2

Contents

Executive summary 3

01.Introduction 5

02. The changing legislation around State Pension Age 7

03. Independent reviews of State Pension Age conducted to date 10

04. The third State Pension Age review 15

05. Proposals 18

06. Wider considerations and alternative approaches 23

3.

3

Executive Summary

Changing legislationaround State Pension Age

Despite huge improvements in life expectancy during the 20th Century, State Pension Age

(SPA) has been very slow to adjust. SPA was set at 65 (for both men and women) in the

mid-1920s and reduced to 60 for women in 1940. However, for the rest of the century, no

adjustments were made to reflect the dramatic increases in life expectancy.

The result of this long period of inactivity has been that the cost of paying for state

pensions has risen sharply. Although the 1995 Pension Act paved the way for equality in

SPA between men and women, equality was not due to be achieved until 2020, and still

only at age 65. Since that Act was passed, there has been a growing recognition of the

need to move faster in order to constrain the rapidly rising cost of state pensions. Key

landmarks included:

• The Turner Commission, which first recommended moving gradually to 66, then 67,

and then 68, with a timetable enshrined in the 2007 Pensions Act;

• A move to 65 and 66 sooner, set out in the 2011 Pensions Act;

• A move to 67 sooner, set out in the 2014 Pensions Act.

Following the controversy over these pension age increases and the way they were (or

were not effectively) communicated, the 2014 Act also provided for periodic independent

reviews of the SPA. Two such reviews have now taken place, and the third has recently

been commissioned. This paper aims to feed into that third review.

Key findings

Our key findings are:

• The failure to increase SPA during the entire 20th century means that we are now in

a period of “catch-up”; typical retirees have been able to enjoy an increasing

proportion of adult life in receipt of a State Pension, to an extent that is now widely

seen as unsustainable.

• In our view, we should therefore not be “locking in” these historically long retirements

but should gradually move to a more affordable system.

• Whilst this could still be based on a set (lower) percentage of adult life spent on

retirement, we are attracted to the idea of a fixed expected number of years in

retirement as the basis for setting SPA in future. Based on cohort life expectancy, a

figure of 20 years would broadly match current outturns but – crucially – would mean

that any future improvements in life expectancy would be converted entirely into an

extension of “working life”. A constant figure of 20 years might also assist in the

communication of the need for future SPA changes.

4.

4

• To mitigatethe impacts of a faster schedule of SPA increases than is currently

envisaged, we think the Government could borrow from the insurance sector the idea

of a minimum guaranteed payout of state pension (akin to the guarantee periods on

annuities).

One idea would be that those who reach SPA would be guaranteed a minimum of (say)

five years of payments, with their heirs receiving the payments if they die within five years.

This approach could simultaneously facilitate a fiscally responsible schedule of increases in

SPA whilst providing a concrete mitigation for those who would otherwise be most

adversely affected.

The final section of the paper discusses other considerations, including highlighting the

subjectivity inherent in the use of “cohort life expectancy” to set SPA for future retirees. We

also discuss whether allowing “early access” to the state pension in certain situations

would help to mitigate the impact of increased SPA. We conclude, for a number of reasons,

that such an approach would raise serious issues of affordability and practicality and

should not be pursued.

5.

5

Introduction

What can weexpect from the State Pension Age review

Changes to State Pension Age (SPA) have been a contentious issue in the UK in recent

years.

For women, SPA rose by six years between 2010 and 2020, from 60 to 66, and for men it

rose by one year from 65 to 66, with the change starting in 2018. An increase to 67 (for

both men and women) is scheduled to take place during this Parliament, and a move to 68

is on the Statute Book for the 2040s.

One point of contention about these changes has been the extent to which they were – or

were not – effectively communicated to those most affected. In particular, the Women

Against State Pension Inequality (WASPI) campaign was formed and, along with other

campaign groups, has been active in raising concerns. The Parliamentary Ombudsman

concluded that there had been maladministration in the way that the Department for Work

& Pensions (DWP) failed to communicate effectively during the first decade of this century.

There remains an impasse over whether compensation should be paid in light of that

finding.

Against this backdrop, measures were introduced in the 2014 Pensions Act to require a

systematic review of the SPA to be undertaken every six years, rather than the ad hoc

changes which had occurred previously. Such a review would consider the latest

information about life expectancies, as well as other relevant factors. A policy was also

adopted, that in the future, people would be given a minimum of ten years’ notice of

changes to their SPA.

Since that Act was passed, the first two independent reviews have been undertaken, but

neither led to legislative change. However, in July 2025, the Government announced that a

third independent review was being set up; it is widely expected that this will be followed by

legislation to provide for a new schedule of SPA increases.

The purpose of this paper is to assess what may come out of that review, particularly in

light of the latest data on life expectancy, and to offer some thoughts on alternative

approaches.

The paper begins with a brief description of the evolution of policy on SPA, including:

• the 1995 Pensions Act, which provided for equalising of SPA between men and

women;

• the 2007 Pensions Act, which first provided a timetable for going beyond age 65; and

• the 2011 and 2014 Acts, which further accelerated the schedule of increases.

6.

6

We then lookat the reviews which have been published so far, summarising their

conclusions and describing how the principles underlying the choice of SPA have evolved.

Next, we take advantage of the latest data on life expectancy, informed for the first time by

the results of the 2021 census, to see what kinds of SPA schedule we might face in future.

This includes considering whether a statutory timetable for going beyond age 68 is likely.

In the final two sections, we offer some thoughts on whether the current approach to

setting SPA makes sense, and what changes could be made.

7.

7

01 The changinglegislation around State

Pension Ages

a) The early years of the UK State Pension

When it was created by the Old Age Pensions Act of 1908, the UK State Pension was only

available to those aged 70 or over and was payable on a means-tested basis. It was viewed

as a form of poverty relief, initially only for those “of good character,” who had the good

fortune, or perhaps misfortune, to live well beyond their expected lifespan1.

The age of eligibility for the State Pension was reduced from 70 to 65 under the 1925

National Insurance Act, which also reformed the basis of eligibility. SPA for men was to

remain at 65 for nearly a century. But SPA for women was reduced to 60 in 1940, partly

reflecting assumptions about the different lives of men and women. Remarkably, this

differential remained in force until 2010.

Life expectancies for both men and women improved dramatically over the 20th century.

The life expectancy of young adults entering the workforce increased by 17 years between

1900 and 20002. Despite this transformational increase in life expectancy, the first major

review of SPAs did not take place until the early 1990s, with a Green Paper published in

1991, a White Paper in 1993, and legislation in the form of the Pensions Act of 19953.

b) The Pensions Act 1995

The key change brought about by the Pensions Act 1995 was a timetable for equalising

SPAs between men and women on a phased basis between 2010 and 2020. Under the

timetable set out in the Act, women’s SPA would rise from 60 to 61 by April 2012, to 62 by

April 2014 and so on until it reached 65 by April 2020.

A notable feature of the 1995 Act was the long notice period before any changes were

made. Because of the fifteen-year lead time, no woman aged 45 or over when the Act

became law would see any change at all to her SPA.

Unfortunately, one of the consequences of the long lead time – and of the fact that most of

those affected by these changes to their pension age were relatively young when the

legislation was passed – meant that awareness of the changes was limited.

1 See: https://commonslibrary.parliament.uk/research-briefings/sn04817/ for a description of the early evolution of state

pensions in the UK

2 Human Mortality Database; Life expectancy at age 20 in England & Wales increased from age 62 to age 79

3 Pensions Act 1995

8.

8

In the early2000s, DWP undertook research to assess awareness of these changes and

found that it was patchy, with many women not knowing the specifics of the changes, and

some women – particularly those on lower incomes – being completely unaware that SPAs

were changing at all. It was the failure of the DWP to act promptly on this research, which

was the basis for the Parliamentary Ombudsman’s finding of maladministration in its 2024

report4.

c) The Turner Commission

The Labour government elected in 1997 decided that a comprehensive review of the

pension system was needed, with a particular focus on the low level of private pension

provision in the workforce. An independent Commission was set up, headed by industrialist

Adair (now Lord) Turner, trade unionist Jeannie (now Baroness) Drake and the (late)

academic Professor John Hills.

As well as making recommendations which led to the introduction of automatic enrolment

into workplace pensions, the Commission also recommended that SPAs needed to rise.

Their report provided the justification for increases in SPA beyond 65, and these were

included in the Pensions Act 2007.

d) The Pensions Act 2007

The Pensions Act 2007 made no changes to the timetable for equalising the SPAs between

men and women but did set out a timetable for SPAs to rise beyond 65. Under the

provisions of the Act, SPA would rise (for both men and women):

• to 66 by April 2026;

• to 67 by April 2036; and

• to 68 by April 2046.

In each case, the transition would be made gradually over the preceding two years. Thus,

for example, SPA would start rising above 67 in April 2044 and would gradually reach 68

two years later. This remains the legislative timetable for the move to 68.

e) The Pensions Act 2011

When the Coalition Government was elected in 2010, it became clear that the established

timetable for SPA increases had not – and would not – keep pace with the dramatic

increases in life expectancy seen over the previous century. For example, male SPA would

have remained unchanged at 65 from 1925 to 2024 – a period of nearly a century in which

the length of time a man could expect to live beyond SPA had soared.

4 https://www.ombudsman.org.uk/sites/default/files/Women%E2%80%99s-State-Pension-age-our-findings-on-injustice-

and-associated-issues.pdf

9.

9

In order toincrease SPAs for both men and women, the Government legislated in the

Pensions Act 20115 to bring forward the date for equality in male and female SPAs from

April 2020 to October 2018, and to bring forward the date for reaching an SPA of 66 from

April 2026 to April 2020.

The Parliamentary Ombudsman reports6 that the Coalition Government issued more than

five million letters to women affected by this Act between January 2012 and November

2013. For some women, these letters were the first which alerted them, not only to the more

modest changes brought about by the 2011 Act, but also to the much larger changes under

the 1995 Act.

f) The Pensions Act 20147

The 2011 Act brought forward the date for equality at 65 and the date for an SPA of 66 but

made no further changes. This meant that a move to 67 remained on the unchanged

timetable of 2036, fully sixteen years after the move to 66. This would have meant SPA rises

falling behind expected improvements in life expectancy over that period.

In response, the 2014 Act brought forward the timetable for moving the SPA to 67 by eight

years, meaning that SPA for men and women will reach 67 in April 2028, during the lifetime

of this Parliament.

However, previous controversies over SPA increases made their mark on the 2014 Act.

Rather than the ad hoc increases which had been a feature of recent policy, the Act

provided that there should be a systematic review of SPAs at least once every six years.

The first report relating to these changes was to be published by May 2017.

The legislation also required the Government Actuary to provide estimates of the proportion

of adult life people would spend in retirement based on different SPAs. Although the

legislation was not specific, discussion around the time of the passage of the Act suggested

that the Government had in mind a target of people spending “up to one third” of their adult

life8 above pension age.

The Government also stated that its policy (though not referenced in the legislation) was that

in future people should have a minimum of ten years’ notice of changes in their SPA.

In the next section we look at the two reviews which have been published since the passage

of this Act.

5 Pensions Act 2011

6 Annex A, p93

7 Pensions Act 2014

8 For these purposes, “adult life” has been defined as starting from age twenty.

10.

10

02 Independent Reviewsof State Pension Age

conducted to date

The two reviews which have been published so far were those led by John Cridland and

published in 20179, and by Baroness Lucy Neville-Rolfe, published in 202310.

We consider each review in turn.

a) The Cridland Review

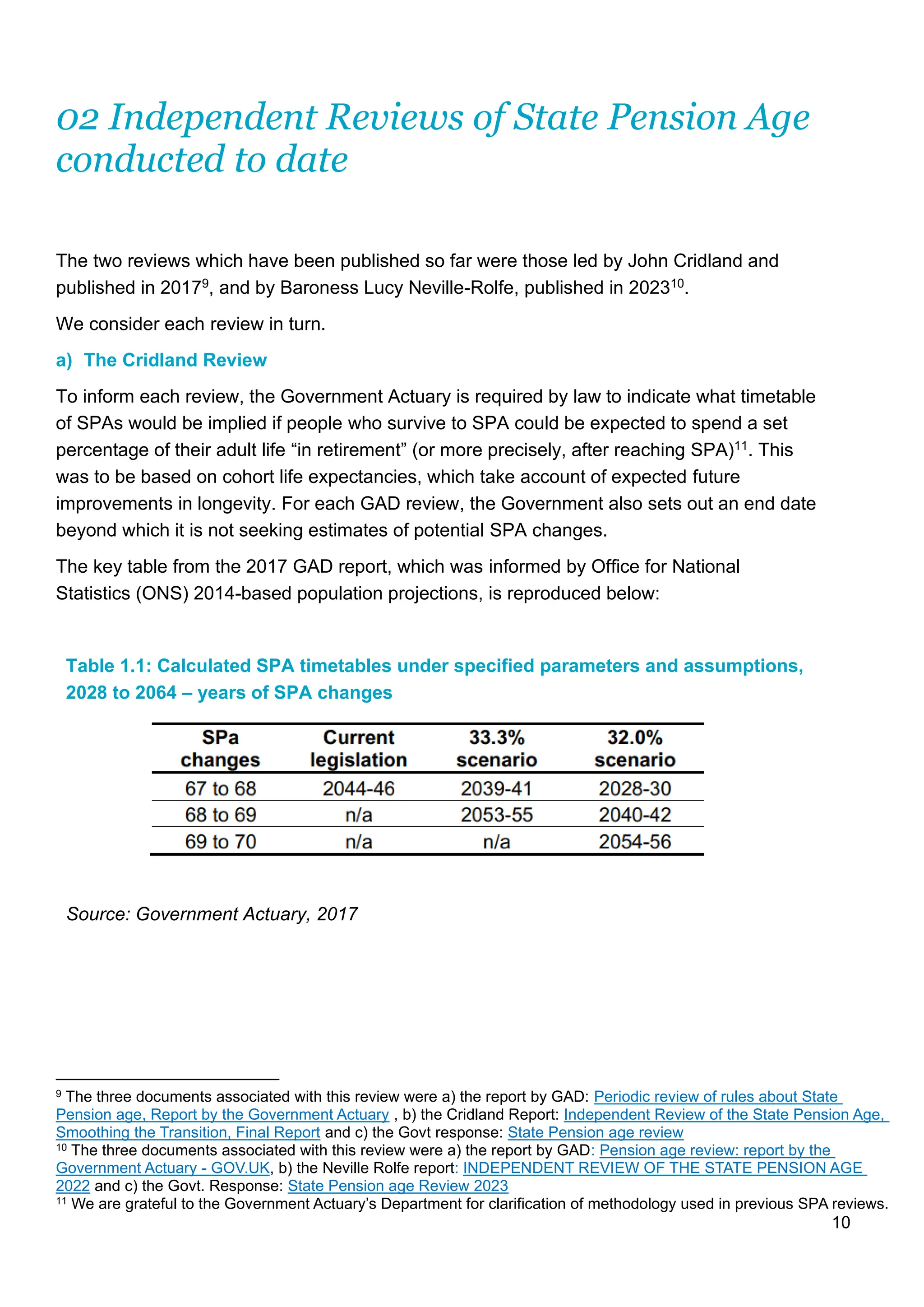

To inform each review, the Government Actuary is required by law to indicate what timetable

of SPAs would be implied if people who survive to SPA could be expected to spend a set

percentage of their adult life “in retirement” (or more precisely, after reaching SPA)11. This

was to be based on cohort life expectancies, which take account of expected future

improvements in longevity. For each GAD review, the Government also sets out an end date

beyond which it is not seeking estimates of potential SPA changes.

The key table from the 2017 GAD report, which was informed by Office for National

Statistics (ONS) 2014-based population projections, is reproduced below:

Table 1.1: Calculated SPA timetables under specified parameters and assumptions,

2028 to 2064 – years of SPA changes

Source: Government Actuary, 2017

9 The three documents associated with this review were a) the report by GAD: Periodic review of rules about State

Pension age, Report by the Government Actuary , b) the Cridland Report: Independent Review of the State Pension Age,

Smoothing the Transition, Final Report and c) the Govt response: State Pension age review

10 The three documents associated with this review were a) the report by GAD: Pension age review: report by the

Government Actuary - GOV.UK, b) the Neville Rolfe report: INDEPENDENT REVIEW OF THE STATE PENSION AGE

2022 and c) the Govt. Response: State Pension age Review 2023

11 We are grateful to the Government Actuary’s Department for clarification of methodology used in previous SPA reviews.

11.

11

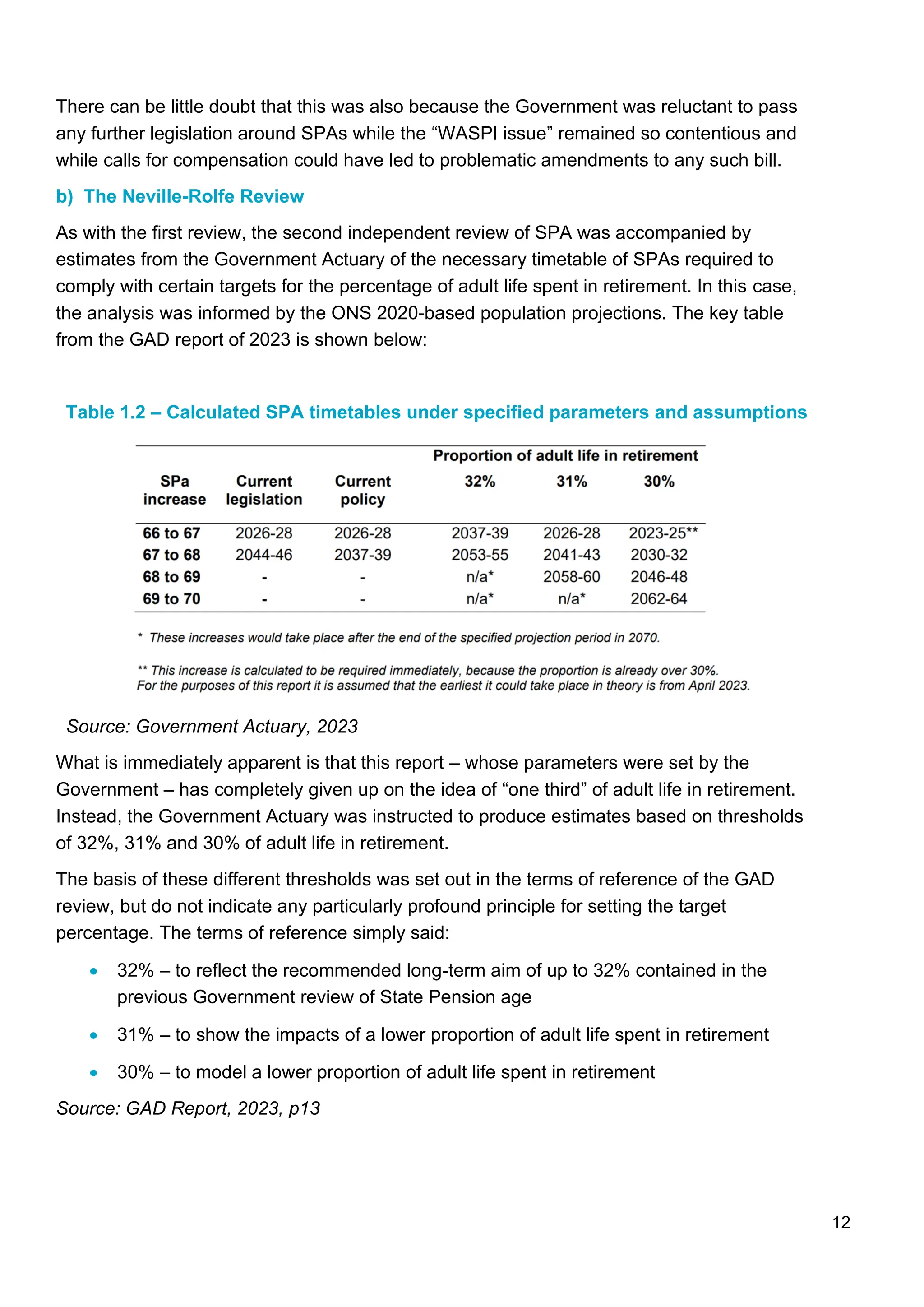

In his report,the Government Actuary said that he had been “instructed” to undertake

analysis on the basis of 33.3% of adult life in retirement (the “up to one third” principle) but

also 32.0%. The justification given by the DWP for asking for this additional set of figures

was that:

“…this broadly reflects the average proportion of their adult life people reaching age 65

(current male Spa) in the last 20 years were expected to spend above this.”12

It is noteworthy that even as soon as the first SPA review, the Government was giving

consideration to moving to a more aggressive timetable of SPA increases, than would be

implied by the “up to a third” principle advanced when the legislation was first passed.

The key points about the timetable set out in Table 1.1 are:

• The move from 67 to 68 would be brought forward by five years under the “up to a

third” scenario but by sixteen years under the “32% rule”; indeed, in principle, this

latter rule would imply that no sooner had SPA reached 67 in 2028 that it would be

increased again over the next two years to 68; and

• The 33.3% scenario would imply a date for reaching 69 (for the first time) whilst the

32.0% scenario would lead to a schedule including both 69 and 70.

The independent reviewer was to have regard to this information but also to consider “other

relevant factors” when reaching his recommendations. In his report, John Cridland rejected

the timetable implied by the 32% rule, as this would, as noted above, have led to “back-to-

back” pension age increases.

Instead, he recommended a move to 68 between 2037 and 2039, slightly faster than the

timetable implied by the GAD 33.3% scenario. This was justified on the basis that these

estimates are themselves highly volatile, and that the previous population estimates (for

2012) would have implied a much more aggressive schedule than set out the Table above.

John Cridland chose his timetable as something of a “midpoint” between the implications of

the 2012-based estimates and the 2014-based estimates.

The Government of the day accepted this recommended timetable, and this remains the last

statement of government policy on this issue.

However, it declined to legislate to put this new timetable into effect. In part this was

because it argued (reasonably) that further population estimates would become available

before it was necessary to legislate whilst still being able to adhere to the principle of 10

years notice.

12 Source: GAD report, 2017, p9.

12.

12

There can belittle doubt that this was also because the Government was reluctant to pass

any further legislation around SPAs while the “WASPI issue” remained so contentious and

while calls for compensation could have led to problematic amendments to any such bill.

b) The Neville-Rolfe Review

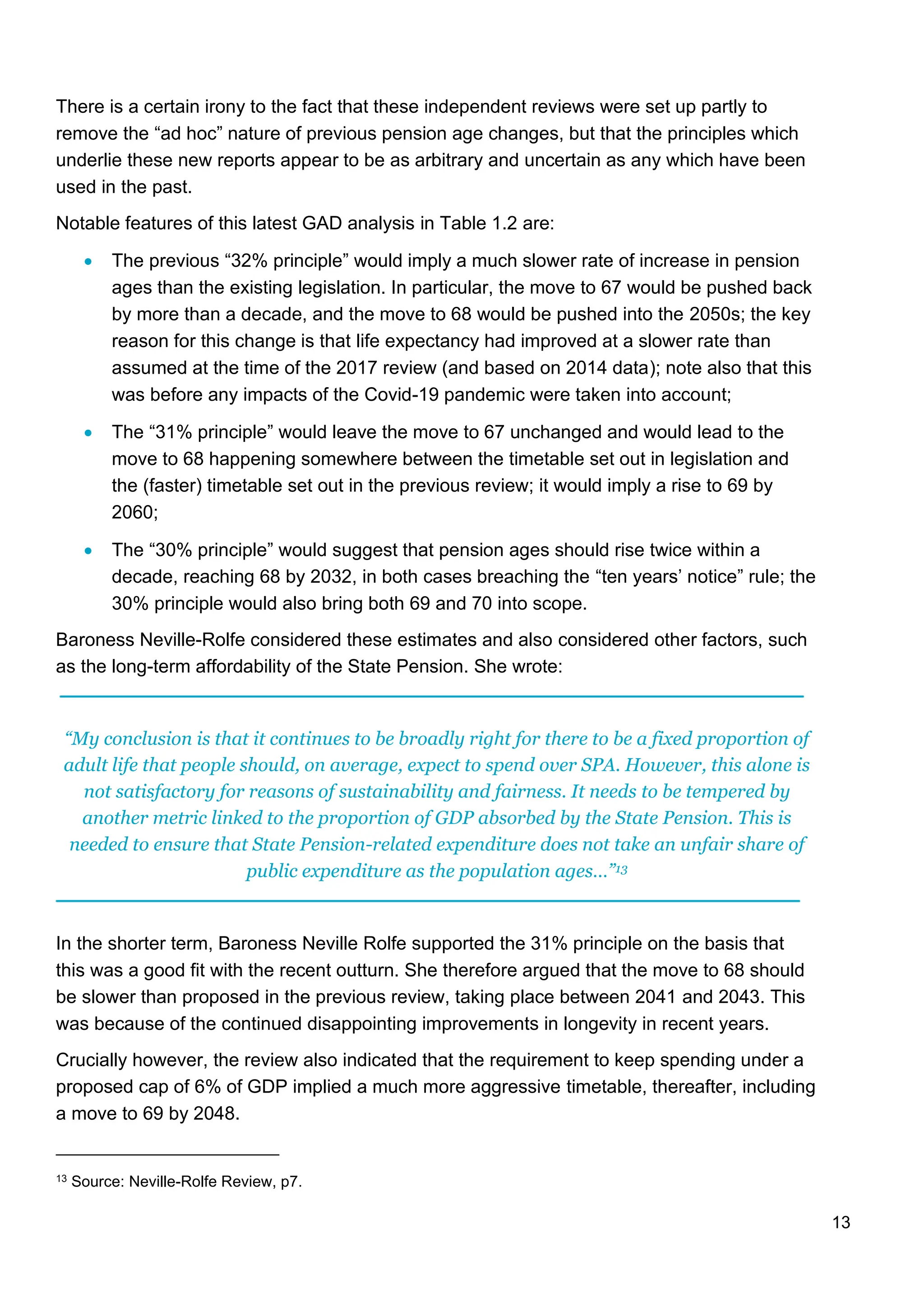

As with the first review, the second independent review of SPA was accompanied by

estimates from the Government Actuary of the necessary timetable of SPAs required to

comply with certain targets for the percentage of adult life spent in retirement. In this case,

the analysis was informed by the ONS 2020-based population projections. The key table

from the GAD report of 2023 is shown below:

Table 1.2 – Calculated SPA timetables under specified parameters and assumptions

Source: Government Actuary, 2023

What is immediately apparent is that this report – whose parameters were set by the

Government – has completely given up on the idea of “one third” of adult life in retirement.

Instead, the Government Actuary was instructed to produce estimates based on thresholds

of 32%, 31% and 30% of adult life in retirement.

The basis of these different thresholds was set out in the terms of reference of the GAD

review, but do not indicate any particularly profound principle for setting the target

percentage. The terms of reference simply said:

• 32% – to reflect the recommended long-term aim of up to 32% contained in the

previous Government review of State Pension age

• 31% – to show the impacts of a lower proportion of adult life spent in retirement

• 30% – to model a lower proportion of adult life spent in retirement

Source: GAD Report, 2023, p13

13.

13

There is acertain irony to the fact that these independent reviews were set up partly to

remove the “ad hoc” nature of previous pension age changes, but that the principles which

underlie these new reports appear to be as arbitrary and uncertain as any which have been

used in the past.

Notable features of this latest GAD analysis in Table 1.2 are:

• The previous “32% principle” would imply a much slower rate of increase in pension

ages than the existing legislation. In particular, the move to 67 would be pushed back

by more than a decade, and the move to 68 would be pushed into the 2050s; the key

reason for this change is that life expectancy had improved at a slower rate than

assumed at the time of the 2017 review (and based on 2014 data); note also that this

was before any impacts of the Covid-19 pandemic were taken into account;

• The “31% principle” would leave the move to 67 unchanged and would lead to the

move to 68 happening somewhere between the timetable set out in legislation and

the (faster) timetable set out in the previous review; it would imply a rise to 69 by

2060;

• The “30% principle” would suggest that pension ages should rise twice within a

decade, reaching 68 by 2032, in both cases breaching the “ten years’ notice” rule; the

30% principle would also bring both 69 and 70 into scope.

Baroness Neville-Rolfe considered these estimates and also considered other factors, such

as the long-term affordability of the State Pension. She wrote:

“My conclusion is that it continues to be broadly right for there to be a fixed proportion of

adult life that people should, on average, expect to spend over SPA. However, this alone is

not satisfactory for reasons of sustainability and fairness. It needs to be tempered by

another metric linked to the proportion of GDP absorbed by the State Pension. This is

needed to ensure that State Pension-related expenditure does not take an unfair share of

public expenditure as the population ages…”13

In the shorter term, Baroness Neville Rolfe supported the 31% principle on the basis that

this was a good fit with the recent outturn. She therefore argued that the move to 68 should

be slower than proposed in the previous review, taking place between 2041 and 2043. This

was because of the continued disappointing improvements in longevity in recent years.

Crucially however, the review also indicated that the requirement to keep spending under a

proposed cap of 6% of GDP implied a much more aggressive timetable, thereafter, including

a move to 69 by 2048.

13 Source: Neville-Rolfe Review, p7.

14.

14

In response, theGovernment of the day pointed out that the recent experience of the Covid-

19 pandemic meant that life expectancy projections were especially uncertain and that it

would therefore be inappropriate to make firm commitments to any particular revisions to the

SPA timetable. It would be fair to say that announcing potentially contentious changes to

State Pension ages the year before a General Election would also have been challenging!

It did however say that a new review should be undertaken in the first two years of the next

Government, and this forms the basis for the new Government’s decision to launch a third

review starting in 2025.

In the next section we consider the evidence base which will inform this next review.

15.

15

03 The thirdState Pension age review

a) Terms of reference of the third independent review and of the GAD report

In July 2025, the Labour government announced the establishment of a third independent

review of SPA, led by Dr Suzy Morrissey, Deputy Director of the Pensions Policy Institute.

Key features of the terms of reference of the new review were that it should consider14:

• the merits of linking SPA to life expectancy, including on fairness between

generations;

• the role of SPA in managing the long-term sustainability of the State Pension;

• the international experience of automatic adjustment mechanisms (AAM) for making

decisions about State Pension age.

Notably, the reviewer was told that she should “...assume that current policies regarding the

entitlement and value of State Pension remain unchanged over the long-term.” In particular

(though not explicitly stated), the reviewer was therefore being told to assume that the

relatively generous “triple lock” uprating of the State Pension would continue indefinitely,

something which most commentators think is highly unlikely.

There is a good case for considering both SPA and the generosity of the State Pension

together, as there are clear trade-offs between the two.

For example, the Institute for Fiscal Studies has recently argued15 that if the cost of the

“triple lock” leads to a more aggressive schedule of increases in State Pension ages then

this will be to the detriment of people in more deprived areas compared with a less generous

State Pension but one which is paid sooner. It is frustrating that such holistic considerations

are deemed “out of scope” for this review.

Alongside this, a separate term of reference document has been published16 for the

Government Actuary’s review. Notably, GAD is asked again to look at the figures on the

basis of 32%, 31% and 30% of adult life spent in retirement, with the following stated

justifications:

• 32% – as recommended in the 2017 Government review of State Pension age;

• 31% – outlined in the 2022 Independent Report;

• 30% – to reflect that historical rates have varied between 30% to 31% in recent years.

14 Source: https://www.gov.uk/government/publications/third-review-of-state-pension-age-independent-report-terms-of-

reference/third-review-of-state-pension-age-independent-report-terms-of-reference

15 https://ifs.org.uk/publications/pensions-review-final-recommendations

16 https://www.gov.uk/government/publications/third-review-of-state-pension-age-government-actuarys-report-terms-of-

reference/report-by-the-government-actuary-terms-of-reference

16.

16

The Government Actuaryis also asked to look at the sensitivity of these estimates, as GAD

has previously pointed out that small changes in life expectancy assumptions can lead to

very substantial swings in the dates at which different State Pension ages should be

reached.

b) What might GAD find?

The terms of reference of the GAD review say that it should be based on the ONS 2022-

based population projections, which were published in February 2025. Since this information

is already in the public domain, we have been able to produce our own estimates of the

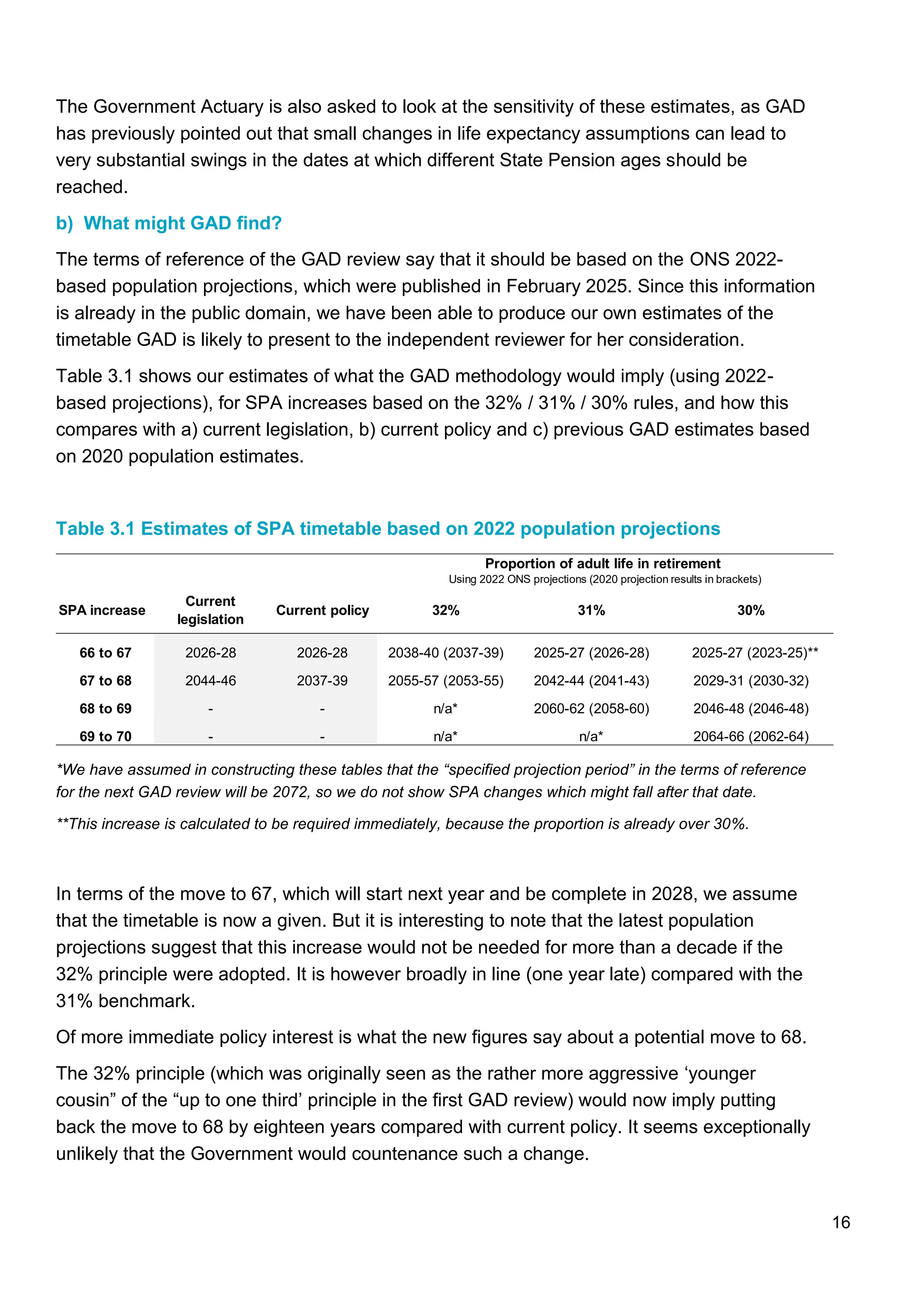

timetable GAD is likely to present to the independent reviewer for her consideration.

Table 3.1 shows our estimates of what the GAD methodology would imply (using 2022-

based projections), for SPA increases based on the 32% / 31% / 30% rules, and how this

compares with a) current legislation, b) current policy and c) previous GAD estimates based

on 2020 population estimates.

Table 3.1 Estimates of SPA timetable based on 2022 population projections

*We have assumed in constructing these tables that the “specified projection period” in the terms of reference

for the next GAD review will be 2072, so we do not show SPA changes which might fall after that date.

**This increase is calculated to be required immediately, because the proportion is already over 30%.

In terms of the move to 67, which will start next year and be complete in 2028, we assume

that the timetable is now a given. But it is interesting to note that the latest population

projections suggest that this increase would not be needed for more than a decade if the

32% principle were adopted. It is however broadly in line (one year late) compared with the

31% benchmark.

Of more immediate policy interest is what the new figures say about a potential move to 68.

The 32% principle (which was originally seen as the rather more aggressive ‘younger

cousin” of the “up to one third’ principle in the first GAD review) would now imply putting

back the move to 68 by eighteen years compared with current policy. It seems exceptionally

unlikely that the Government would countenance such a change.

SPA increase

Current

legislation

Current policy 32% 31% 30%

66 to 67 2026-28 2026-28 2038-40 (2037-39) 2025-27 (2026-28) 2025-27 (2023-25)**

67 to 68 2044-46 2037-39 2055-57 (2053-55) 2042-44 (2041-43) 2029-31 (2030-32)

68 to 69 - - n/a* 2060-62 (2058-60) 2046-48 (2046-48)

69 to 70 - - n/a* n/a* 2064-66 (2062-64)

Proportion of adult life in retirement

Using 2022 ONS projections (2020 projection results in brackets)

17.

17

The 31% principleimplies a timetable for the move to 68 somewhere between government

policy and current legislation, whereas a 30% rule would imply such a rapid move to 68 as to

breach the policy of giving ten years’ notice of changes.

Beyond this, both the 31% principle and the 30% principle imply a timetable for a move to

69, whilst the 30% principle would also mean an SPA of 70 for someone in their twenties

today.

Of course, as we have seen before, the independent reviewer is not bound by any of the

GAD timetables and may see it as part of their role to divert from strict adherence to

formulas on the basis of the ‘wider considerations’ that they are invited to take into account.

Indeed, the terms of reference of the latest review would allow the reviewer to conclude that,

based on UK and international experience, a formulaic approach of this sort is

unsatisfactory. And the Government is then entirely free to disregard both the GAD

timetables and the independent review recommendations in finalising its own policy.

18.

18

04 Proposals

In thissection we introduce proposals which could impact the timetable emerging from the

next review, or which might enable the timetable to be accelerated whilst at the same time

supporting those with shorter life expectancy. In the final section we will then discuss other

considerations, which do not necessarily imply a change to the timetable.

a) Proposal 1 – Challenge the premise of maintaining the recent proportion

The premise of previous reviews has effectively been that the proportion of adult life spent in

retirement for recent retirees is about right. Reviews have therefore sought to determine

SPA on the basis of keeping this proportion broadly constant.

It is understandable that this approach has been taken given a desire to try to achieve a

measure of intergenerational fairness, and to do so by ‘levelling up” (as opposed to “levelling

down’).

However, Baroness Neville-Rolfe also noted the need to ensure that the State Pension is

sustainable and affordable for future generations on taxpayers, introducing a secondary

constraint based on the share of GDP. In reality it would be this constraint, rather than the

share of adult life spent in retirement, which would drive SPA increases, were her

recommendations implemented.

Fiscal constraints are particularly limiting in light of the ageing population and increasing

numbers of people reaching SPA relative to the size of the working population. This means

that funding the State Pension (alongside other spending pressures from an ageing

population) becomes increasingly challenging even if the proportion of adult life spent in

retirement stops increasing.

A more candid approach would therefore be to accept that recent retirees are something of

a historical anomaly, enjoying longer retirements than any generation that came before

them, as SPA increases began much too late relative to increases in life expectancy. This

approach would start from the premise that SPA is currently too low, designing a timetable

of increases to get to a more sustainable starting point, and potentially implementing a

formulaic link thereafter.

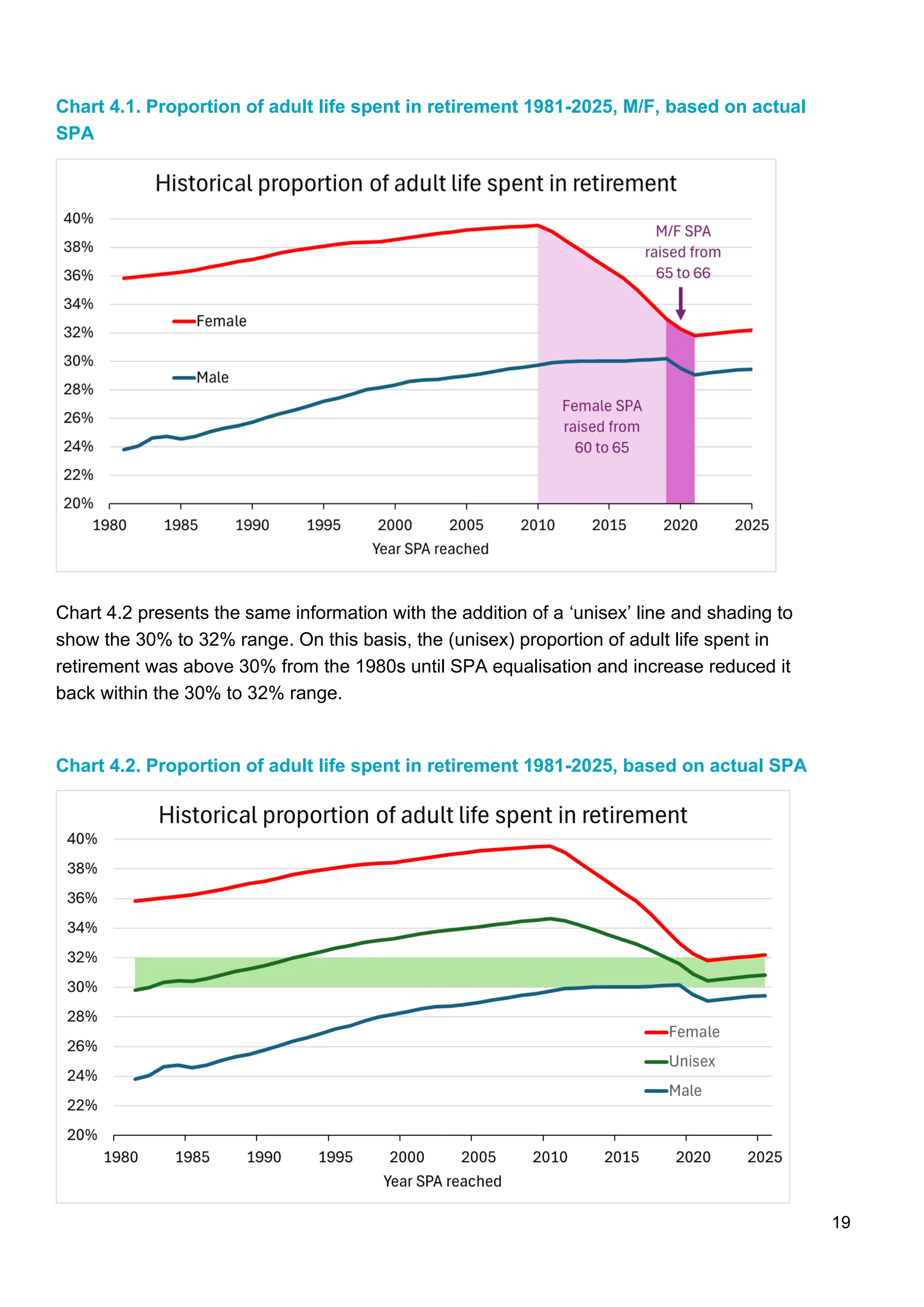

Chart 4.1 shows the historical proportion of adult life spent in retirement for males and for

females, based on actual historical SPA. This shows a significant difference between the

sexes, with women enjoying longer life expectancy and a historically lower SPA, and also

between the generations, with the proportion increasing over time for both men and for

women, except during the period when SPA was equalised and then increased.

19.

19

Chart 4.1. Proportionof adult life spent in retirement 1981-2025, M/F, based on actual

SPA

Chart 4.2 presents the same information with the addition of a ‘unisex’ line and shading to

show the 30% to 32% range. On this basis, the (unisex) proportion of adult life spent in

retirement was above 30% from the 1980s until SPA equalisation and increase reduced it

back within the 30% to 32% range.

Chart 4.2. Proportion of adult life spent in retirement 1981-2025, based on actual SPA

20.

20

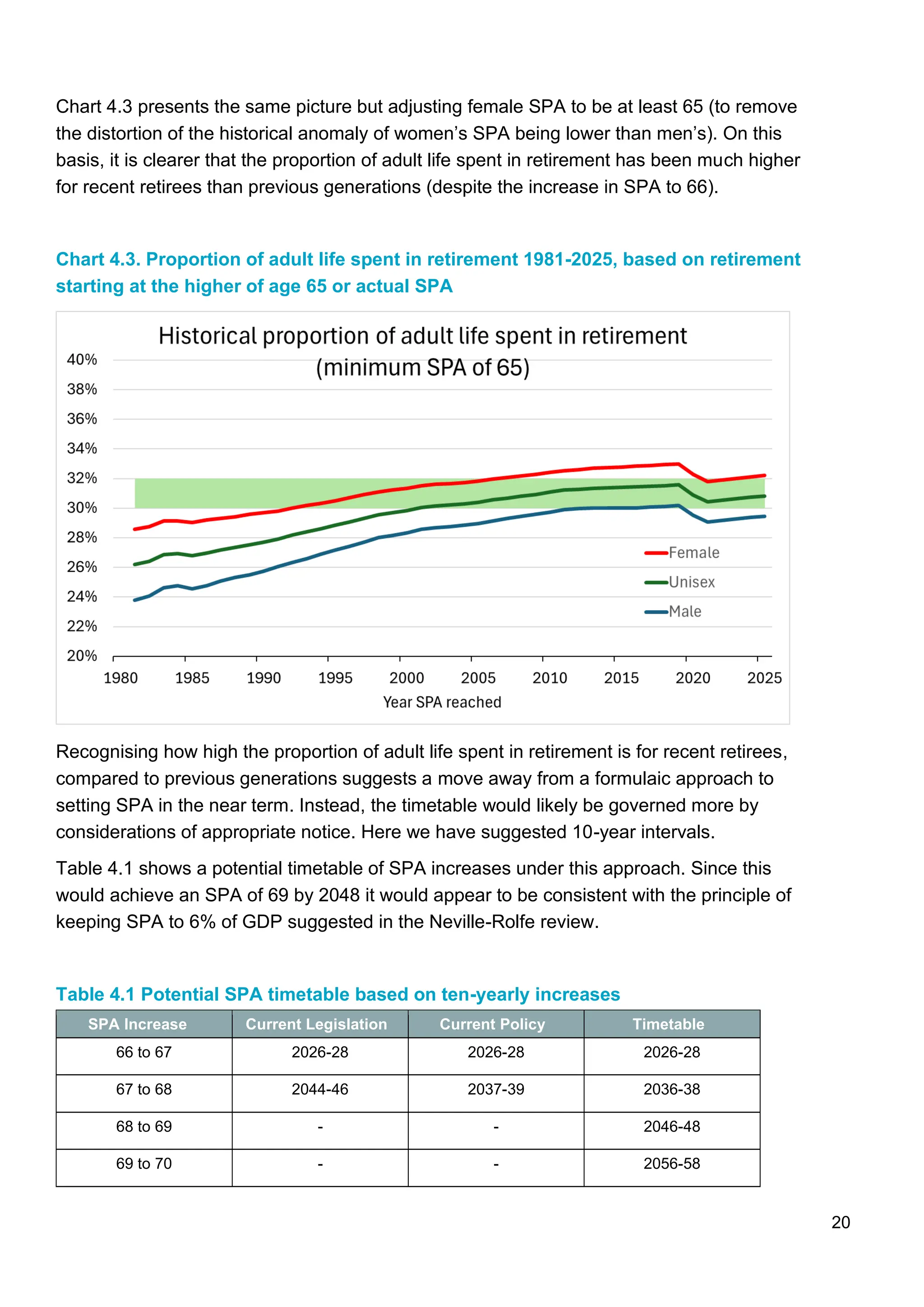

Chart 4.3 presentsthe same picture but adjusting female SPA to be at least 65 (to remove

the distortion of the historical anomaly of women’s SPA being lower than men’s). On this

basis, it is clearer that the proportion of adult life spent in retirement has been much higher

for recent retirees than previous generations (despite the increase in SPA to 66).

Chart 4.3. Proportion of adult life spent in retirement 1981-2025, based on retirement

starting at the higher of age 65 or actual SPA

Recognising how high the proportion of adult life spent in retirement is for recent retirees,

compared to previous generations suggests a move away from a formulaic approach to

setting SPA in the near term. Instead, the timetable would likely be governed more by

considerations of appropriate notice. Here we have suggested 10-year intervals.

Table 4.1 shows a potential timetable of SPA increases under this approach. Since this

would achieve an SPA of 69 by 2048 it would appear to be consistent with the principle of

keeping SPA to 6% of GDP suggested in the Neville-Rolfe review.

Table 4.1 Potential SPA timetable based on ten-yearly increases

SPA Increase Current Legislation Current Policy Timetable

66 to 67 2026-28 2026-28 2026-28

67 to 68 2044-46 2037-39 2036-38

68 to 69 - - 2046-48

69 to 70 - - 2056-58

21.

21

A formulaic approachmight then be considered in the more distant future if it becomes

necessary to increase SPA beyond age 70.

Using the current formulaic approach and 2022-based population projection would imply a

proportion of adult life in retirement between 29% and 30%.

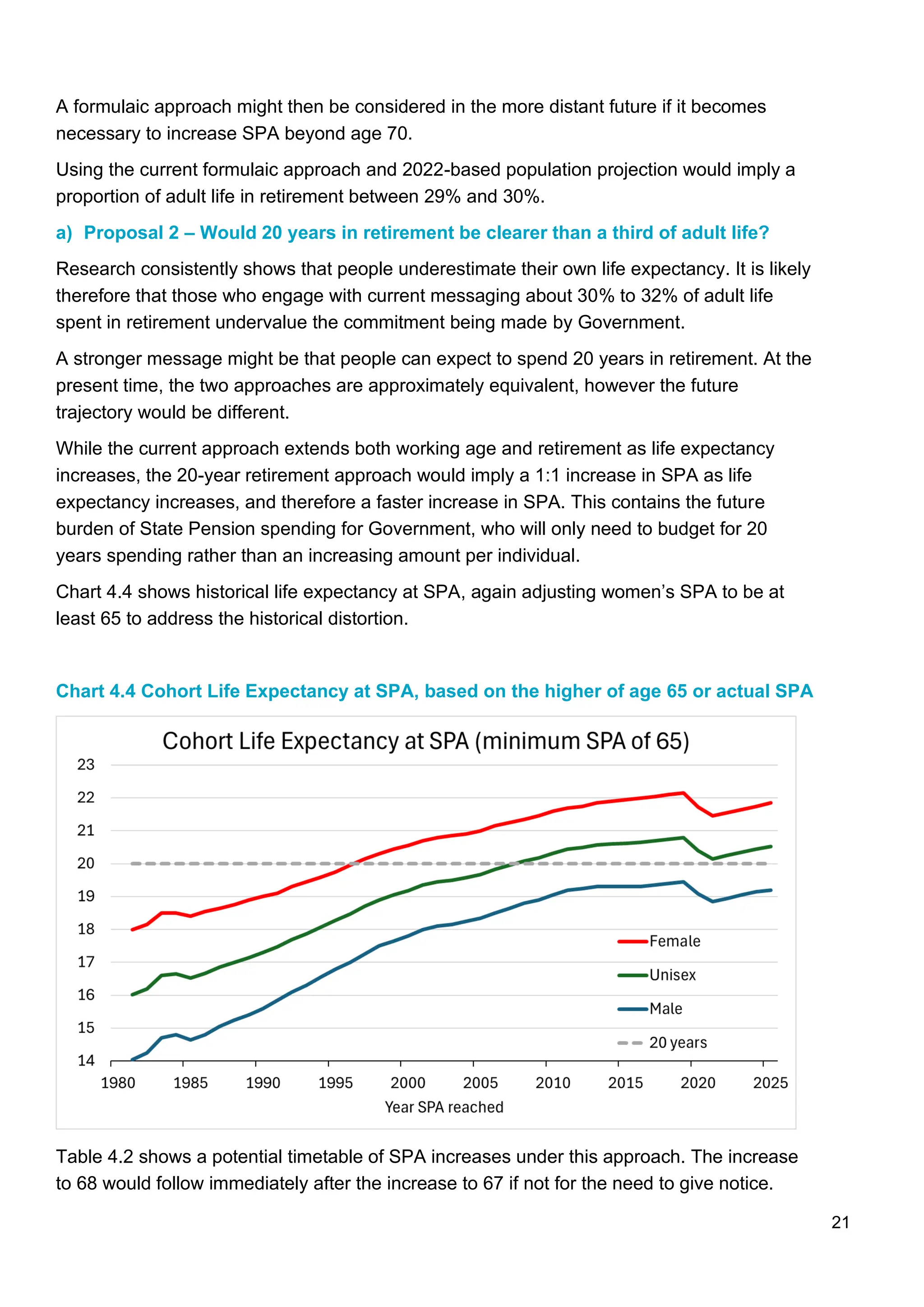

a) Proposal 2 – Would 20 years in retirement be clearer than a third of adult life?

Research consistently shows that people underestimate their own life expectancy. It is likely

therefore that those who engage with current messaging about 30% to 32% of adult life

spent in retirement undervalue the commitment being made by Government.

A stronger message might be that people can expect to spend 20 years in retirement. At the

present time, the two approaches are approximately equivalent, however the future

trajectory would be different.

While the current approach extends both working age and retirement as life expectancy

increases, the 20-year retirement approach would imply a 1:1 increase in SPA as life

expectancy increases, and therefore a faster increase in SPA. This contains the future

burden of State Pension spending for Government, who will only need to budget for 20

years spending rather than an increasing amount per individual.

Chart 4.4 shows historical life expectancy at SPA, again adjusting women’s SPA to be at

least 65 to address the historical distortion.

Chart 4.4 Cohort Life Expectancy at SPA, based on the higher of age 65 or actual SPA

Table 4.2 shows a potential timetable of SPA increases under this approach. The increase

to 68 would follow immediately after the increase to 67 if not for the need to give notice.

22.

22

Table 4.2 Potentialtimetable for SPA rises targeting 20-year retirement, ignoring the

need for notice periods

SPA Increase Current Legislation Current Policy Timetable

66 to 67 2026-28 2026-28 2026-28

67 to 68 2044-46 2037-39 2027-29

68 to 69 - - 2039-41

69 to 70 - - 2050-52

While it is interesting to consider how much acceleration of the timetable might be justified

by this approach, in practice timing might be as per table 4.1 above.

b) Proposal 3 – Could the State Pension have a guarantee period?

With each increase in SPA, it becomes more likely that people in more deprived areas will

not reach SPA at all or will only draw their State Pension for a few years. This could

increase the sense of unfairness of SPA increases deemed necessary for fiscal reasons.

One change which might help to address this issue – and which mirrors the way that the

private sector typically provides annuities – would be to introduce the idea of a minimum

‘guarantee period’ of State Pension payment. For example, anyone starting to receive a

State Pension could be guaranteed five years’ worth of payments, with their estate receiving

the money if they die within five years.

To avoid a cliff-edge, something similar could potentially be offered as a lump sum death

benefit for those who die before pension age, perhaps subject to a minimum contribution

record.

Although adding a ‘guarantee period’ would increase the cost of the system at a time when

the pressure is to reduce it, it could accompany – and enable – a more aggressive schedule

of increases to SPA, improving the overall fiscal position but in a way less likely to be seen

as unfair.

The cost of guaranteeing a minimum of five years’ worth of payments to those who start to

receive the State Pension would be modest when compared to the savings from increasing

SPA, increasing costs by around 0.5%17.

The cost of also paying a lump sum death benefit for those dying before they reach SPA

would be larger, depending on the amount paid and the eligibility requirement.

17 LCP calculation

23.

23

05 Wider considerationsand alternative

approaches

In this final section, we offer some thoughts on whether the current approach to setting SPA

makes sense, and what changes could be made.

a) Is it reasonable to base SPA on very long-term subjective forecasts?

The current approach bases SPA increases on ‘cohort life expectancy.’ Cohort life

expectancy calculations aim to provide a realistic assessment of how long someone will live,

making them entirely appropriate when assessing the future cost of the State Pension.

However, they are necessarily subjective, requiring forecasts or projections of how death

rates will change over time.

It could be argued that it is unusual to base benefit entitlement for individuals on a subjective

assessment of what may or may not happen to death rates several decades in the future.

Importantly, forecasting cohort life expectancy requires projecting over an individual’s entire

remaining lifetime. For example, a forecast of the cohort life expectancy of someone

reaching retirement age in 2050 requires death rates extending out to the turn of the next

century, in 2100. Such long-term forecasts should be treated with caution! While mortality

assumptions for the next two decades is largely based on projecting past trends by age and

birth cohort, the very long-term rate of improvement in life expectancy is set by expert

judgement, typically based on longer term observed averages.

Even small changes in the assumed long-term rate of improvement can alter the timetable of

SPA increases. For instance, ONS reduced the assumed long-term rate of improvement

from 1.2% per annum to 1.1% per annum between the 2020-based and 2022-based

mortality projections. This is the main reason Table 3.1 above shows that the implied date

for SPA increases in the 2050s move back by two years. A shift of two years over a two-year

period illustrates the significant volatility of this method, as rightly highlighted by GAD.

An alternative approach would be to be acknowledge the limits of forecasting distant-future

mortality rates and instead base SPA on forecasts of ‘period life expectancy.’ Period life

expectancy is calculated based on death rates in a specific year. Forecasting remains

necessary to anticipate SPA rises and give notice. However, to forecast the period life

expectancy of someone reaching retirement age in 2050 only requires assumptions for

death rates up to 2050, rather than 2100. This significantly reduces the subjectivity and

aligns more closely with the time period over which these forecasts are typically used in

actuarial work.

The implications for the SPA increase timetable would depend upon the targeted proportion

of adult life spent in retirement. Since period life expectancies are lower than cohort life

expectancies, the target proportion would need to be adjusted downward.

24.

24

The main rationalefor this approach is not fiscal, but rather to reduce subjectivity and

dependence on assumptions about long-term mortality improvements.

b) Is it fair to disregard those who do not make it to SPA?

The current calculation only considers the proportion of adult life spent in retirement by

those who survive to SPA, disregarding the lives of those people who sadly die before

reaching SPA. This raises questions of fairness, particularly given decades of rising

inequalities, where most increases in life expectancy gains have accrued to those who

already lived longer, while poorer groups have seen less improvement. For example, the

most deprived 10% of women experienced a decline between 2011-13 and 2017-19

whereas less deprived women and men, saw life expectancy gains of around six months

over the same period18.

Under the current formulaic approach, if inequalities continue to widen, SPA could be

increasingly influenced by the experience of long-lived affluent groups, moving out of the

reach for deprived groups who die before SPA and whose experience is excluded from the

calculation.

A fairer approach would be to consider the proportion of adult life spent in retirement by

those who survive to adulthood, rather than to SPA. This ensures that the formula accounts

for all individuals reaching working age and contributing to funding the State Pension

through taxation.

The main reason to adopt this approach would be fairness, rather than fiscal, by considering

the experience of those who die before SPA.

c) Should State Pension age be tied to Healthy Life Expectancy?

A common expressed concern about SPA increases is that some people may be unable to

keep working up to an increased age, creating a gap between leaving work and their starting

pension, which they are dependent on modest means-tested benefits. This group on

average will be more likely to include people from more deprived areas and those who have

done more physically demanding work, and so raising SPA can be hardest for those who

are already more disadvantaged.

Current calculations consider how long people live but not their state of health. Many may

not reach SPA in good health; for example, health life expectancy (HLE) in England in 2021-

23 was just 62 years (for males and for females)19. HLE, as measured by ONS, relies on an

individual’s subjective personal assessment of their own health. Cultural and generational

differences in how such survey questions are answered can make as much difference to

responses, and the resulting HLE, as much as underlying state of health of respondents.

18 Health state life expectancies by national deprivation deciles, England: 2018 to 2020 - Office for National Statistics

19 Healthy life expectancy in England and Wales - Office for National Statistics

25.

25

The UK Governmentcould, in theory, collect objective HLE data, removing the subjectivity

issue. However, inequalities in HLE are substantial – twice as large as life expectancy (LE)

inequalities (19 years HLE difference vs 9 years LE difference between top and bottom

deciles). As currently measured by ONS, HLE is 52 for men and women in the most

deprived 10% of the country and below 65 for half of the country18. These inequalities would

arguably matter even more if HLE became the gateway for access to the State Pension (or

another benefit), as opposed to ‘only’ affecting the number of years for which it is paid.

In our view it is the current large inequalities in HLE, rather than the practical challenge of

obtaining an objective calculation, which would be the biggest challenge to any proposal to

tie SPA to HLE.

d) Should some people get early access?

One potential response to the challenge of health and life expectancy inequalities is to

remove the ‘cliff-edge’ for claiming the State Pension. Currently, there is a minimum age at

which State Pension can be claimed. It is possible to flex this upwards, taking an enhanced

State Pension at a later age. But there is no flexibility to take an earlier pension.

Given the relative generosity of post-retirement benefits compared with pre-retirement

benefits, the chance to take even a reduced State Pension early could improve people’s

standard of living in the gap between finishing work and reaching SPA.

If the right to take a (reduced) State Pension early was generally available, this could cost

the government money in the short-term. Assuming that the reduction in pension for early

access was actuarially fair, the government would in theory be indifferent between people

taking their pension early, late or at SPA. But in terms of cash flow, the policy would bring

forward State Pension expenditure which would be highly unwelcome to a government

already struggling with short-term fiscal pressures.

A targeted early-access approach could reduce the short-term hit on the public finances and

might benefit those most in need, but practical challenged remain:

• Postcode would be a reasonable proxy for deprivation, but it is hard to imagine a

State Pension system in which people living in some towns can get their pension

early but those in neighbouring towns cannot, with ‘cliff edge’ differences and a risk of

‘gaming’ the system; these same challenges are why we do not consider a locally

varying SPA in this paper;

• Those with limited other income to support themselves after they have stopped work

(such as private pensions) could be eligible to claim State Pension early; but this

would have the perverse effect that those who had made sacrifices to save could be

prevented from retiring early on a State Pension, whilst those who had made no

provision would be able to retire early; this disincentivises workplace pension

membership, especially for those with potentially modest entitlements;

26.

26

• Entitlement couldbe restricted to those in poor health and permanently unable to

work; whilst this might seem fair, such a dividing line is difficult to set out objectively;

for example, would it include people who could no longer do the job that they used to

do, or only people who are incapable of doing any job at all? There would also be

challenges if someone’s doctor had to ‘sign them off’ as unable to work, as doctors

might be reluctant to block a patient’s State Pension access, increasing take-up of the

option in ‘marginal’ cases.

Reduced early access could leave some living below the poverty line through retirement for

a decision they took when they were (say) 65; and this ‘scarring’ issue would be more acute

the earlier people were allowed to take their pensions.

A further problem with reduced early access to State Pension is the interaction with means-

tested Pension Credit, which would potentially act to reinstate the income given up in

exchange for early access, for those with no other income.

In short, although superficially attractive, we are not convinced that early access to State

Pensions is a credible solution to the issue of health and life expectancy inequalities.

Instead, the best answer if SPA is to continue to rise would be to focus on the benefit

system for those under pension age. For example, the Institute for Fiscal Studies have

argued20 that means-tested benefits should be enhanced for those within 12 months of State

Pension age, to reduce the financial penalty for those ’in the gap’ between stopping work

and reaching SPA. Whilst this would do little for those who might drop out of the labour

market many years before SPA, it would provide for some enhancement of support which

would not suffer from the permanent “scarring” issue described above once someone was

above pension age.

e) To what extent should dependency ratios be considered?

The dependency ratio – the number of people above SPA relative to those of working age –

provides a high-level indication of demographic pressure on the public finances, indicating

the balance between those contributing through taxation and those drawing pensions and

other age-related benefits, helping to signal long-term fiscal sustainability challenges.

However, the dependency ratio is a blunt instrument. It assumes all working-age adults are

economically active and all above SPA are dependent, which is increasingly inaccurate. It

also overlooks productivity growth, which can offset the fiscal effects of population: a smaller

working-age population might still sustain more retirees if each worker produces and earns

more.

Using the dependency ratio to directly determine SPA could result in increases even if life

expectancy stagnates or declines, creating perceptions of unfairness. While it remains

useful as an indicator of affordability, we do not believe that it should be used

mechanistically to determine SPA.

20 https://ifs.org.uk/publications/means-tested-support-people-approaching-and-beyond-state-pension-age