Introduction to TimeSeries Analysis

• A time-series is a set of observations on a quantitative variable

collected over time.

• Examples

– Dow Jones Industrial Averages

– Historical data on sales, inventory, customer counts, interest

rates, costs, etc

• Businesses are often very interested in forecasting time series

variables.

• Often, independent variables are not available to build a

regression model of a time series variable.

• In time series analysis, we analyze the past behavior of a

variable in order to predict its future behavior.

3.

Methods used inForecasting

• Regression Analysis

• Time Series Analysis (TSA)

– A statistical technique that uses time-

series data for explaining the past or

forecasting future events.

– The prediction is a function of time

(days, months, years, etc.)

– No causal variable; examine past behavior

of a variable and and attempt to predict

future behavior

4.

Components of TSA

•Time Frame (How far can we predict?)

– short-term (1 - 2 periods)

– medium-term (5 - 10 periods)

– long-term (12+ periods)

– No line of demarcation

• Trend

– Gradual, long-term movement (up or down) of

demand.

– Easiest to detect

5.

Components of TSA(Cont.)

• Cycle

– An up-and-down repetitive movement in demand.

– repeats itself over a long period of time

• Seasonal Variation

– An up-and-down repetitive movement within a trend

occurring periodically.

– Often weather related but could be daily or weekly

occurrence

• Random Variations

– Erratic movements that are not predictable because they

do not follow a pattern

6.

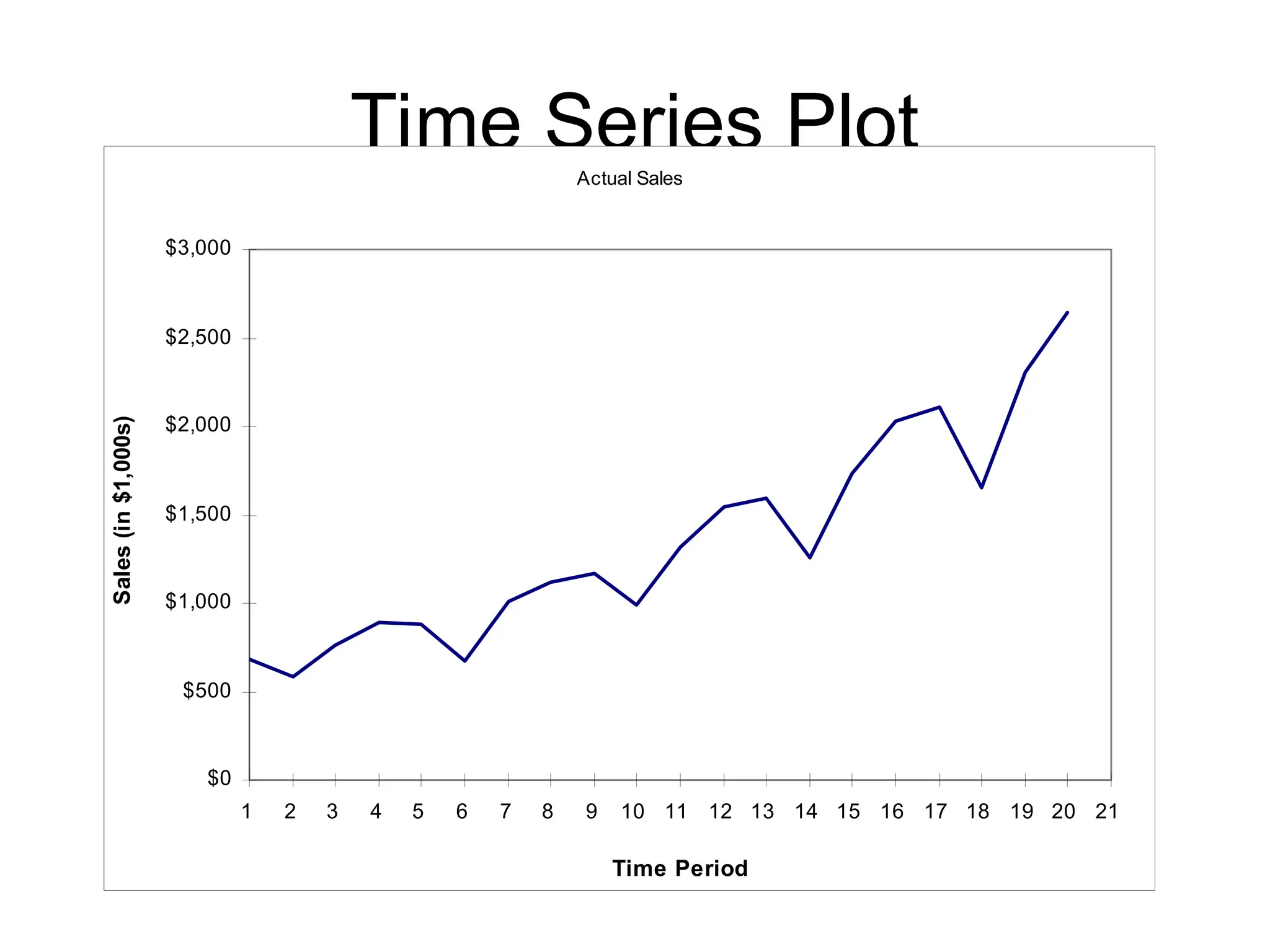

Time Series Plot

ActualSales

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21

Time Period

Sales

(in

$1,000s)

7.

Components of TSA(Cont.)

• Difficult to forecast demand because...

– There are no causal variables

– The components (trend, seasonality,

cycles, and random variation) cannot

always be easily or accurately

identified

8.

Some Time SeriesTerms

• Stationary Data - a time series variable exhibiting

no significant upward or downward trend over

time.

• Nonstationary Data - a time series variable

exhibiting a significant upward or downward

trend over time.

• Seasonal Data - a time series variable exhibiting

a repeating patterns at regular intervals over

time.

9.

Approaching Time SeriesAnalysis

• There are many, many different time series

techniques.

• It is usually impossible to know which technique

will be best for a particular data set.

• It is customary to try out several different

techniques and select the one that seems to

work best.

• To be an effective time series modeler, you need

to keep several time series techniques in your

“tool box.”

10.

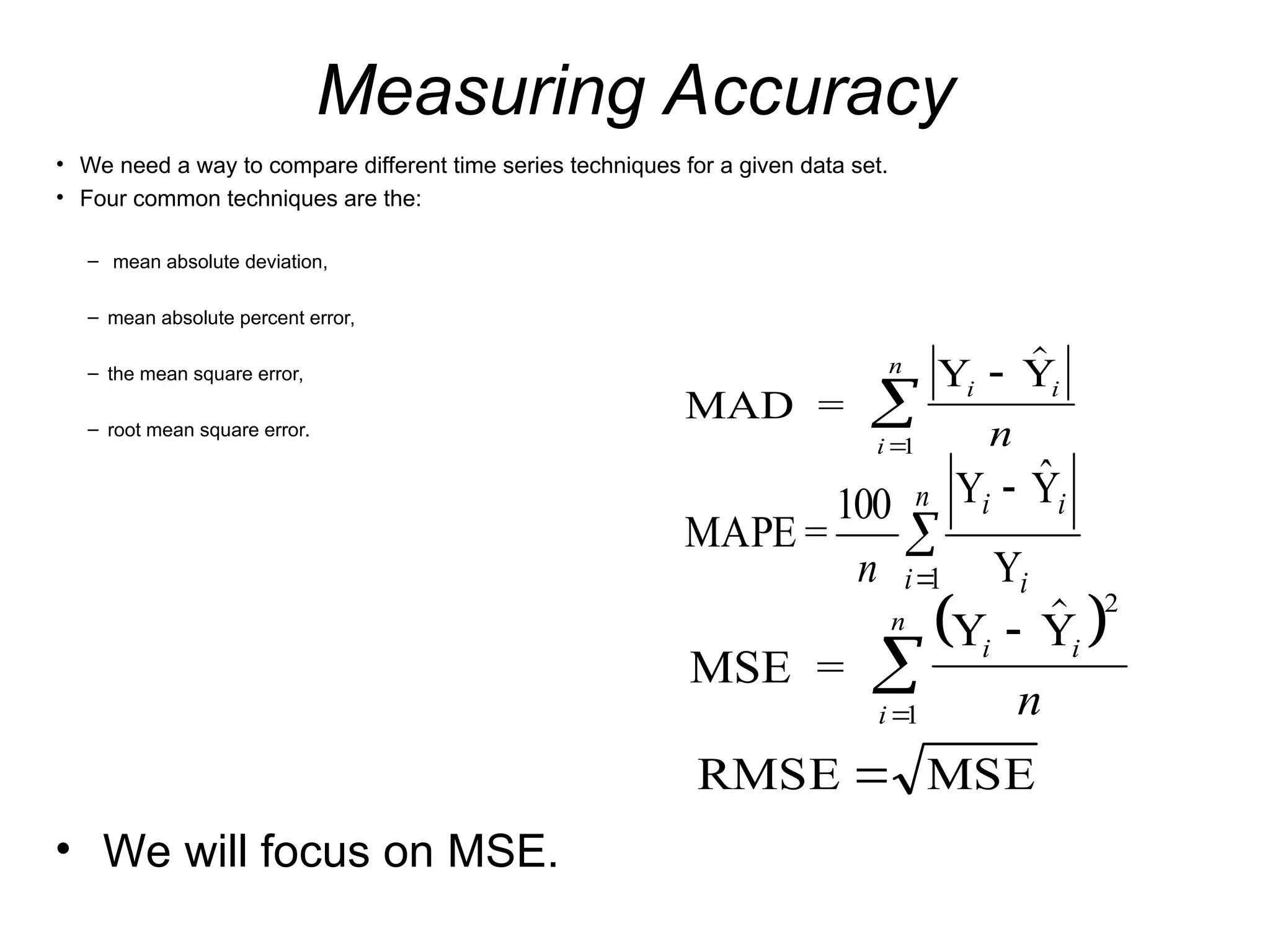

Measuring Accuracy

• Weneed a way to compare different time series techniques for a given data set.

• Four common techniques are the:

– mean absolute deviation,

– mean absolute percent error,

– the mean square error,

– root mean square error.

MAD =

Y Y

i i

i

n

n

1

MSE =

Y Y

i i

i

n

n

2

1

MSE

RMSE

n

i i

i

i

n 1 Y

Ŷ

Y

100

=

MAPE

• We will focus on MSE.

11.

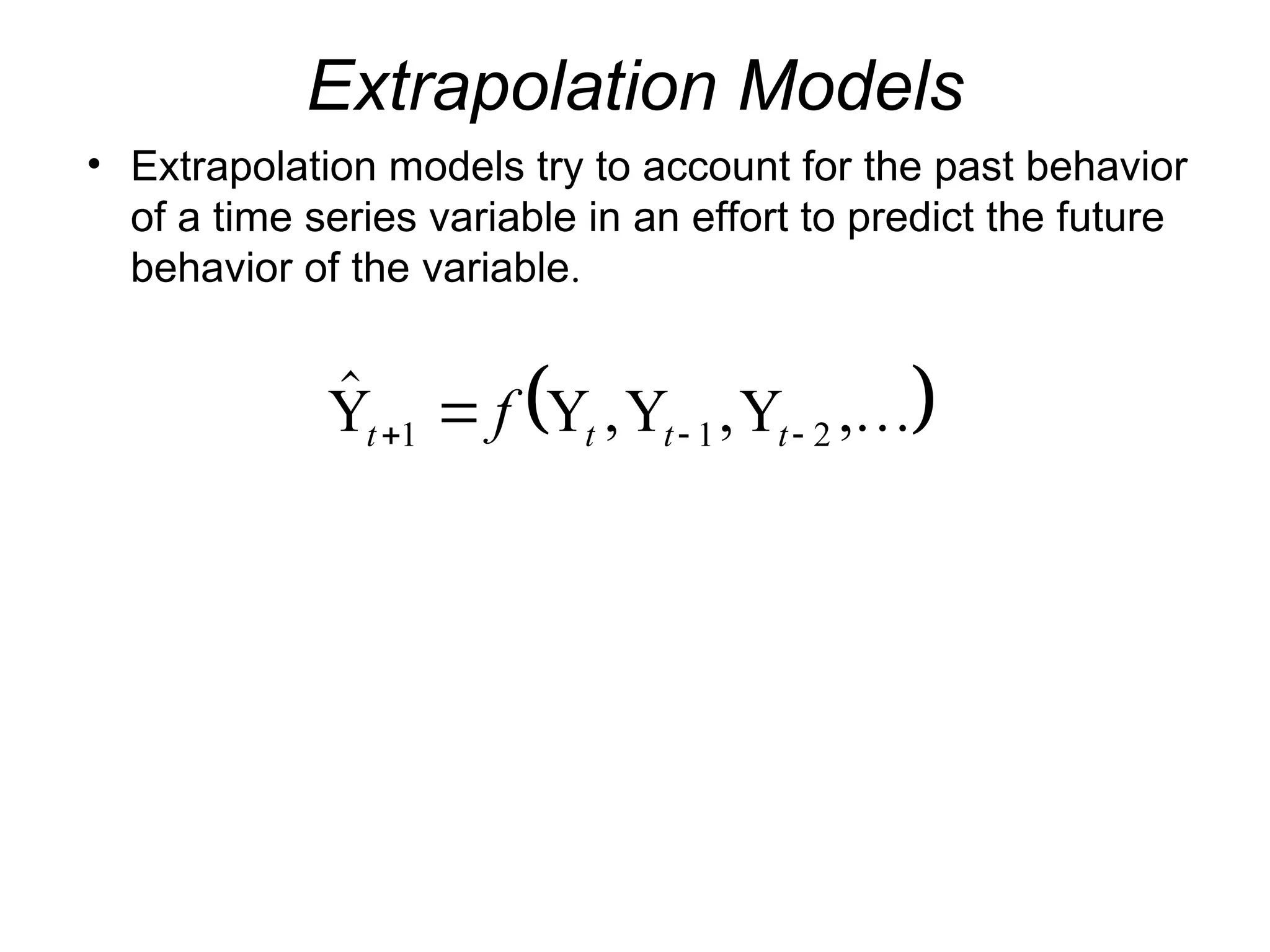

Extrapolation Models

• Extrapolationmodels try to account for the past behavior

of a time series variable in an effort to predict the future

behavior of the variable.

, , ,

Y Y Y Y

t t t t

f

1 1 2

12.

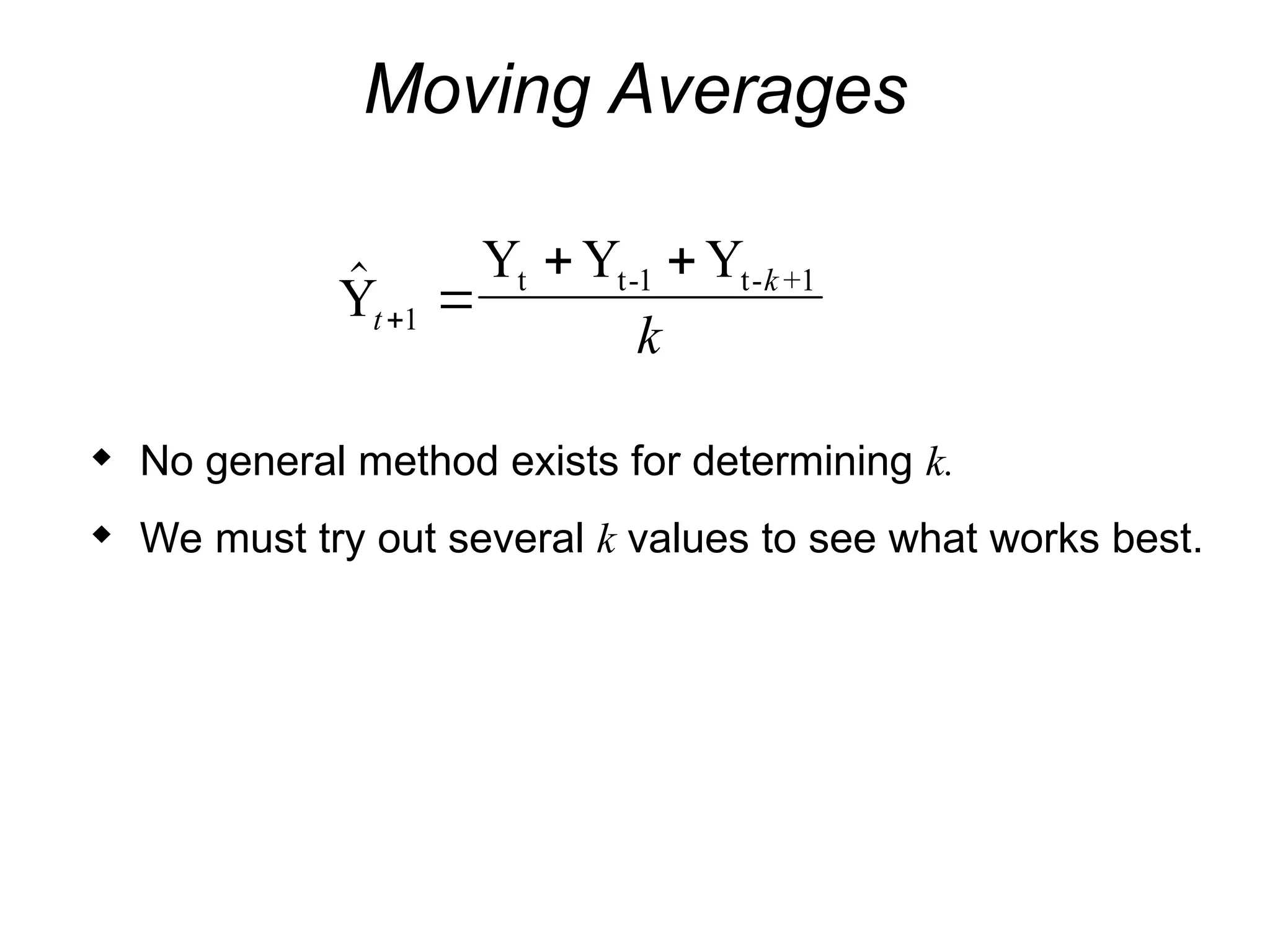

Moving Averages

Y

Y YY

t t-1 t- +1

t

k

k

1

No general method exists for determining k.

We must try out several k values to see what works best.

13.

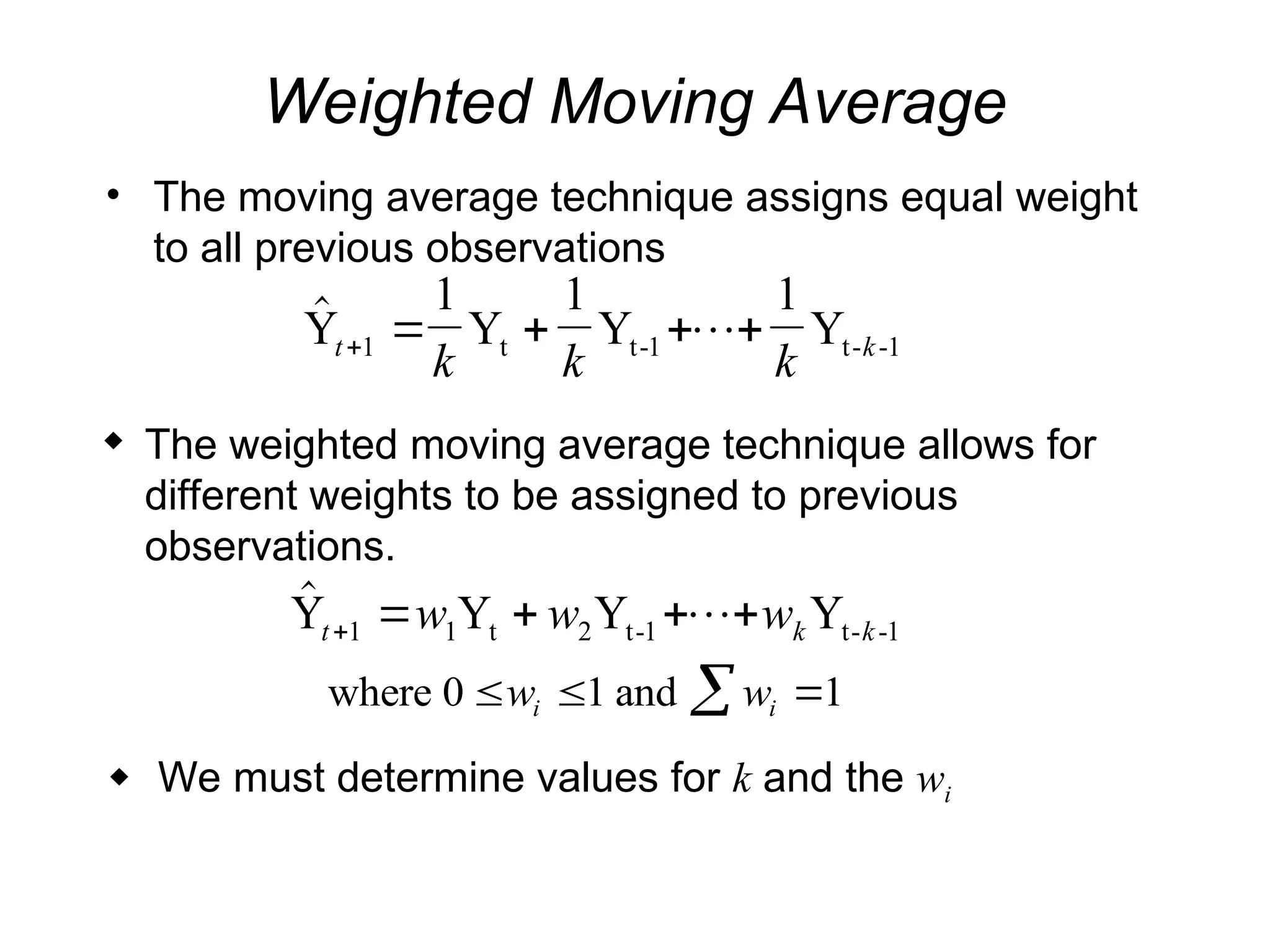

Weighted Moving Average

•The moving average technique assigns equal weight

to all previous observations

Y

1

Y

1

Y

1

Y

t t-1 t- -1

t k

k k k

1

The weighted moving average technique allows for

different weights to be assigned to previous

observations.

Y Y Y Y

t t-1 t- -1

t k k

w w w

1 1 2

where 0 and

w w

i i

1 1

We must determine values for k and the wi

14.

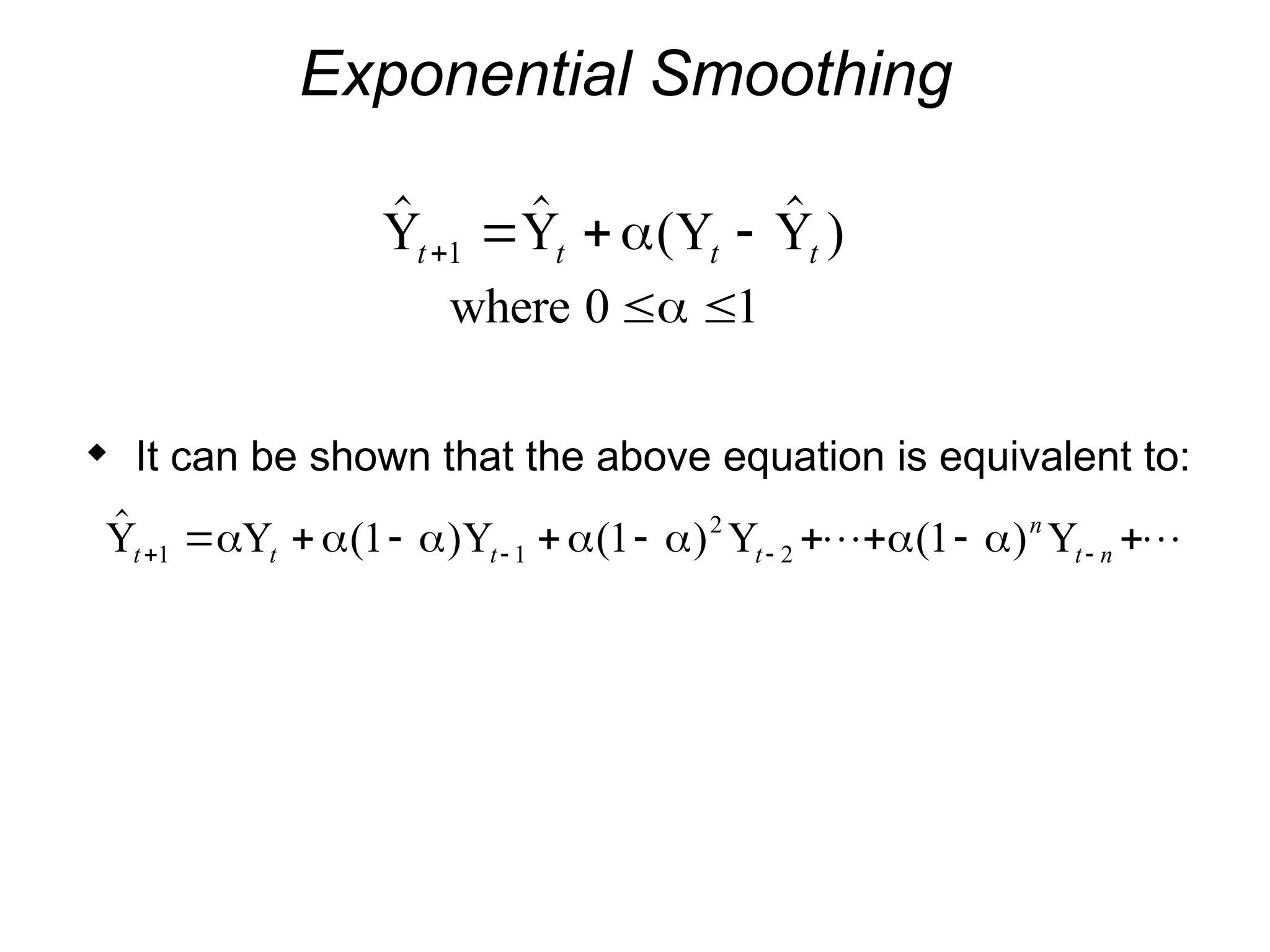

Exponential Smoothing

( )

Y Y Y Y

t t t t

1

where 0 1

It can be shown that the above equation is equivalent to:

( ) ( ) ( )

Y Y Y Y Y

t t t t

n

t n

1 1

2

2

1 1 1

15.

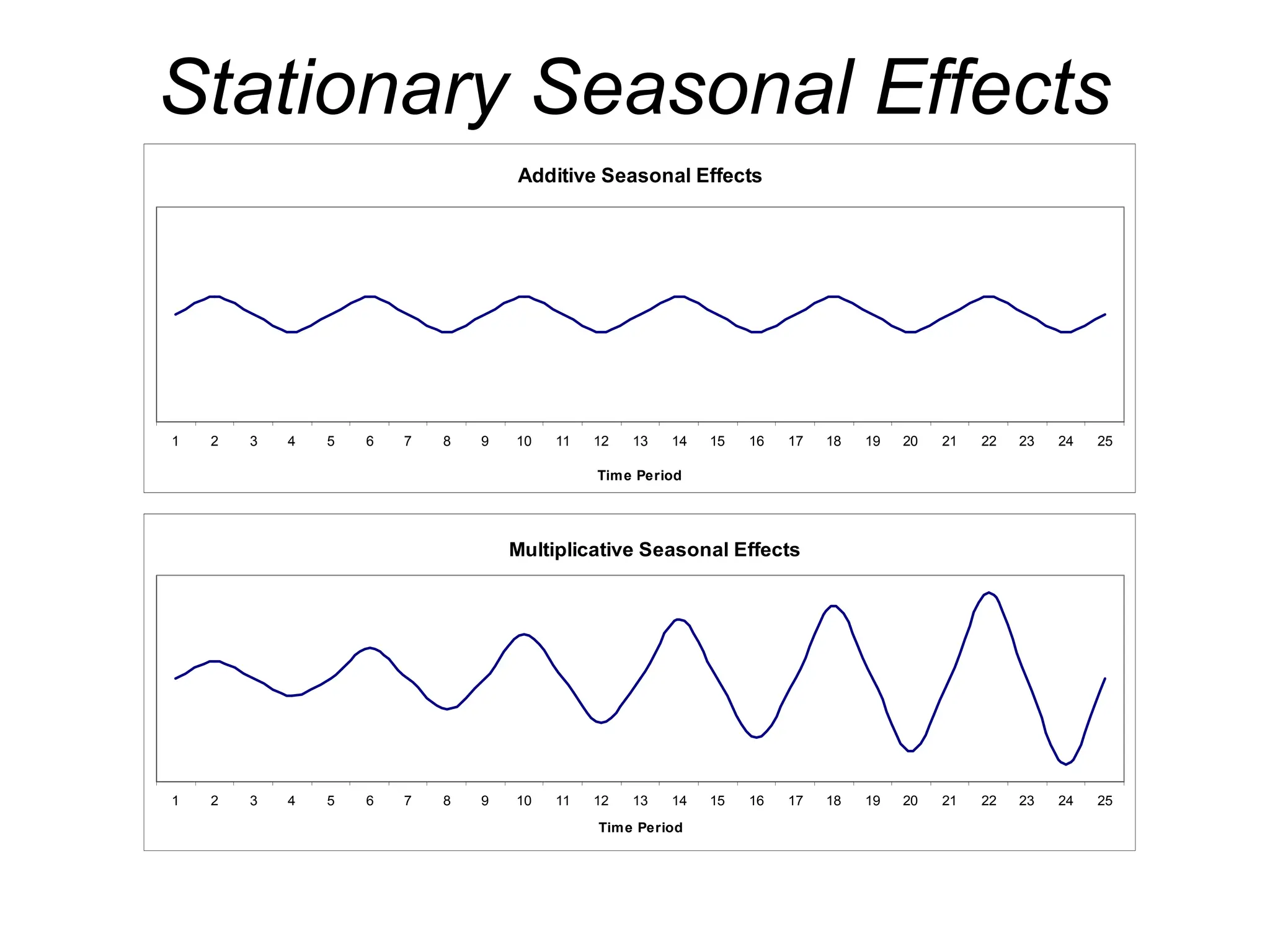

Seasonality

• Seasonality isa regular, repeating

pattern in time series data.

• May be additive or multiplicative in

nature...

Trend Models

• Trendis the long-term sweep or general

direction of movement in a time series.

• We’ll now consider some nonstationary time

series techniques that are appropriate for

data exhibiting upward or downward trends.

18.

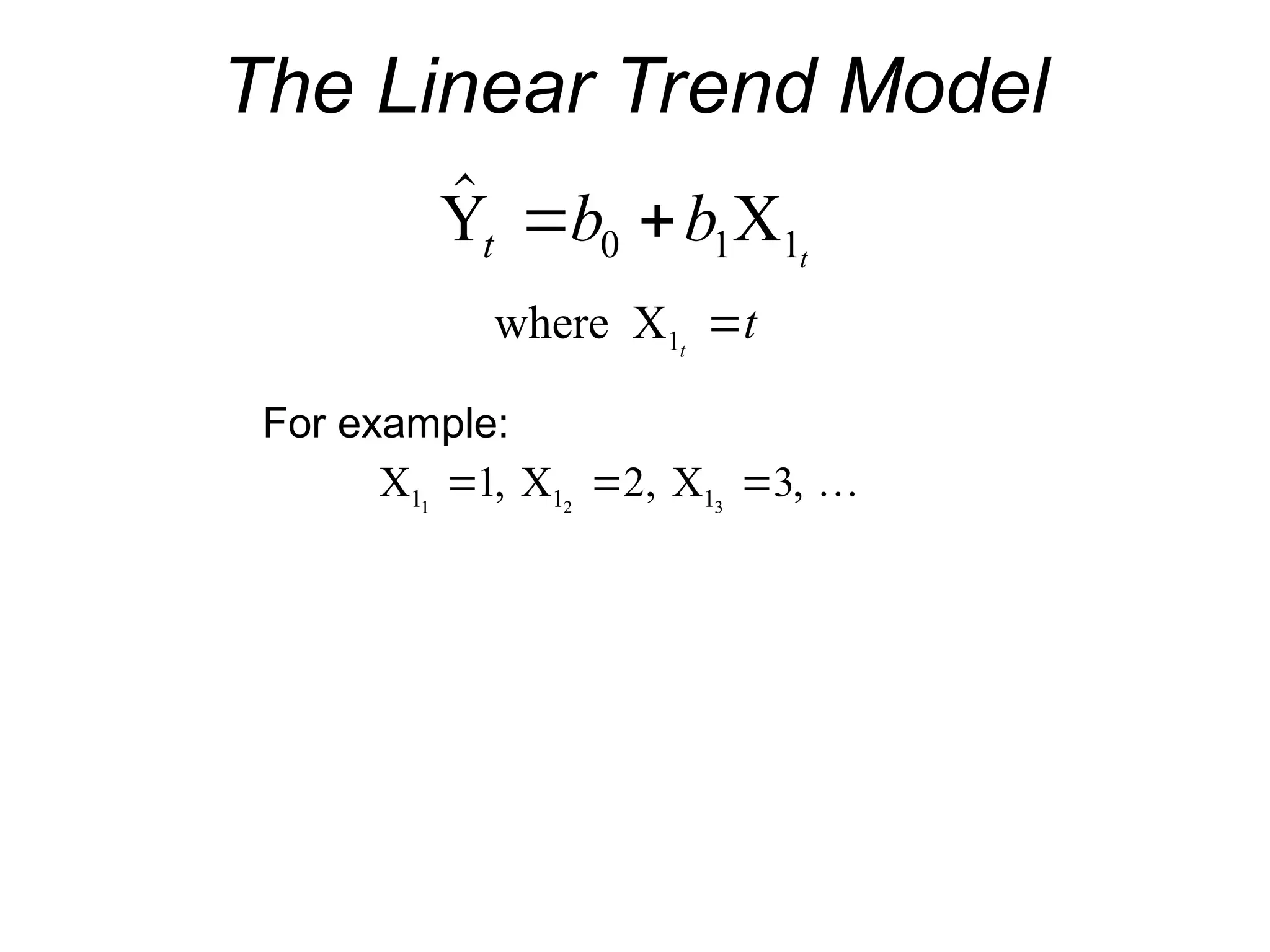

The Linear TrendModel

Y X

t b b t

0 1 1

where X1t

t

For example:

X X X

1 1 1

1 2 3

1 2 3

, , ,

19.

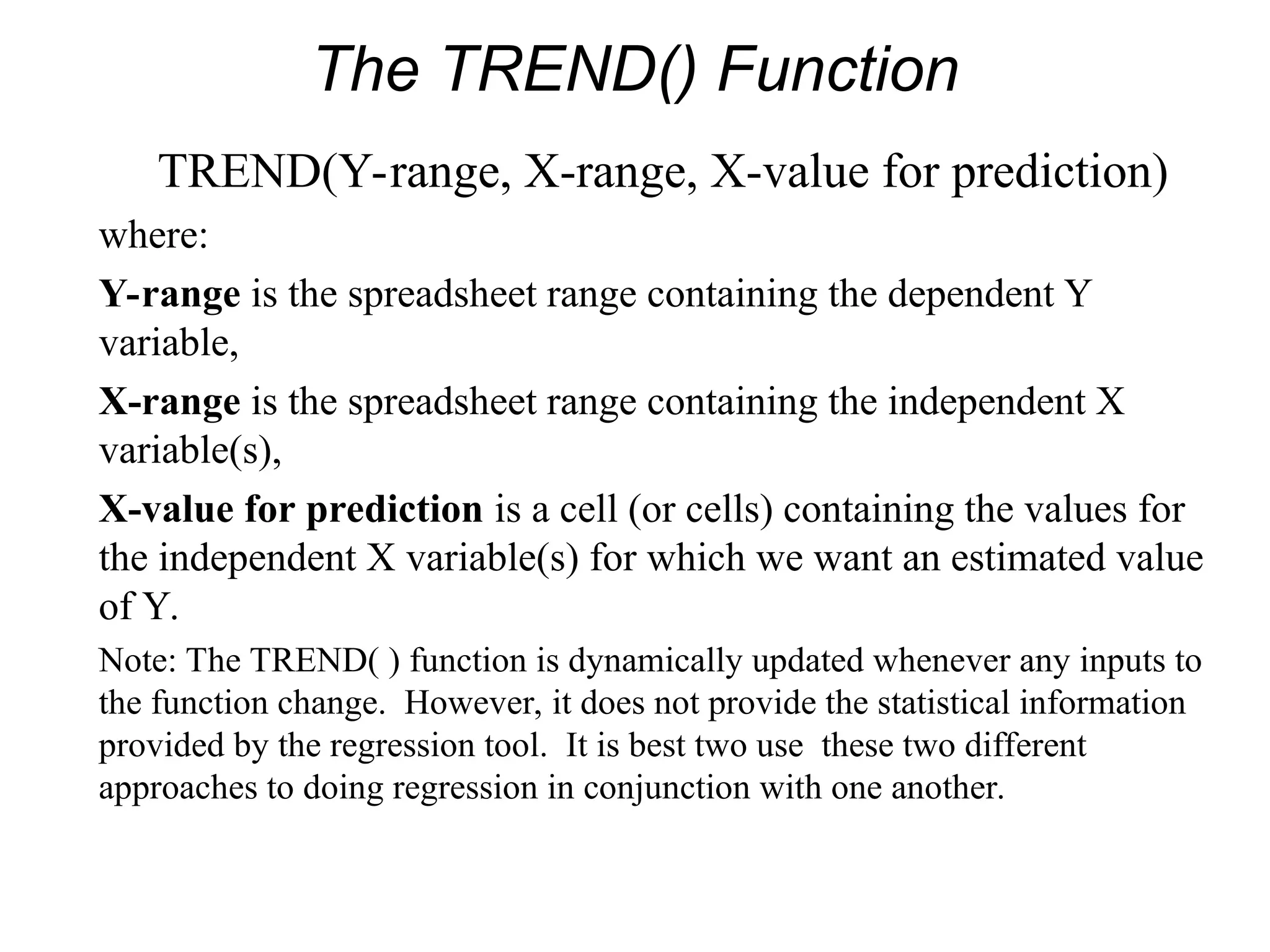

The TREND() Function

TREND(Y-range,X-range, X-value for prediction)

where:

Y-range is the spreadsheet range containing the dependent Y

variable,

X-range is the spreadsheet range containing the independent X

variable(s),

X-value for prediction is a cell (or cells) containing the values for

the independent X variable(s) for which we want an estimated value

of Y.

Note: The TREND( ) function is dynamically updated whenever any inputs to

the function change. However, it does not provide the statistical information

provided by the regression tool. It is best two use these two different

approaches to doing regression in conjunction with one another.

20.

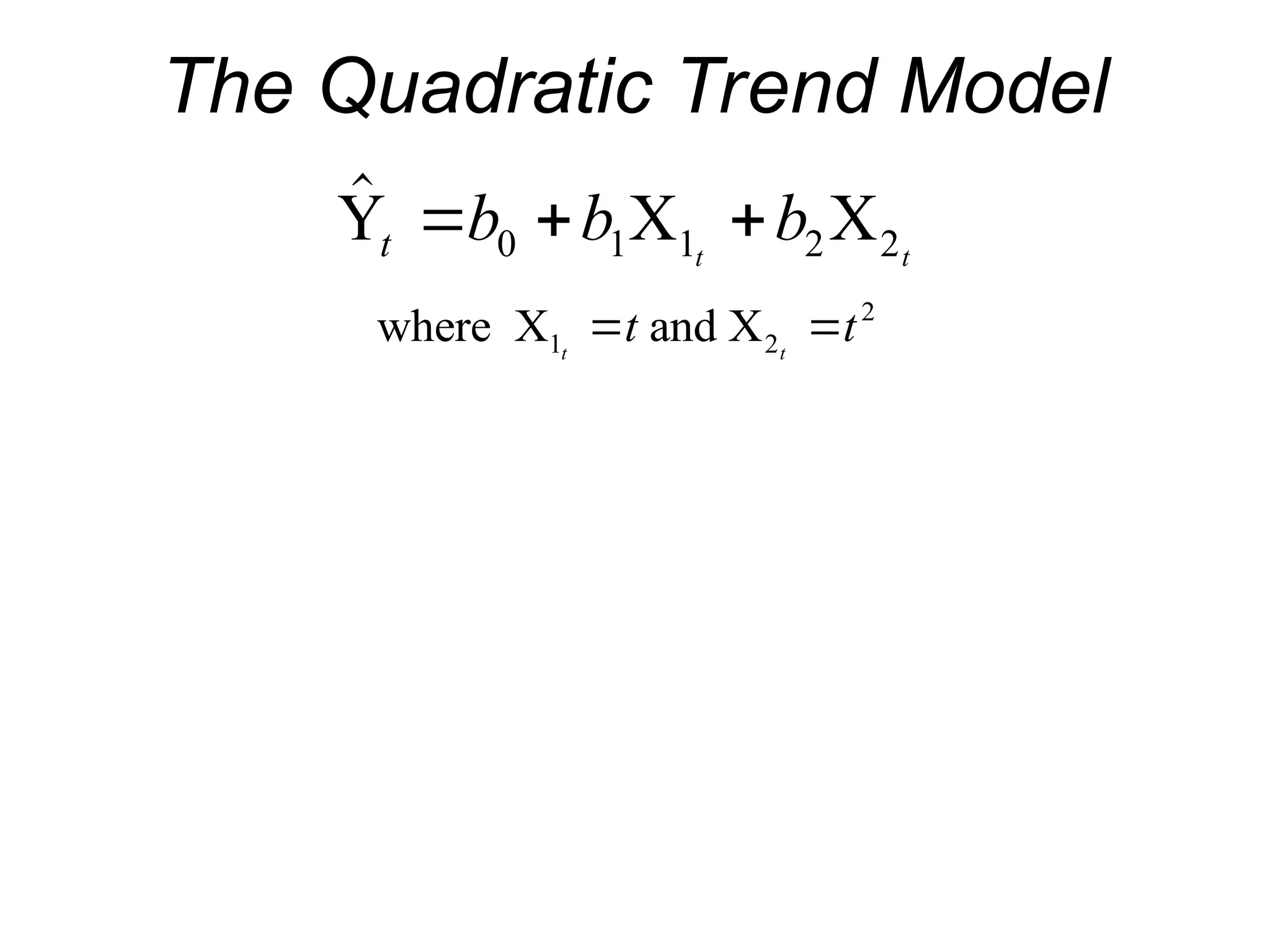

The Quadratic TrendModel

Y X X

t b b b

t t

0 1 1 2 2

where X and X

1 2

2

t t

t t

21.

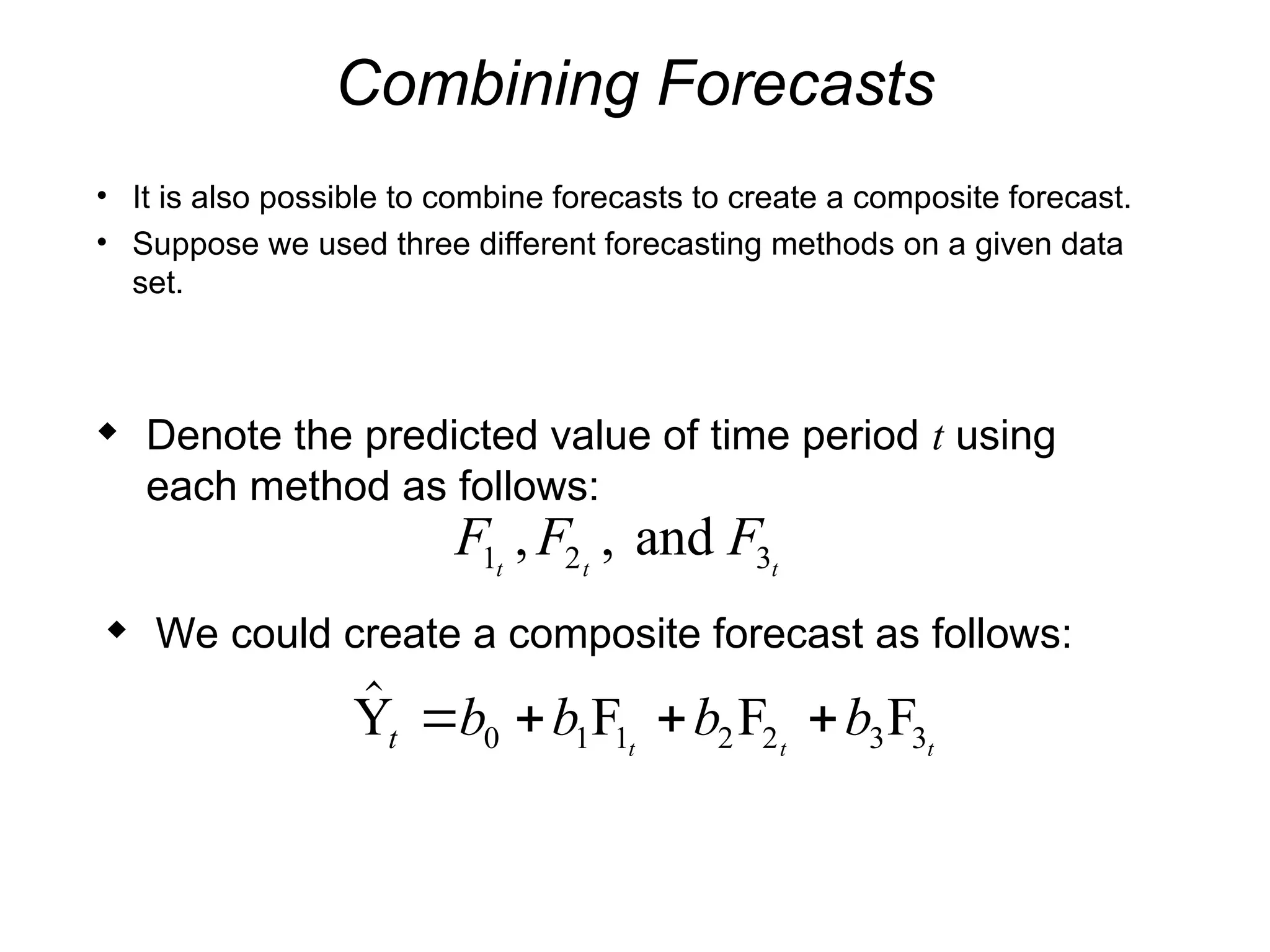

Combining Forecasts

• Itis also possible to combine forecasts to create a composite forecast.

• Suppose we used three different forecasting methods on a given data

set.

Denote the predicted value of time period t using

each method as follows:

F F F

t t t

1 2 3

, , and

We could create a composite forecast as follows:

Y F F F

t b b b b

t t t

0 1 1 2 2 3 3

![SHS_Core_CAE_Q3_LE1 FOR THIRD [FINAL].pdf](https://cdn.slidesharecdn.com/ss_thumbnails/shscorecaeq3le1final-251116055110-e3081055-thumbnail.jpg?width=640&height=640&fit=bounds)