This document provides an overview of time series analysis (TSA), emphasizing its importance in predicting trends and making data-driven decisions across various industries. It discusses key components of TSA, including trends, seasonality, autocorrelation, and methods for forecasting using traditional and advanced models like ARIMA, SARIMA, and LSTM networks. Additionally, the document covers techniques for handling missing data, feature engineering, and future trends in TSA, such as deep learning and real-time analysis.

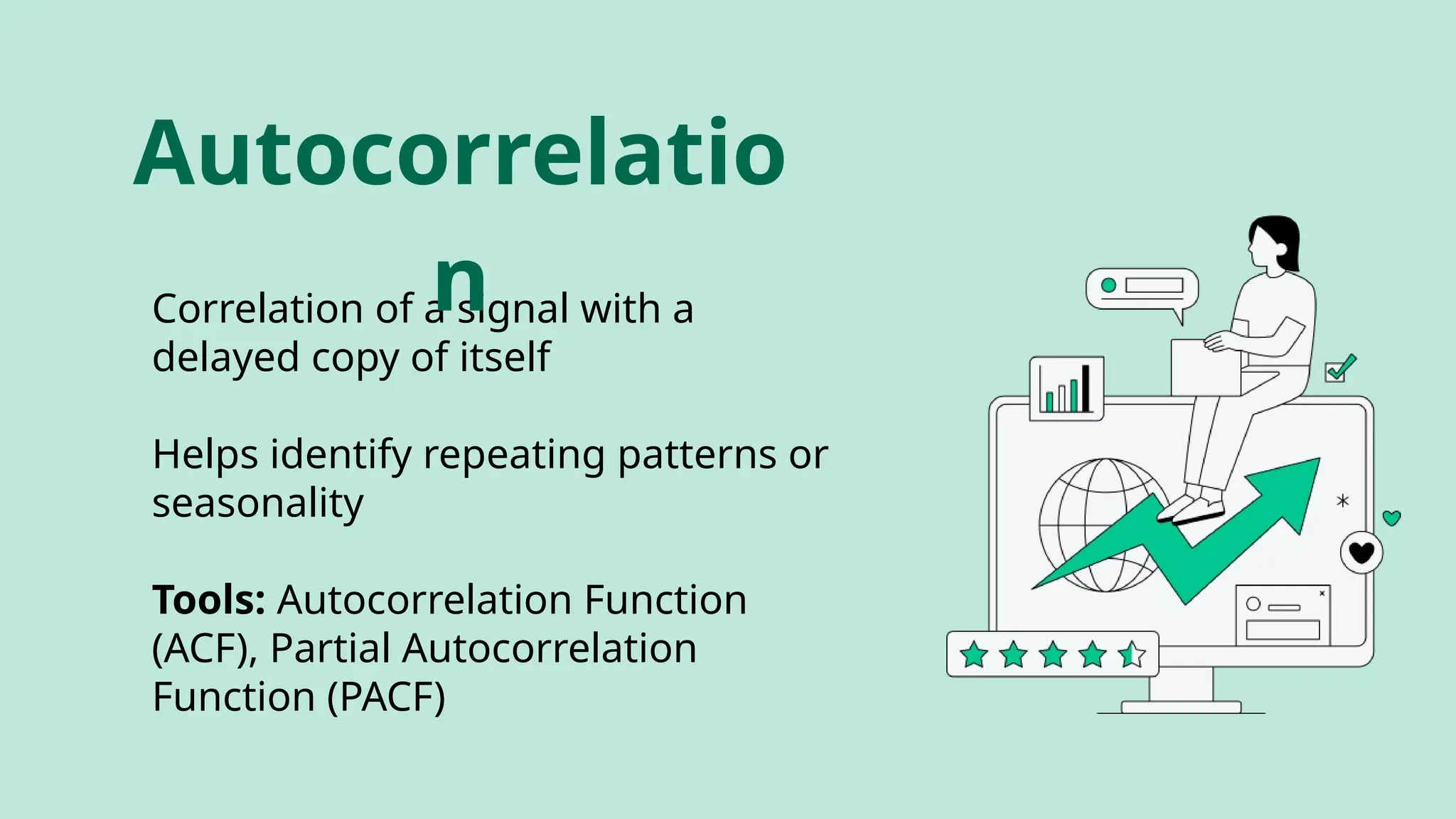

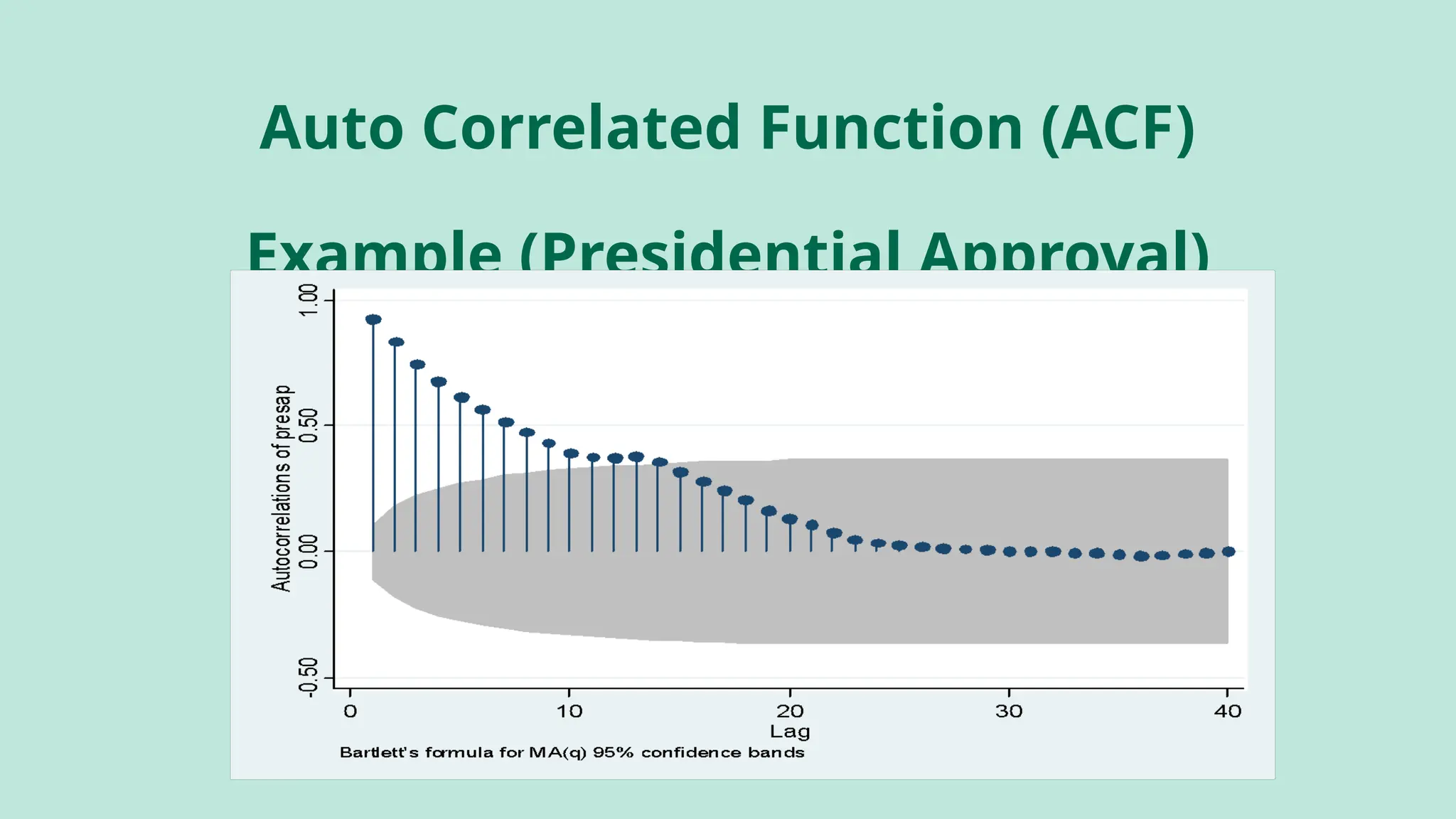

![Autocorrelated Functions (ACF)

The ACF shows how persistent a variable is over its relative delays.

ρk = γk / γ0 = covariance at lag k

variance

ρk = E[(yt – μ)(yt-k – μ)]2

E[(yt – μ)2

]

ACF (0) = 1, ACF (k) = ACF (-k)

Explanation

The approval series shows a long-lasting effect. Even though it doesn't

have a unit root, it has long memory, meaning that shocks to the series

last for at least 12 months.

If the ACF (Autocorrelation Function) shows a hyperbolic pattern, it

might mean the series is fractionally integrated.](https://image.slidesharecdn.com/mahfuzurrahman43timeseriesanalysis-240919065741-2e1964c9/75/Presentation-On-Time-Series-Analysis-in-Mechine-Learning-14-2048.jpg)

![Autocorrelated Functions (ACF)

The ACF shows how persistent a variable is over its relative delays.

ρk = γk / γ0 = covariance at lag k

variance

ρk = E[(yt – μ)(yt-k – μ)]2

E[(yt – μ)2

]

ACF (0) = 1, ACF (k) = ACF (-k)

Explanation

The approval series shows a long-lasting effect. Even though it doesn't

have a unit root, it has long memory, meaning that shocks to the series

last for at least 12 months.

If the ACF (Autocorrelation Function) shows a hyperbolic pattern, it

might mean the series is fractionally integrated.](https://crownmelresort.com/image.slidesharecdn.com/mahfuzurrahman43timeseriesanalysis-240919065741-2e1964c9/75/Presentation-On-Time-Series-Analysis-in-Mechine-Learning-14-2048.jpg)

![[DL輪読会]Deep Learning 第14章 自己符号化器](https://cdn.slidesharecdn.com/ss_thumbnails/deeplearning14-180601023750-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DL輪読会]Deep Learning 第13章 線形因子モデル](https://cdn.slidesharecdn.com/ss_thumbnails/deeplearning13-180601023632-thumbnail.jpg?width=640&height=640&fit=bounds)