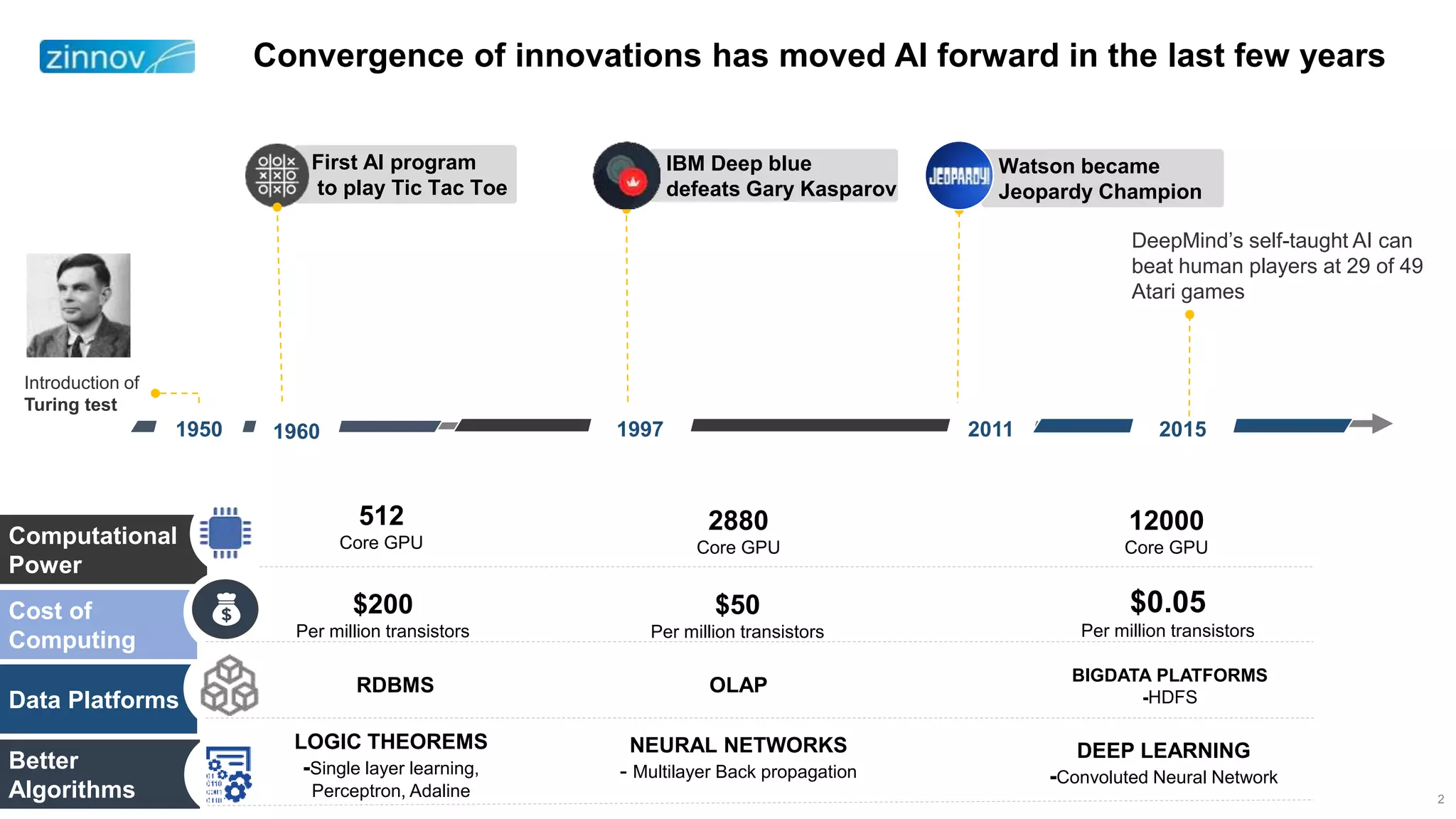

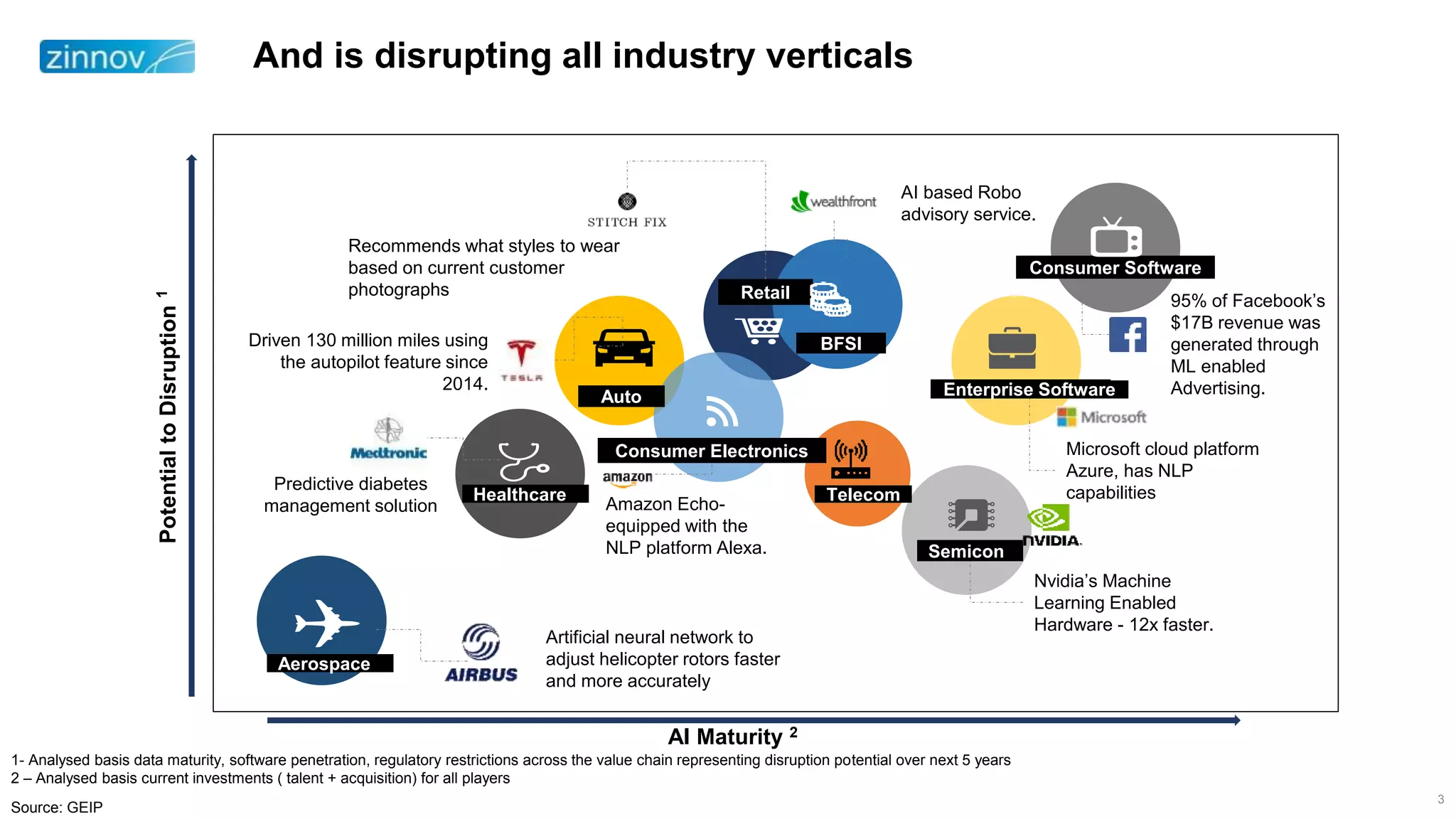

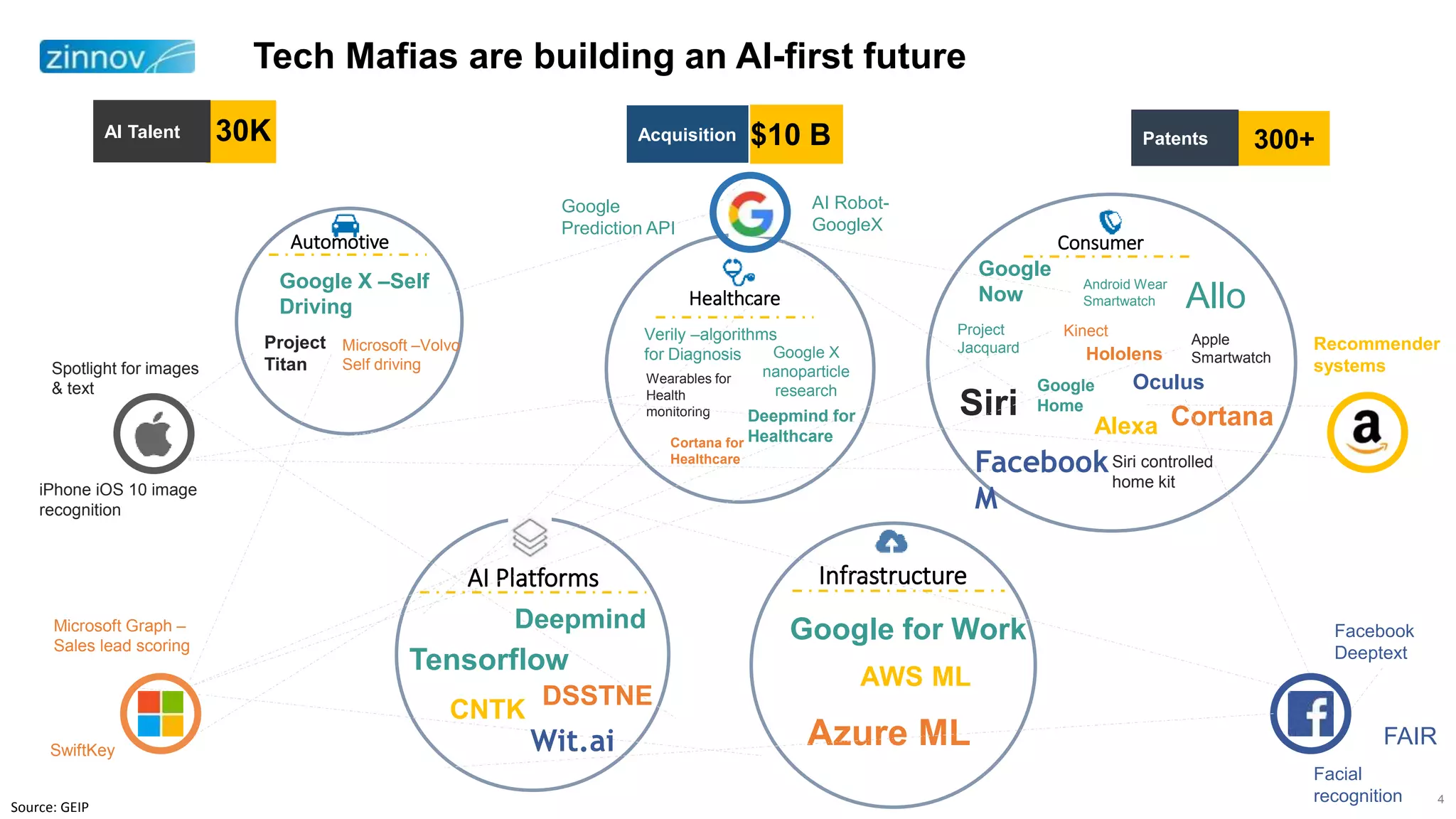

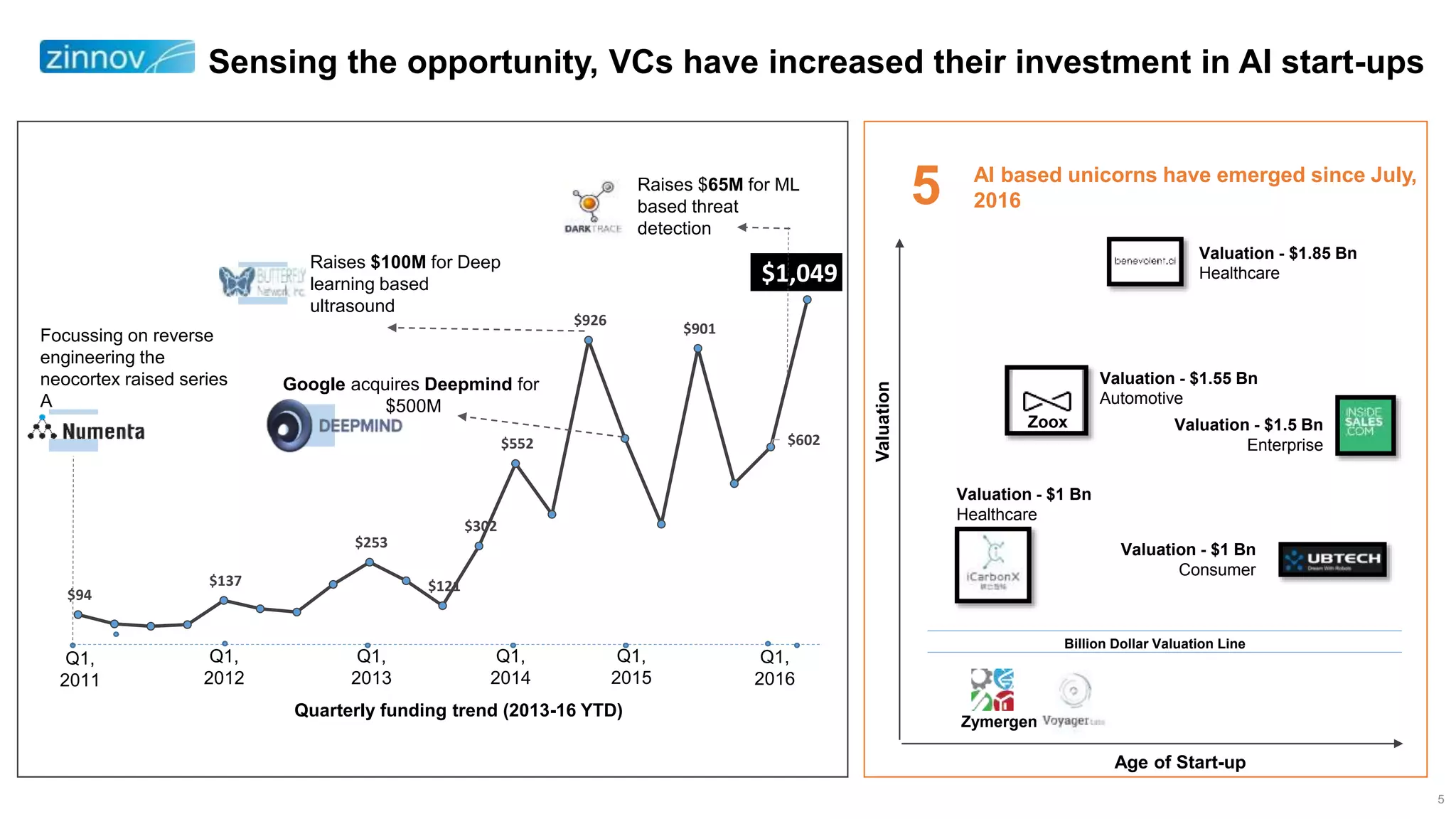

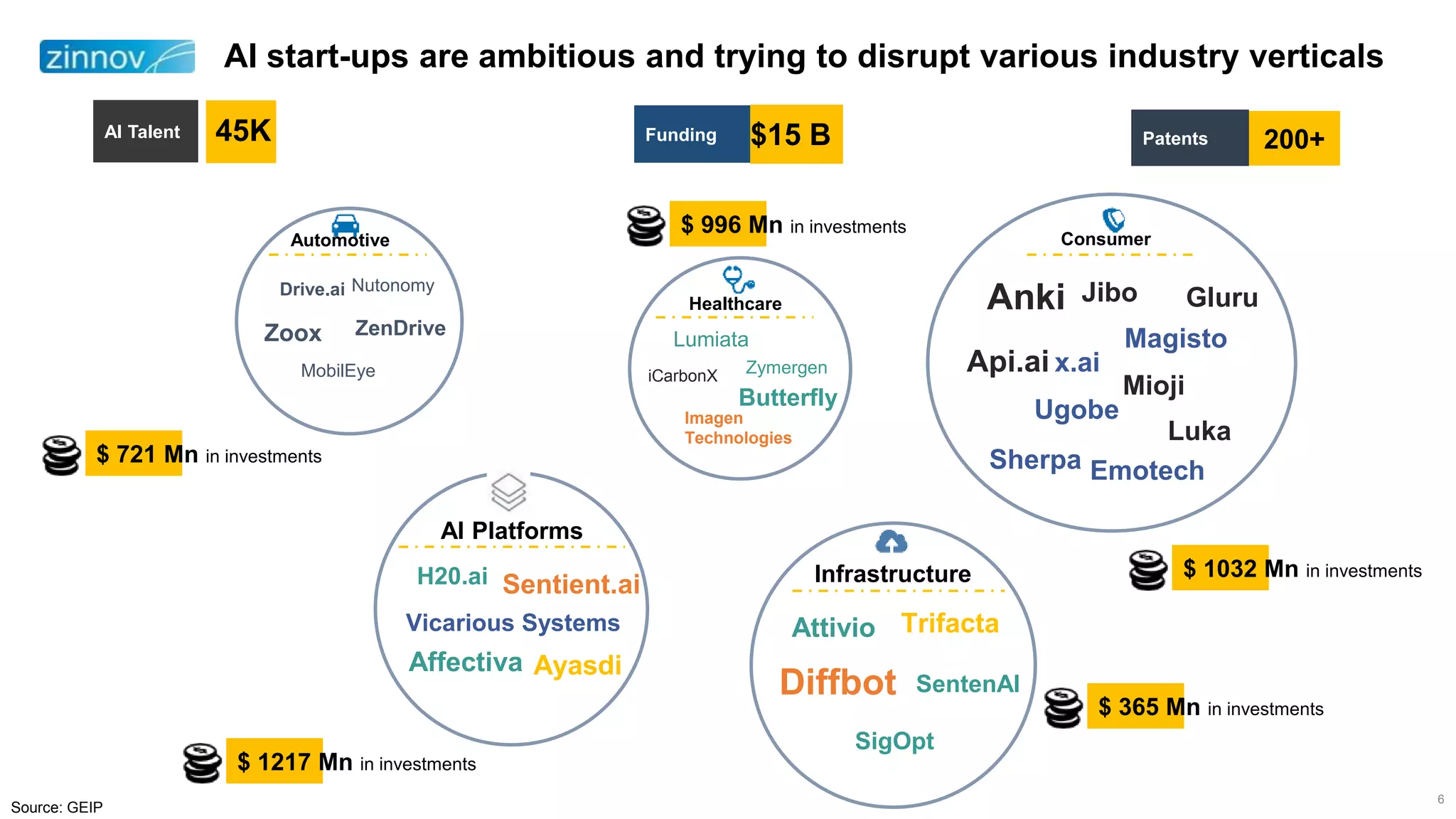

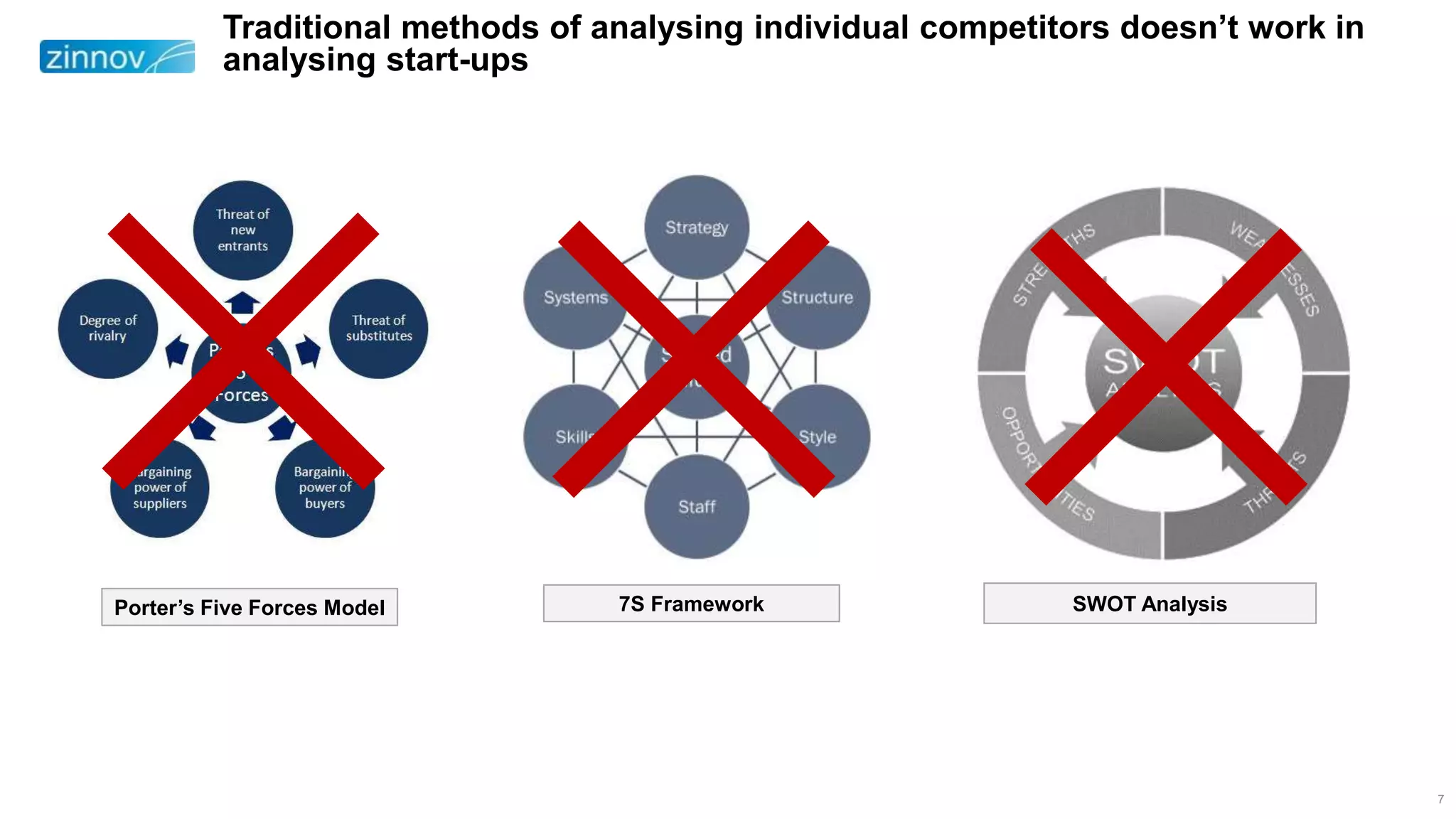

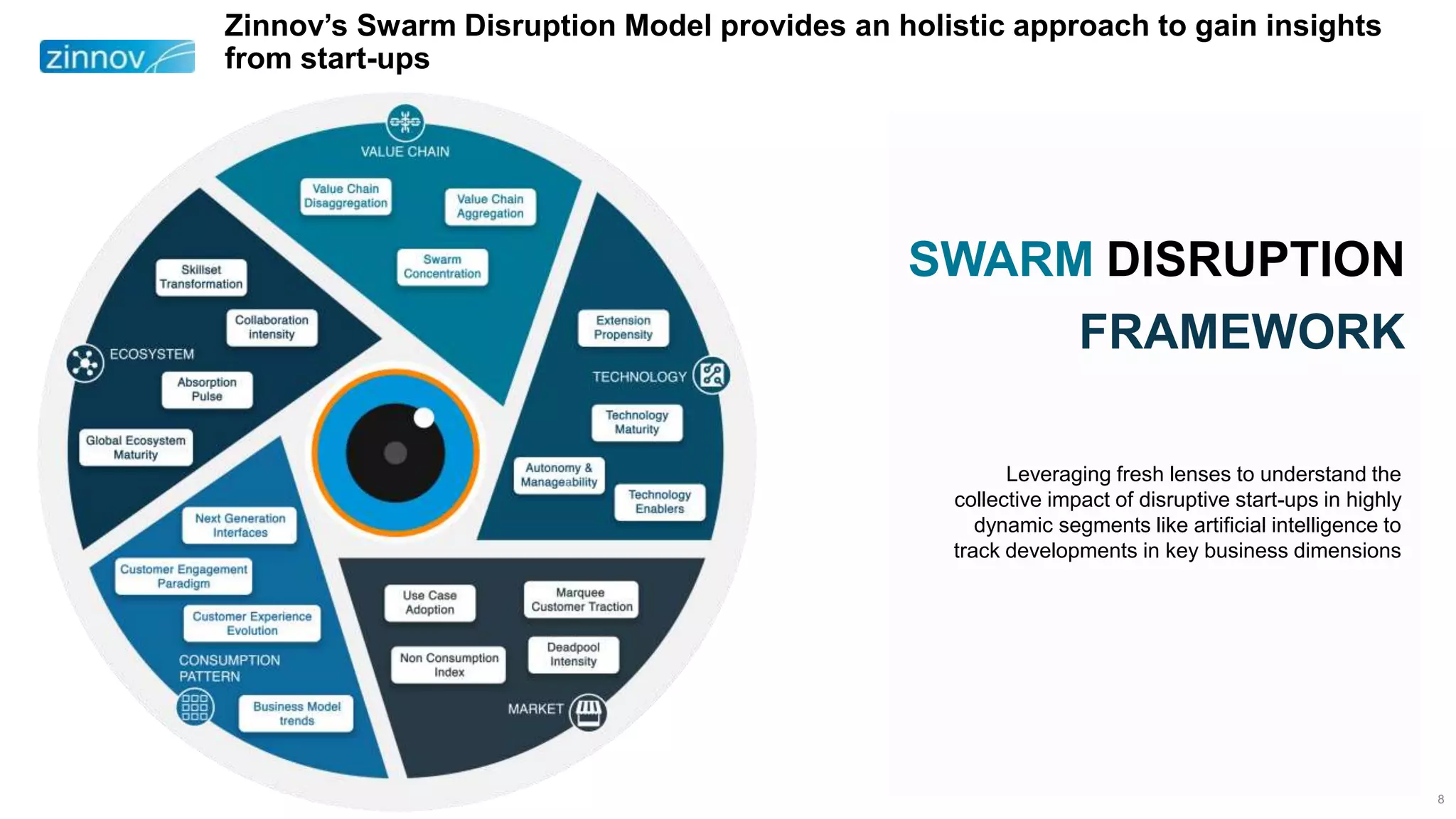

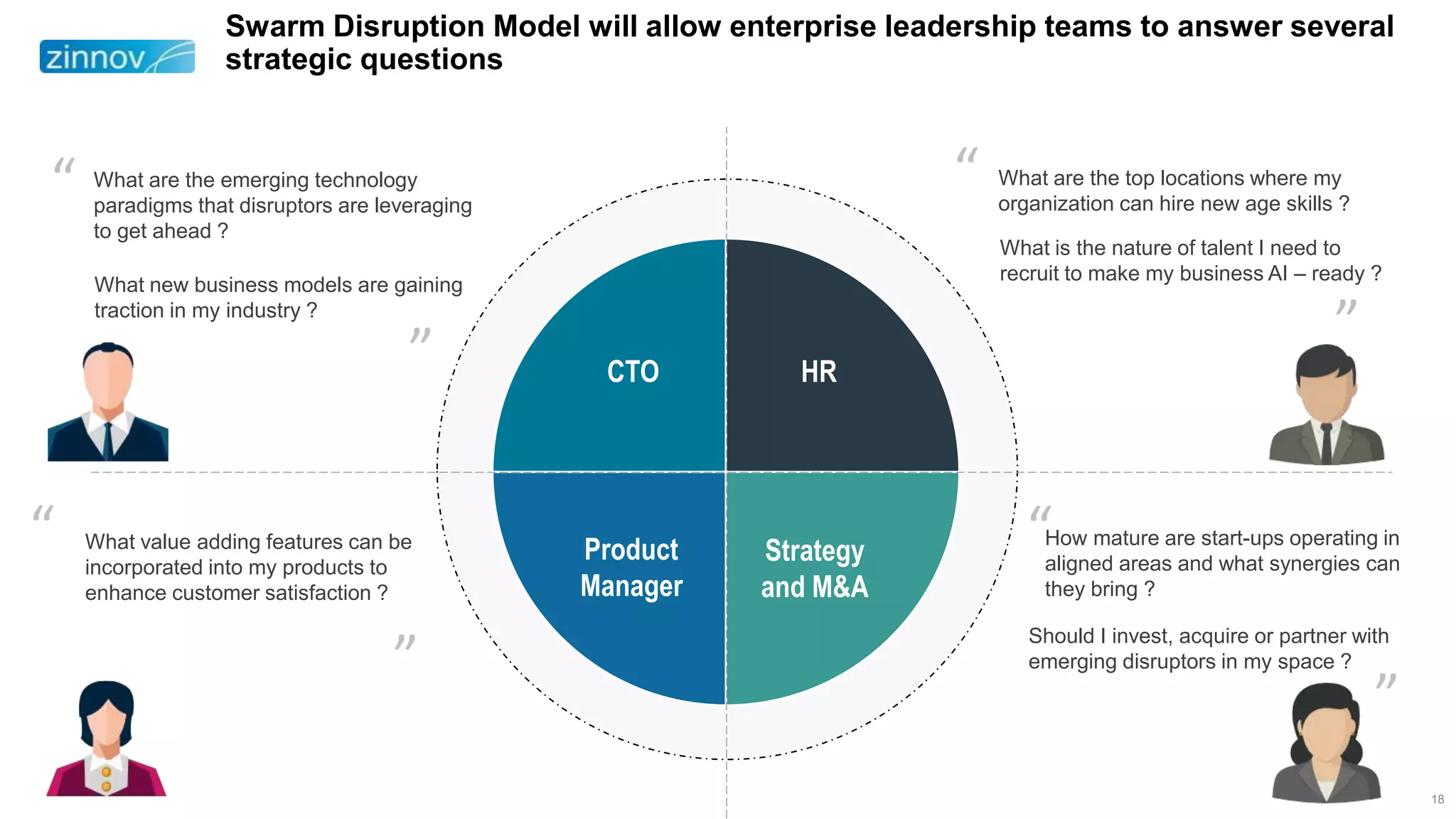

The document discusses the evolution of AI from its early days in the 1950s to recent advancements, highlighting significant milestones such as IBM's Deep Blue defeating Garry Kasparov and the emergence of deep learning technologies. It analyzes the disruptive potential of AI across various industries, including healthcare, automotive, and retail, emphasizing the role of startups and major investments in shaping the AI landscape. Additionally, it introduces a swarm disruption model that helps enterprises strategize and adapt to rapidly changing AI innovations and market conditions.