Downloaded 141 times

![Daniel Pandza, M.A. Centro de Innovación CERTIFICADO EN INNOVACIÓN G2 - ENERO-MAYO 2009 INNOVACIÓN DE MODELOS DE NEGOCIOS SESSION 03 VALUE DISCIPLINES FOR COMPETITIVE ADVANTAGE FACULTY TEAM Ing. Jorge Valdes Simancas Ing. Angel Tonatiuh Flores [ atflores@itesm.mx ] [email_address] Tel 01-(33) 3669 3000 ext. 2266 www.gda.itesm.mx/innovar GAP CAP](https://image.slidesharecdn.com/session-03-value-disciplines-compacto-1233682182869000-2/75/Session-03-Value-Disciplines-Compacto-1-2048.jpg)

![CONTACT: Daniel Pandza | Innovation Center Tecnológico de Monterrey | Campus Guadalajara Tel: 0052 (33) 3669 3000 ext. 2266 E-Mail: [email_address] URL: http://www.gda.itesm.mx/innovar Center Blog: http://paradygnamics.wordpress.com CENTRO DE INNOVACIÓN TECNOLÓGICO DE MONTERREY SERVICES Innovation Certificate for Undergraduate Students Innovation Consulting for the Business Community International Seminars and Executive Training NUEVAS PERSPECTIVAS PARA EL ÉXITO EMPRESARIAL http://paradygnamics.wordpress.com](https://image.slidesharecdn.com/session-03-value-disciplines-compacto-1233682182869000-2/75/Session-03-Value-Disciplines-Compacto-54-2048.jpg)

![Daniel Pandza, M.A. Centro de Innovación CERTIFICADO EN INNOVACIÓN G2 - ENERO-MAYO 2009 INNOVACIÓN DE MODELOS DE NEGOCIOS SESSION 03 VALUE DISCIPLINES FOR COMPETITIVE ADVANTAGE FACULTY TEAM Ing. Jorge Valdes Simancas Ing. Angel Tonatiuh Flores [ atflores@itesm.mx ] [email_address] Tel 01-(33) 3669 3000 ext. 2266 www.gda.itesm.mx/innovar GAP CAP](https://crownmelresort.com/image.slidesharecdn.com/session-03-value-disciplines-compacto-1233682182869000-2/75/Session-03-Value-Disciplines-Compacto-1-2048.jpg)

![CONTACT: Daniel Pandza | Innovation Center Tecnológico de Monterrey | Campus Guadalajara Tel: 0052 (33) 3669 3000 ext. 2266 E-Mail: [email_address] URL: http://www.gda.itesm.mx/innovar Center Blog: http://paradygnamics.wordpress.com CENTRO DE INNOVACIÓN TECNOLÓGICO DE MONTERREY SERVICES Innovation Certificate for Undergraduate Students Innovation Consulting for the Business Community International Seminars and Executive Training NUEVAS PERSPECTIVAS PARA EL ÉXITO EMPRESARIAL http://paradygnamics.wordpress.com](https://crownmelresort.com/image.slidesharecdn.com/session-03-value-disciplines-compacto-1233682182869000-2/75/Session-03-Value-Disciplines-Compacto-54-2048.jpg)

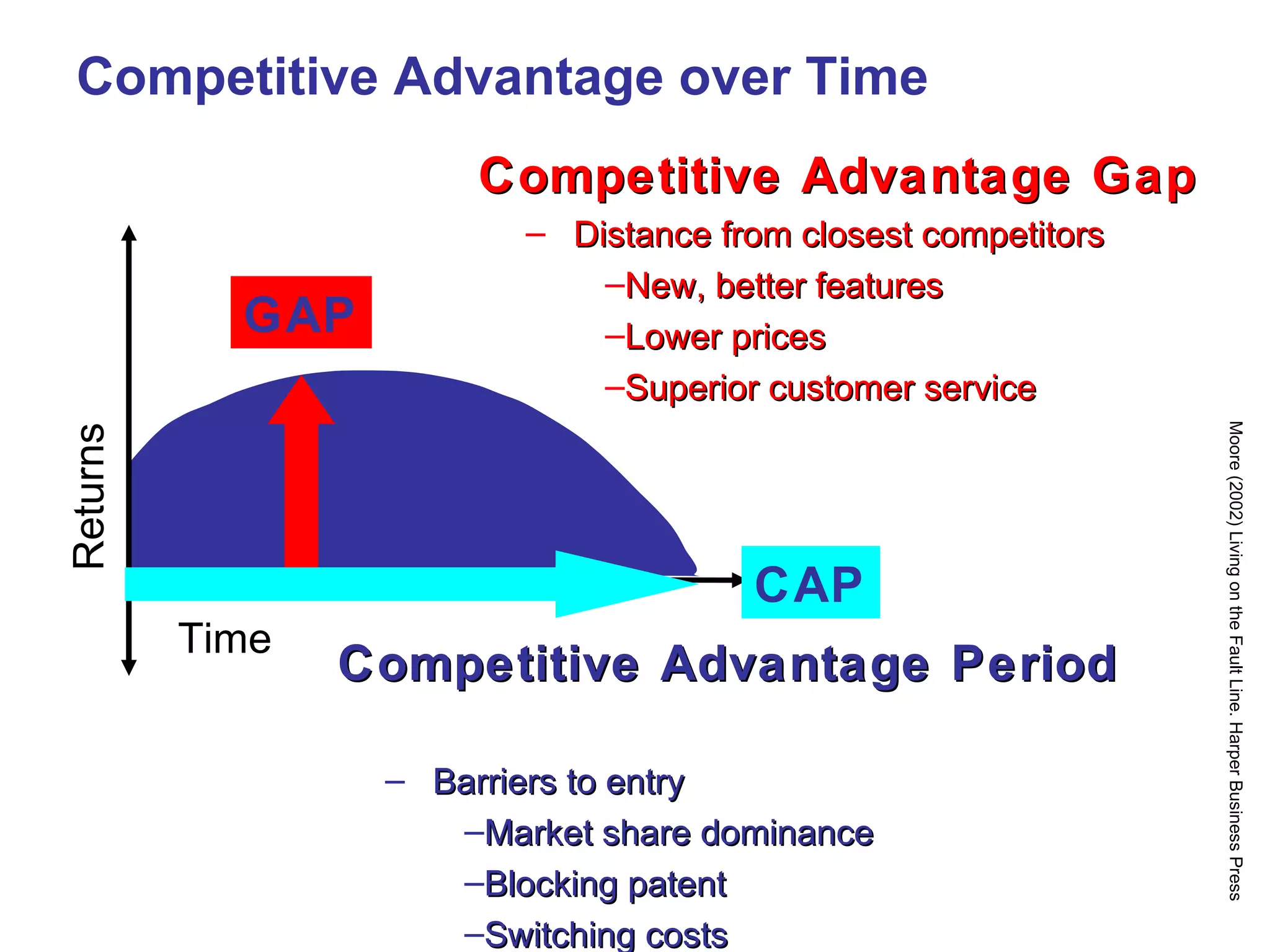

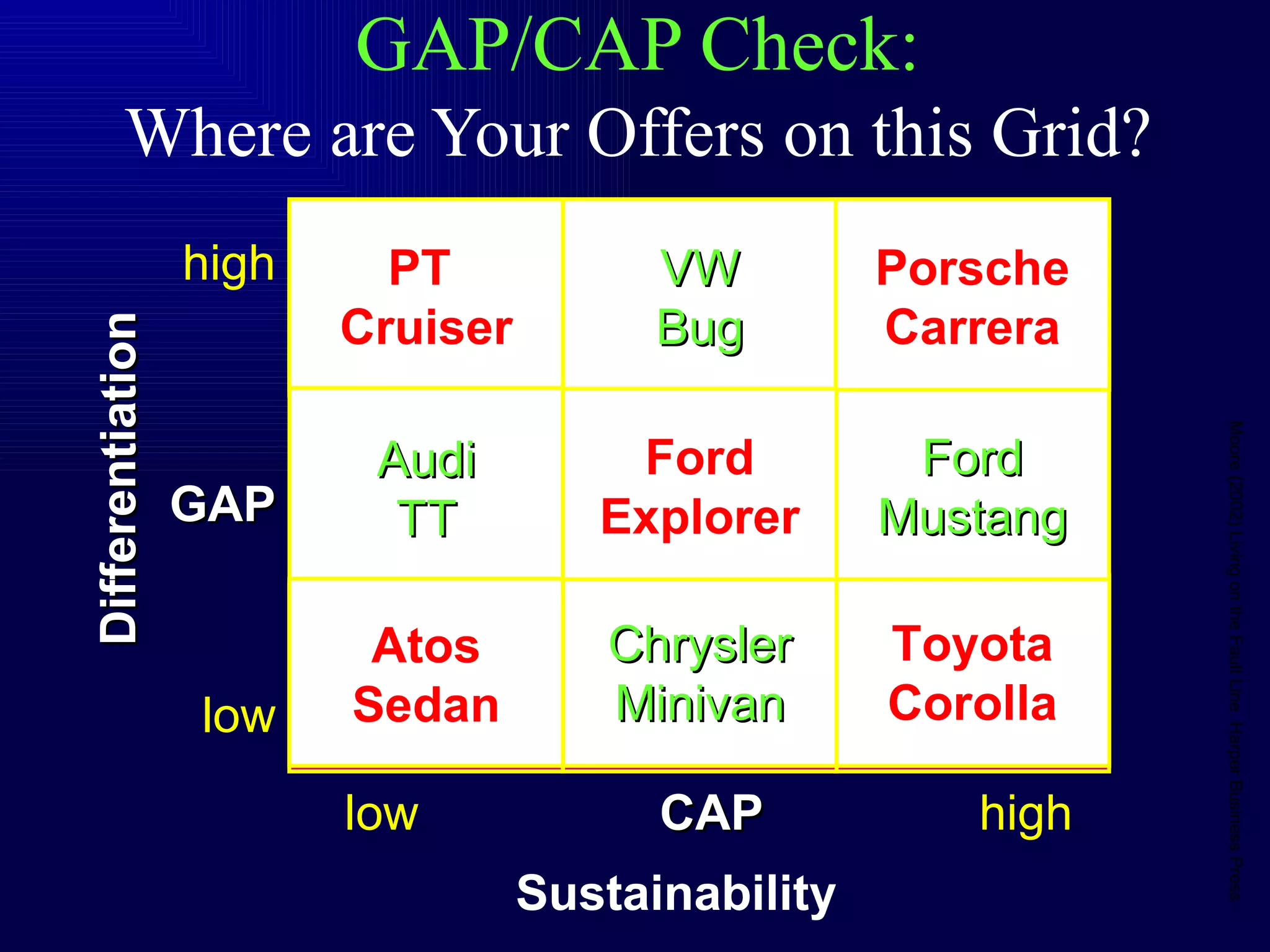

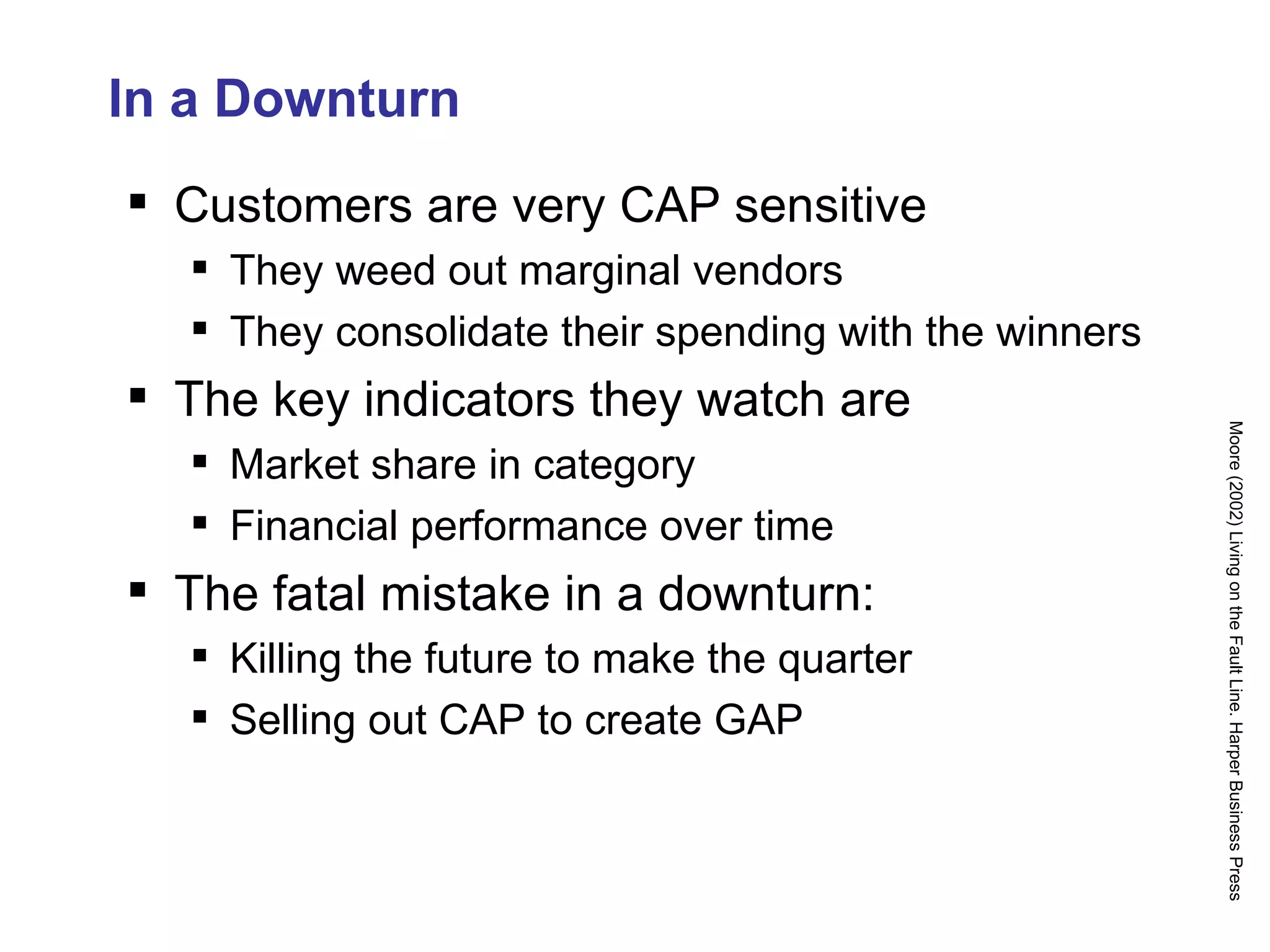

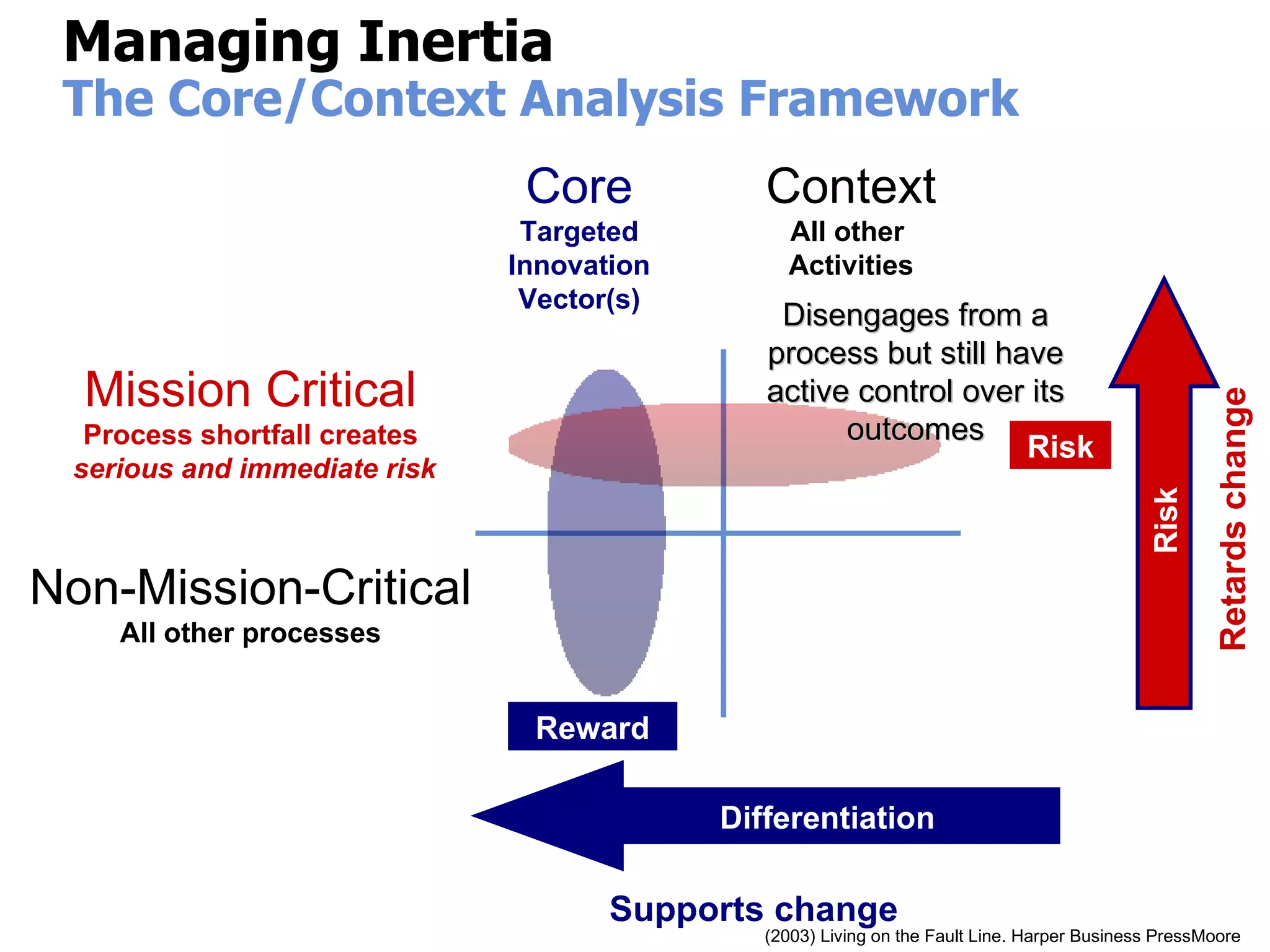

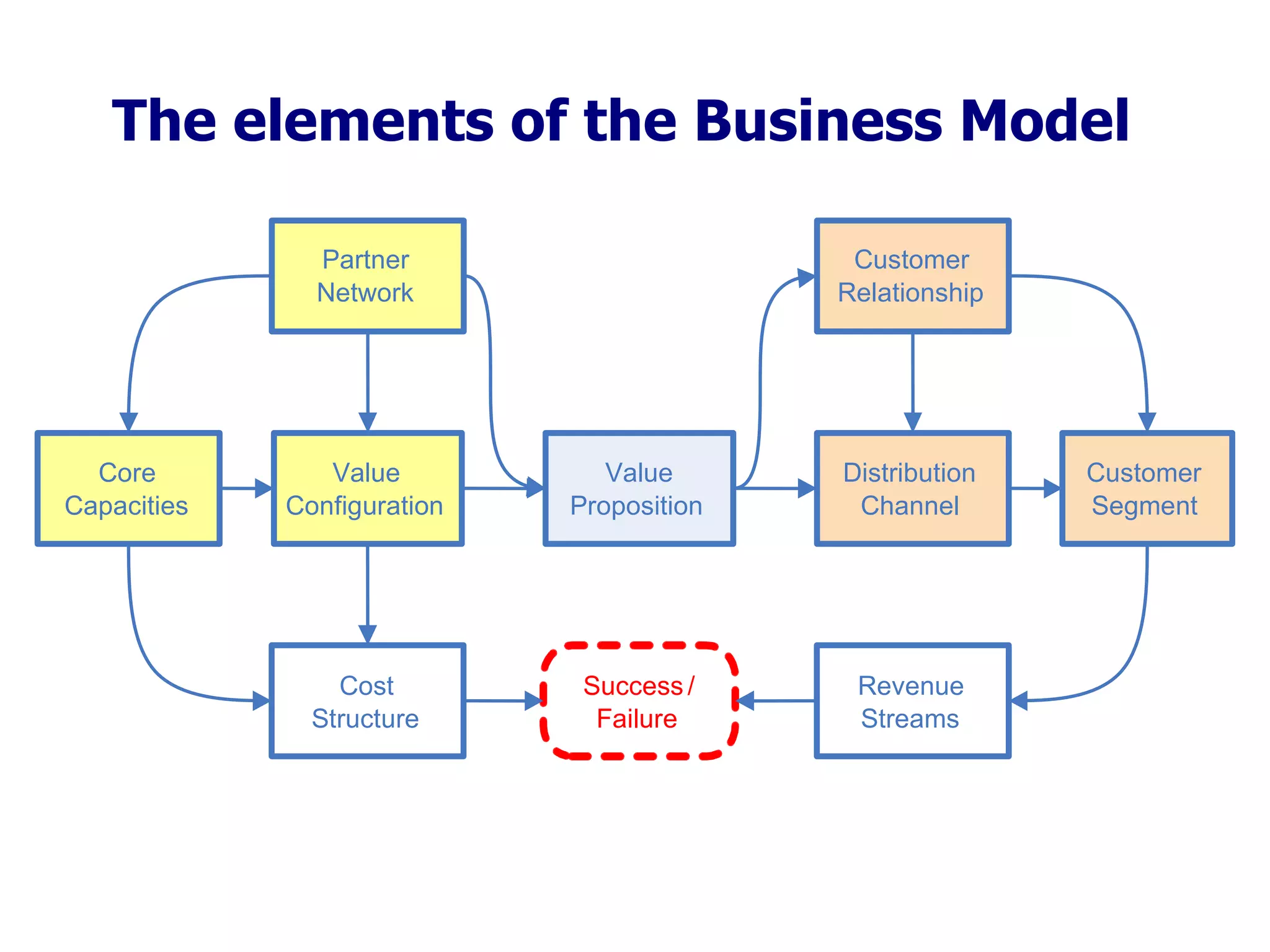

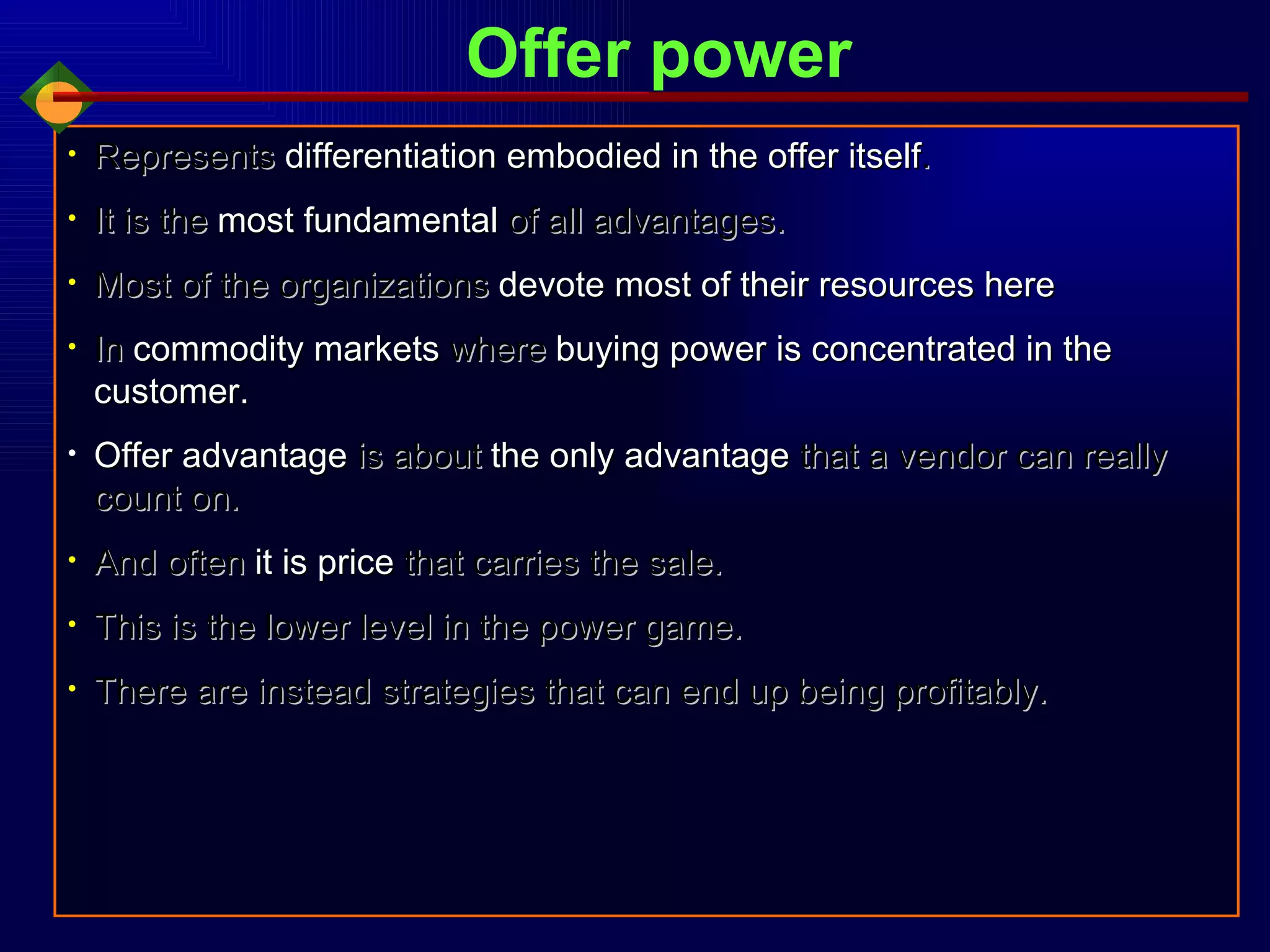

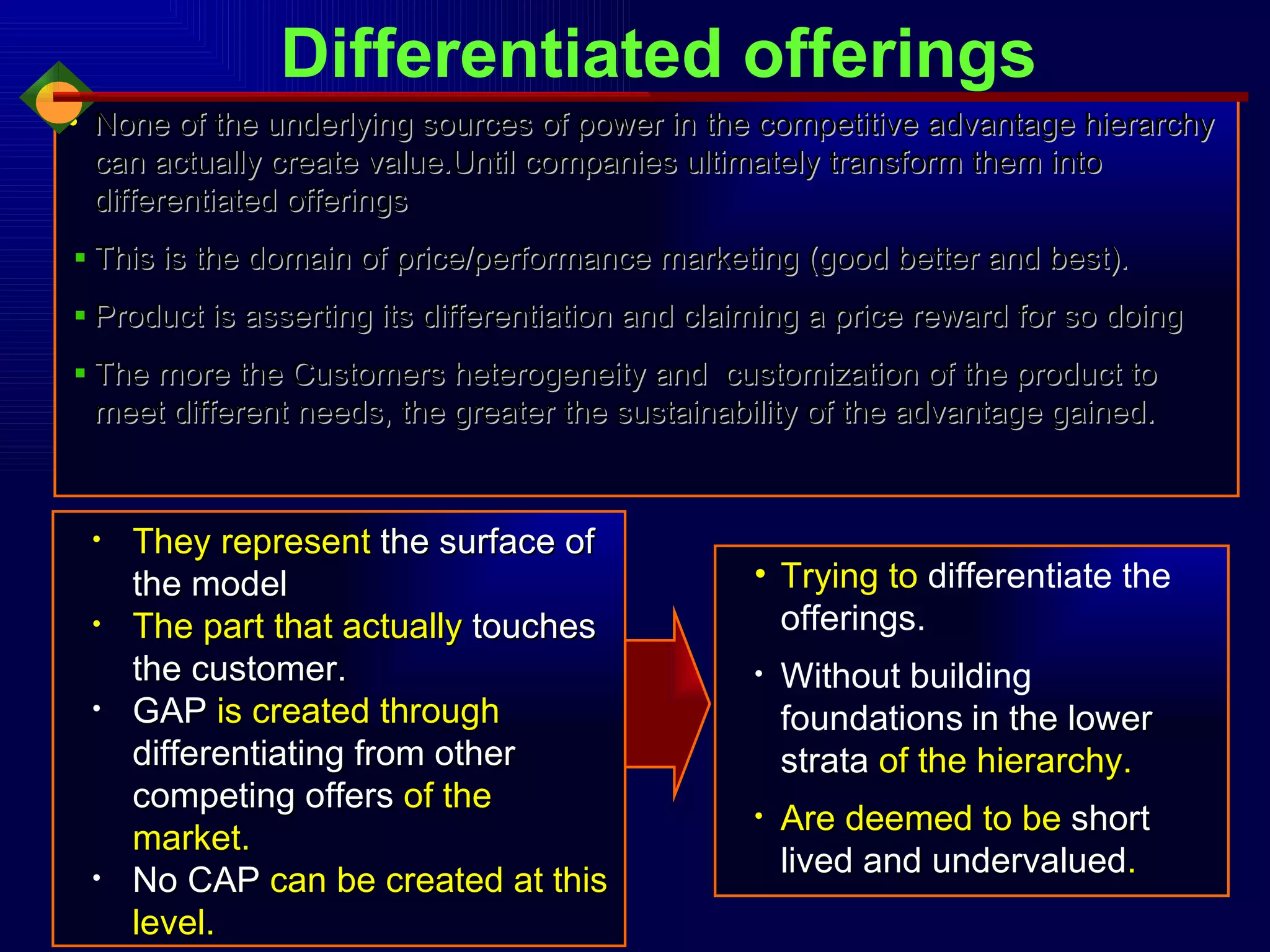

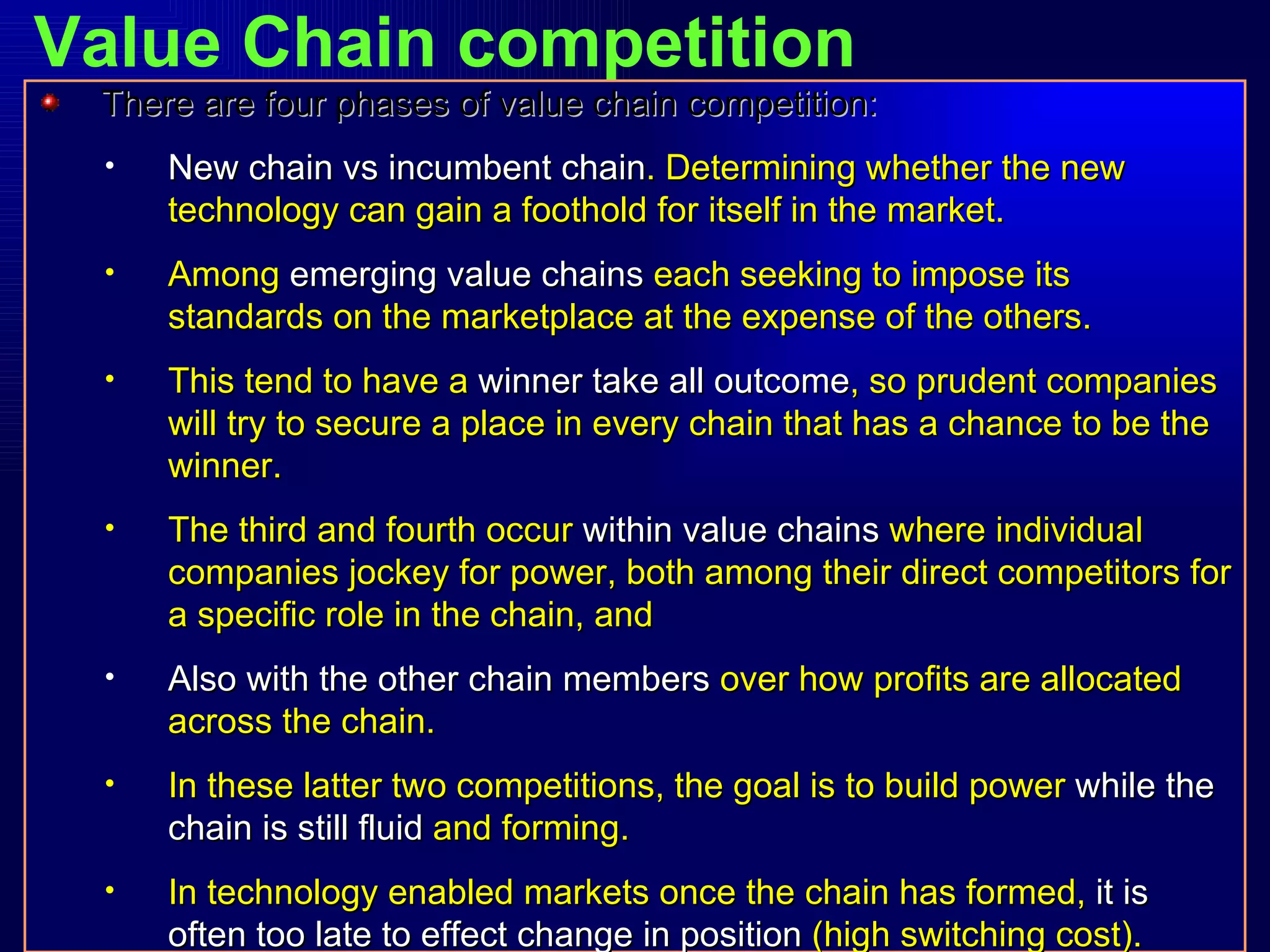

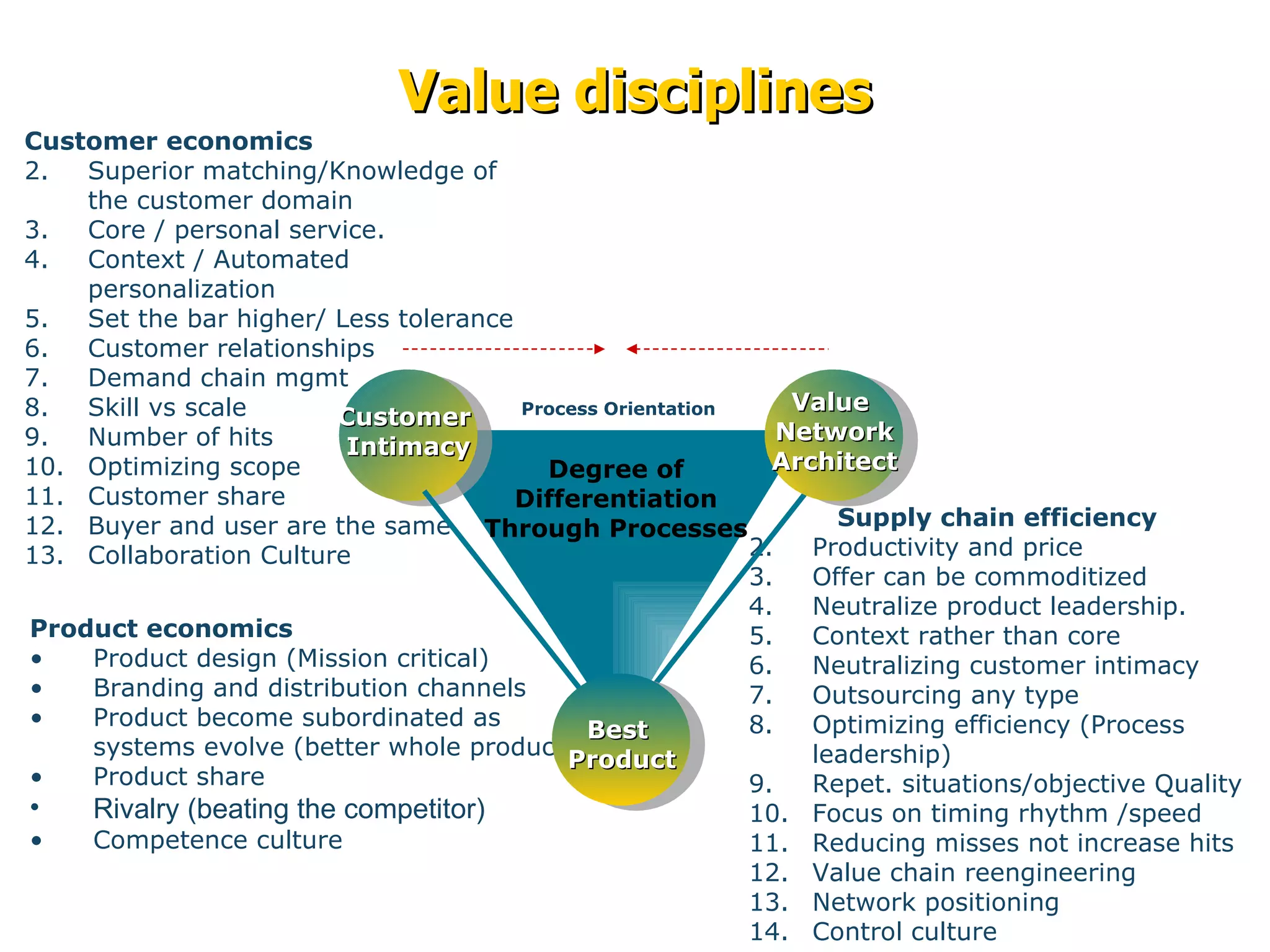

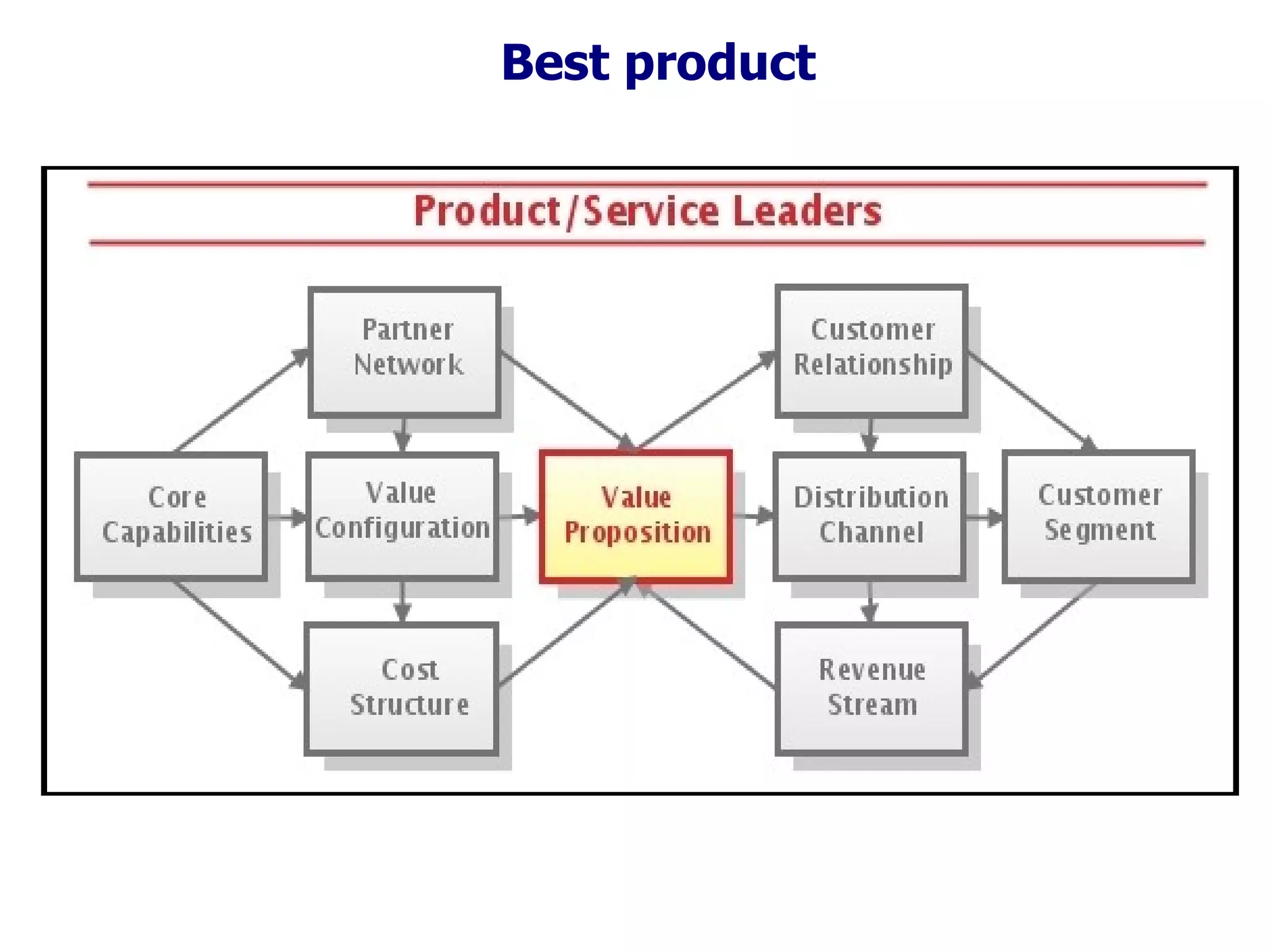

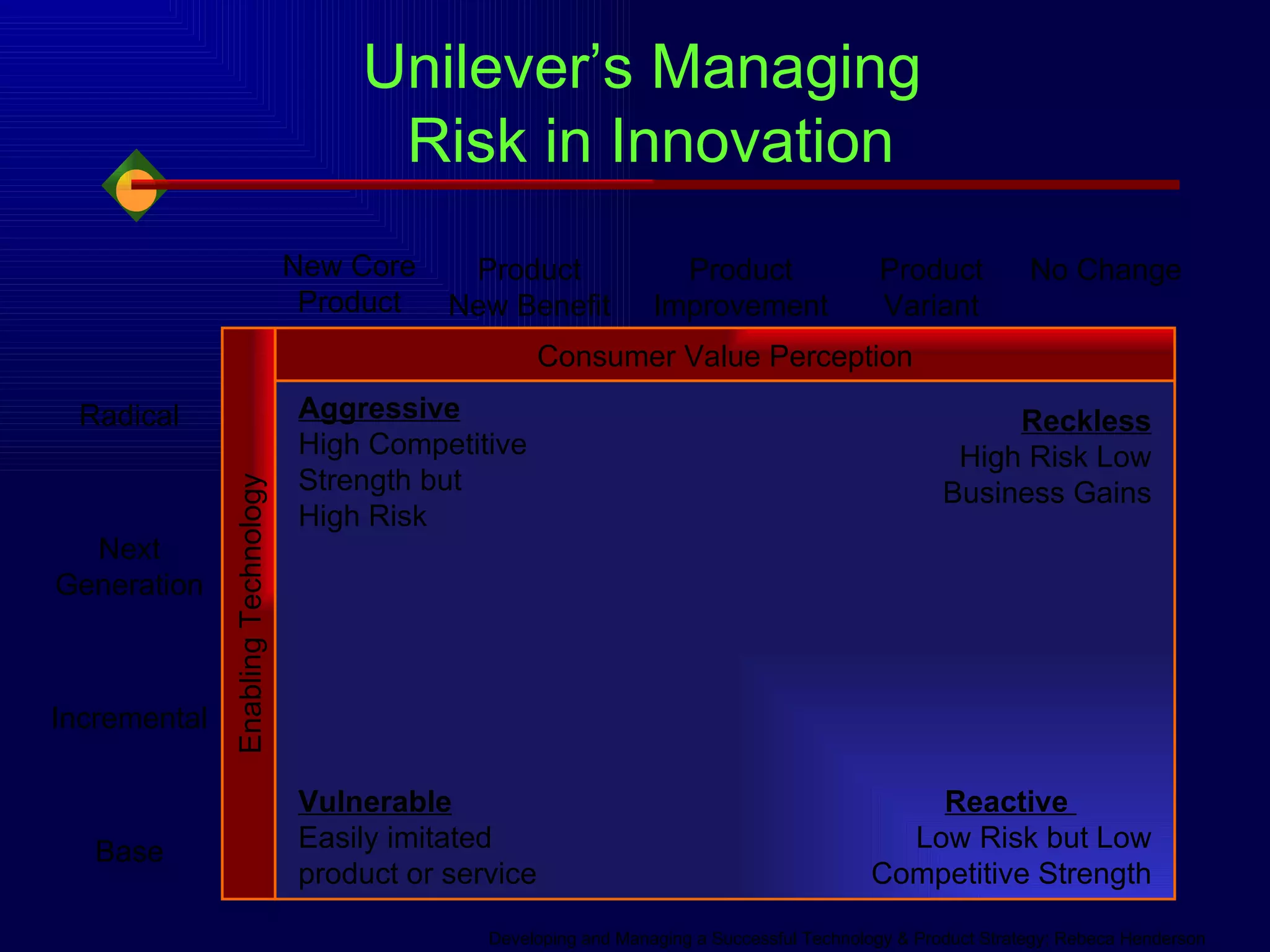

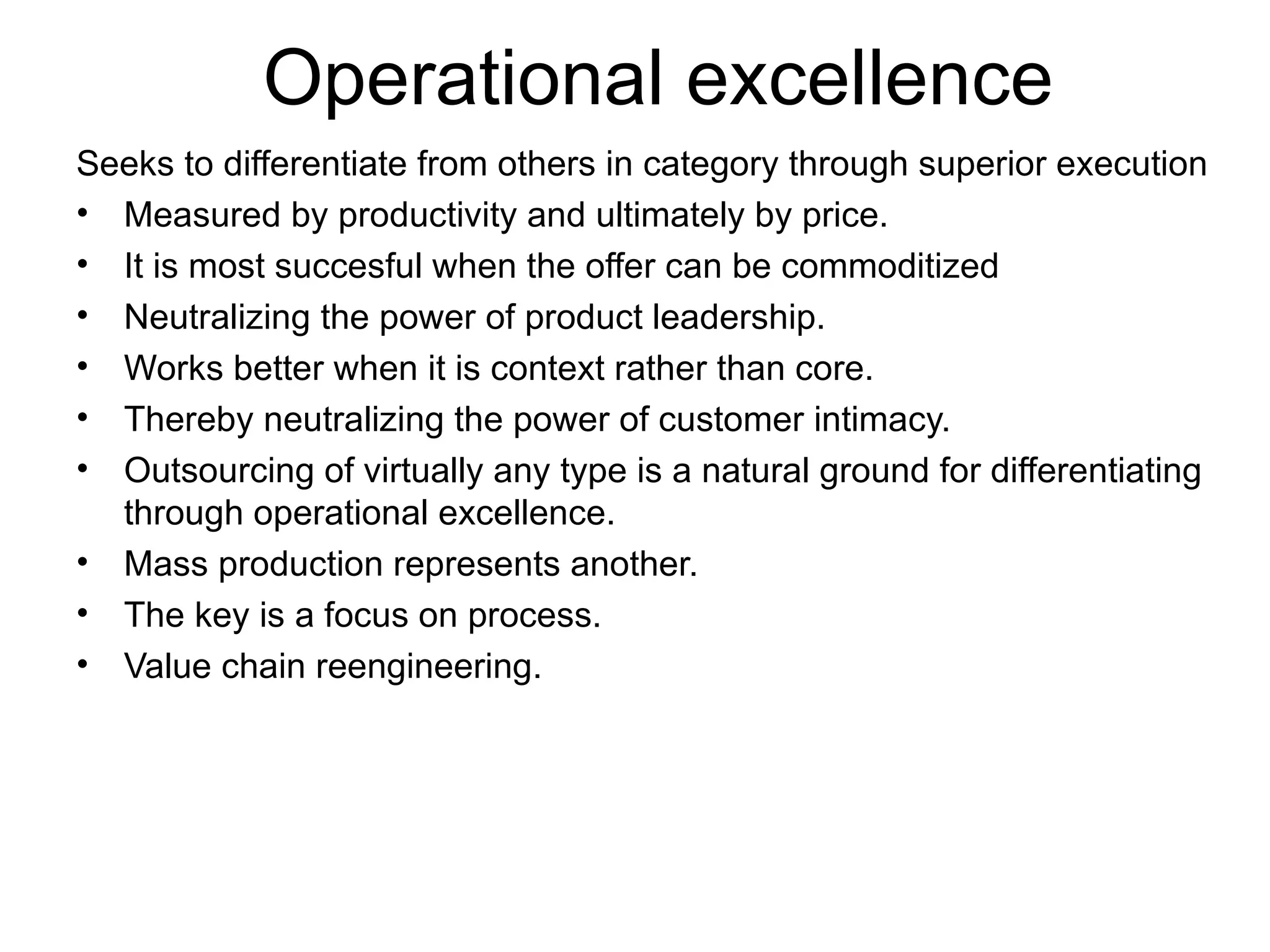

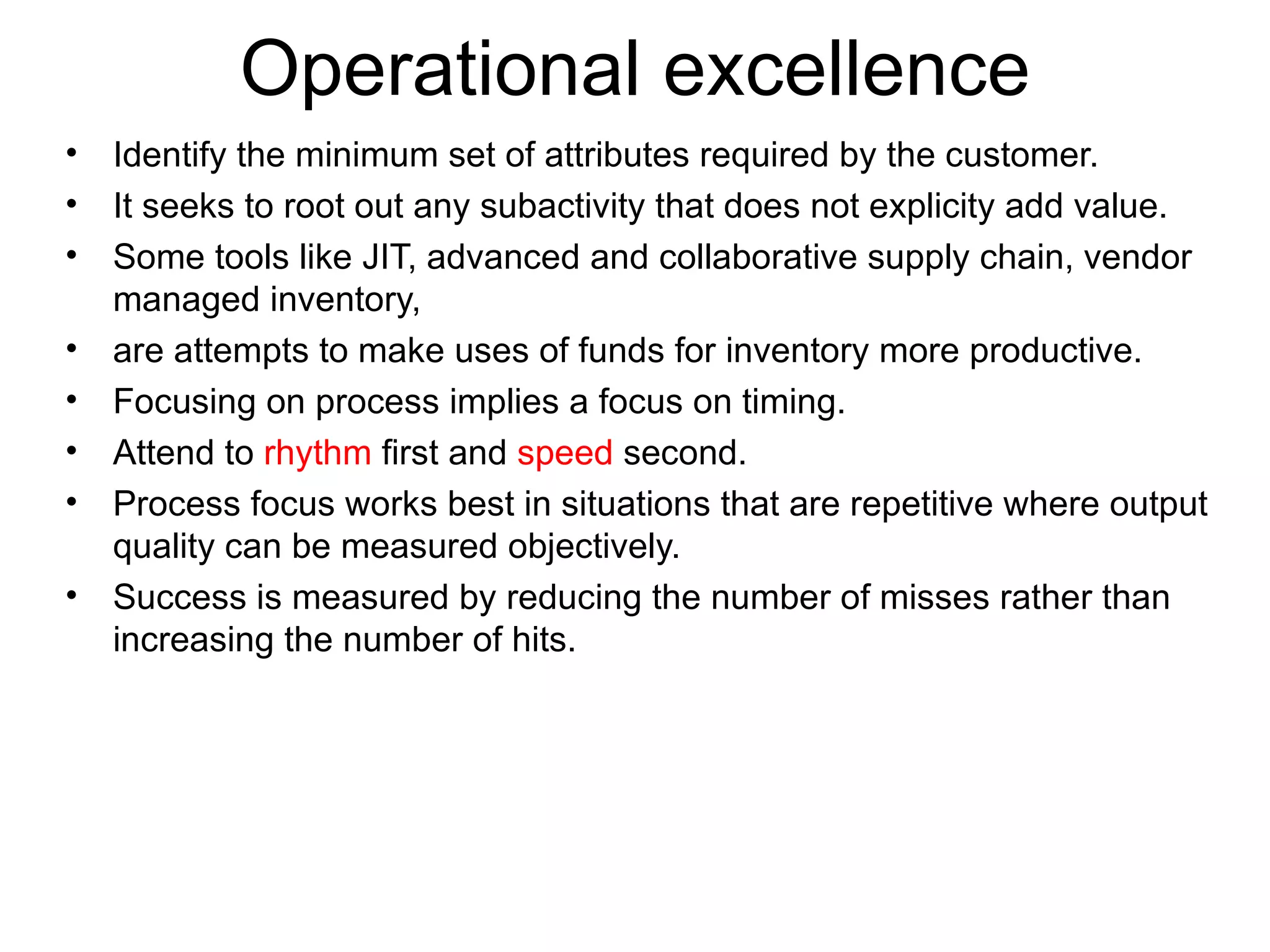

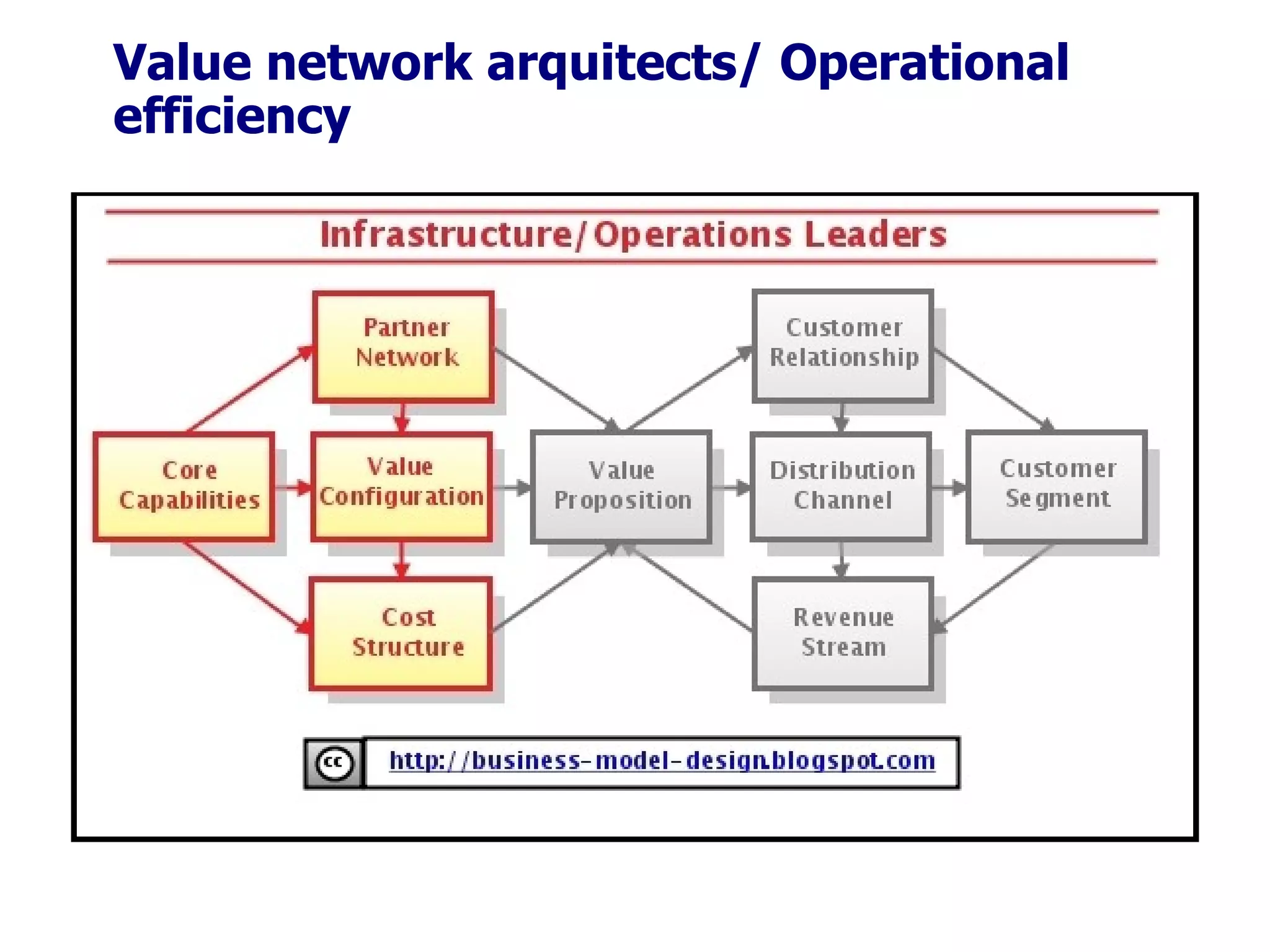

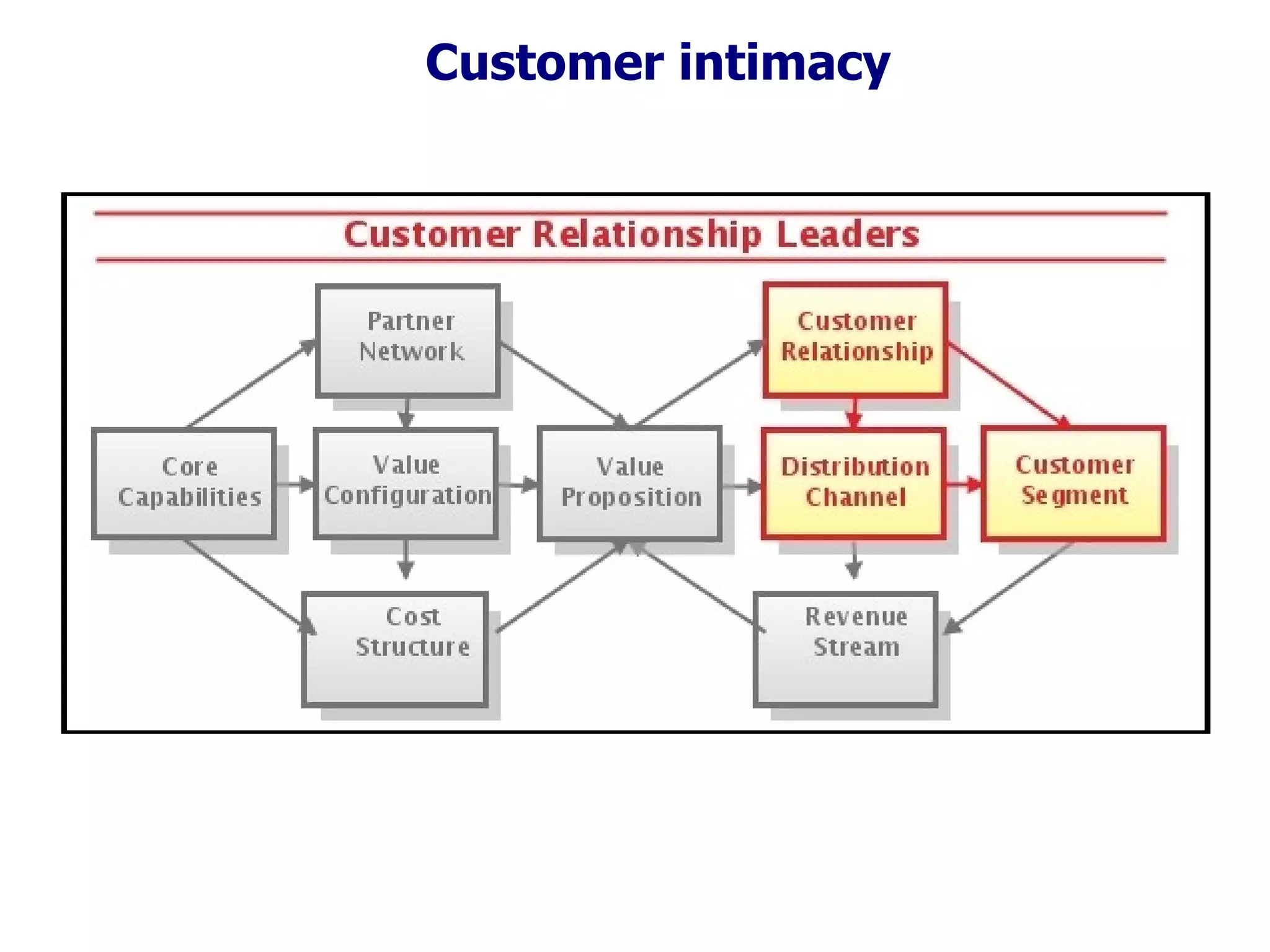

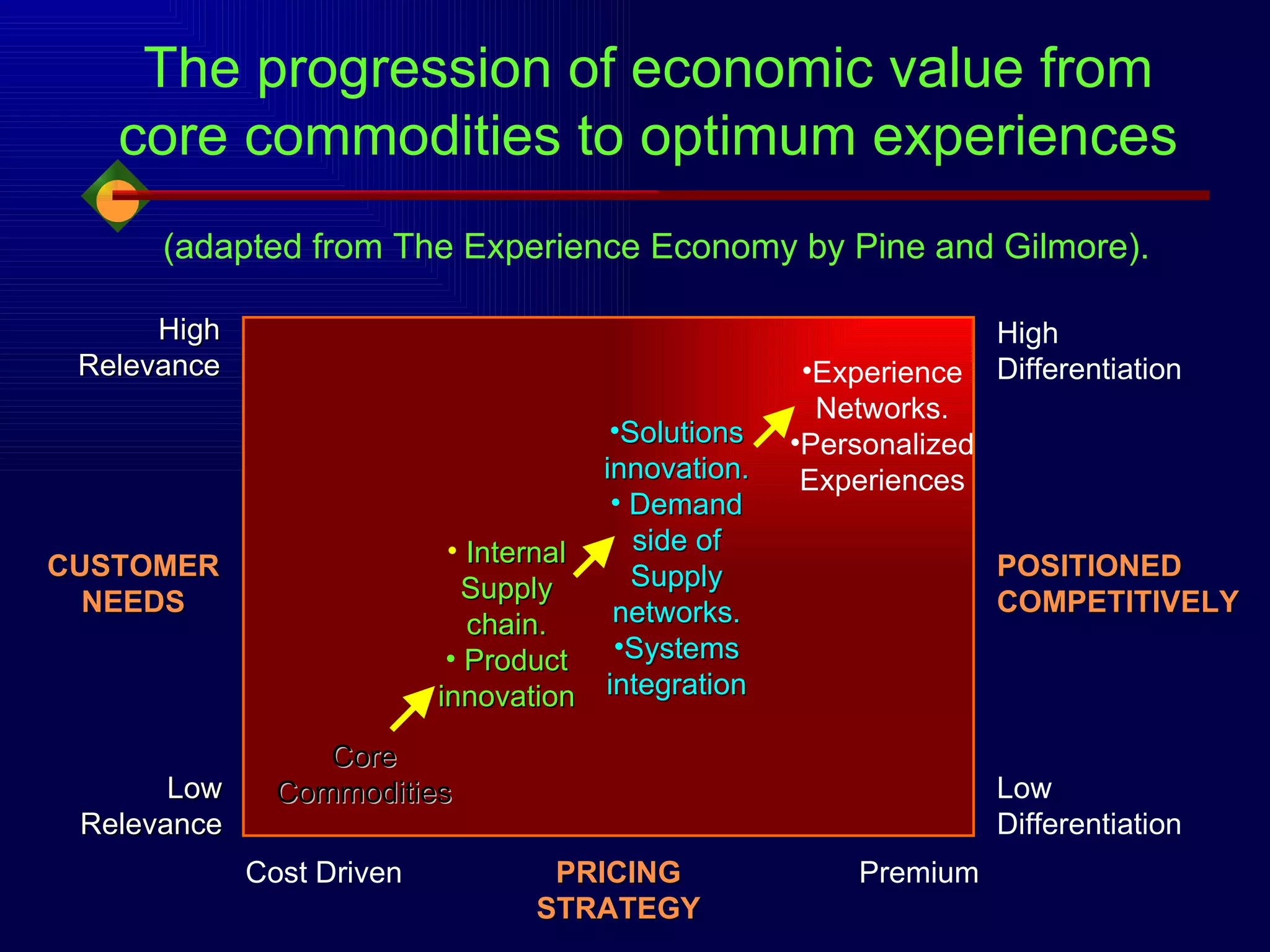

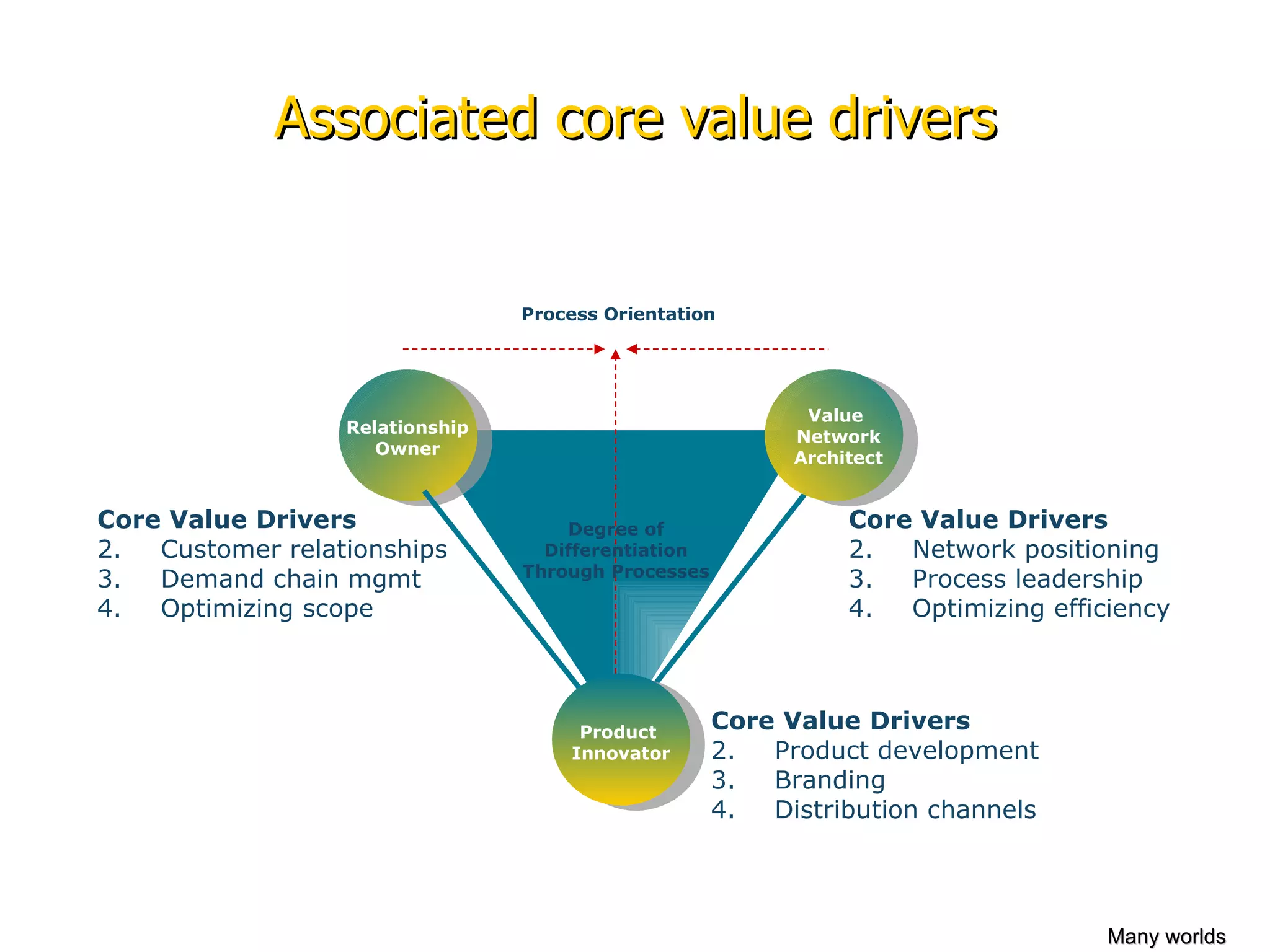

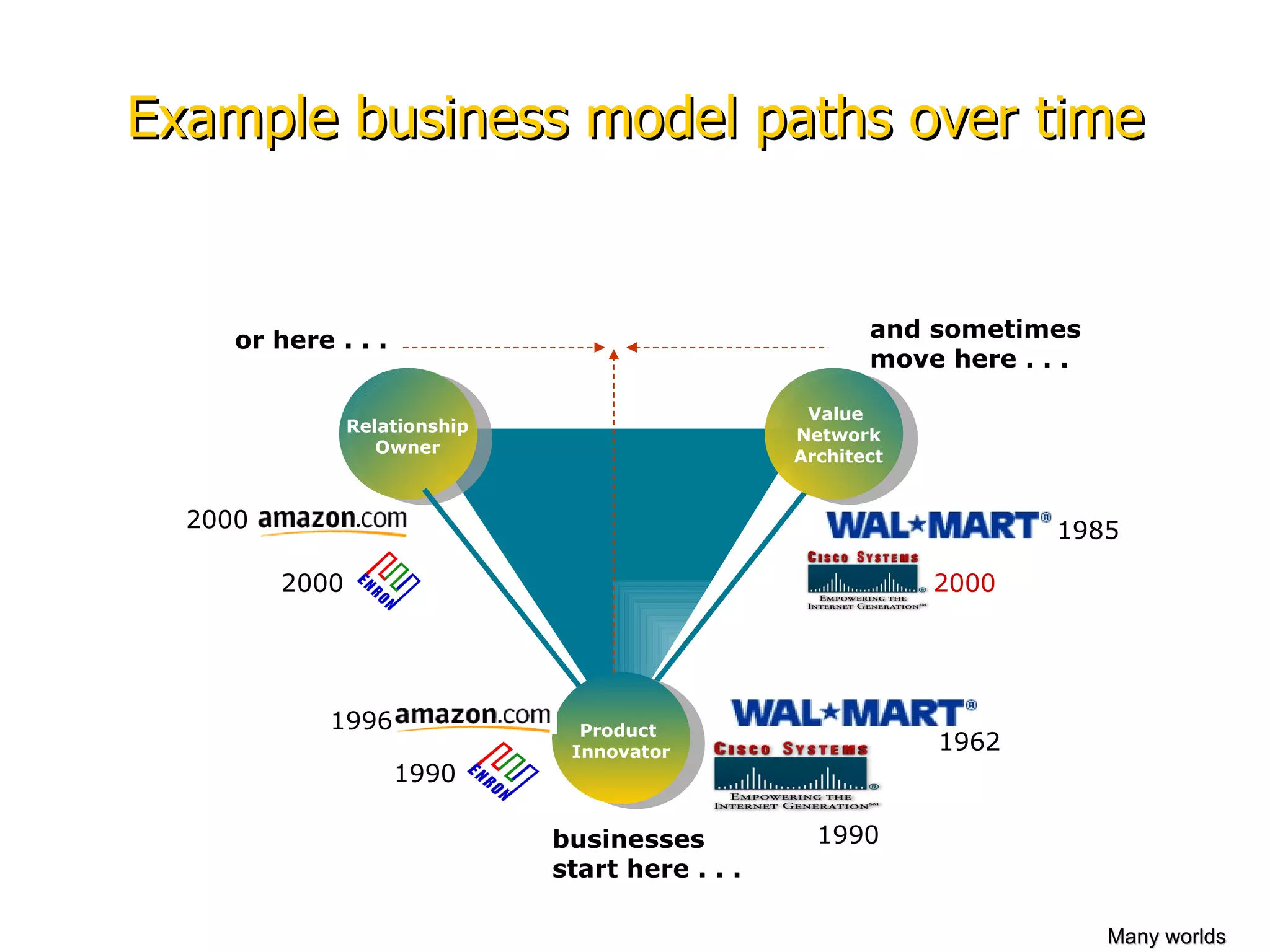

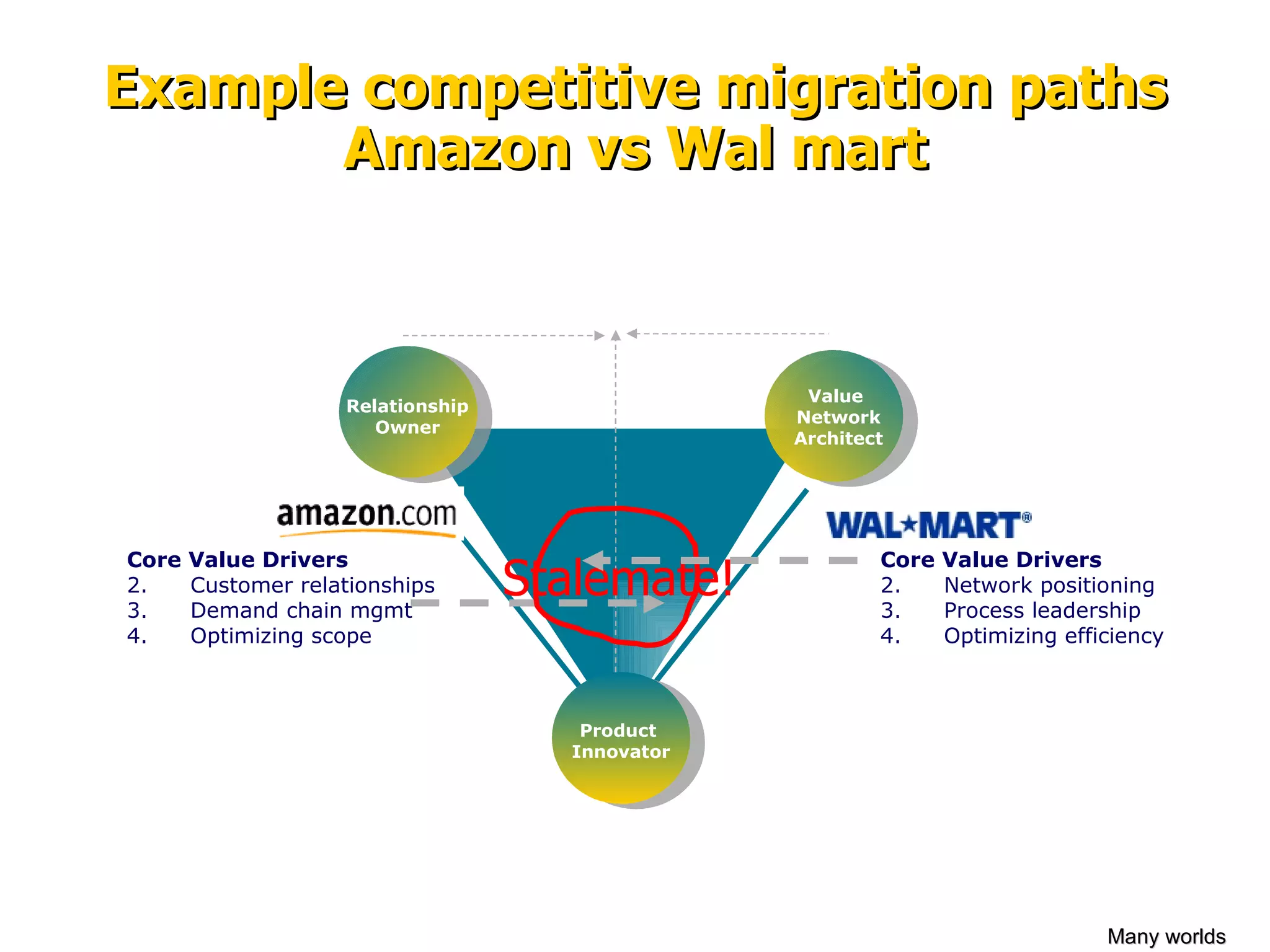

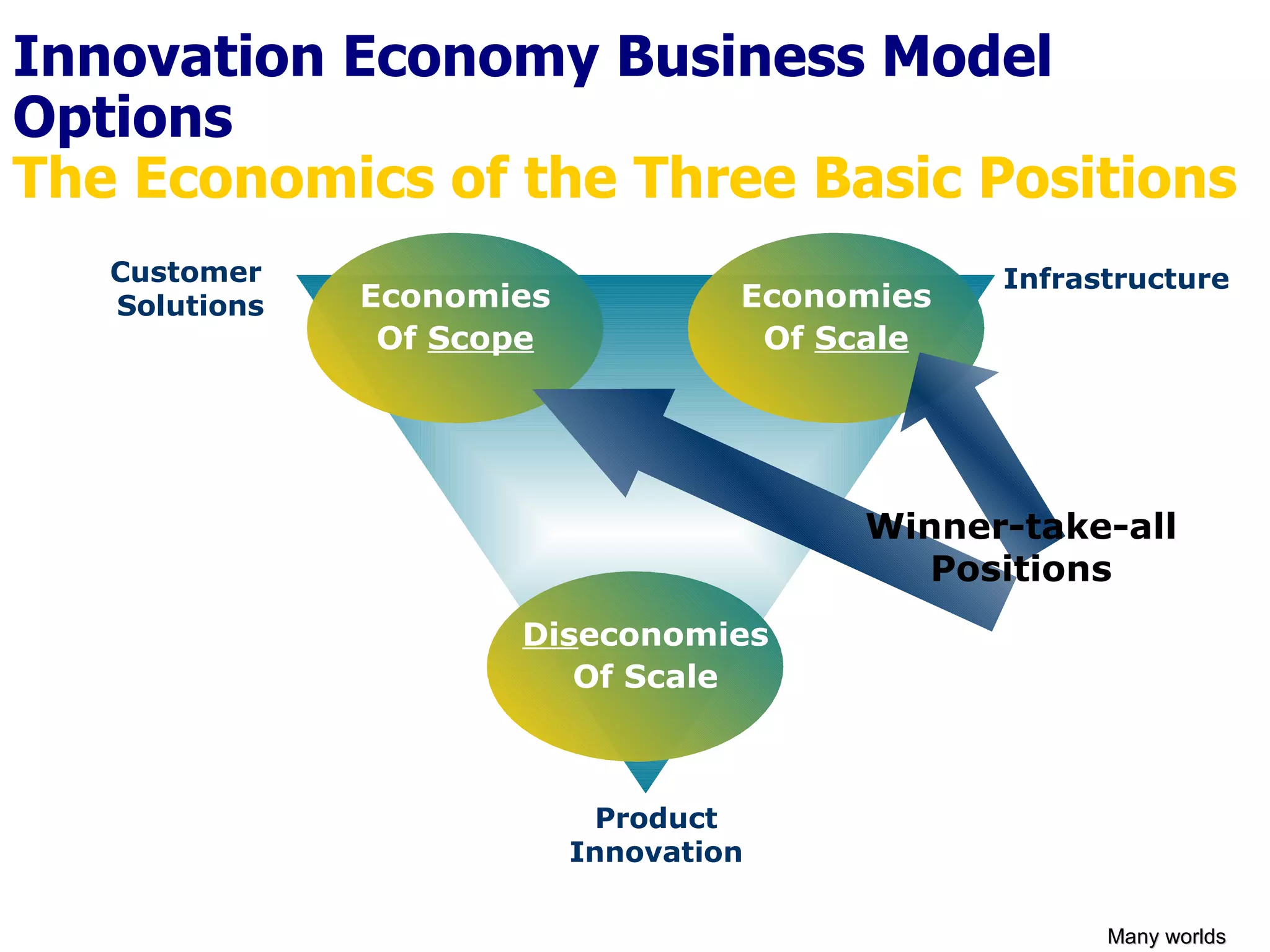

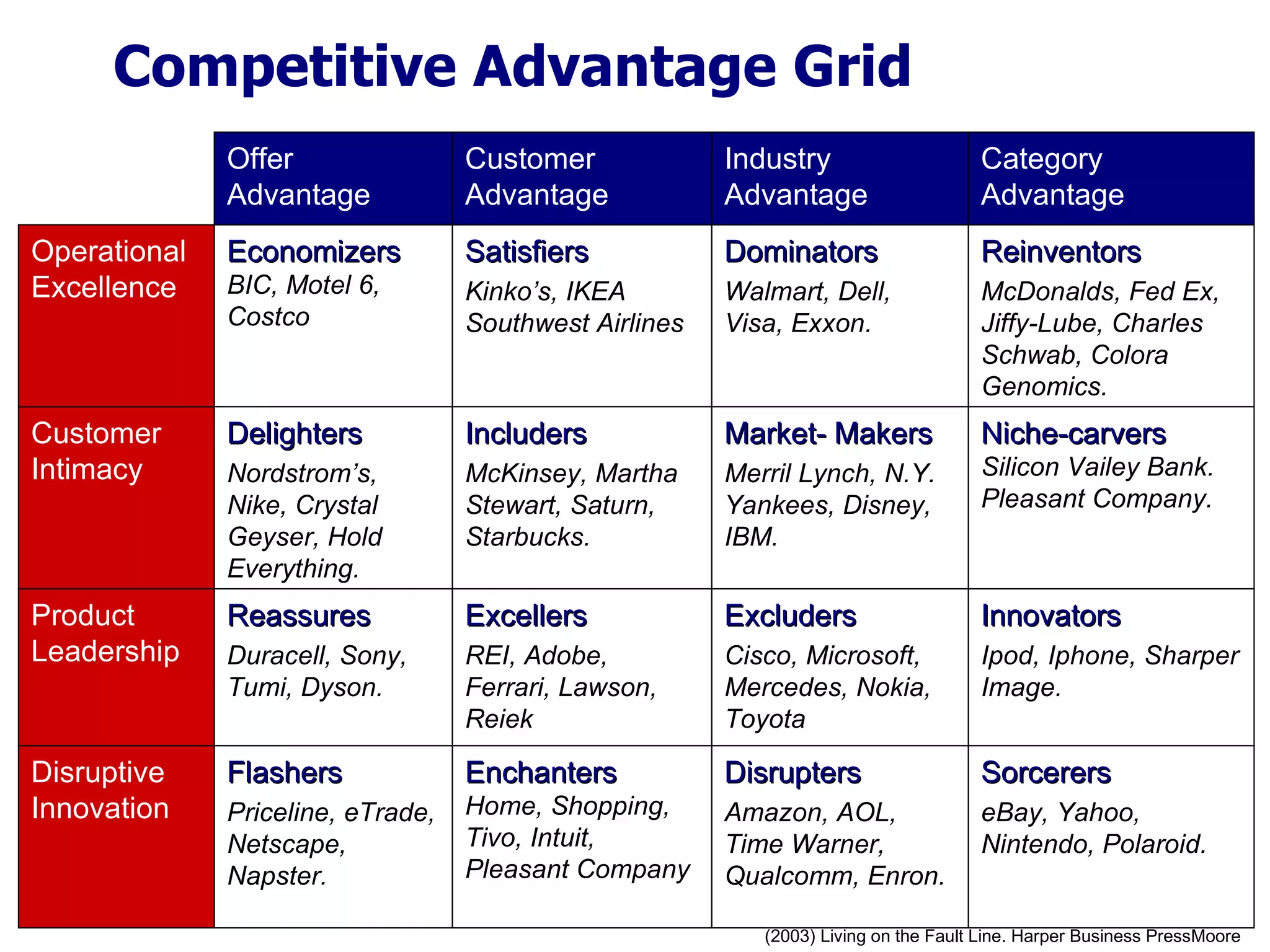

The document discusses various concepts related to competitive advantage and business strategy: 1) It describes different value disciplines like product leadership, operational excellence, and customer intimacy that companies can use to gain competitive advantage. 2) Key factors that determine competitive advantage are discussed, from offering differentiation to controlling important market segments and value chains. 3) The concept of the "competitive advantage hierarchy" is introduced, where advantages lower in the hierarchy like offering differentiation are more fundamental but narrow, while advantages higher like value chain dominance provide stronger leverage but over a limited domain.

![1. b2 b marketing & crm [imcost] chapter first](https://cdn.slidesharecdn.com/ss_thumbnails/1-b2bmarketingcrmimcostchapterfirst-111124203610-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Customer database and database marketing 19-10-13 [compatibility mode]](https://cdn.slidesharecdn.com/ss_thumbnails/customerdatabaseanddatabasemarketing-19-10-13compatibilitymode-140119122506-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)