- Owens Corning presented at a Goldman Sachs roadshow in November 2016 to discuss its businesses and financial performance.

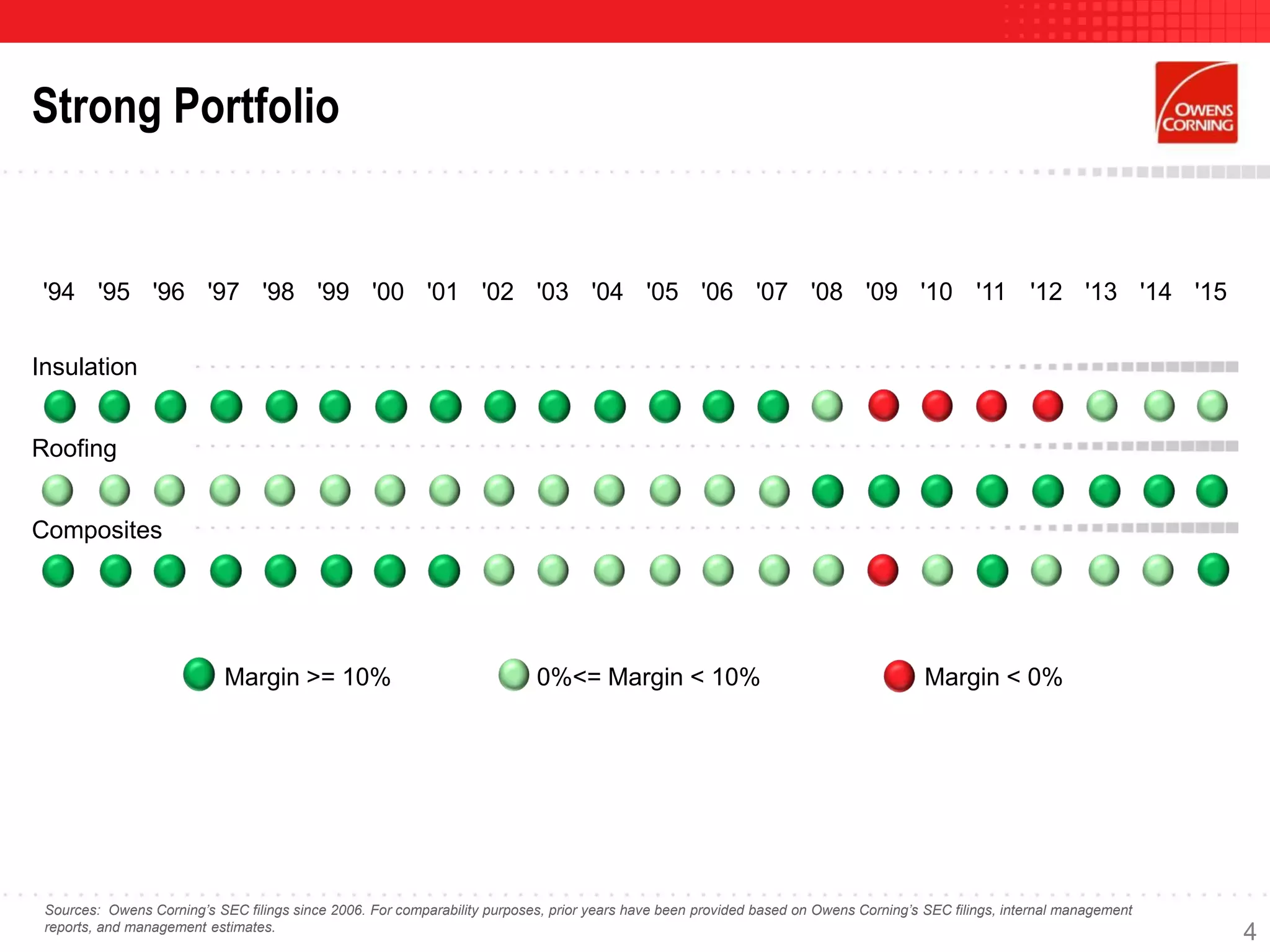

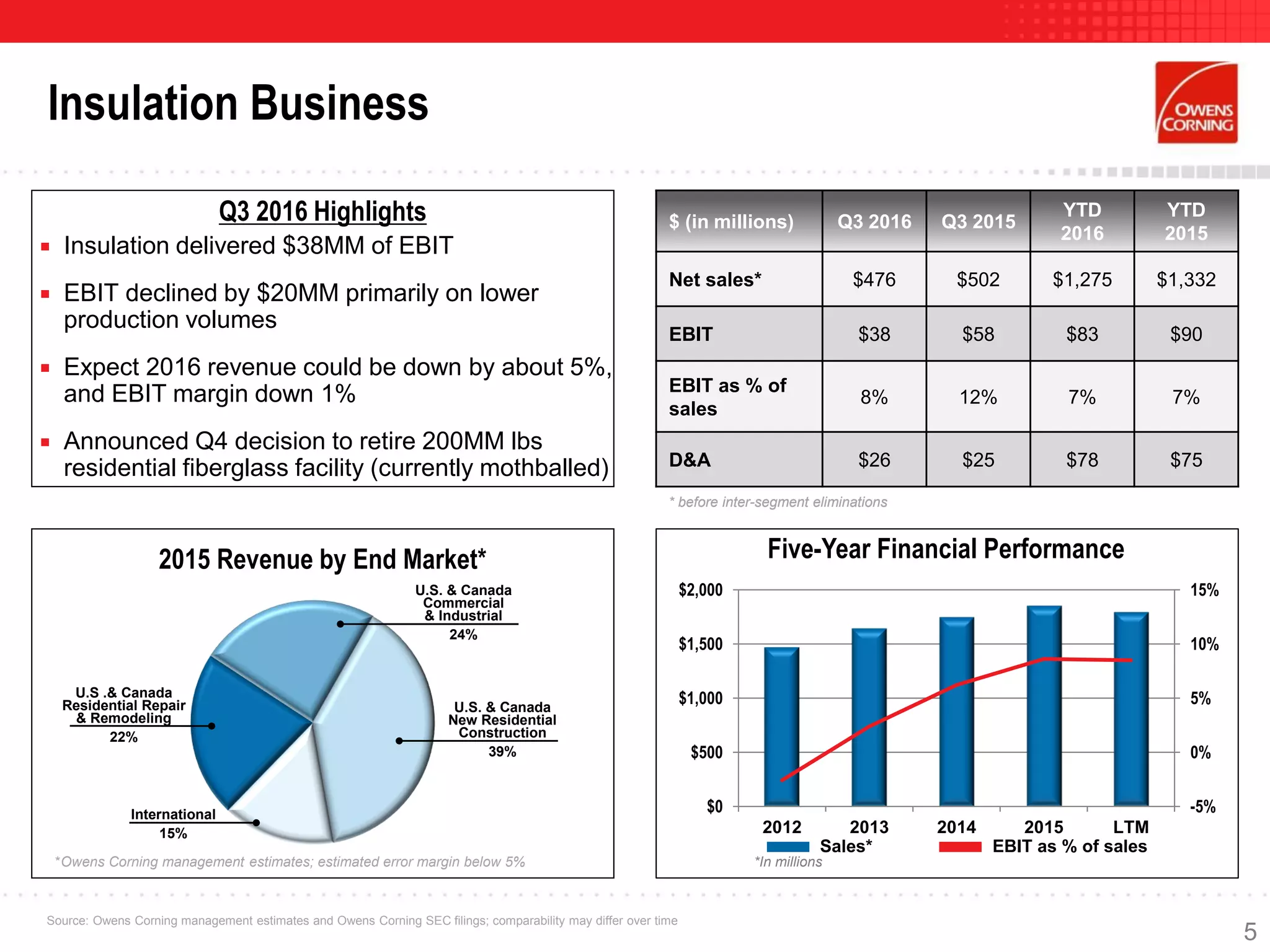

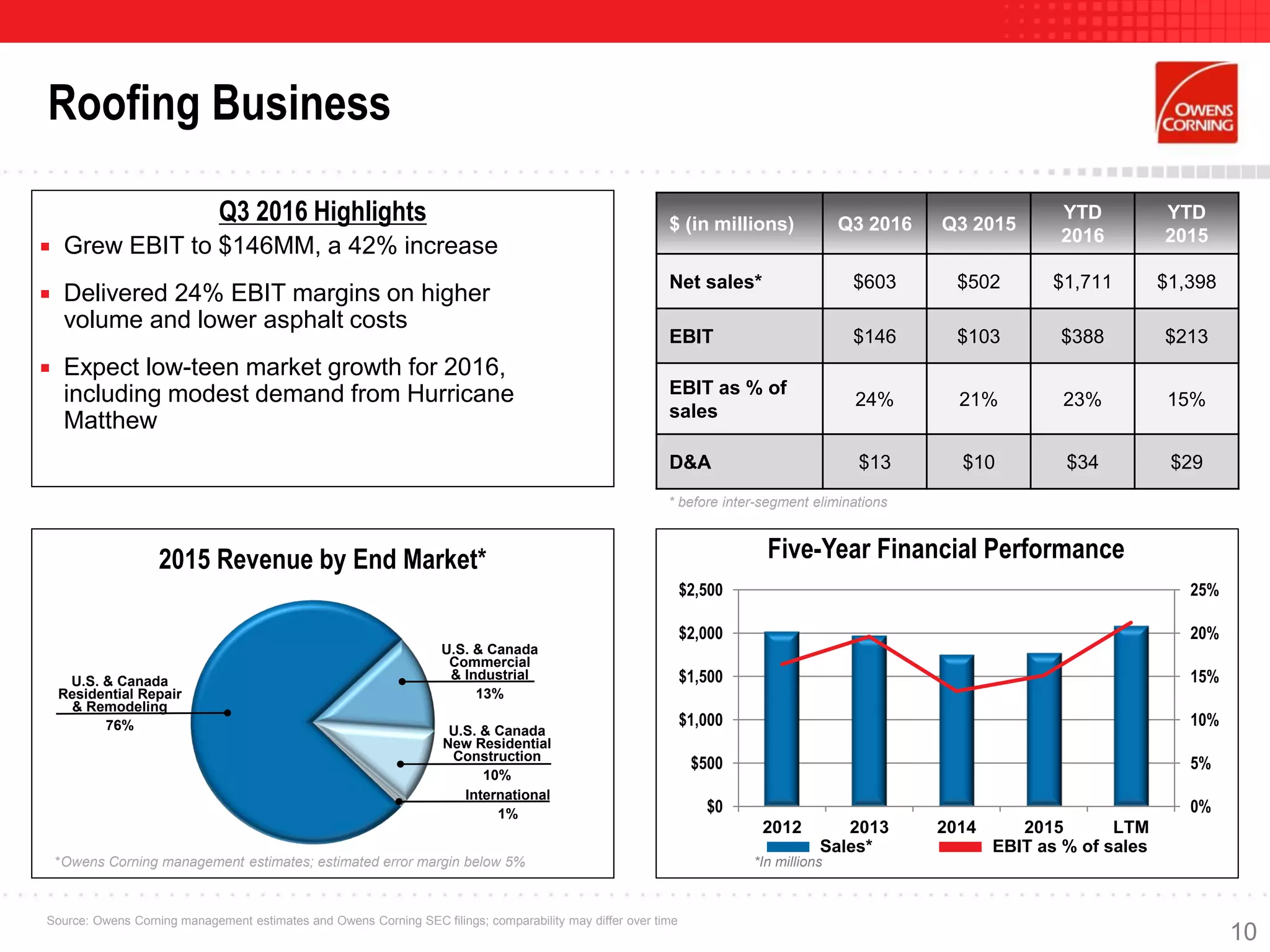

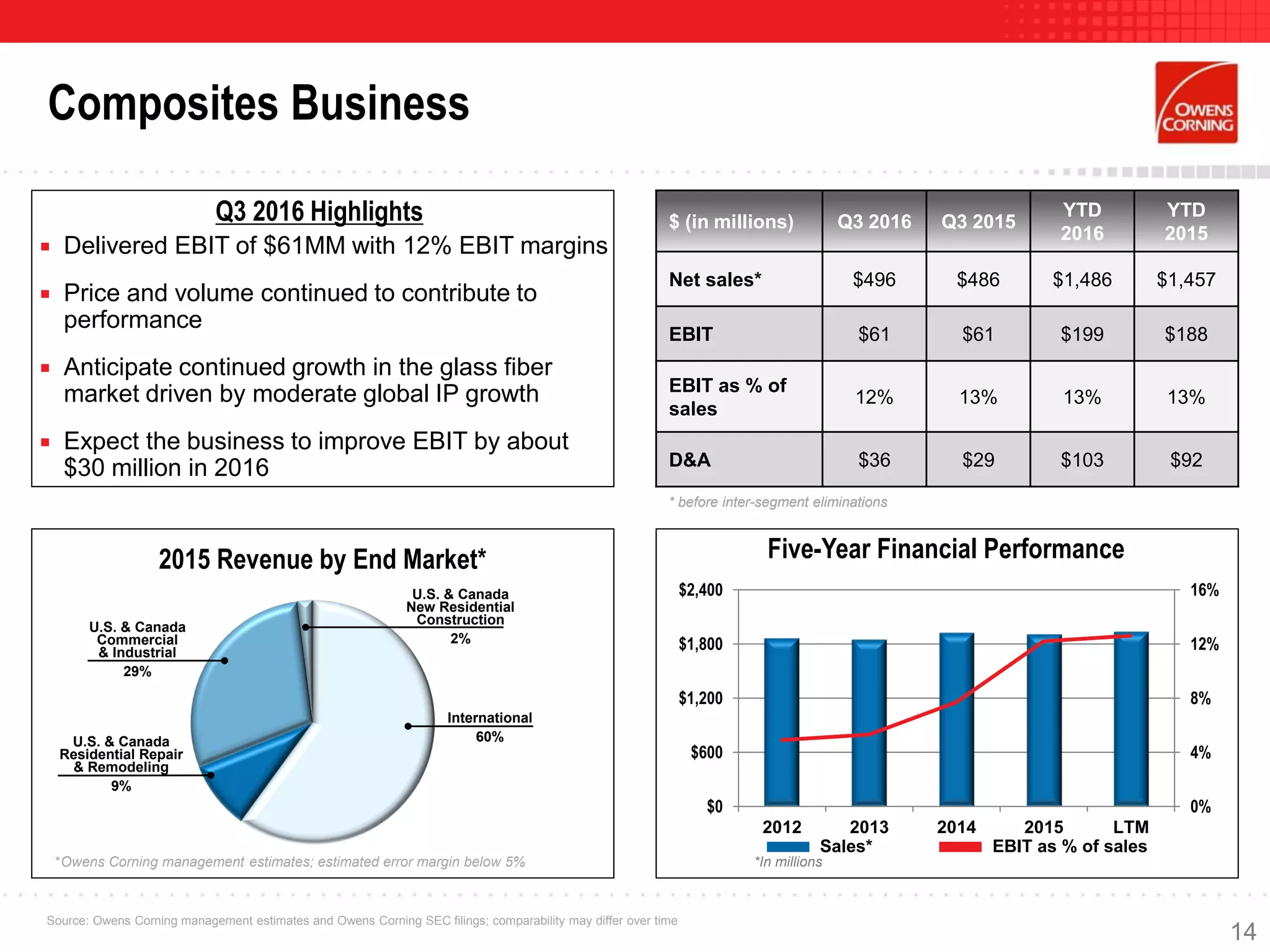

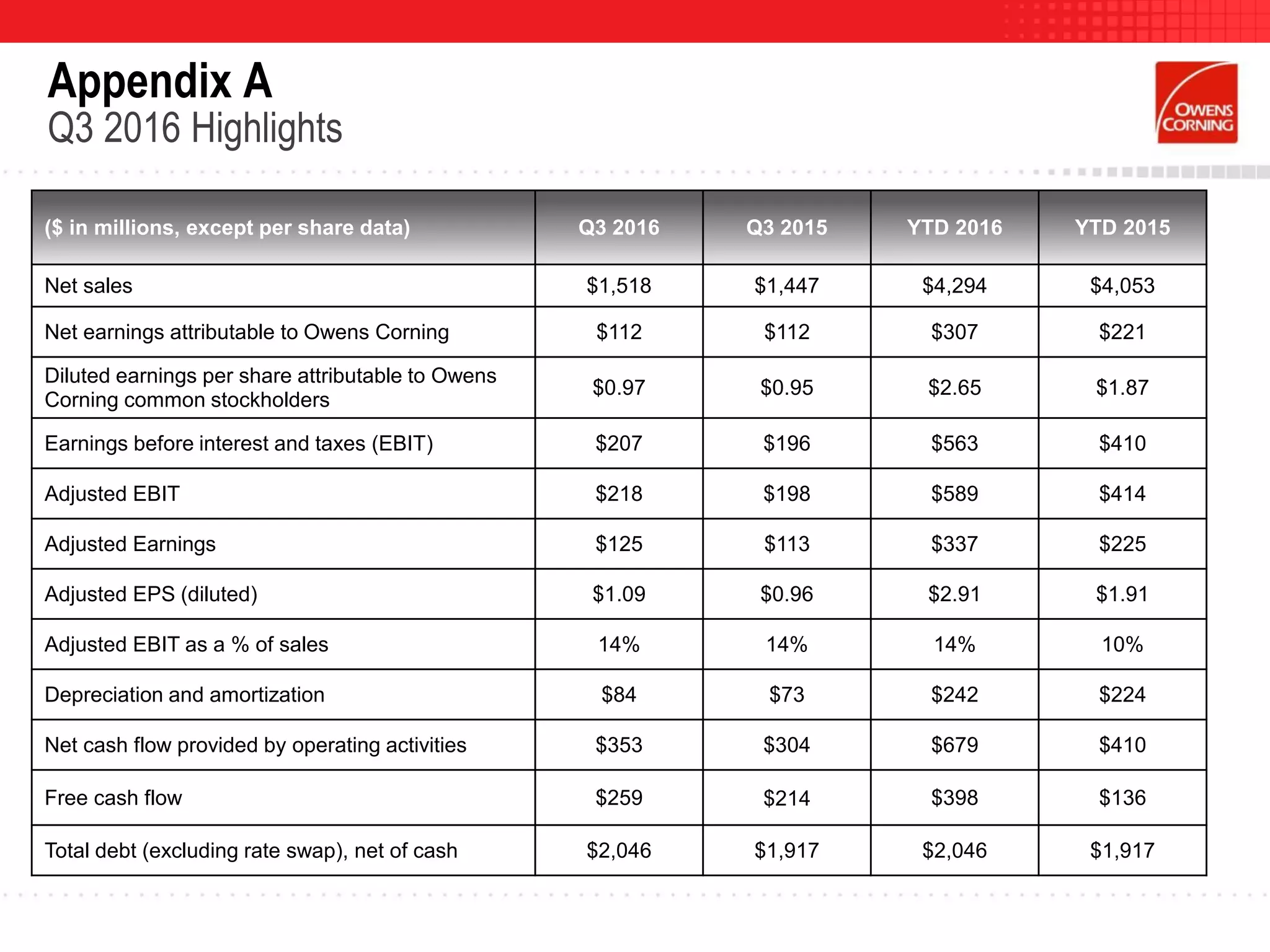

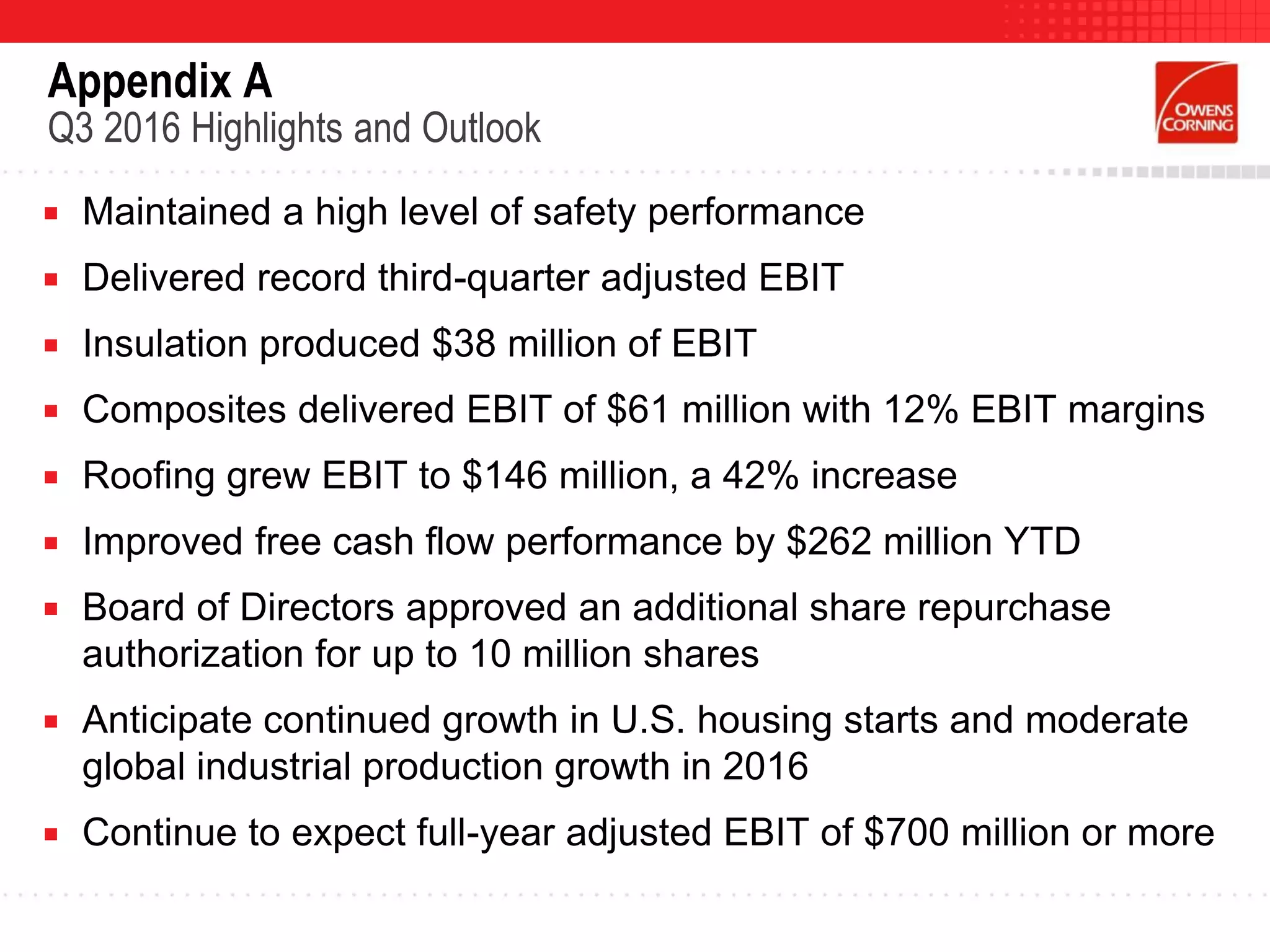

- The presentation discussed Owens Corning's three market-leading businesses: insulation, roofing, and composites. It provided an overview of each business and highlights from Q3 2016 financial results.

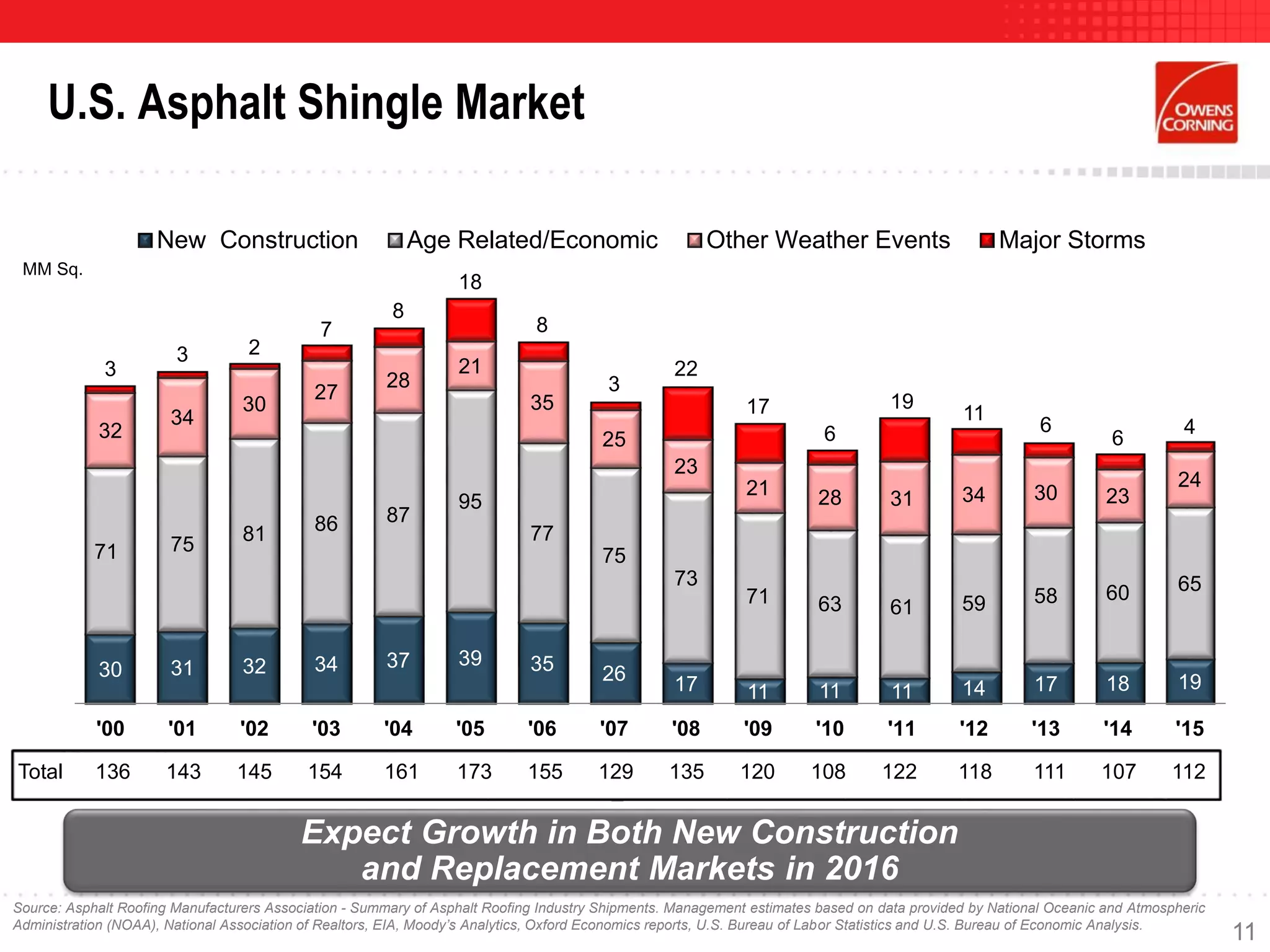

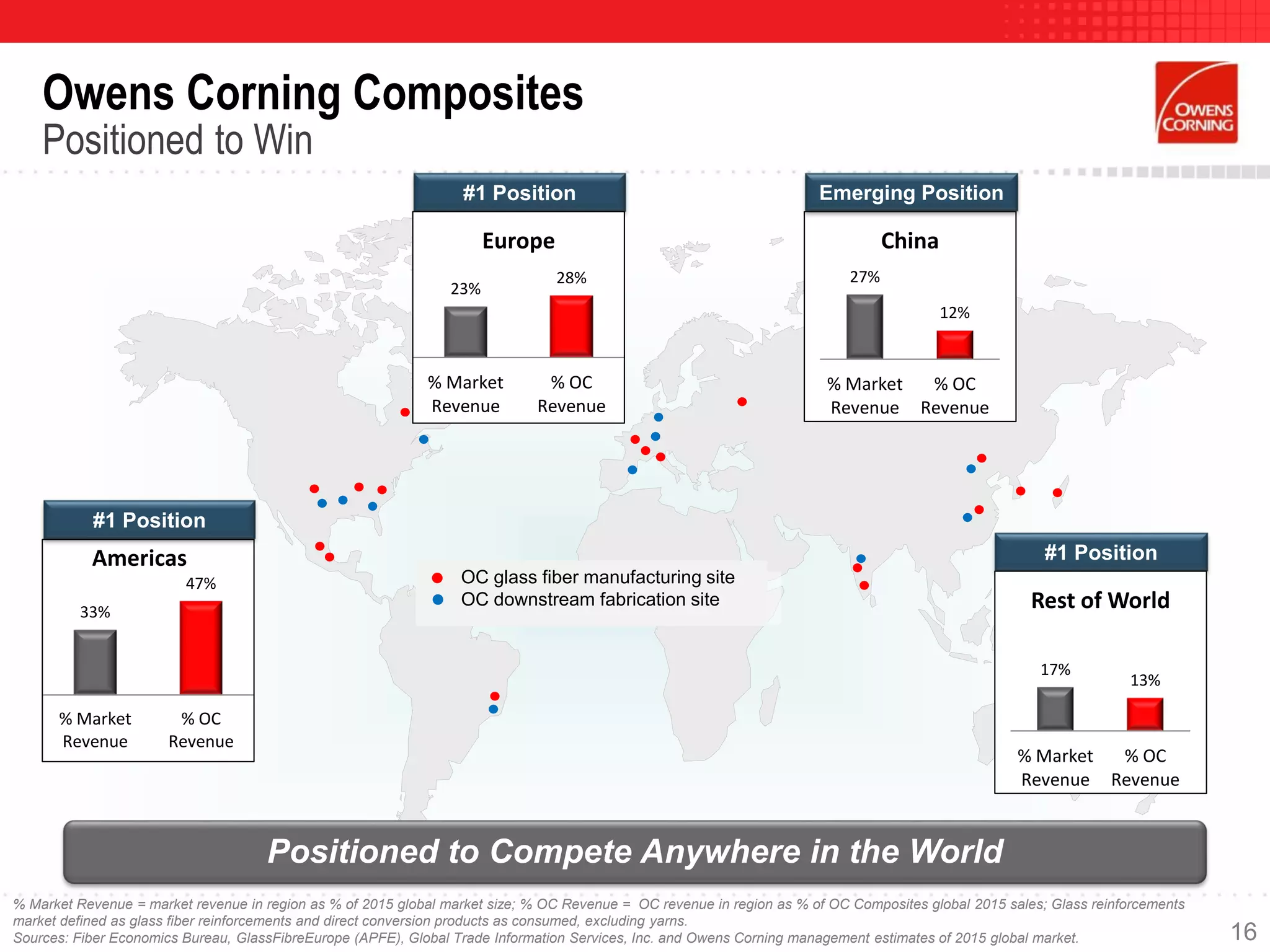

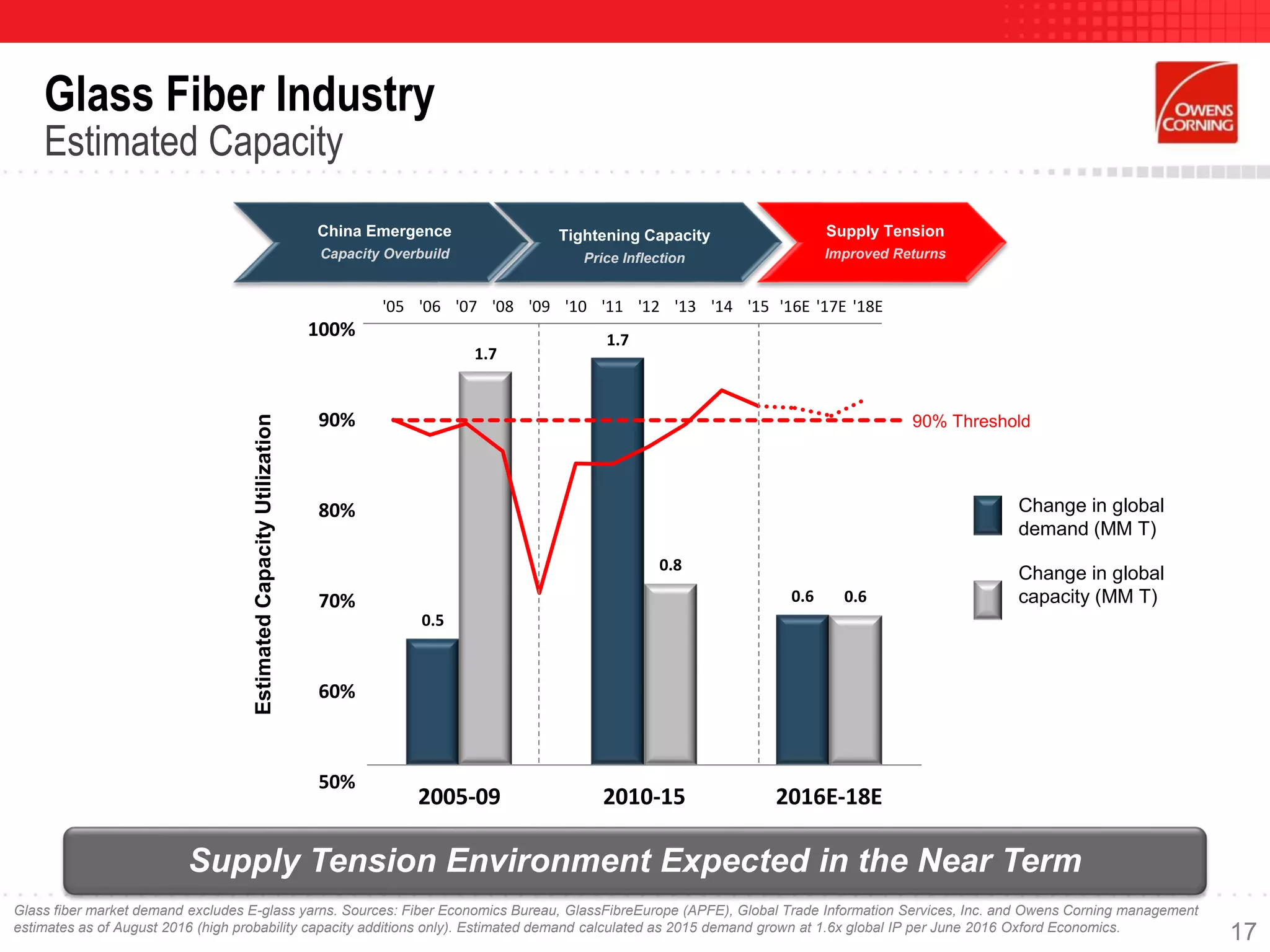

- The presentation also addressed industry dynamics and trends for each business, including expectations for market growth and capacity utilization rates that would drive Owens Corning's profitability going forward.