Download as PDF, PPTX

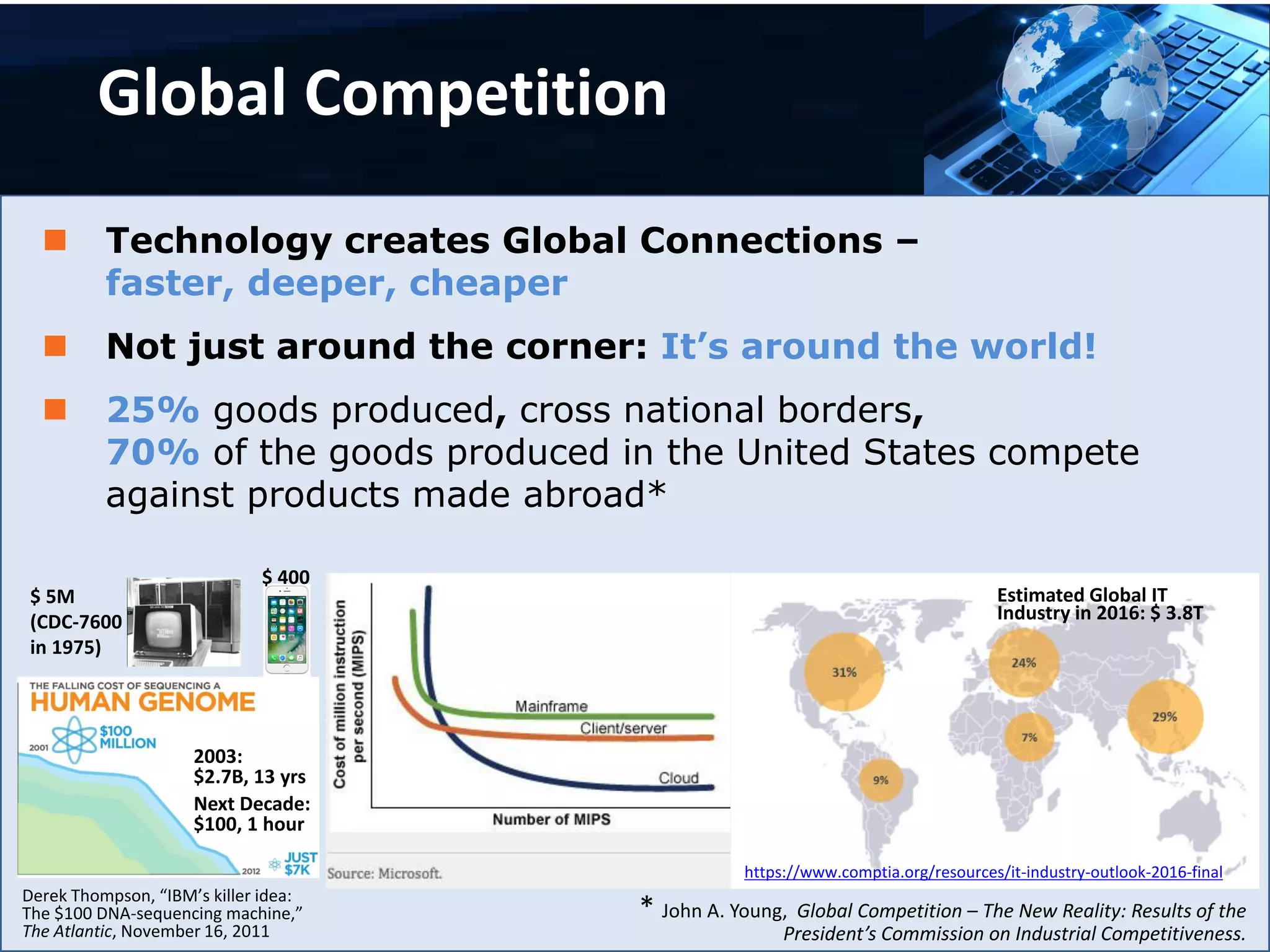

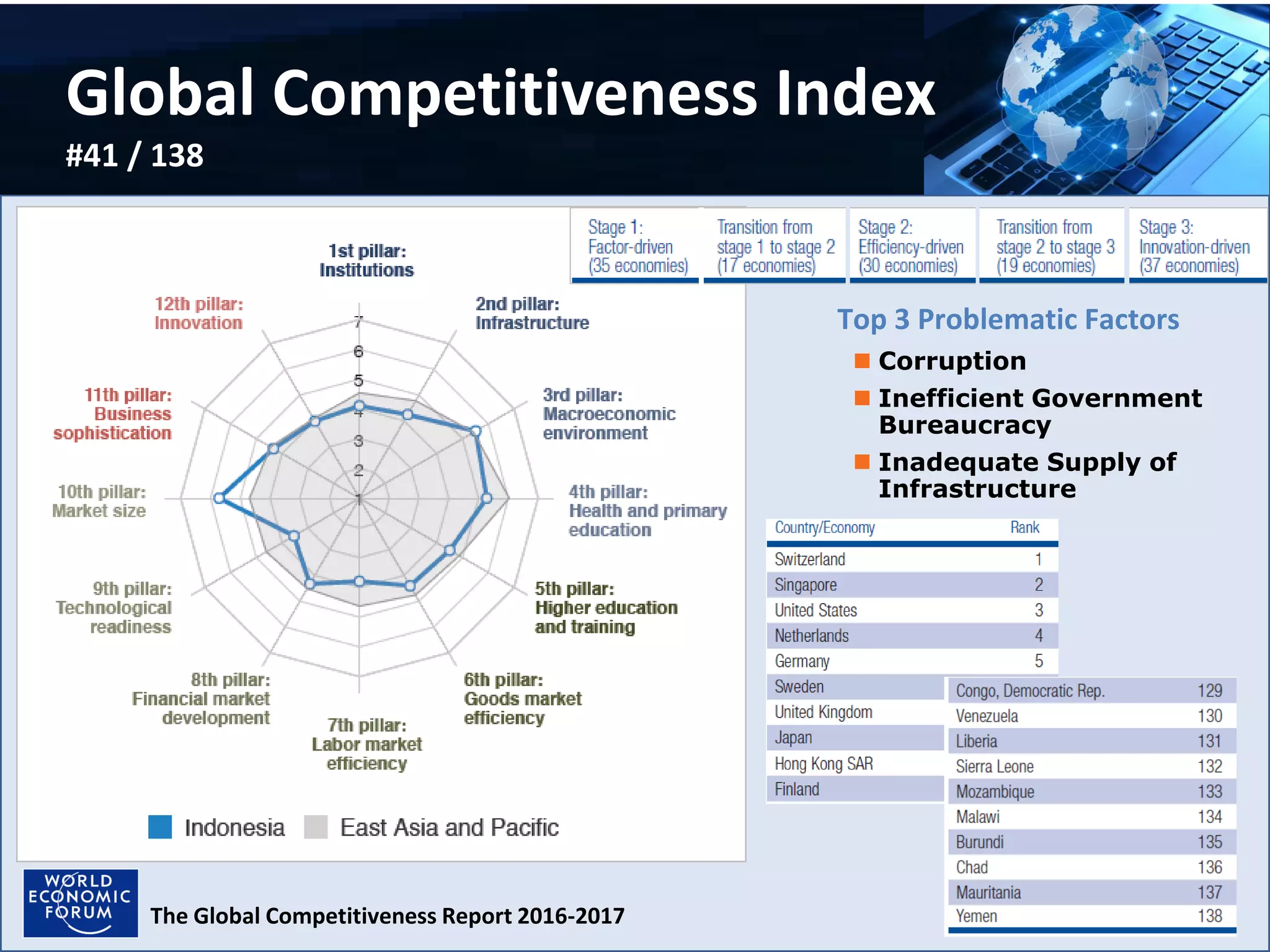

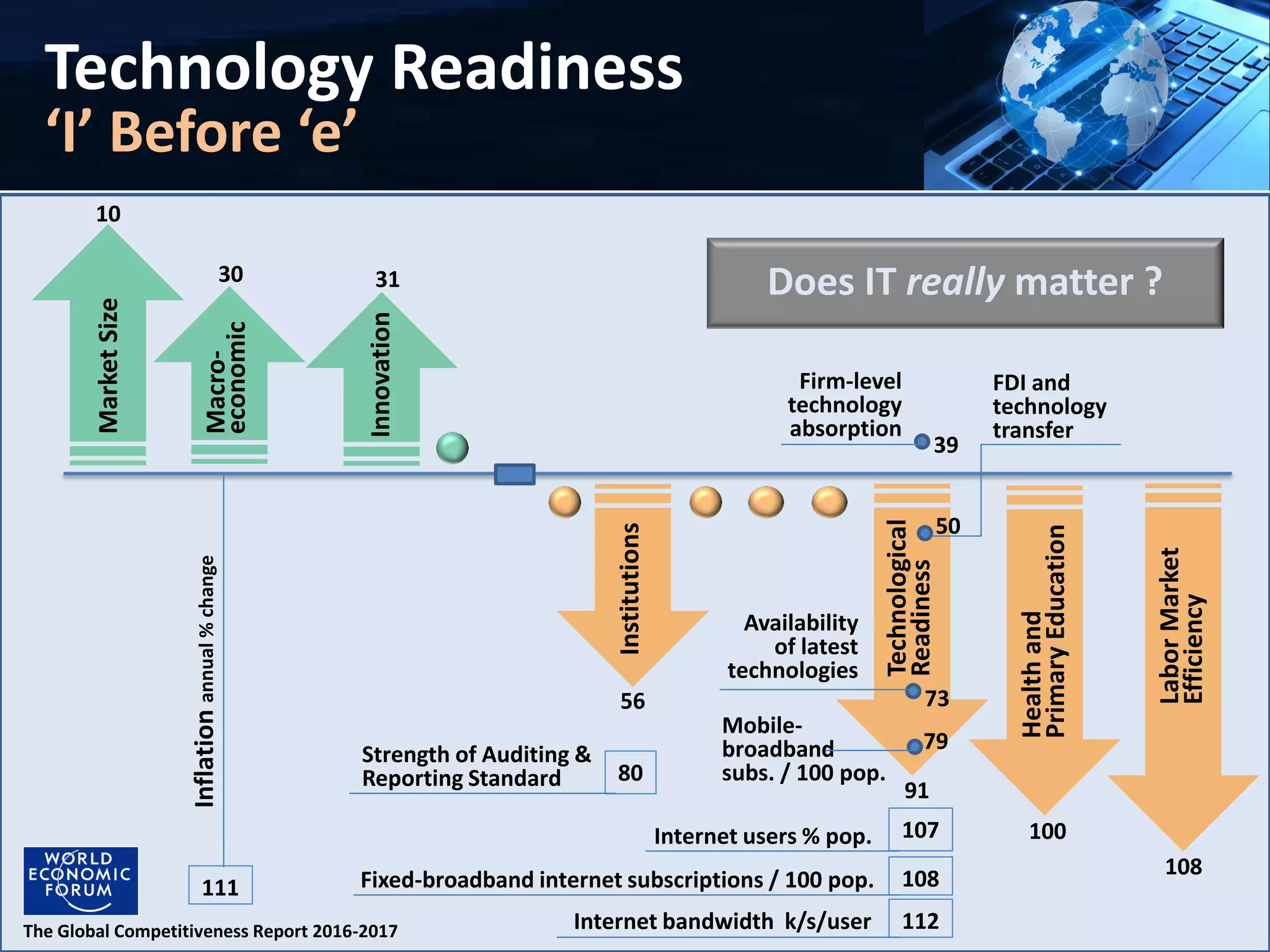

The document discusses the impact of globalization and technology on the economy, particularly within the field of information technology. It highlights the increase in global competition, the importance of innovation, and the challenges facing businesses, such as inadequate infrastructure and corruption. Additionally, it emphasizes the need for a cultural shift in organizations to embrace digital transformation and adapt to new business models.