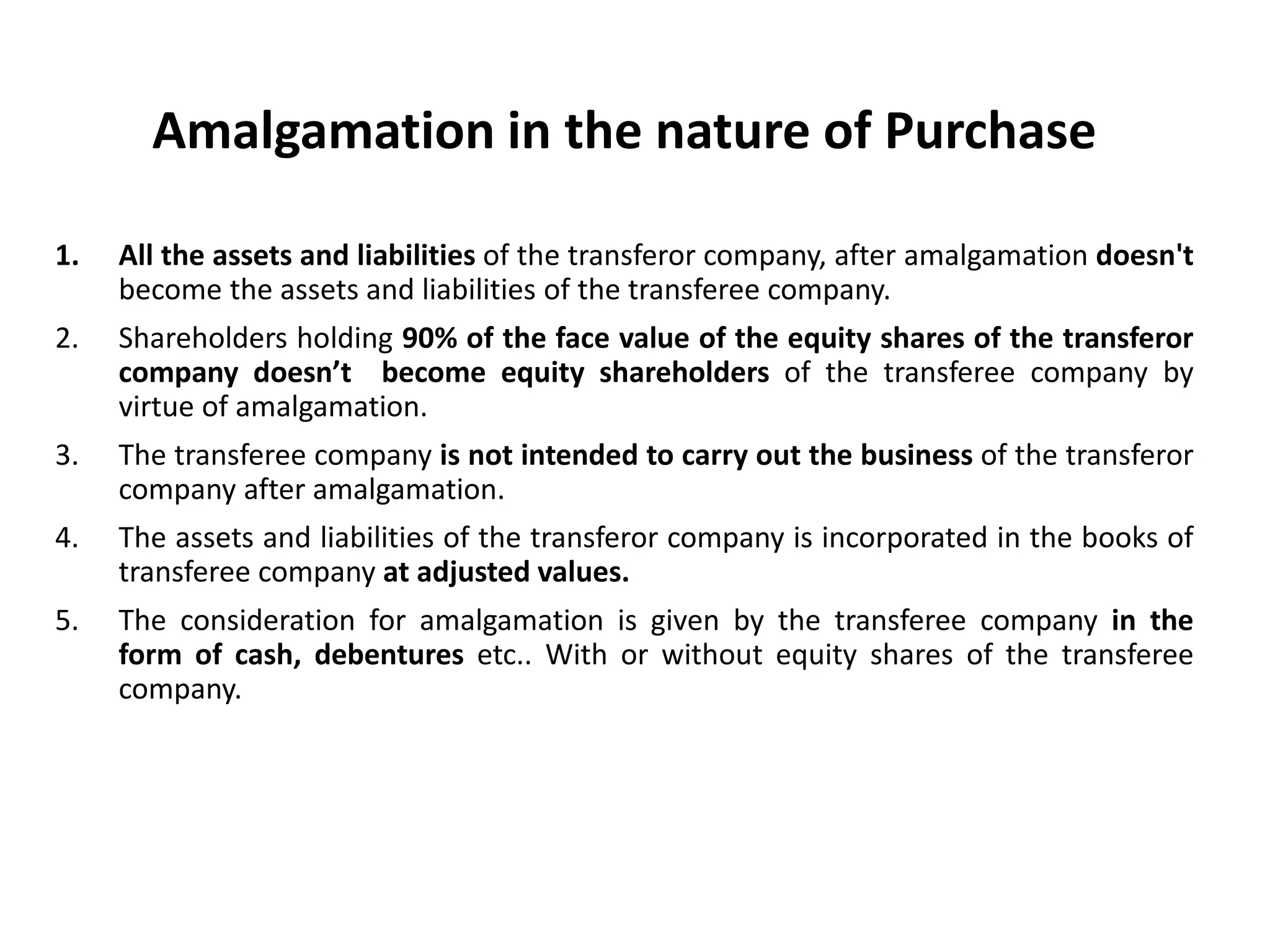

Amalgamation in thenature of Purchase

1. All the assets and liabilities of the transferor company, after amalgamation doesn't

become the assets and liabilities of the transferee company.

2. Shareholders holding 90% of the face value of the equity shares of the transferor

company doesn’t become equity shareholders of the transferee company by

virtue of amalgamation.

3. The transferee company is not intended to carry out the business of the transferor

company after amalgamation.

4. The assets and liabilities of the transferor company is incorporated in the books of

transferee company at adjusted values.

5. The consideration for amalgamation is given by the transferee company in the

form of cash, debentures etc.. With or without equity shares of the transferee

company.

13.

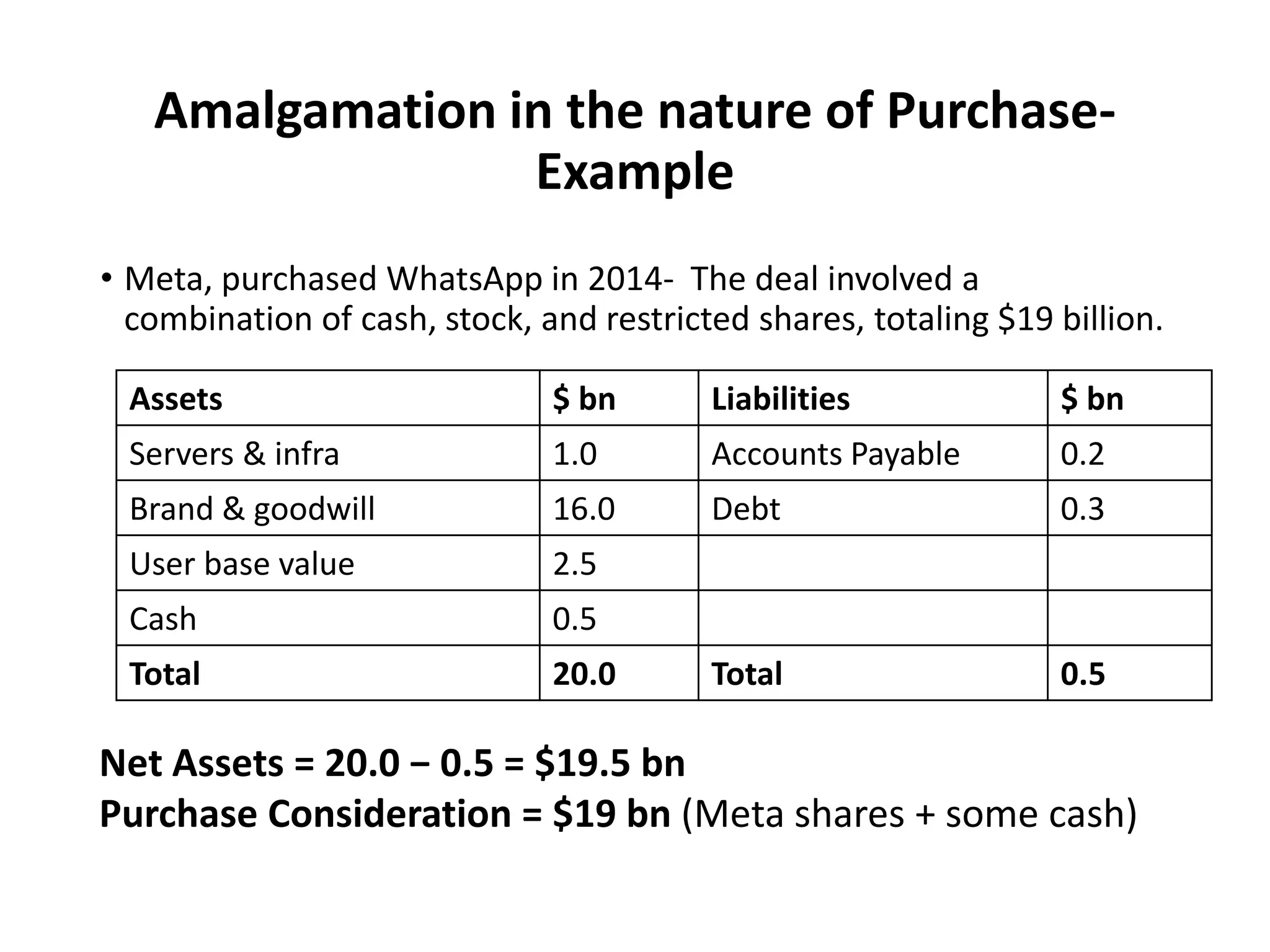

• Meta, purchasedWhatsApp in 2014- The deal involved a

combination of cash, stock, and restricted shares, totaling $19 billion.

Amalgamation in the nature of Purchase-

Example

Assets $ bn Liabilities $ bn

Servers & infra 1.0 Accounts Payable 0.2

Brand & goodwill 16.0 Debt 0.3

User base value 2.5

Cash 0.5

Total 20.0 Total 0.5

Net Assets = 20.0 − 0.5 = $19.5 bn

Purchase Consideration = $19 bn (Meta shares + some cash)

14.

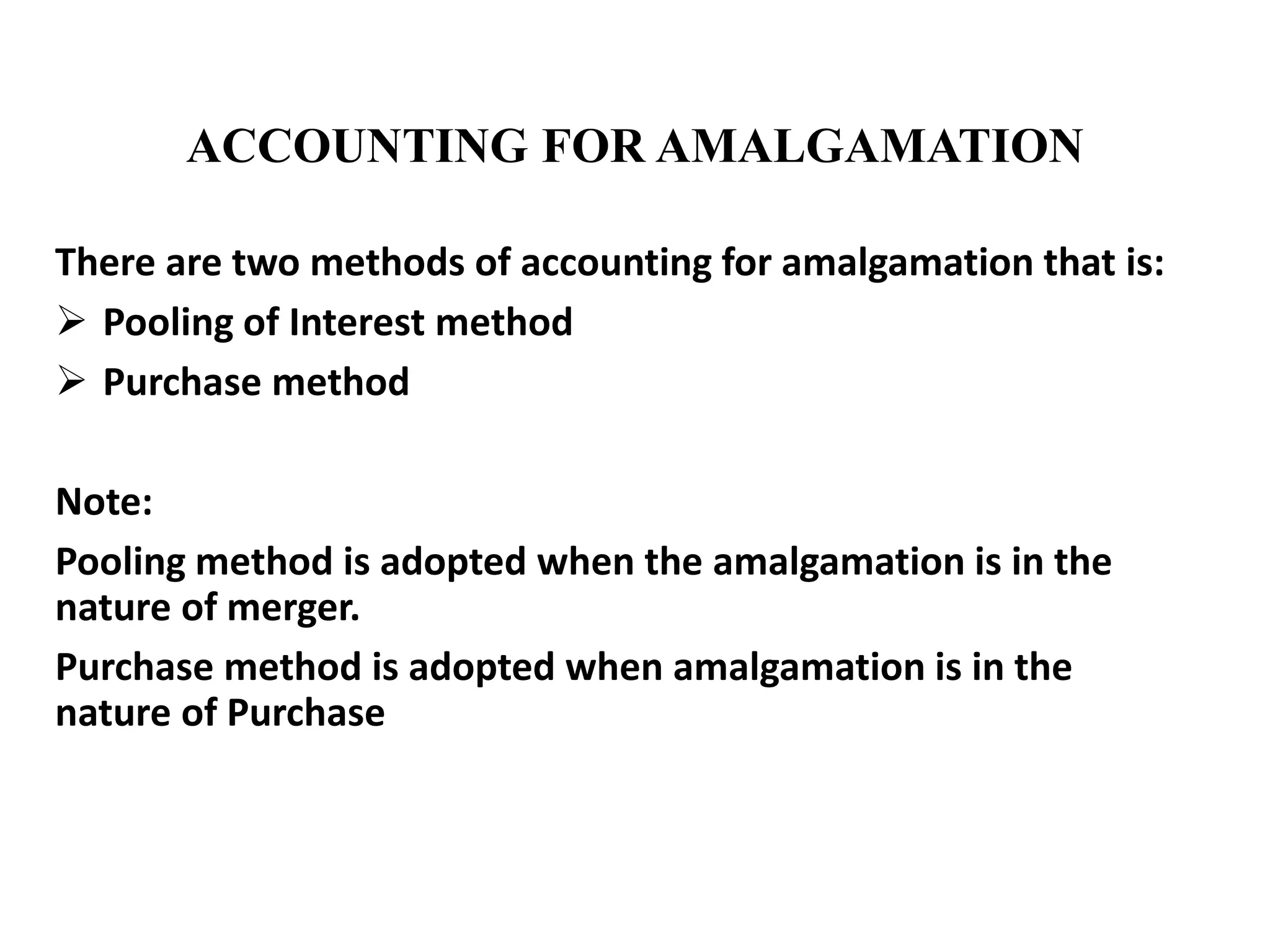

ACCOUNTING FOR AMALGAMATION

Thereare two methods of accounting for amalgamation that is:

Pooling of Interest method

Purchase method

Note:

Pooling method is adopted when the amalgamation is in the

nature of merger.

Purchase method is adopted when amalgamation is in the

nature of Purchase

15.

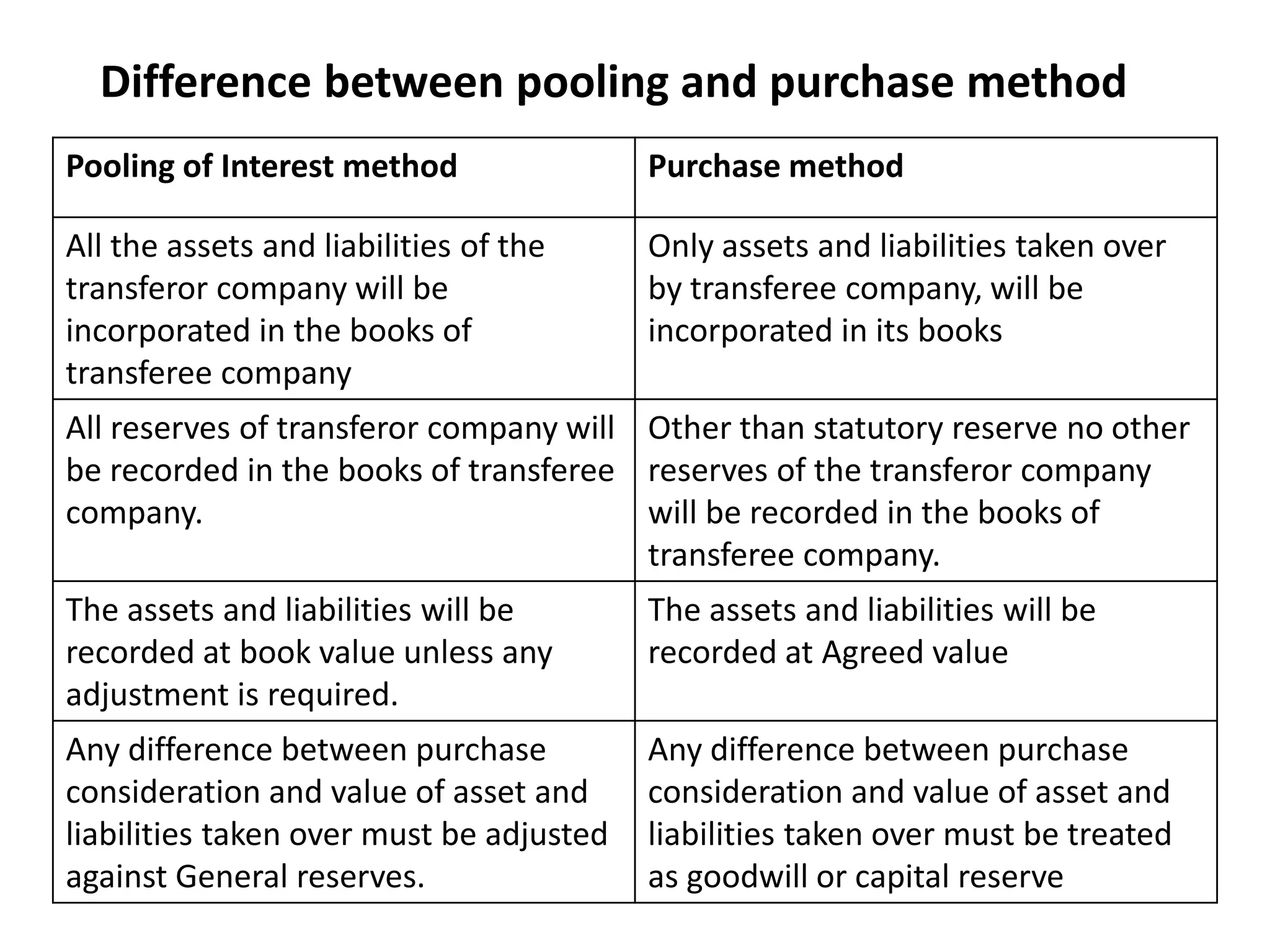

Difference between poolingand purchase method

Pooling of Interest method Purchase method

All the assets and liabilities of the

transferor company will be

incorporated in the books of

transferee company

Only assets and liabilities taken over

by transferee company, will be

incorporated in its books

All reserves of transferor company will

be recorded in the books of transferee

company.

Other than statutory reserve no other

reserves of the transferor company

will be recorded in the books of

transferee company.

The assets and liabilities will be

recorded at book value unless any

adjustment is required.

The assets and liabilities will be

recorded at Agreed value

Any difference between purchase

consideration and value of asset and

liabilities taken over must be adjusted

against General reserves.

Any difference between purchase

consideration and value of asset and

liabilities taken over must be treated

as goodwill or capital reserve

16.

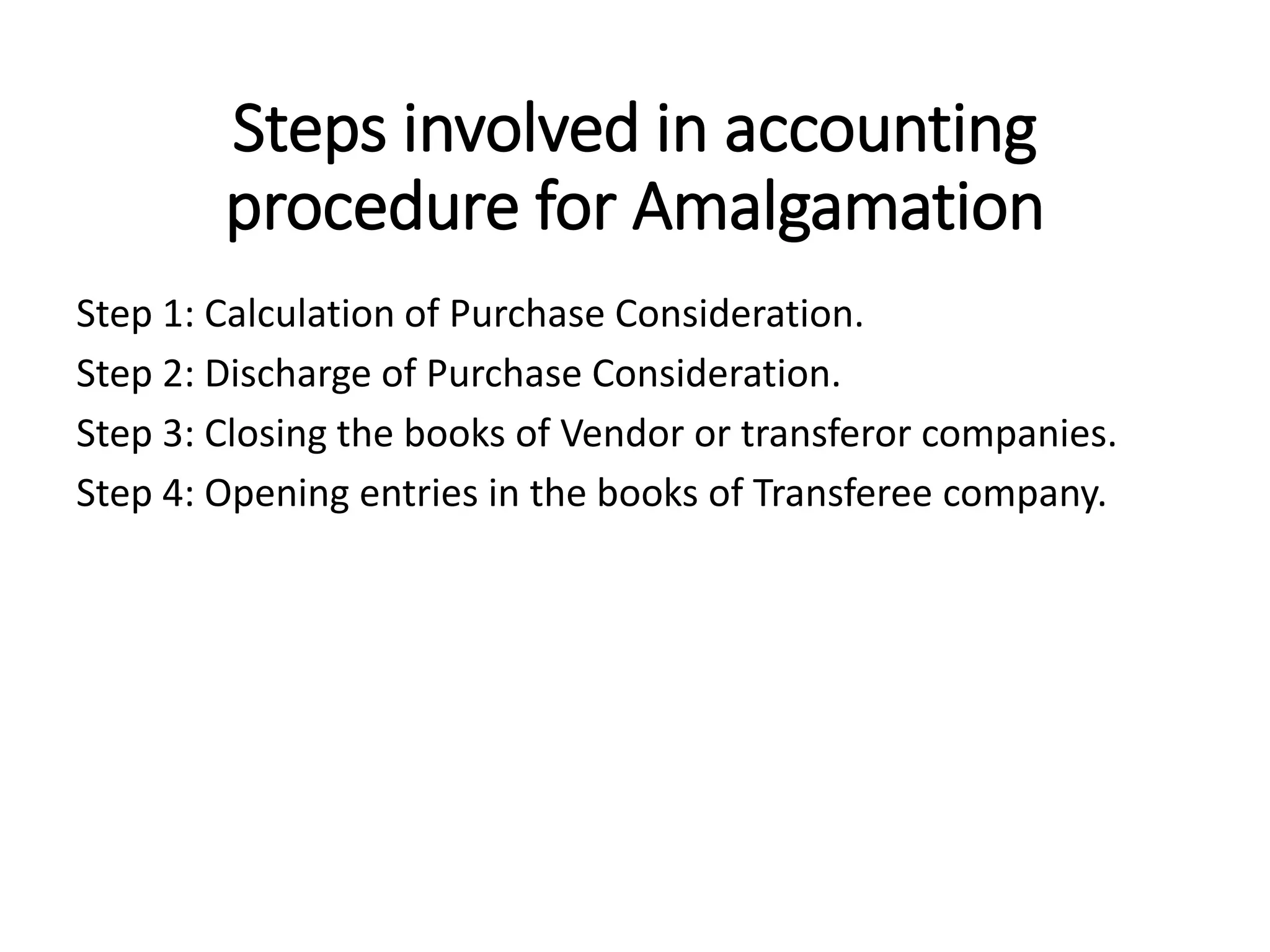

Steps involved inaccounting

procedure for Amalgamation

Step 1: Calculation of Purchase Consideration.

Step 2: Discharge of Purchase Consideration.

Step 3: Closing the books of Vendor or transferor companies.

Step 4: Opening entries in the books of Transferee company.

17.

Purchase Consideration

Purchase considerationis the agreed amount which

transferee company (Purchasing company) pays to the

transferor company (Vendor company) in exchange of the

ownership of the transferor company.

It may be in form of cash, shares or any other assets as

agreed between both the companies.

18.

Methods of calculatingPC

1. Lump Sum Method

2. Net Worth or Net Assets Method

3. Net Payment Method

4. Other basis for purchase consideration

Intrinsic value

Exchange ratio

19.

1. Lump summethod

In this method when Transferee Company

agrees to pay Transferor Company a fixed sum of

money.

Ex: ABC limited agrees to pay XYZ ltd 50 lakh.

This is lump sum method.

20.

2. Net PaymentMethod

In this method purchase consideration is calculated by adding all the

payments made by the transferee company to the shareholders of the

transferor company. Payment can be in the form of cash, shares or

debentures.

Note:

Value of assets and liabilities taken over by the transferee company

are not to be consider

Liquidation expenses paid by the transferee company should not

consider

Amount paid to third party by the transferee company should not

consider

21.

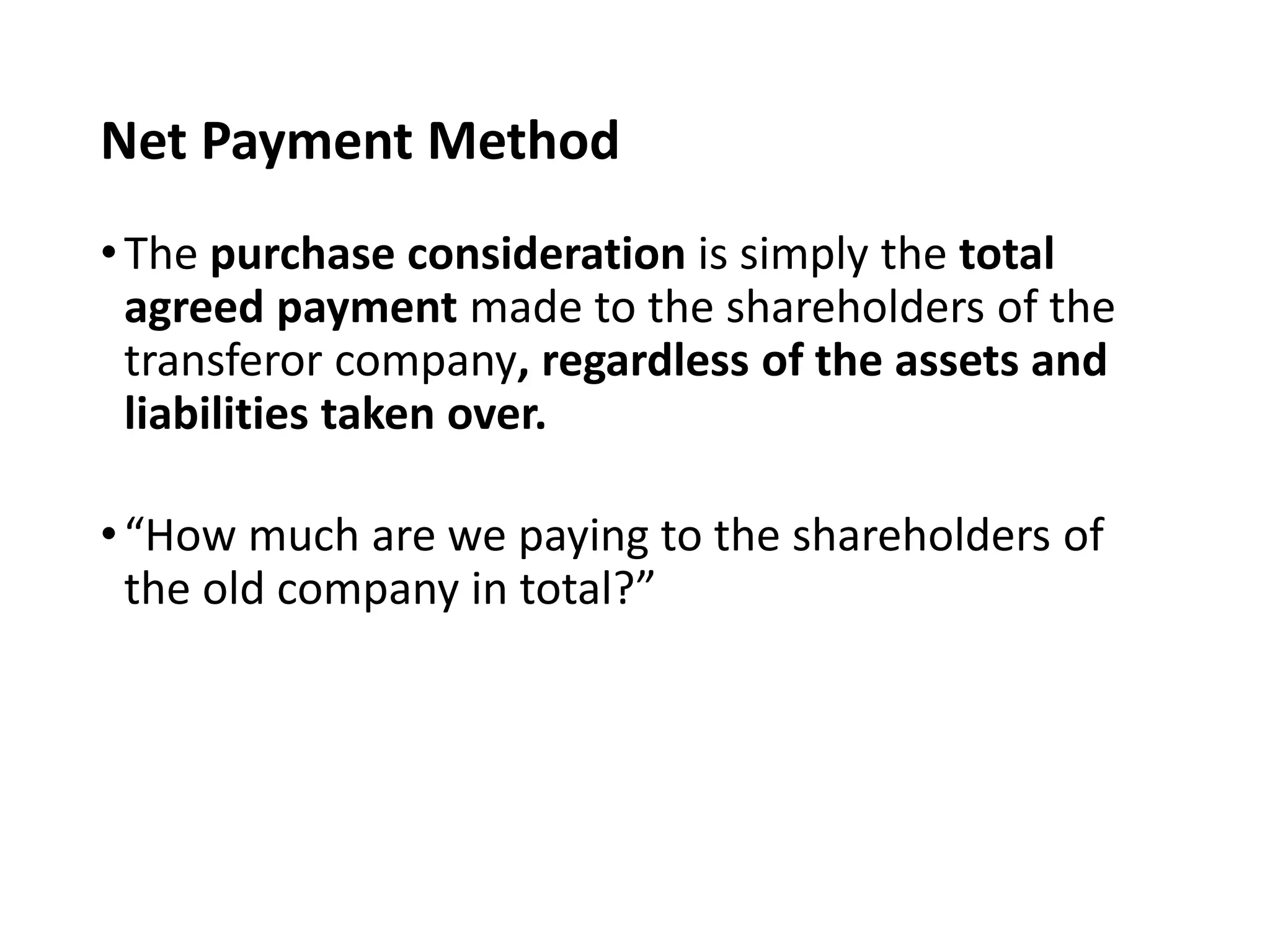

Net Payment Method

•Thepurchase consideration is simply the total

agreed payment made to the shareholders of the

transferor company, regardless of the assets and

liabilities taken over.

•“How much are we paying to the shareholders of

the old company in total?”

22.

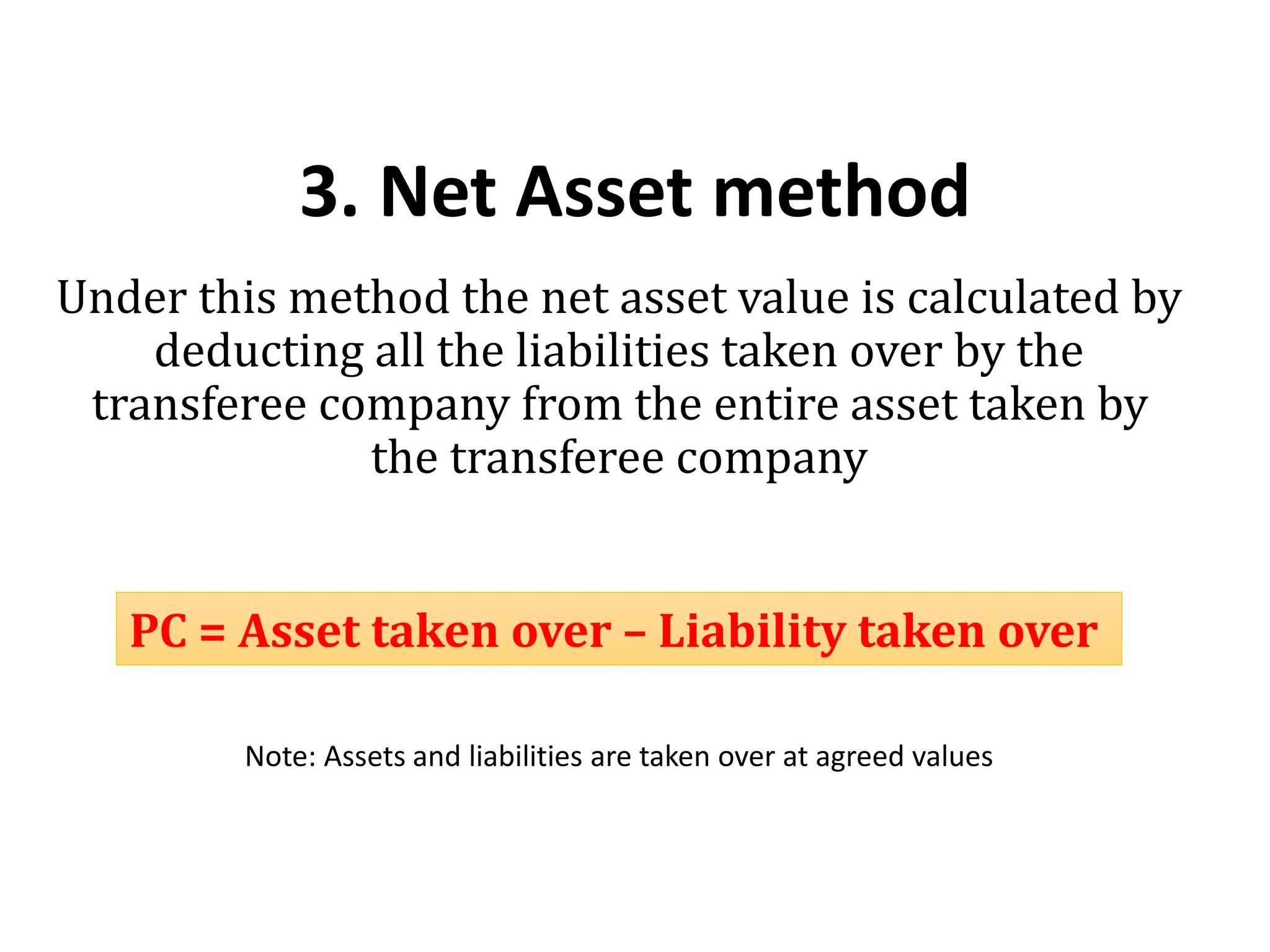

3. Net Assetmethod

Under this method the net asset value is calculated by

deducting all the liabilities taken over by the

transferee company from the entire asset taken by

the transferee company

Note: Assets and liabilities are taken over at agreed values

PC = Asset taken over – Liability taken over

23.

4. Other methodsof PC

Intrinsic Value method

Exchange ratio method