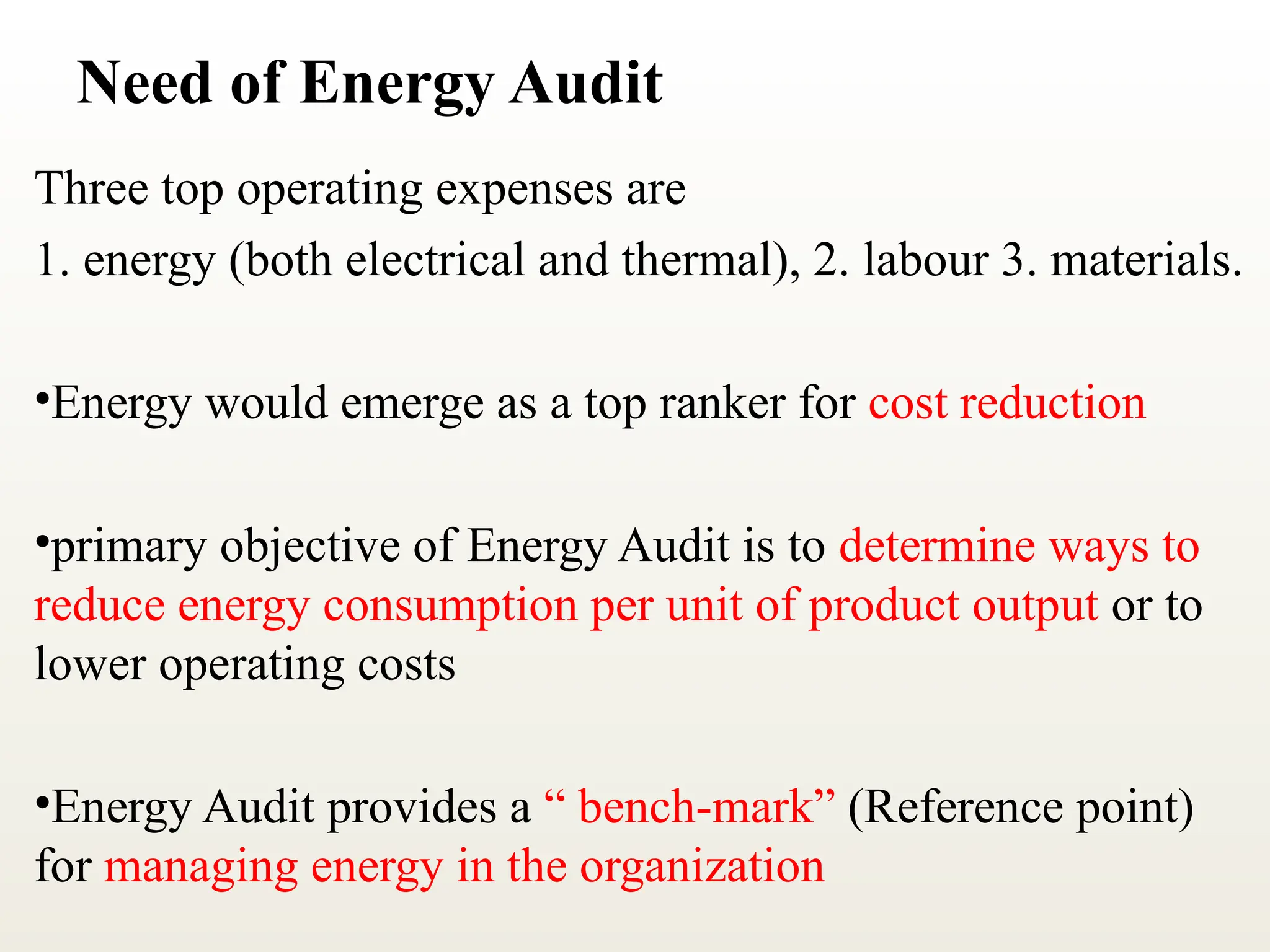

Need of Energy Audit

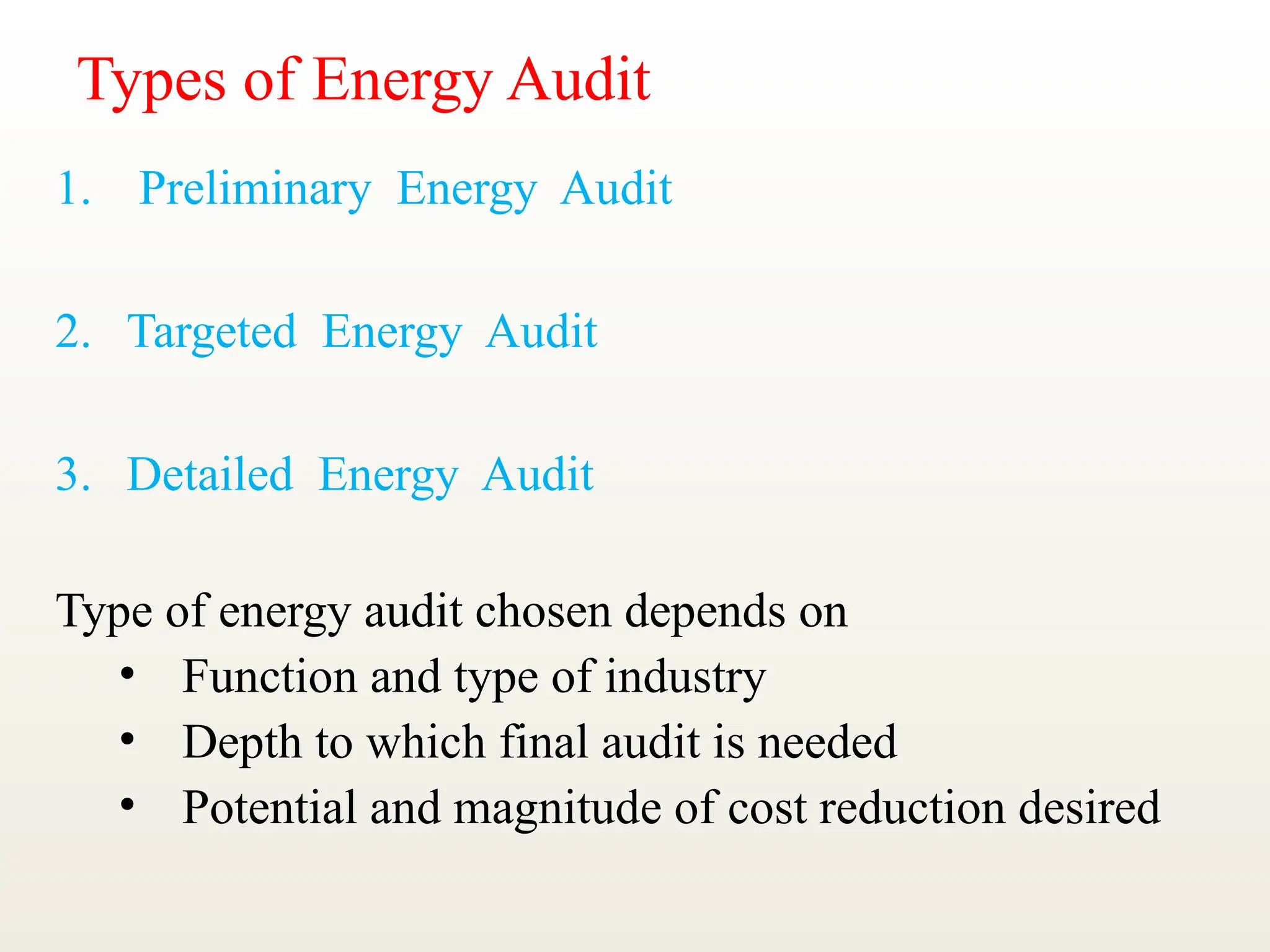

Types of energy audit

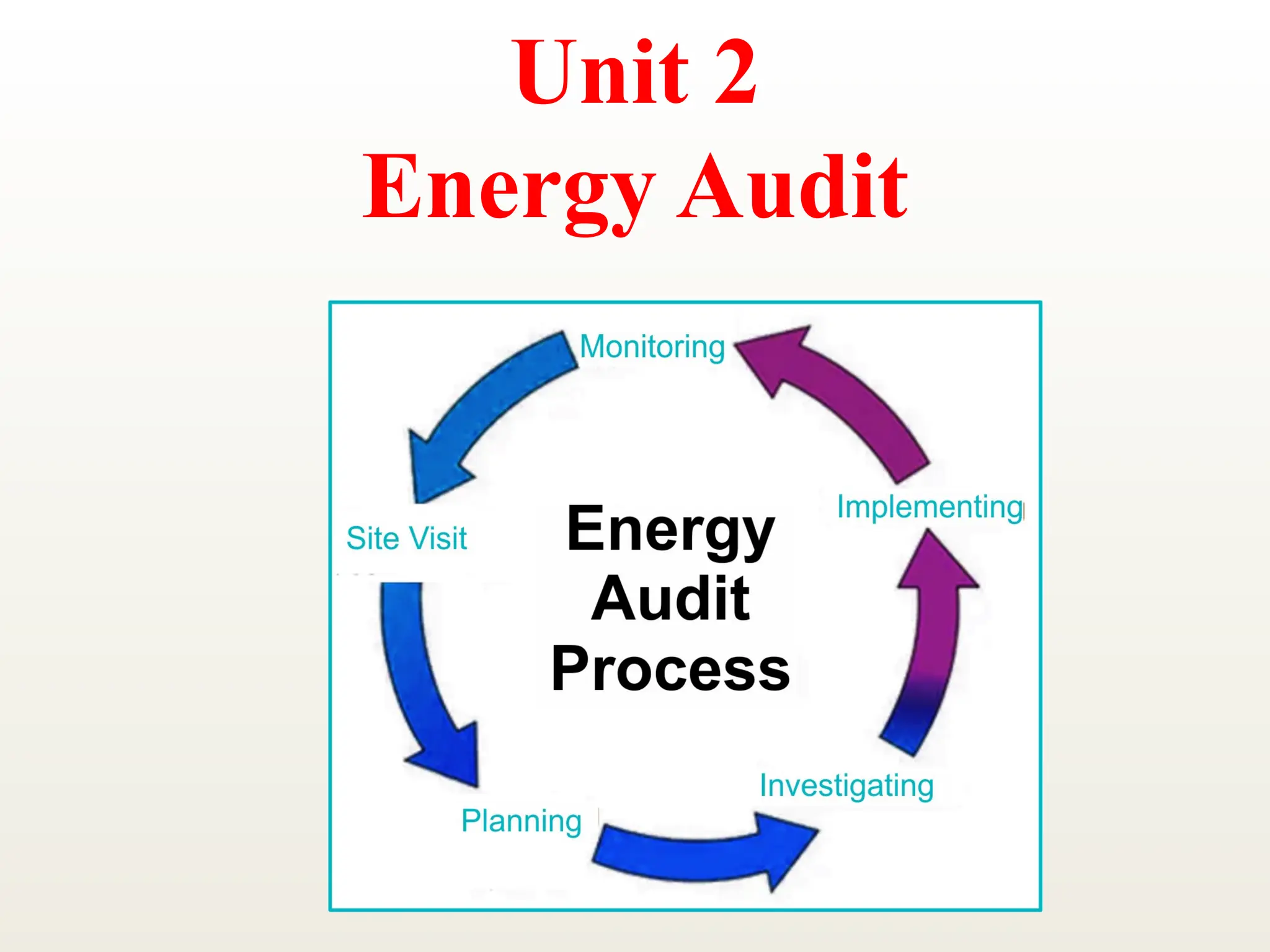

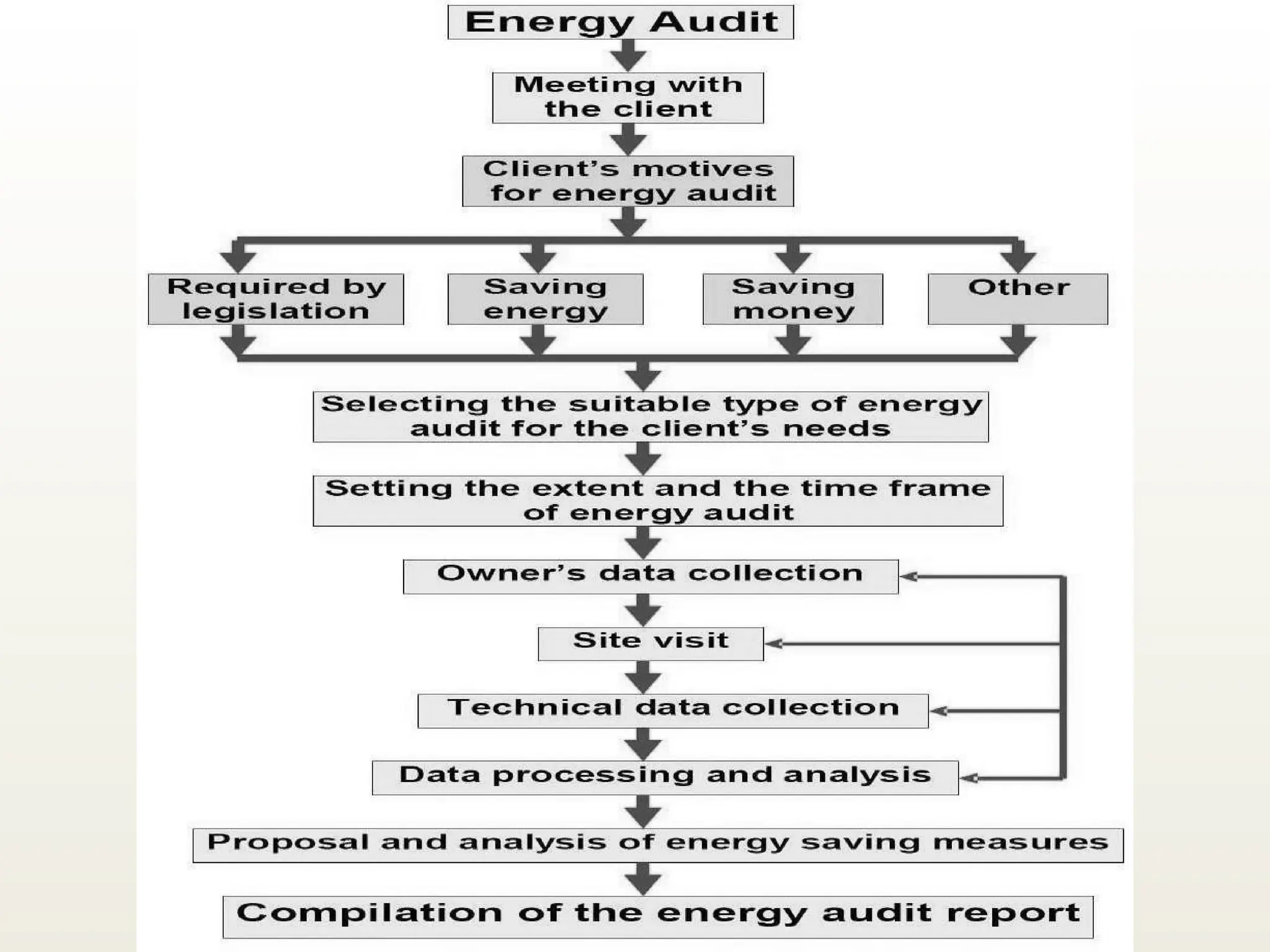

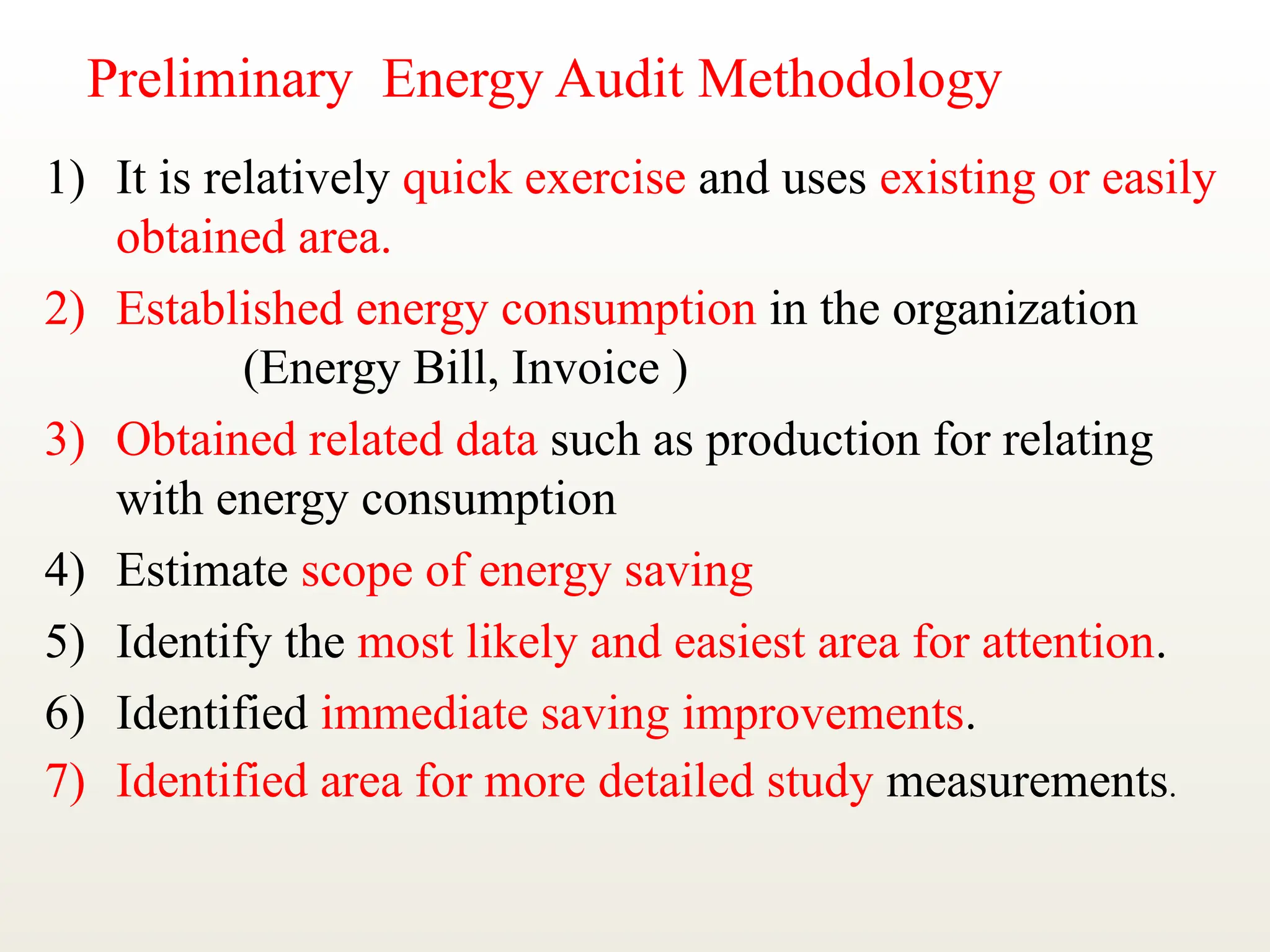

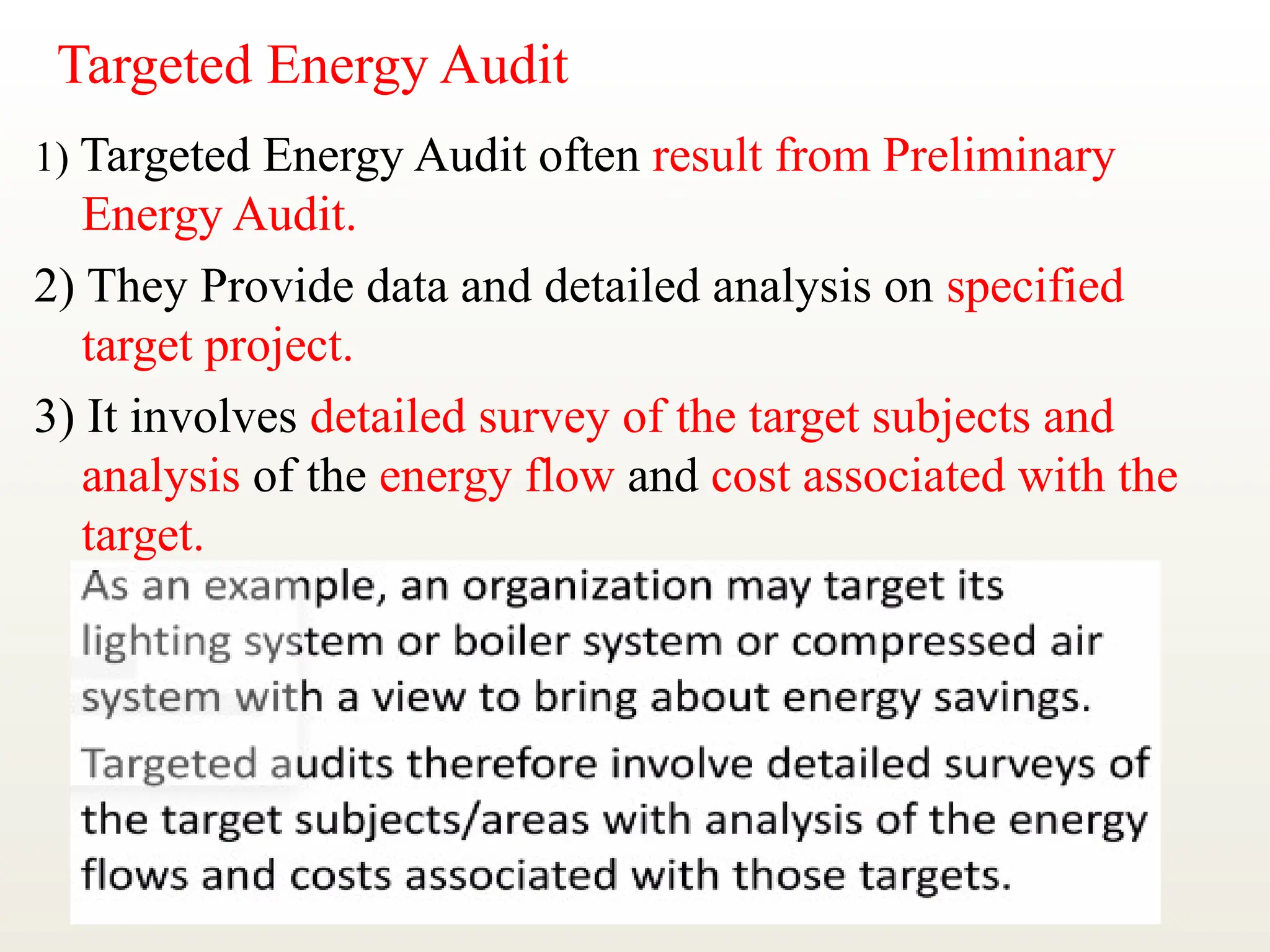

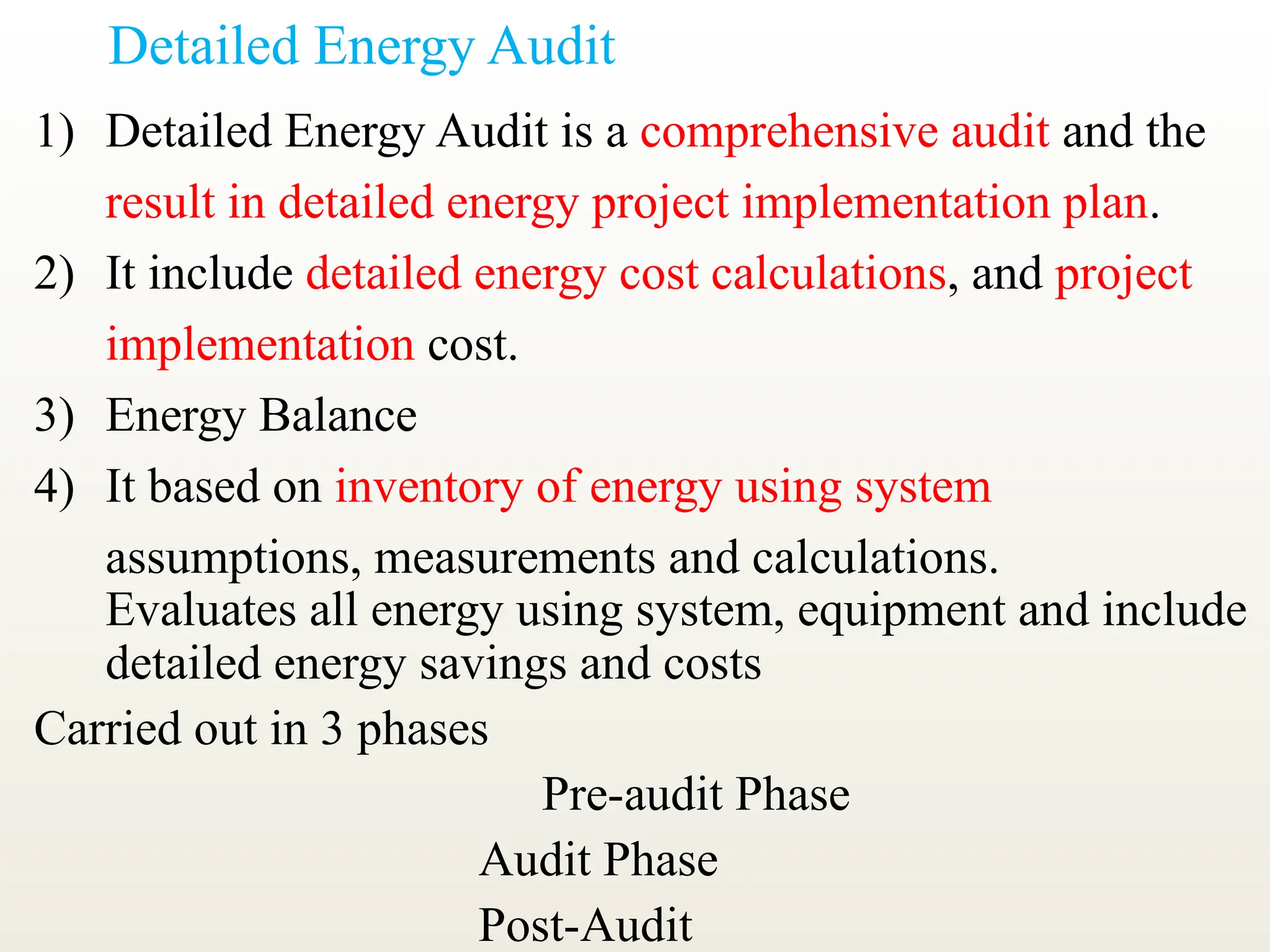

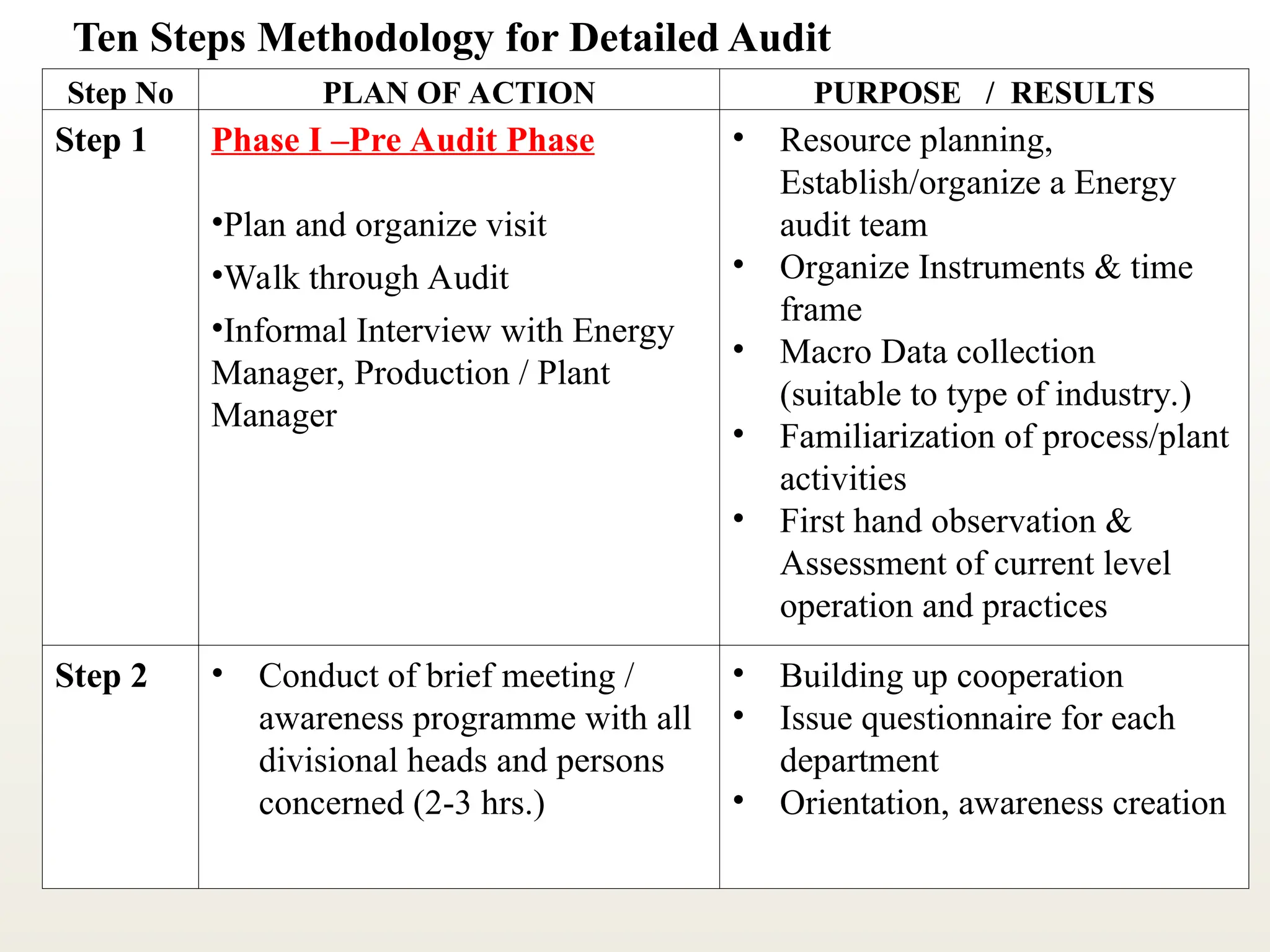

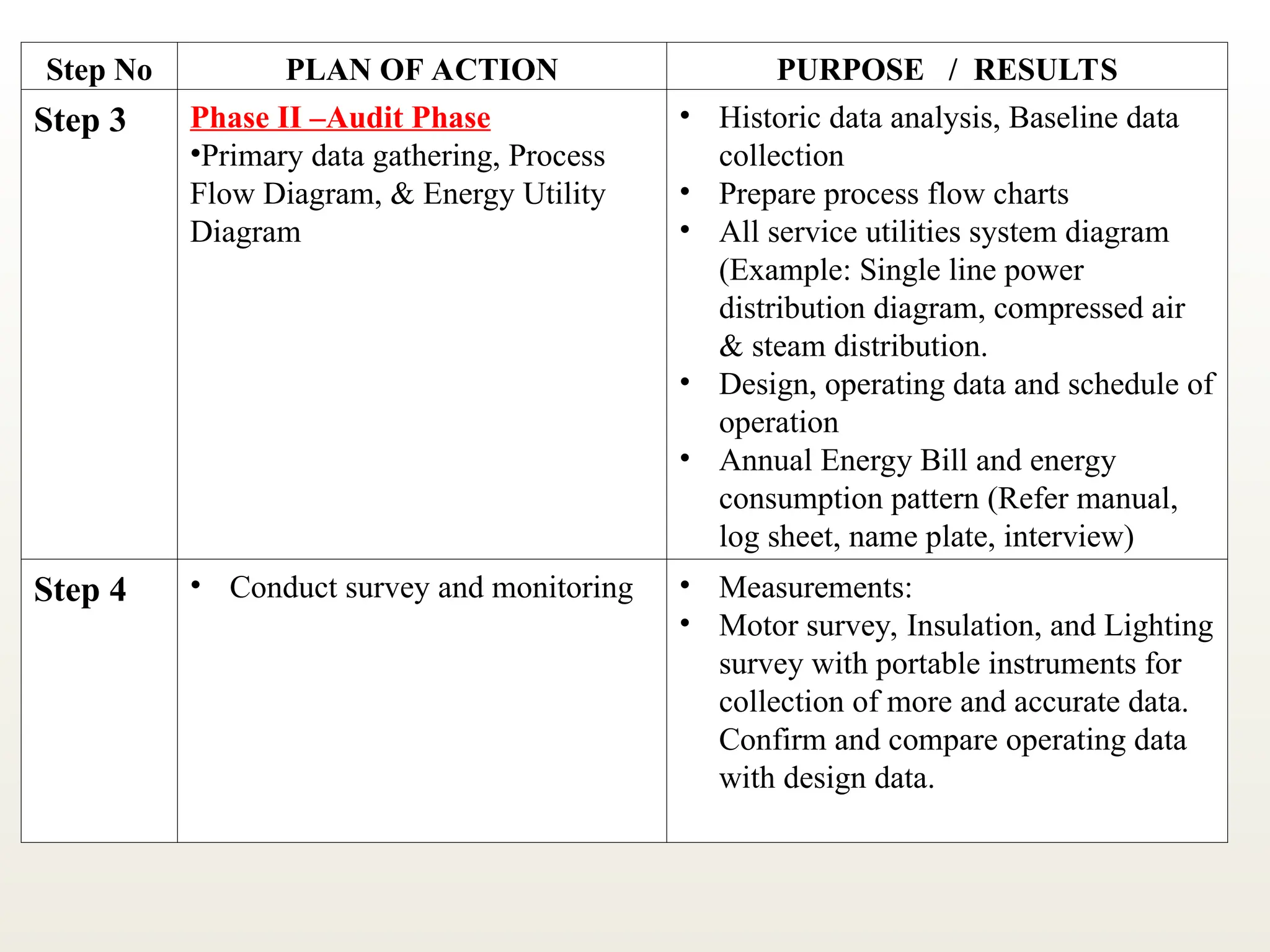

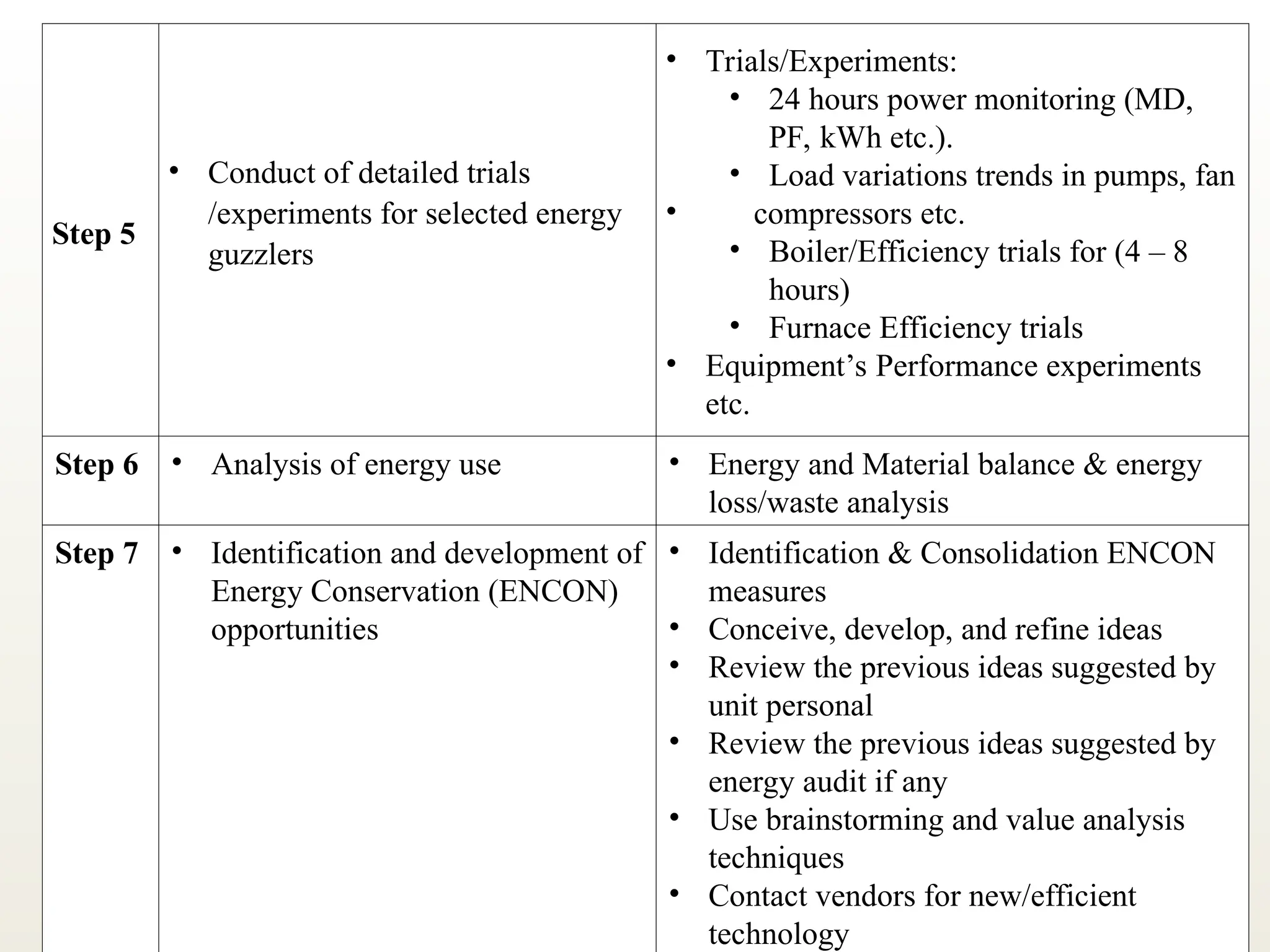

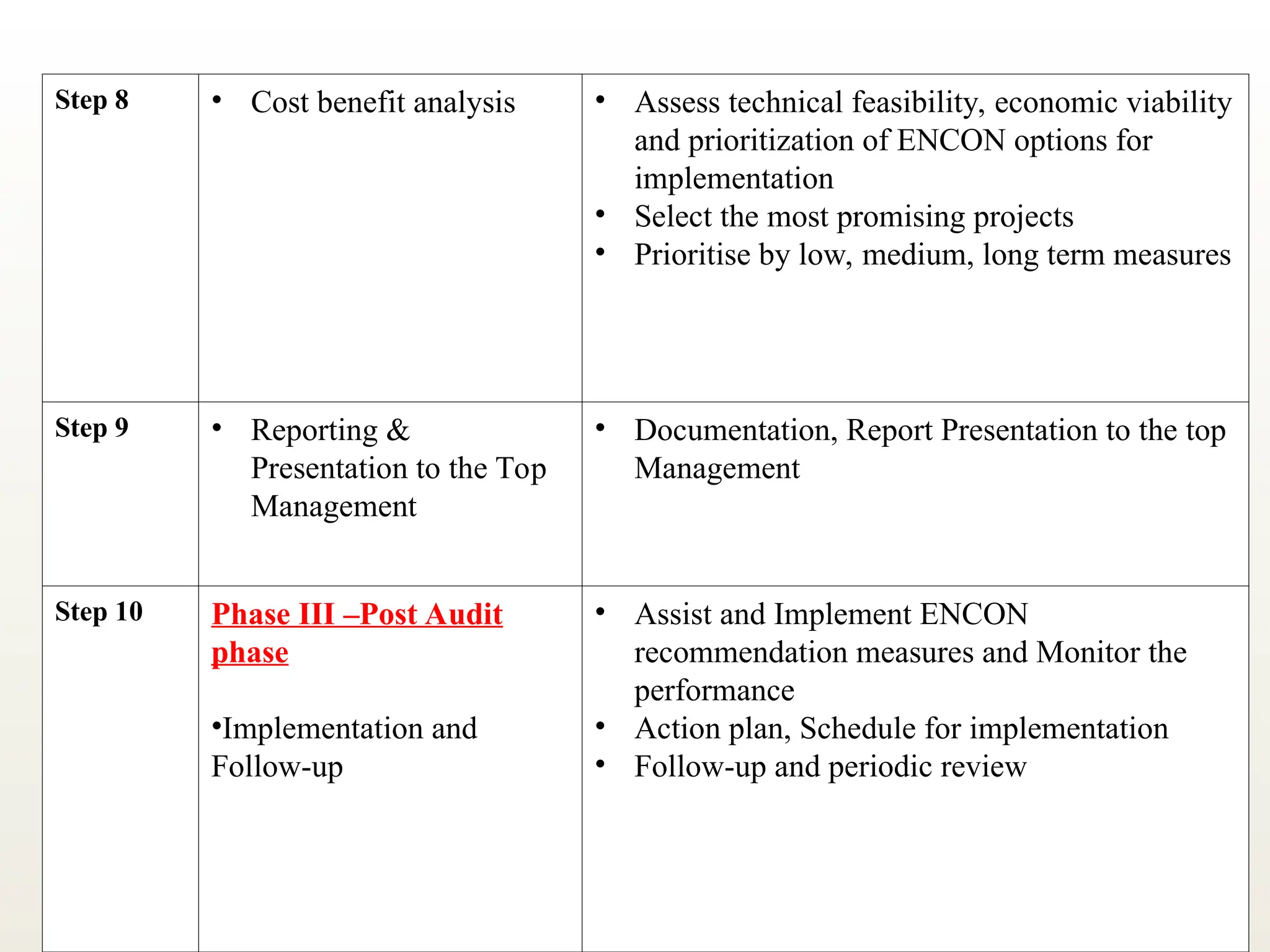

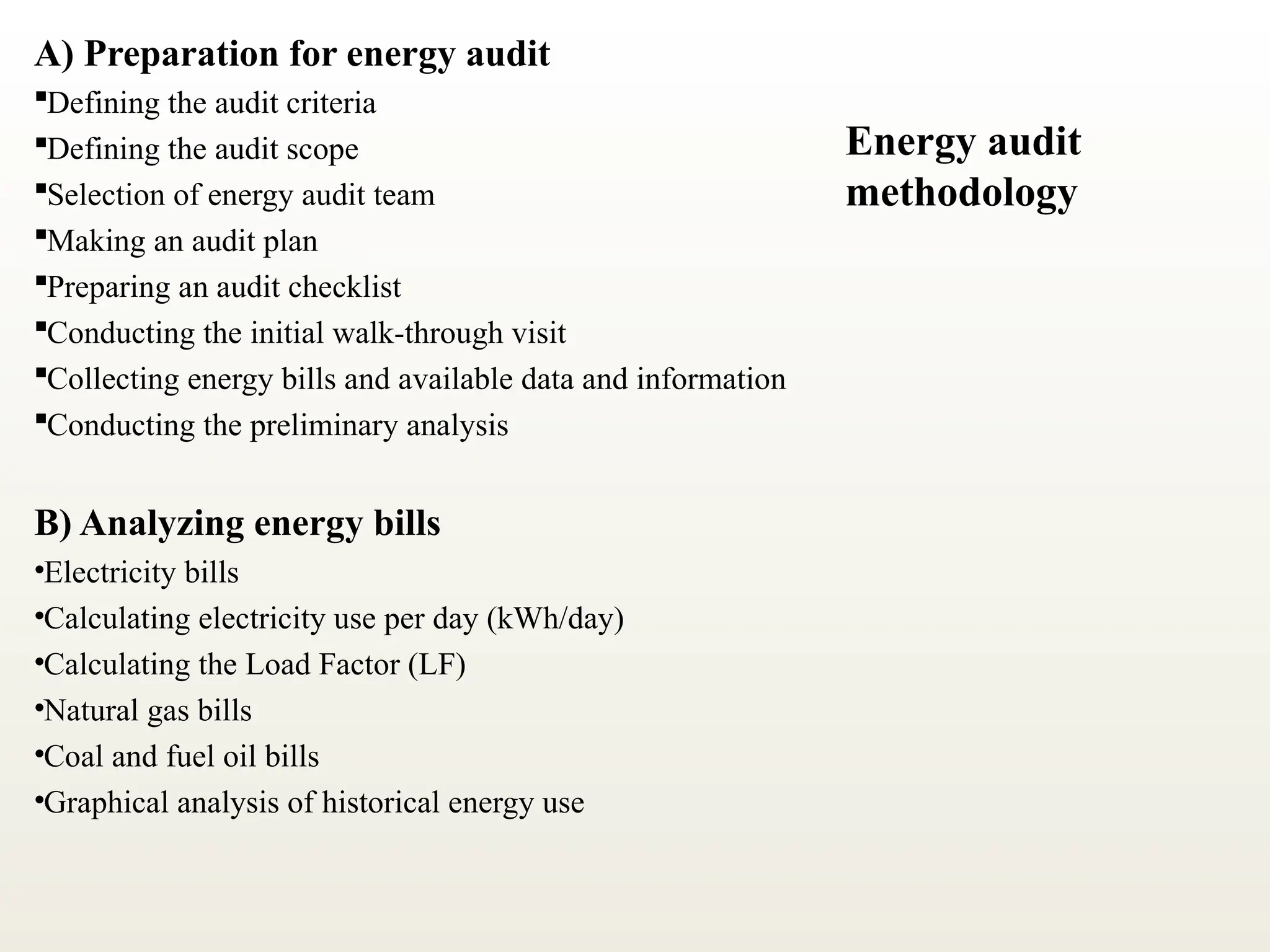

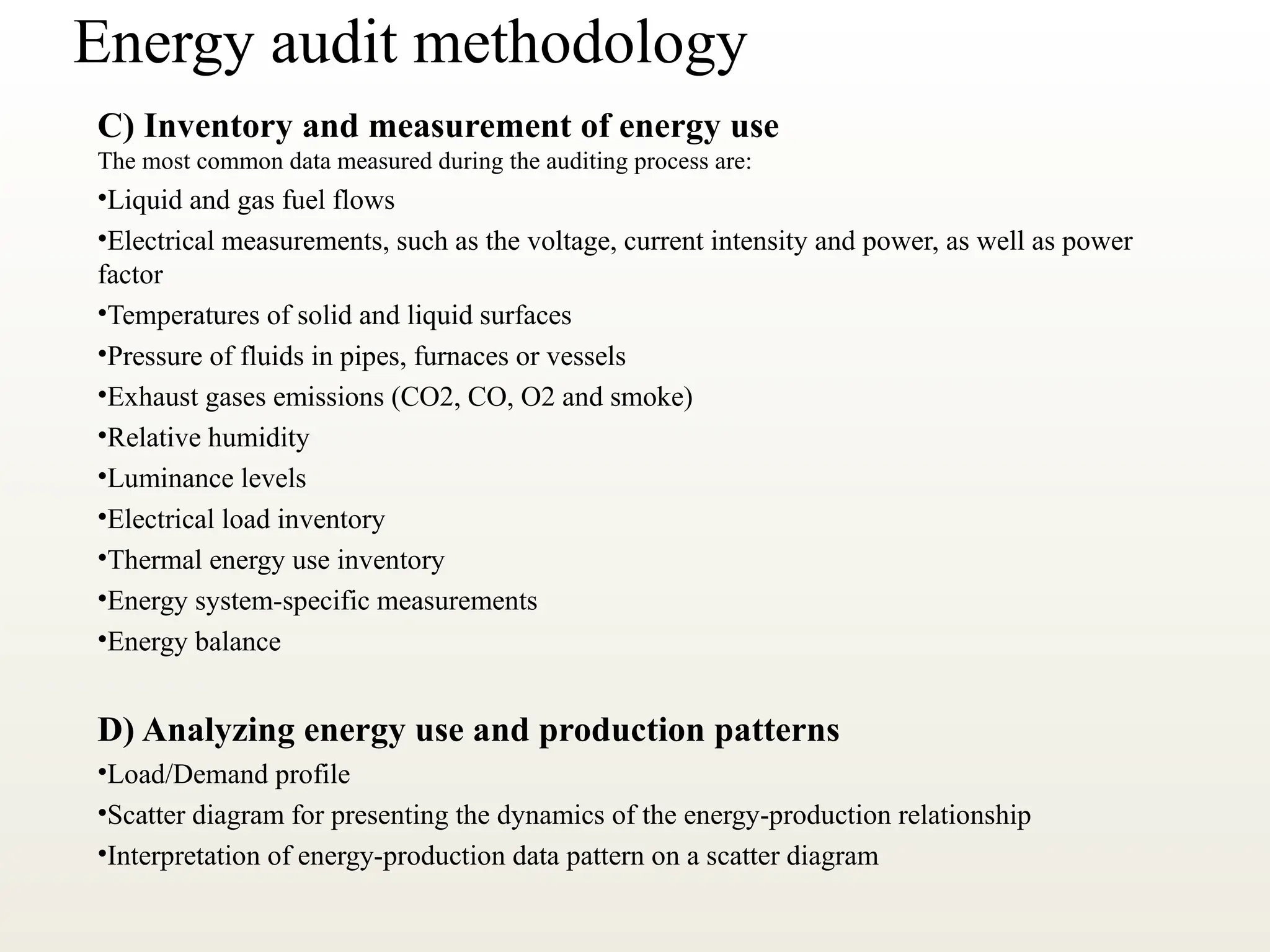

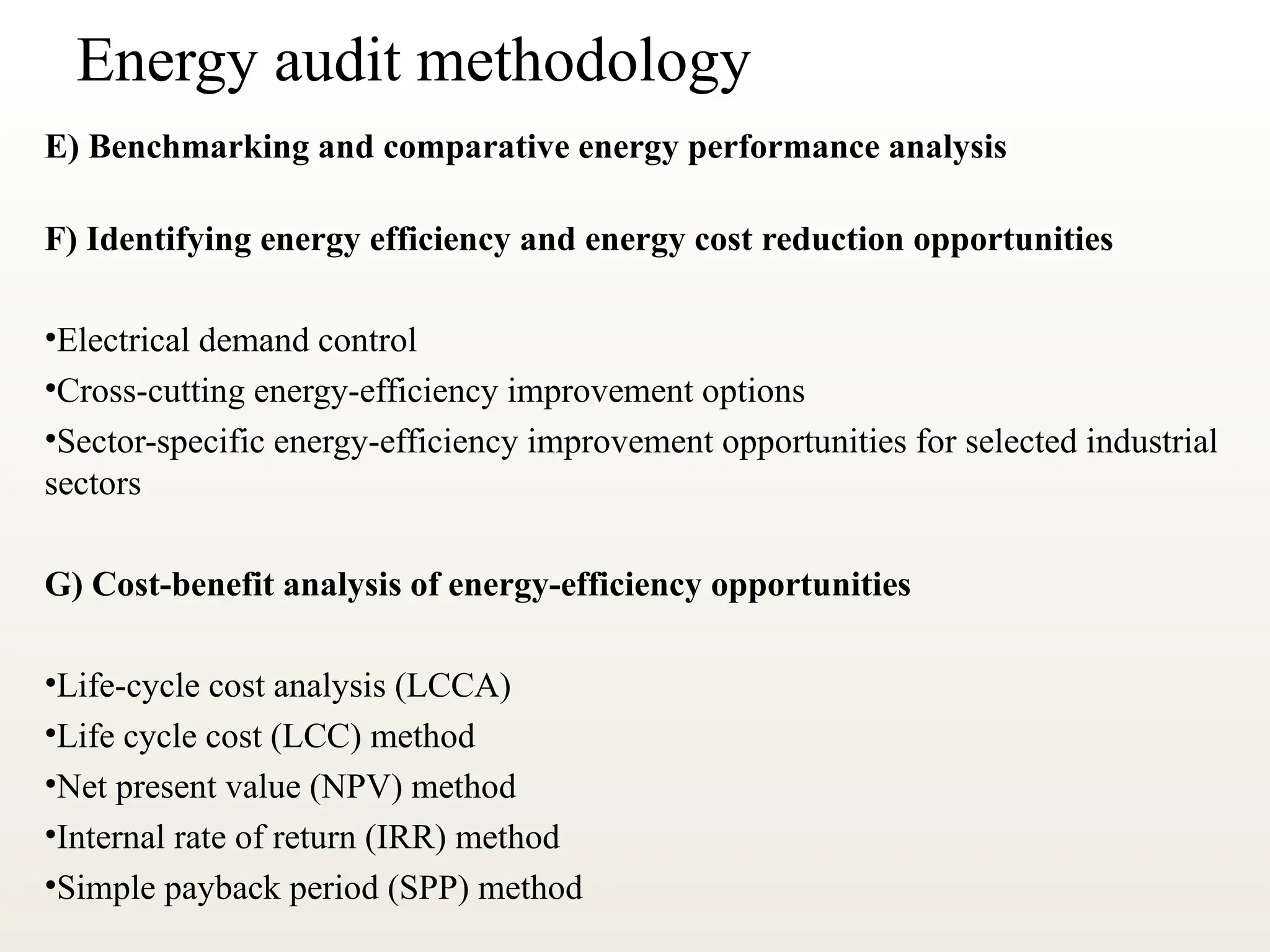

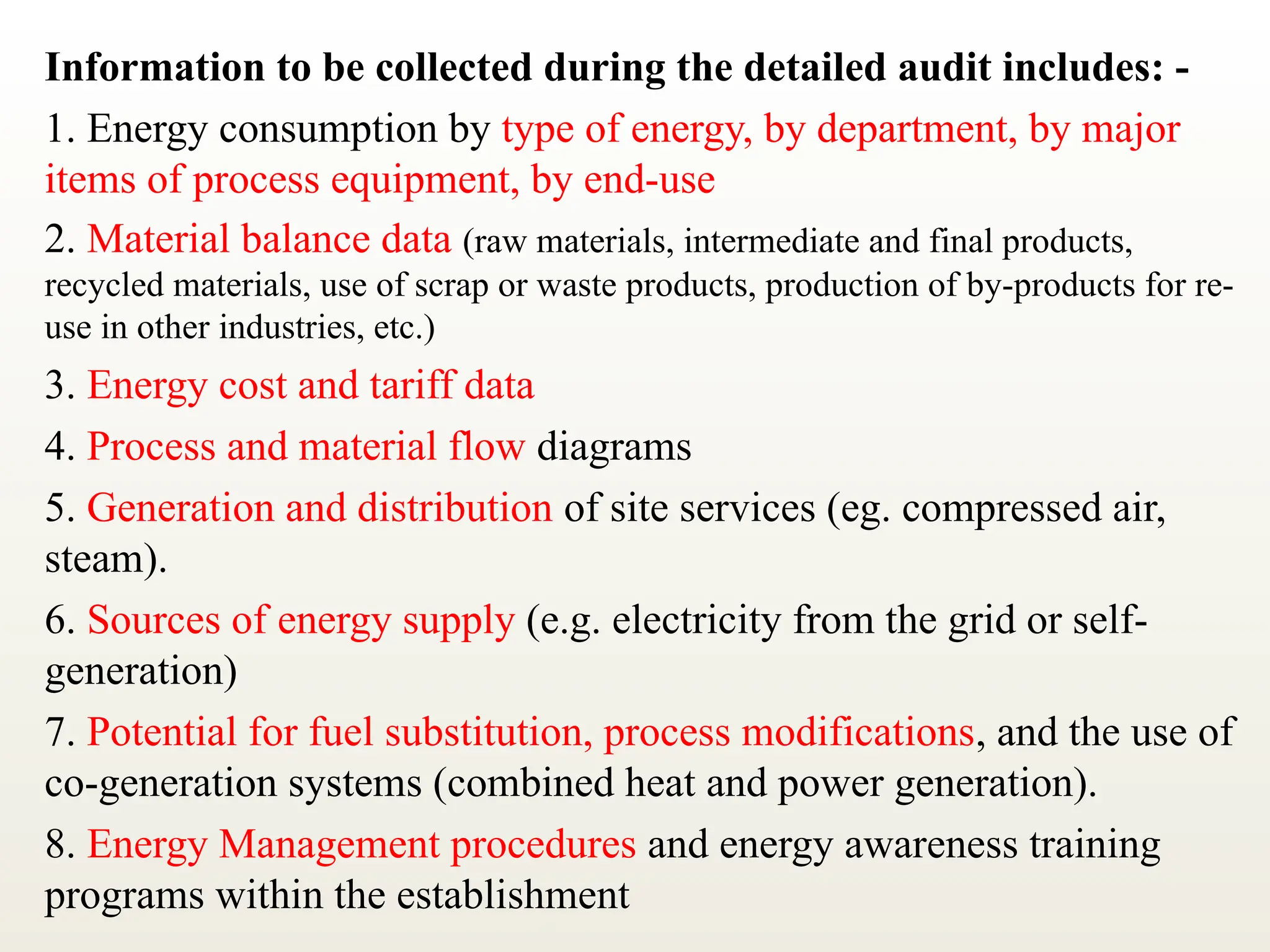

Energy audit methodology

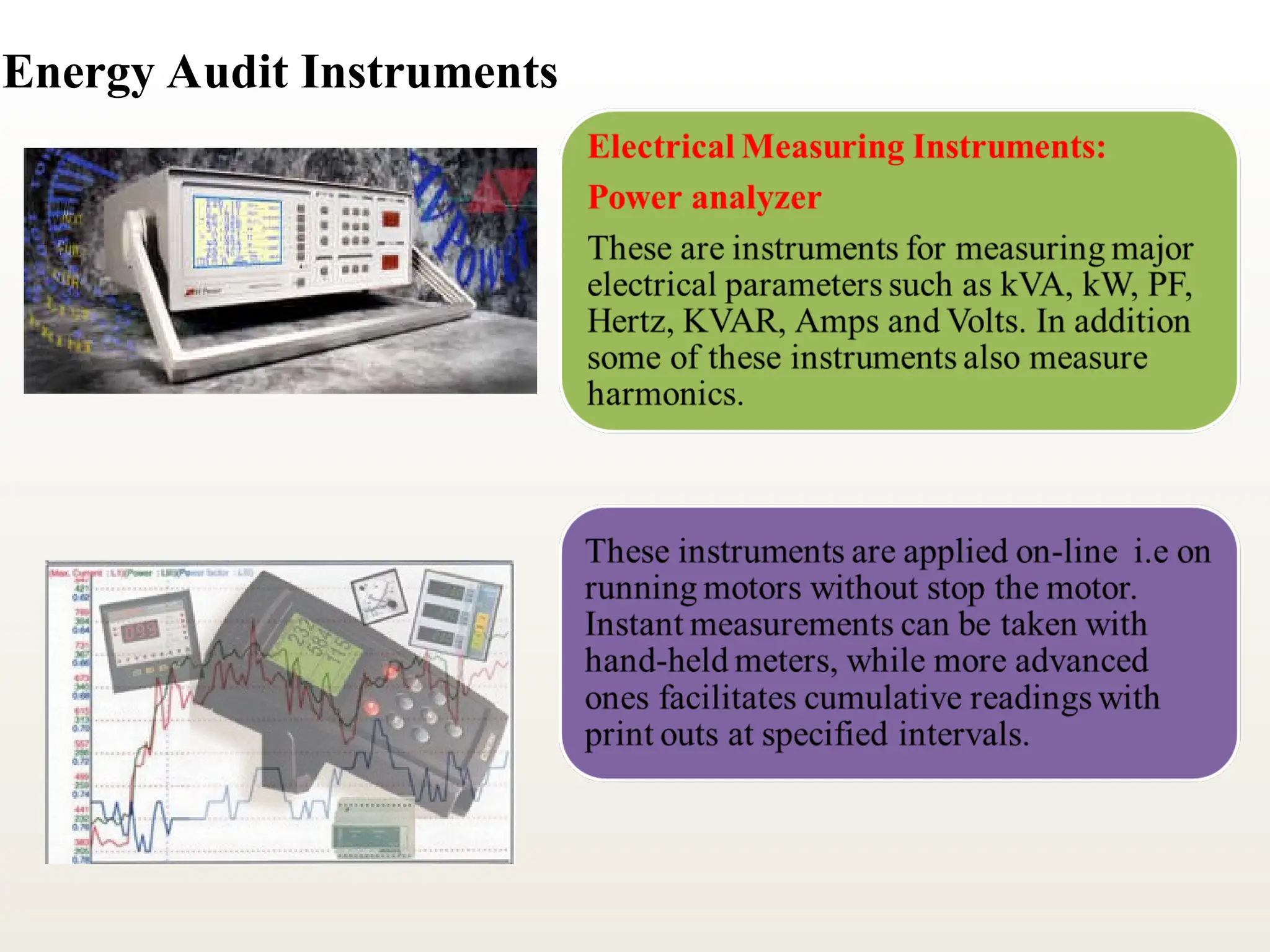

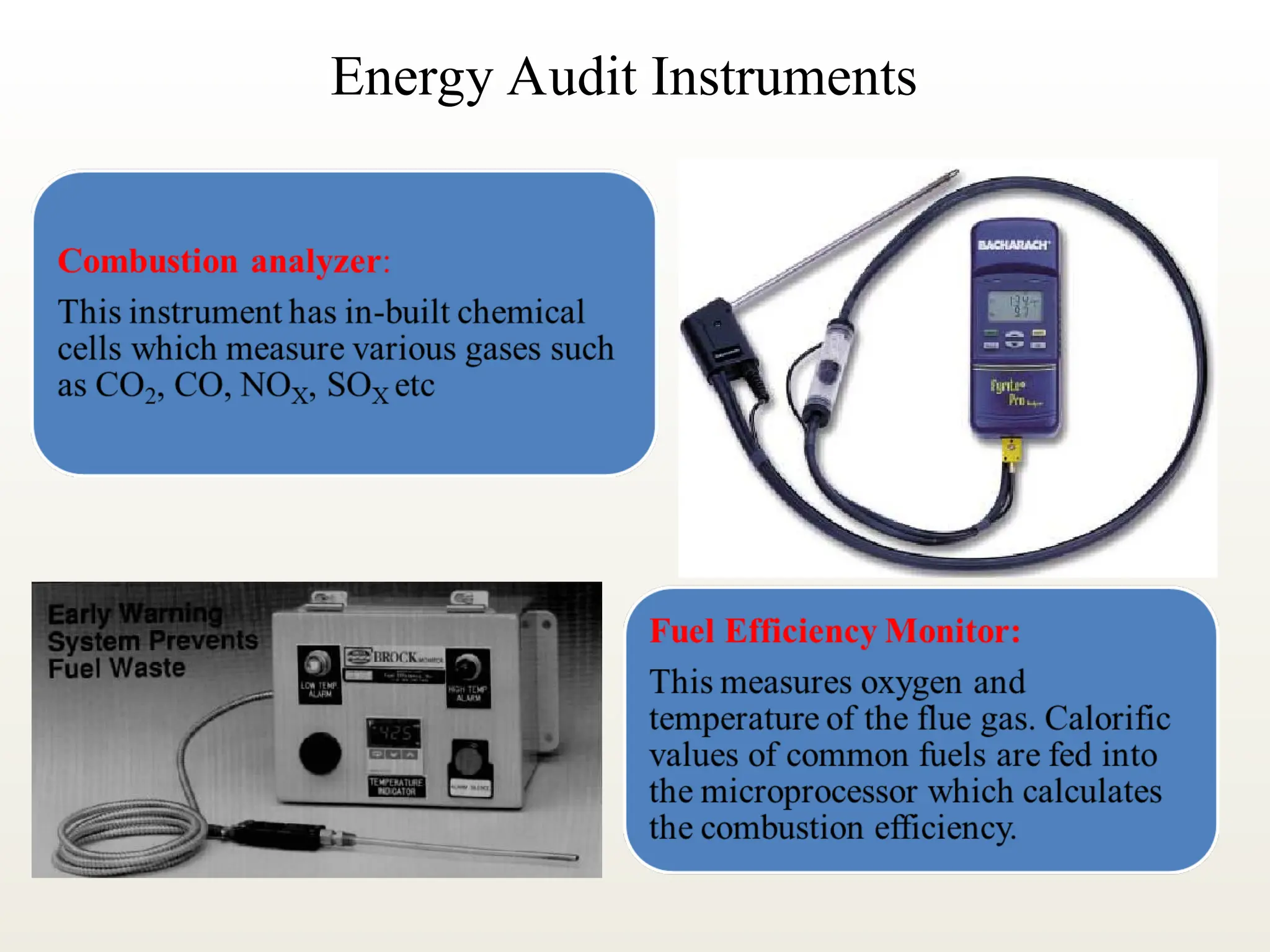

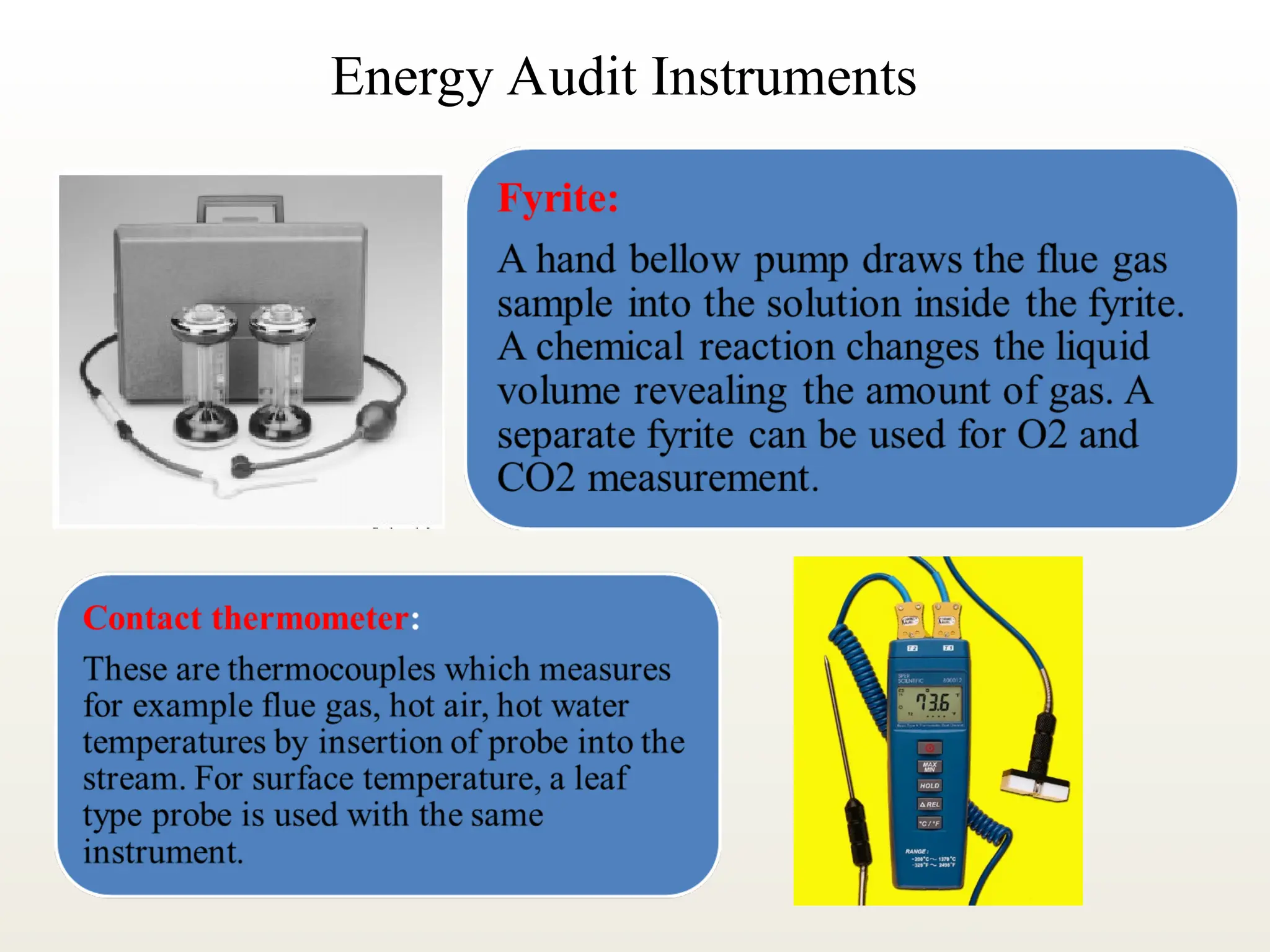

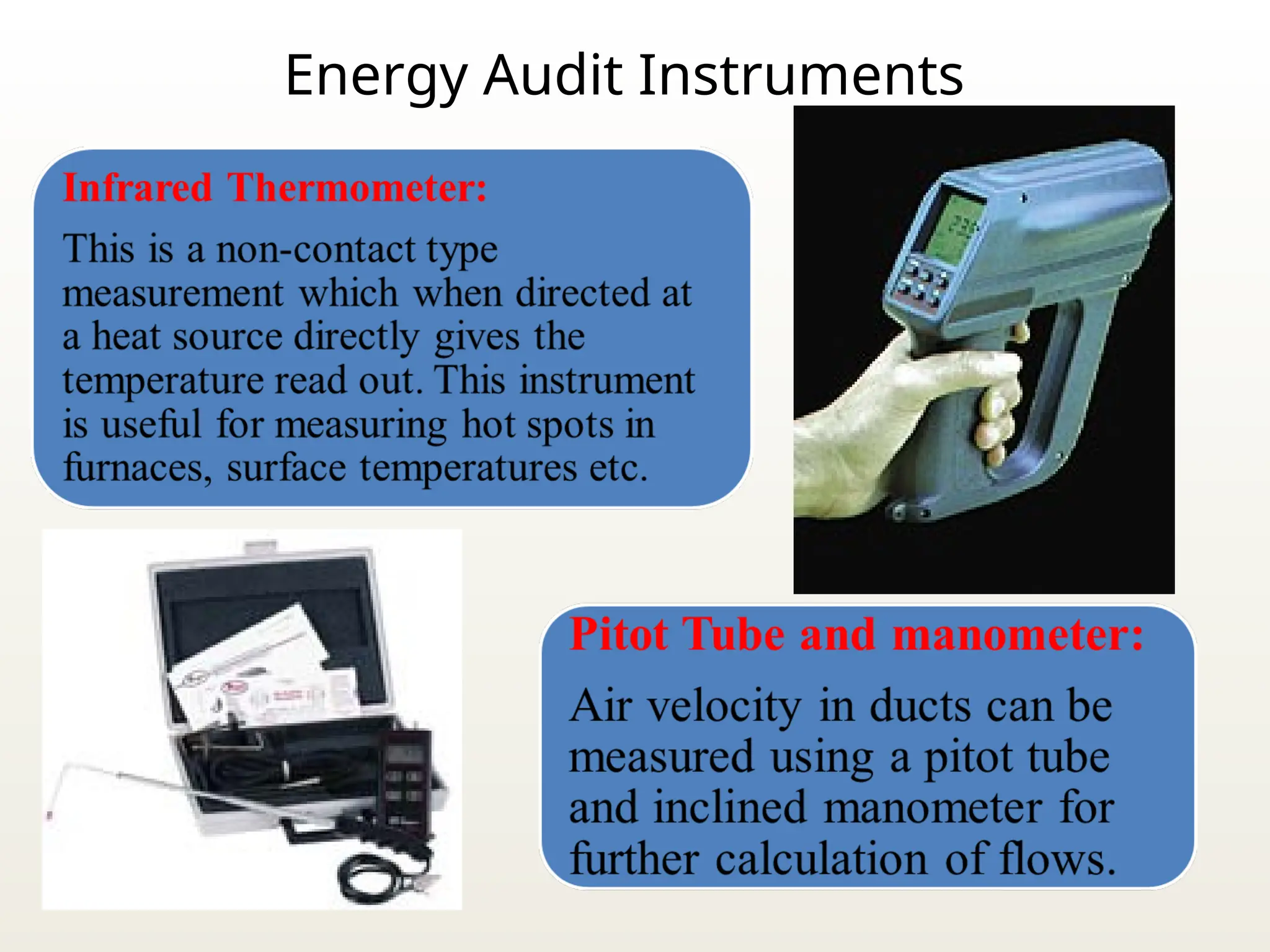

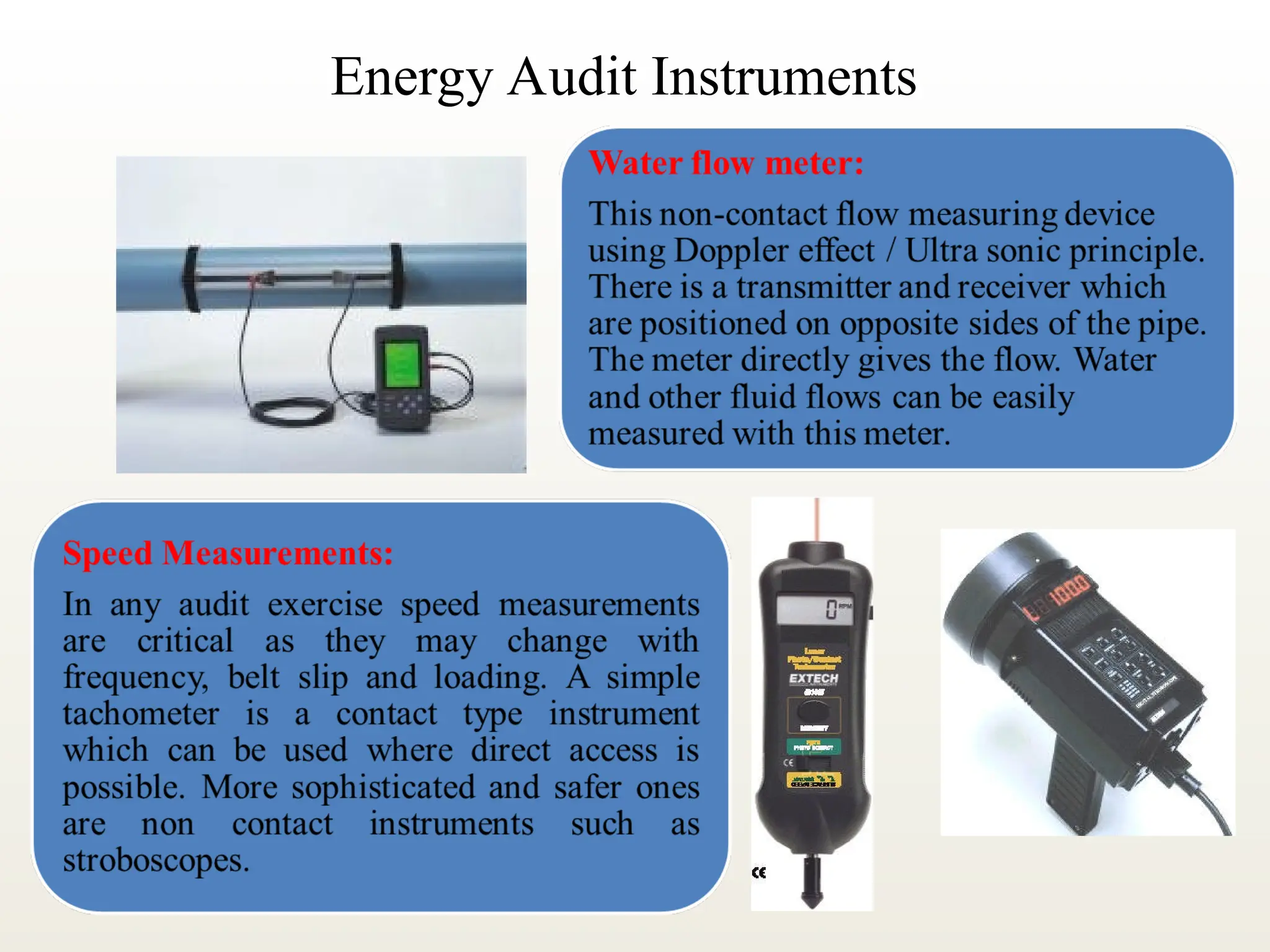

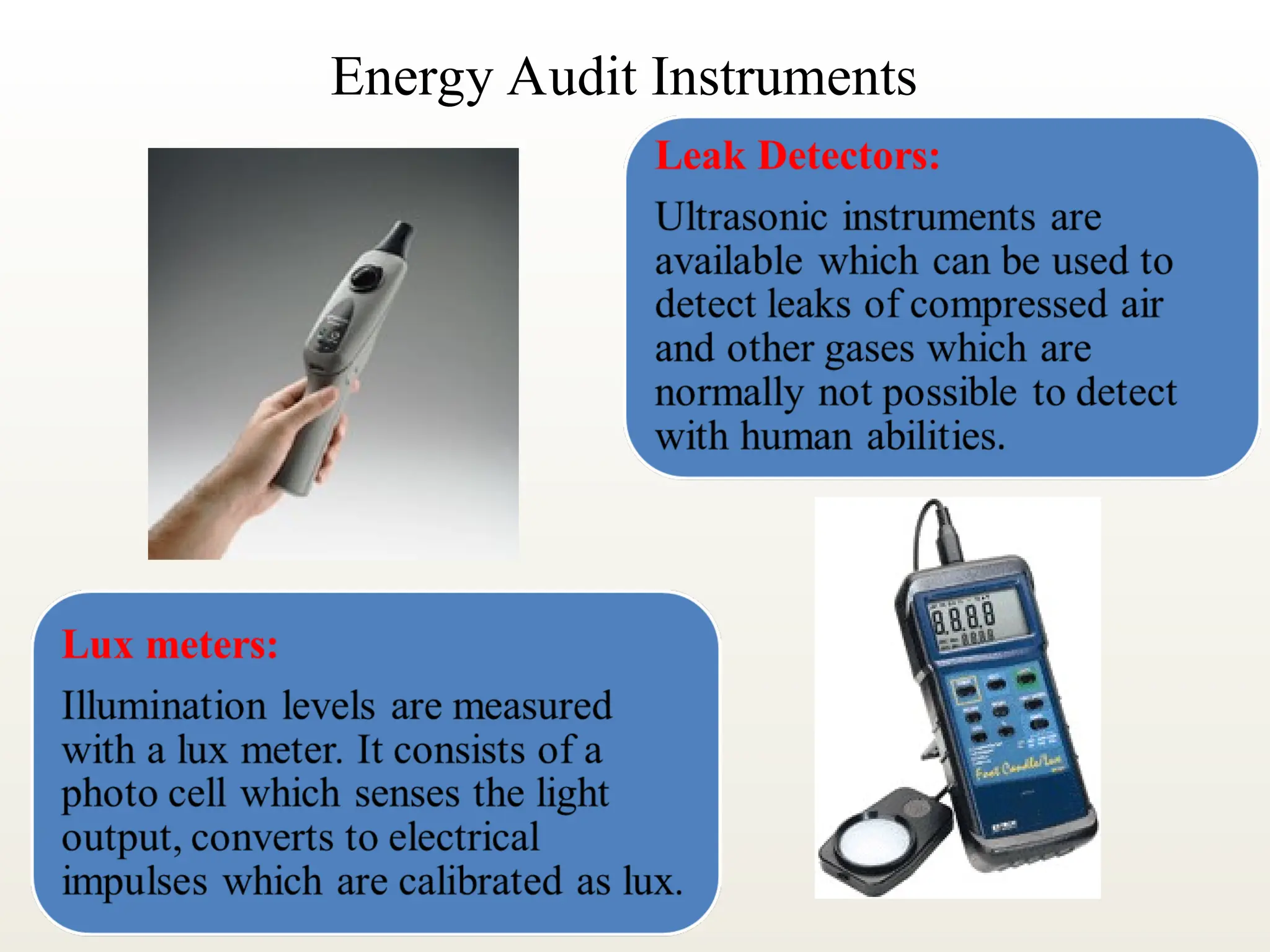

Instruments, equipment used in energy audit

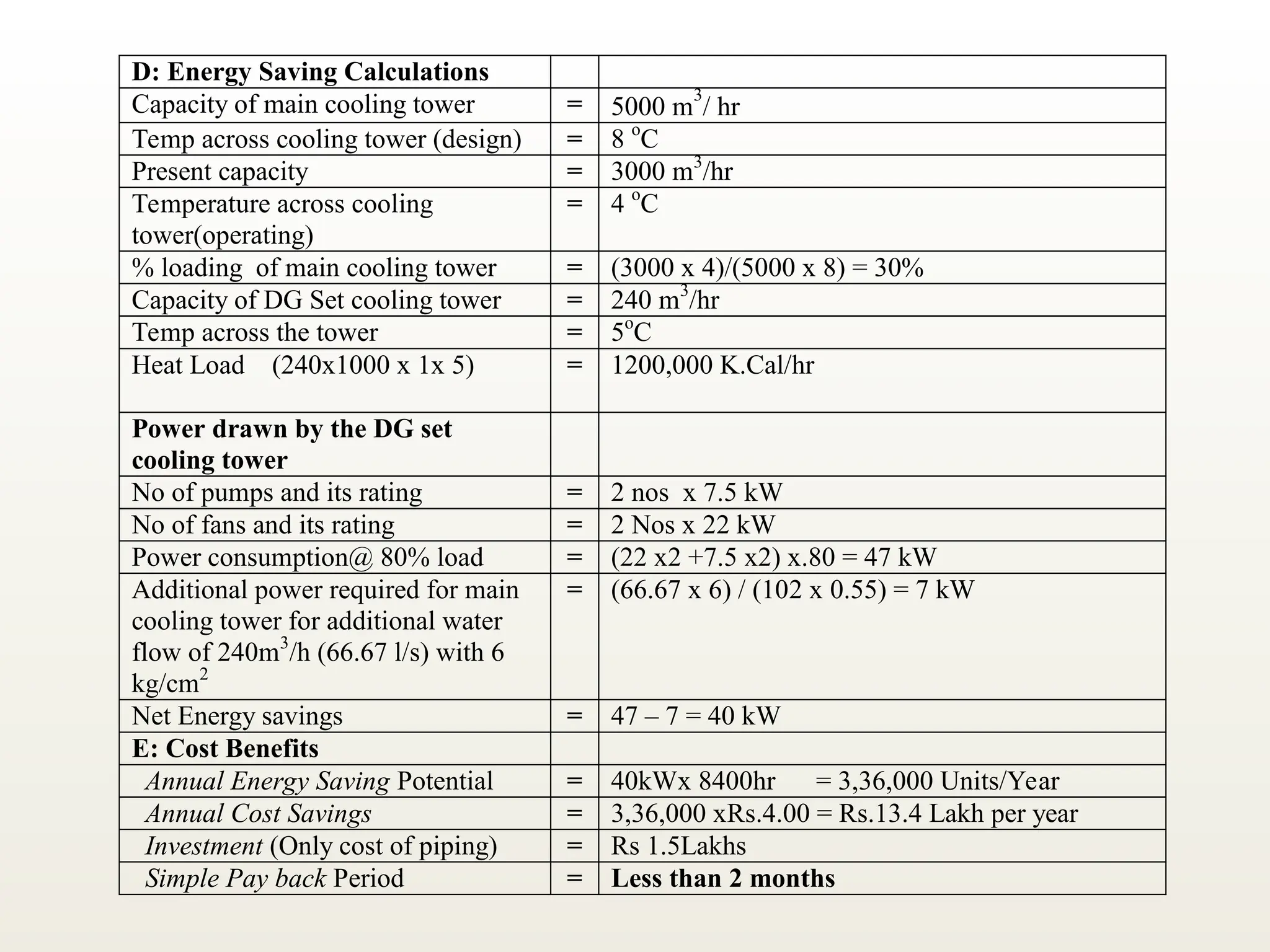

Analysis and recommendations of energy audit

Benchmarking

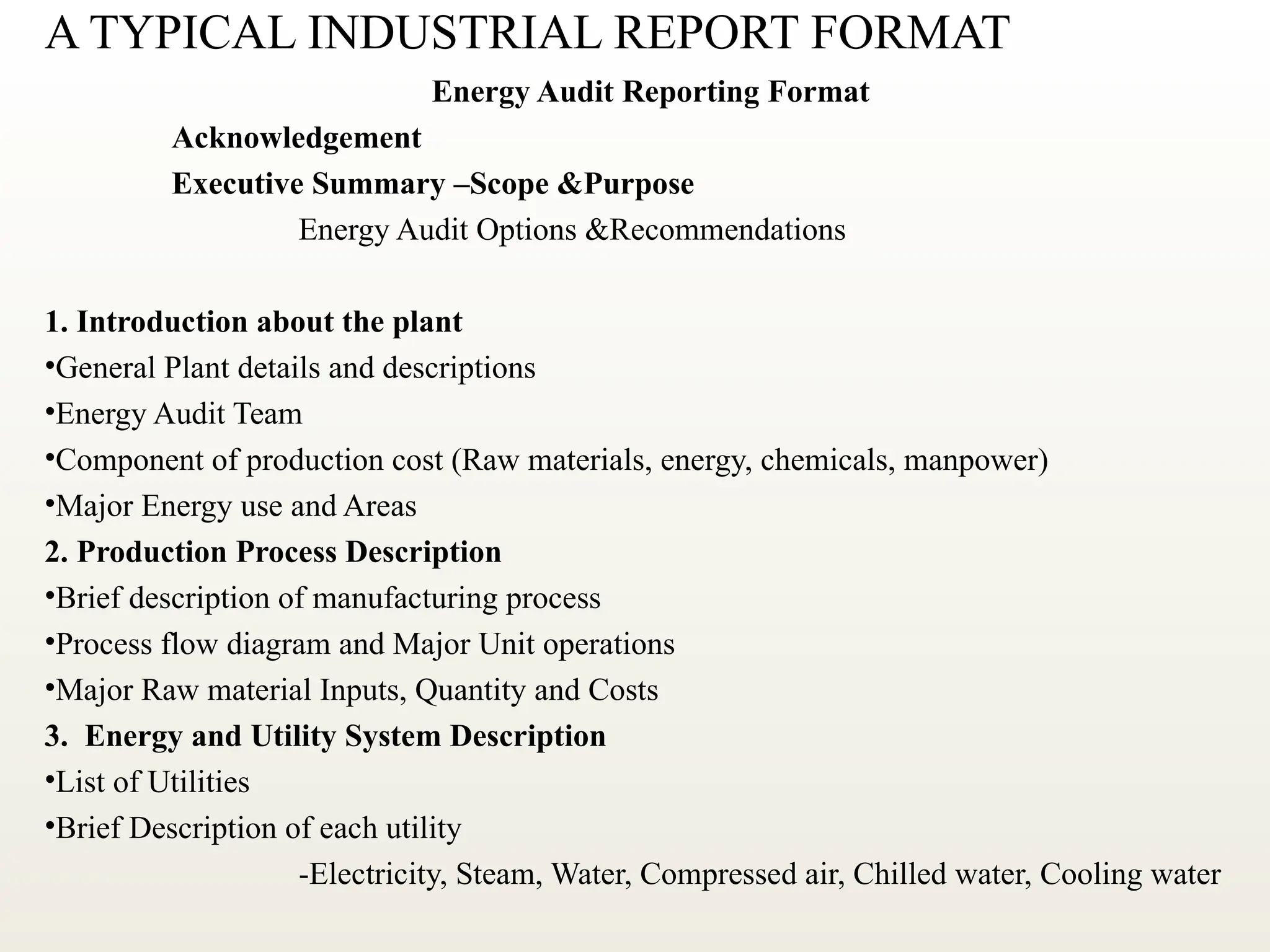

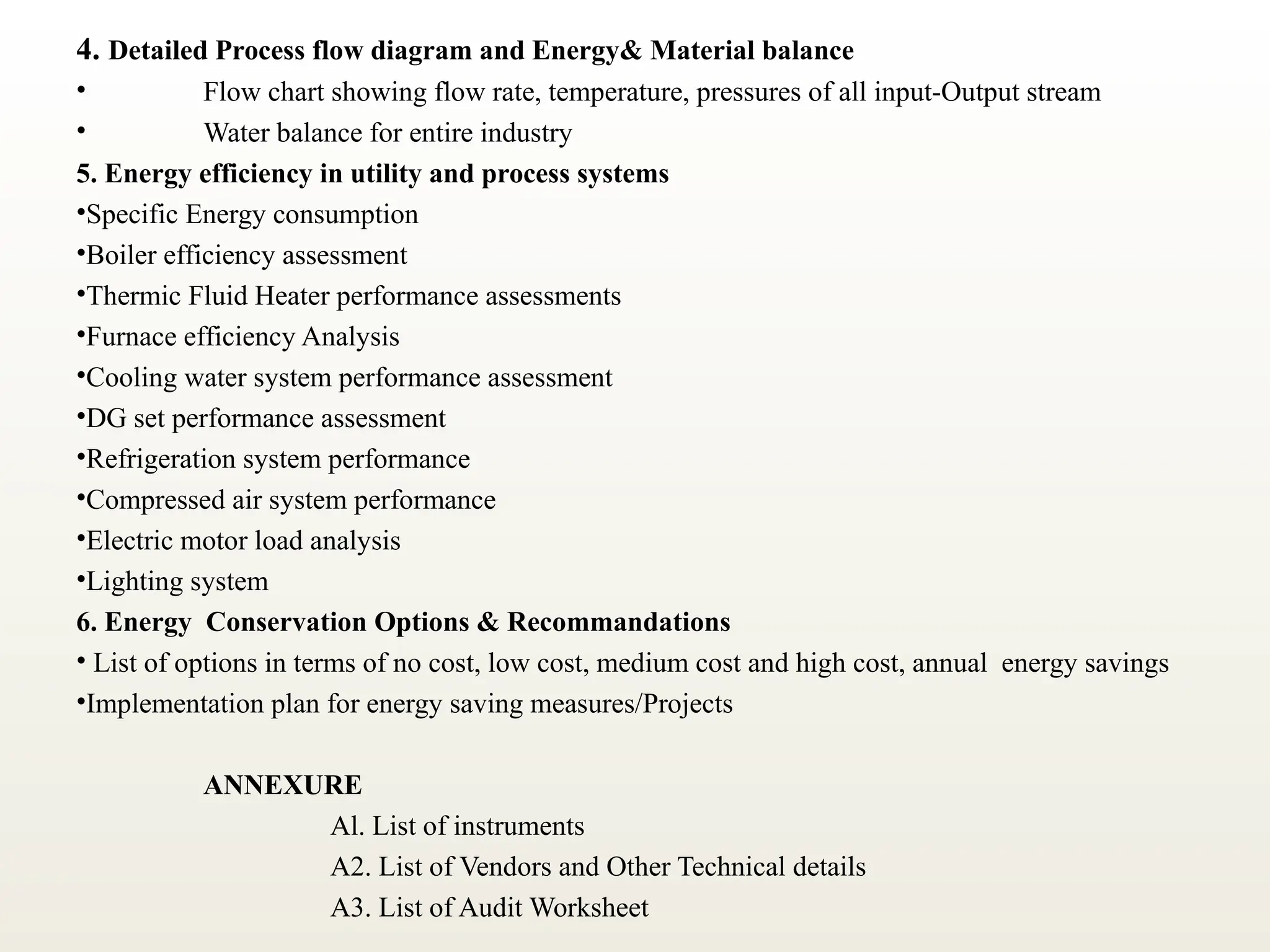

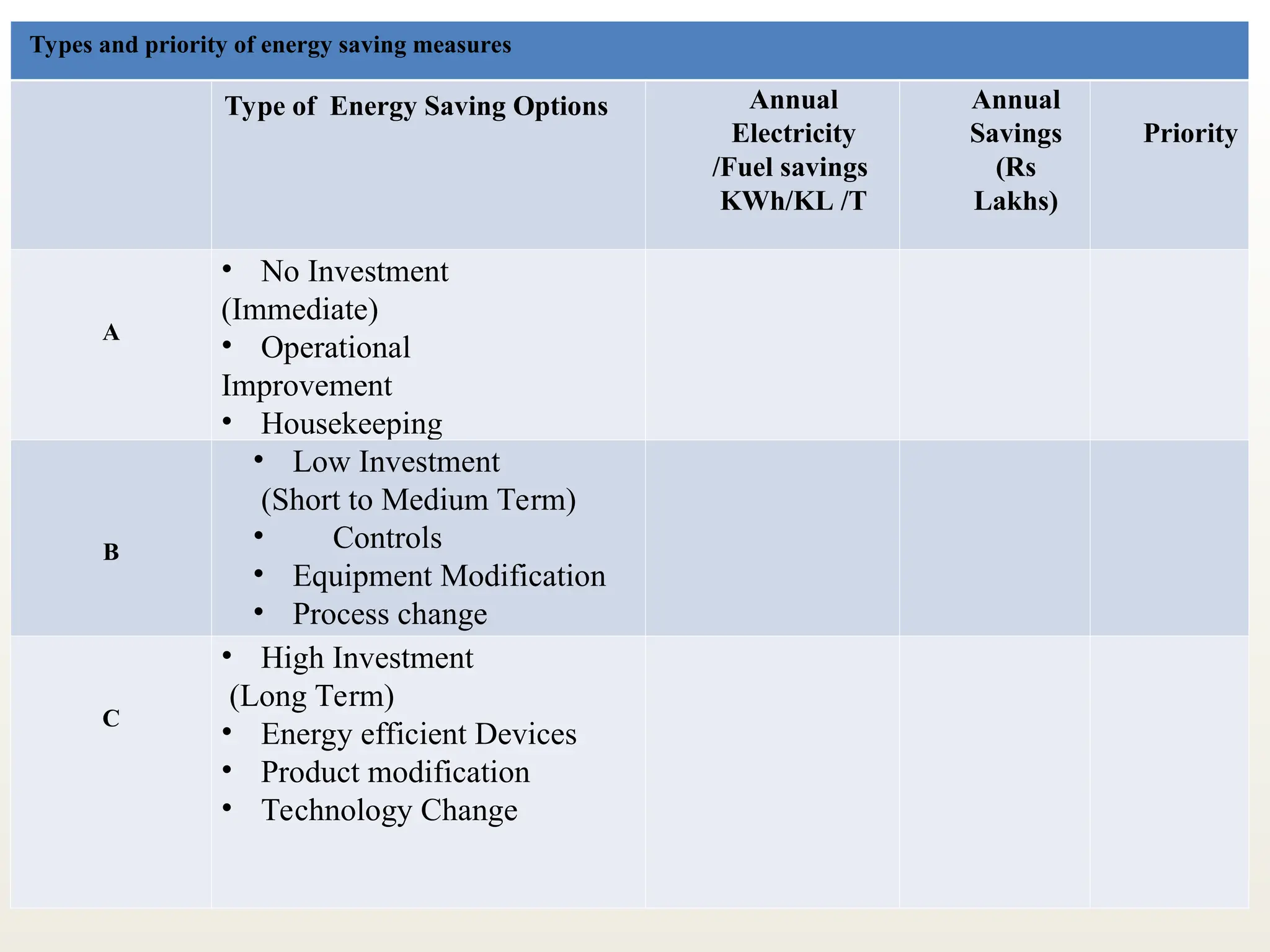

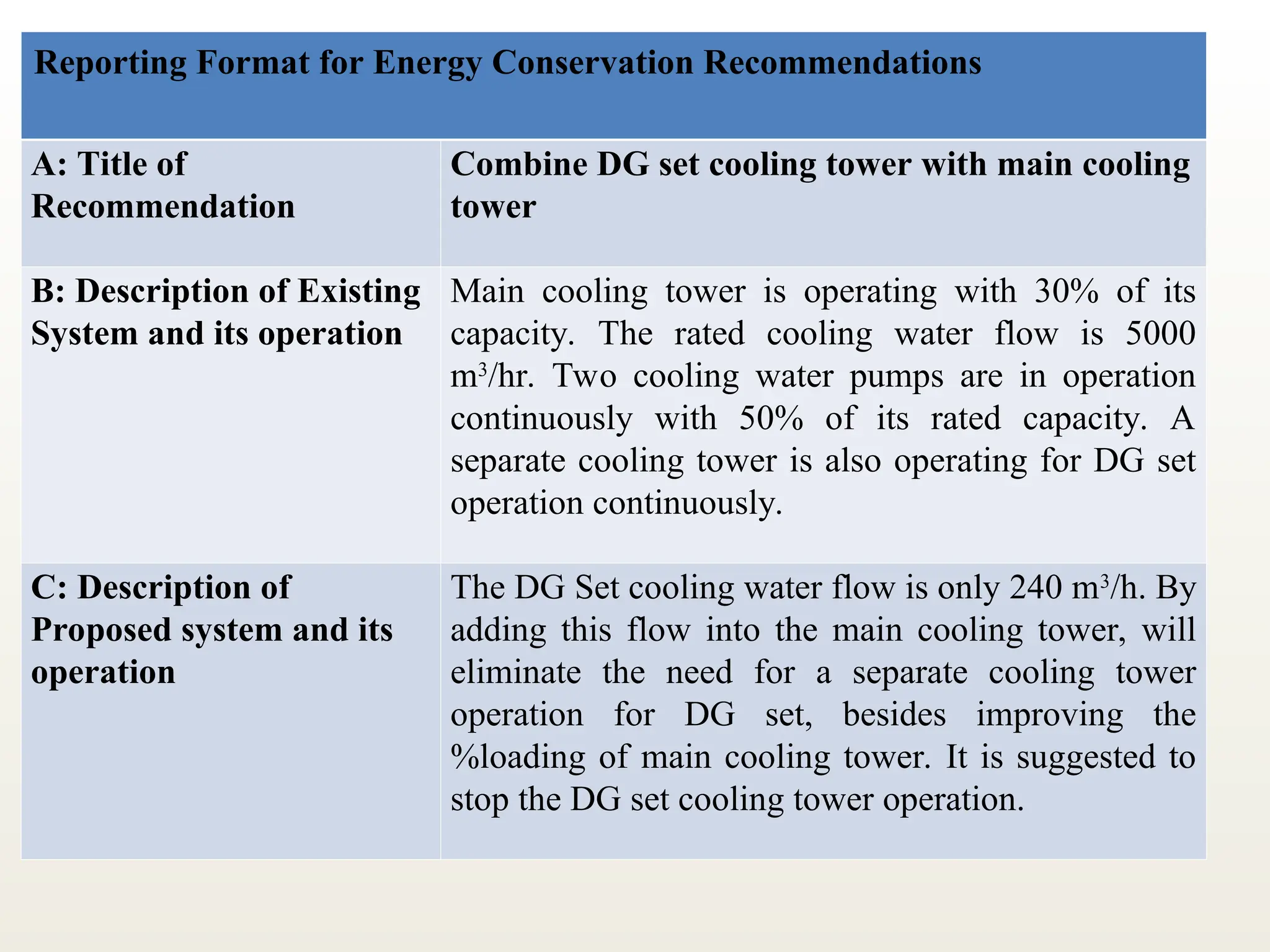

Energy audit reporting

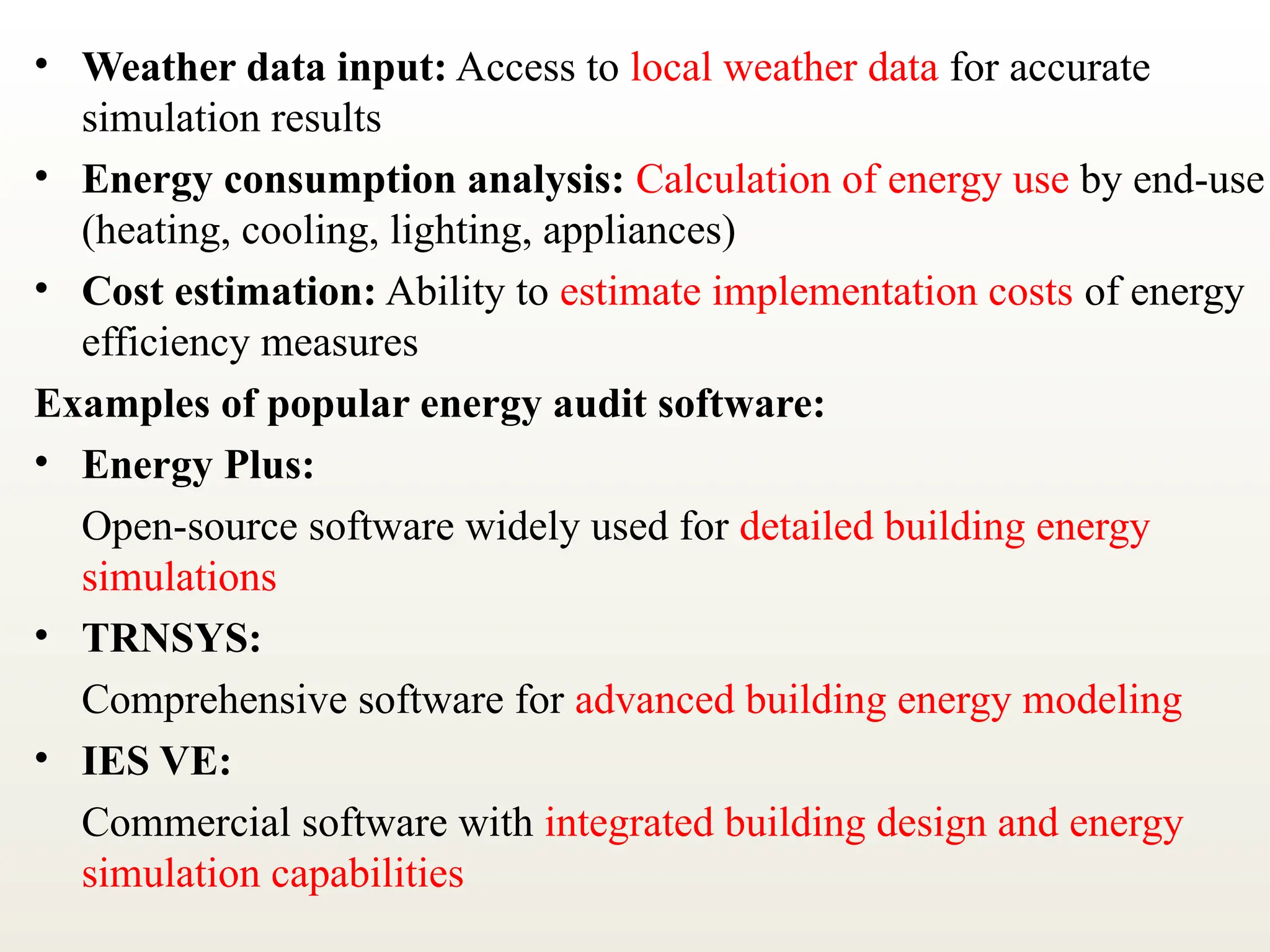

Introduction to software and simulation for energy auditing

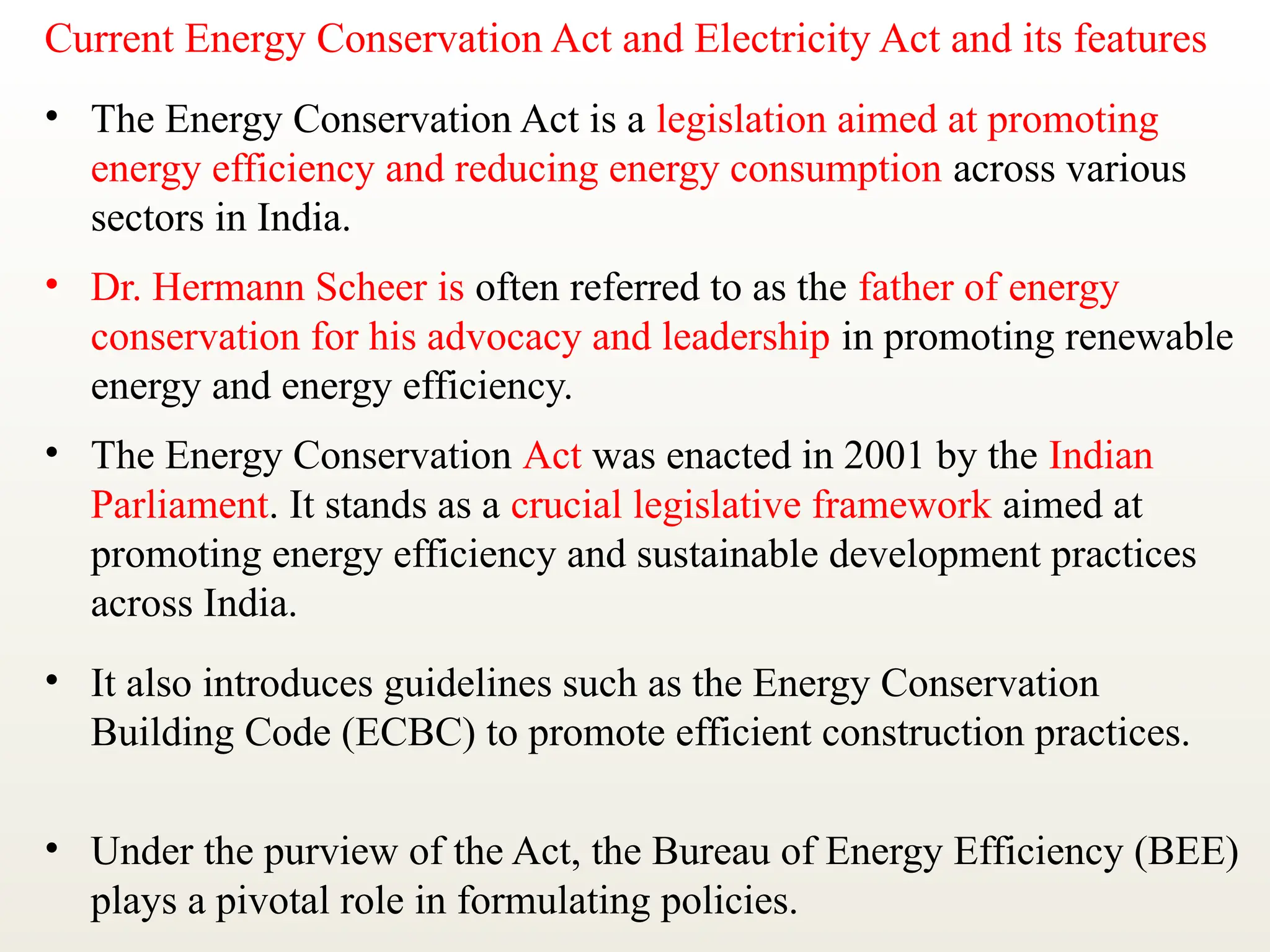

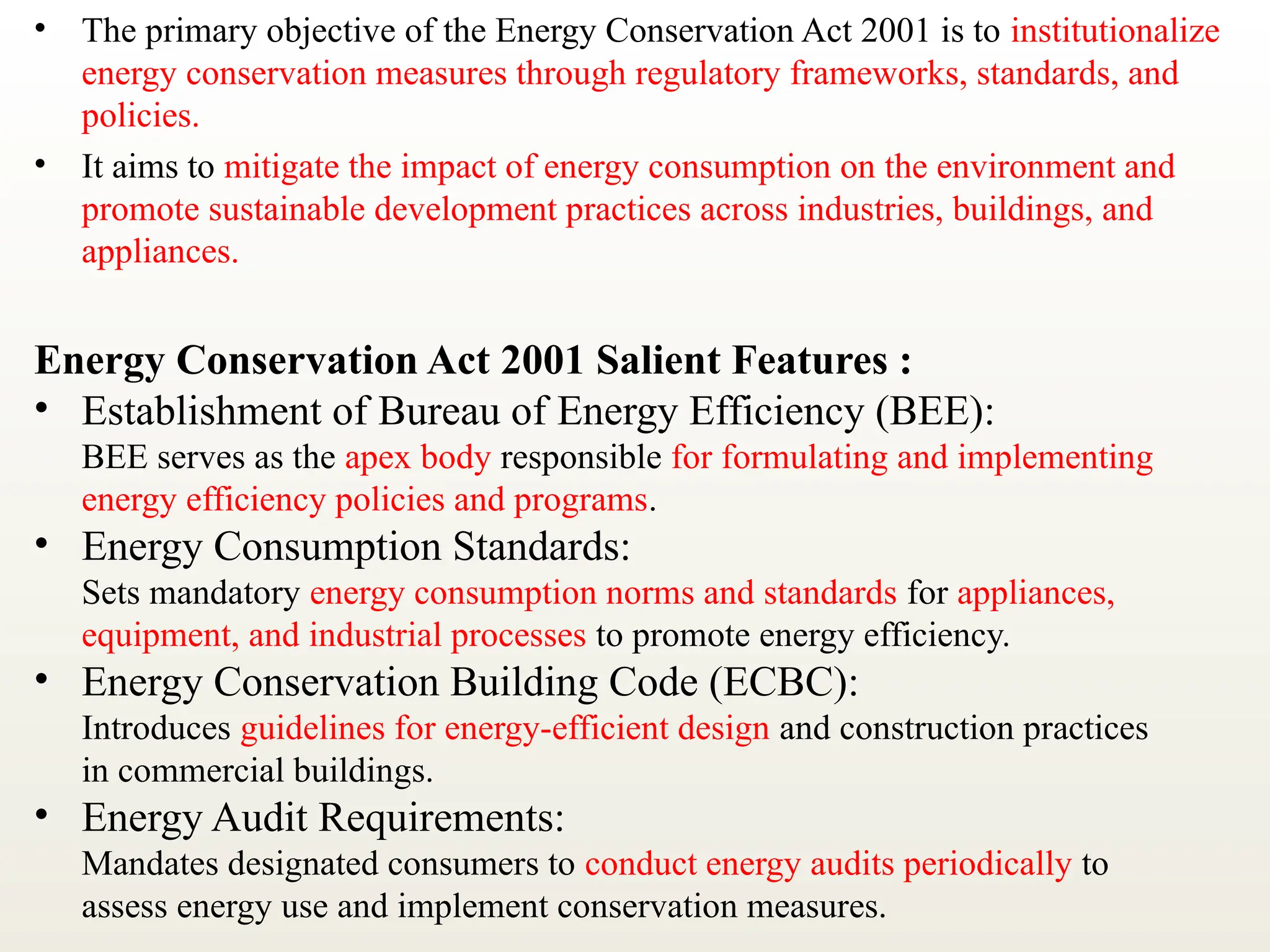

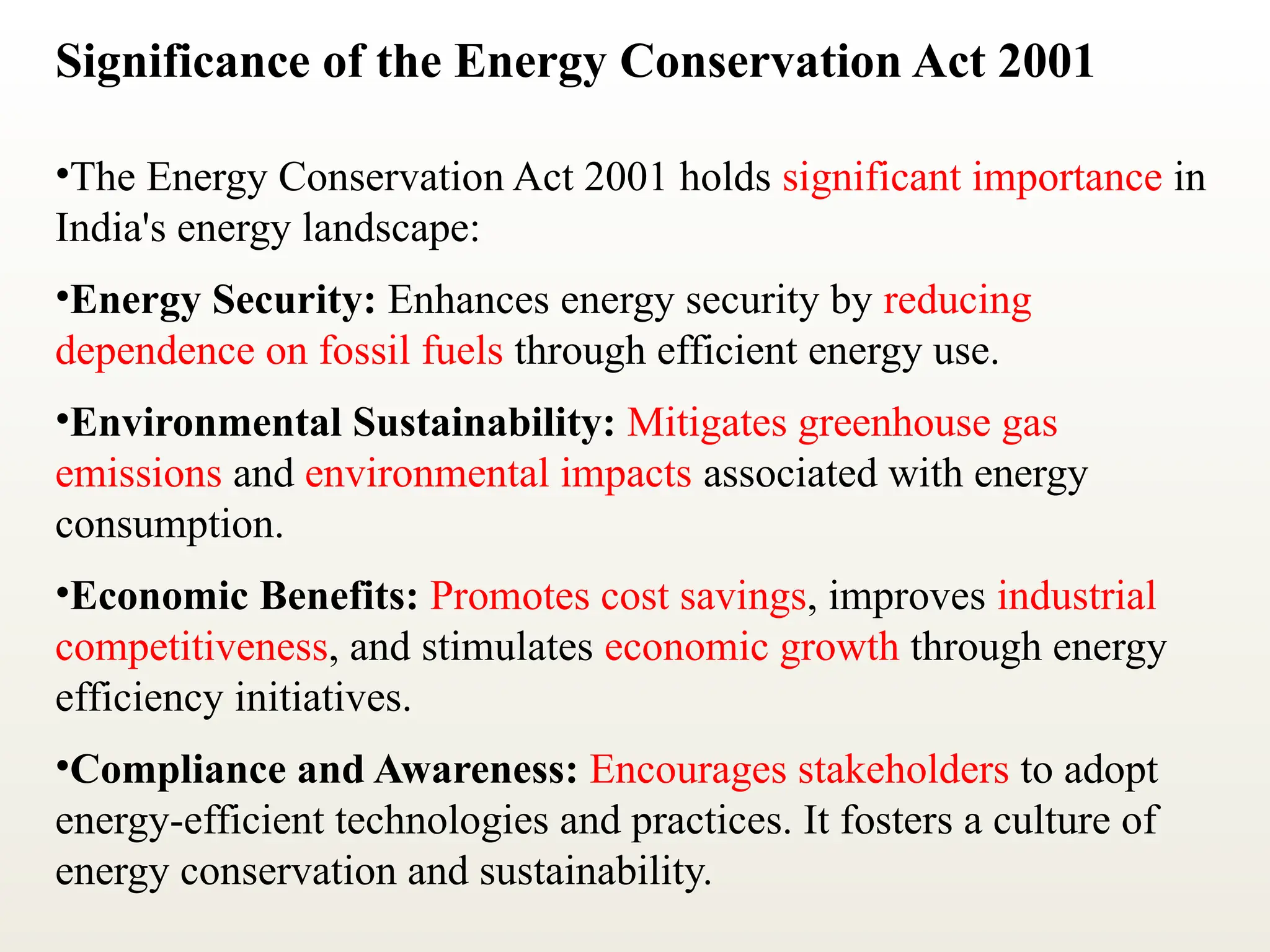

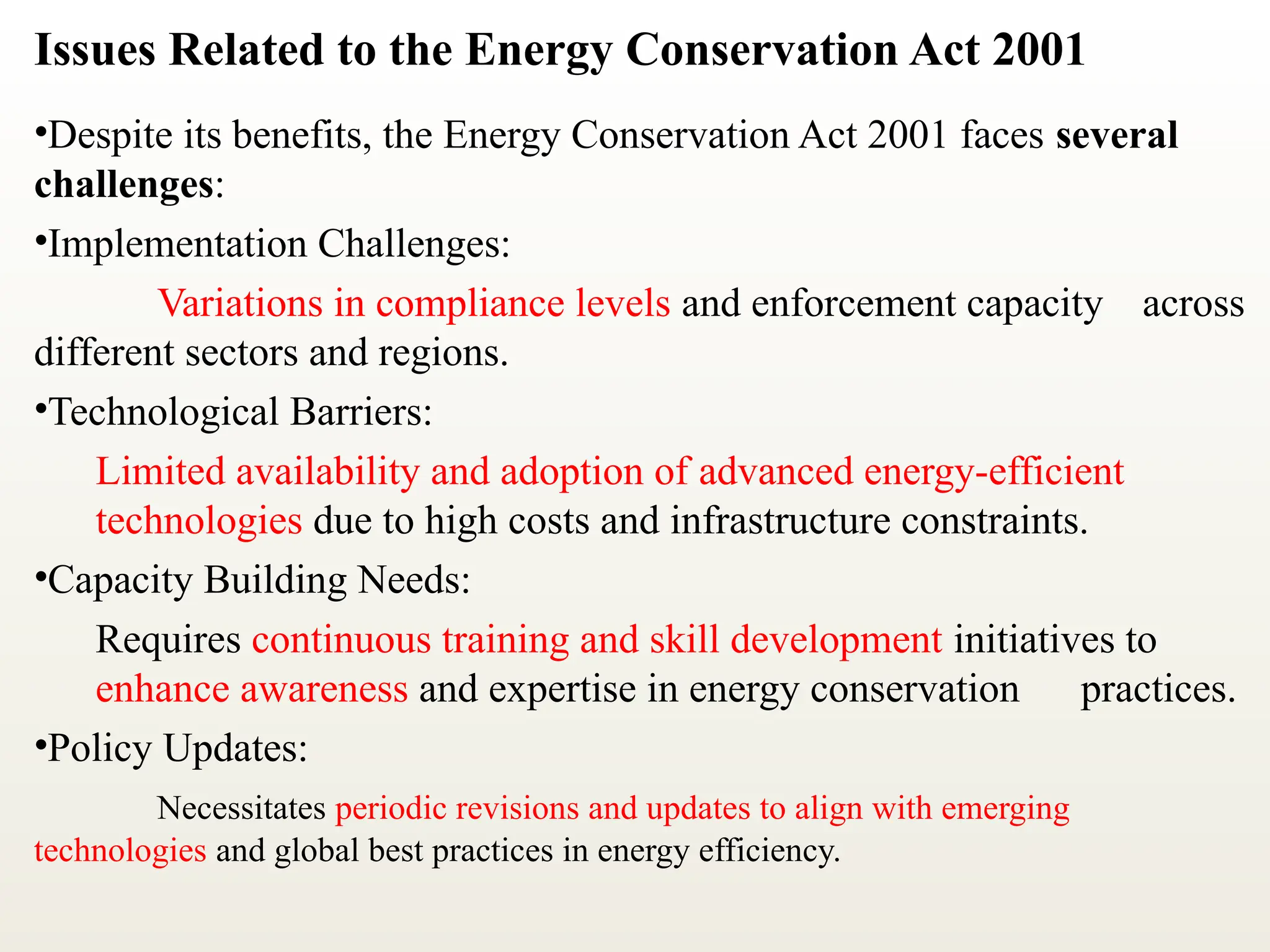

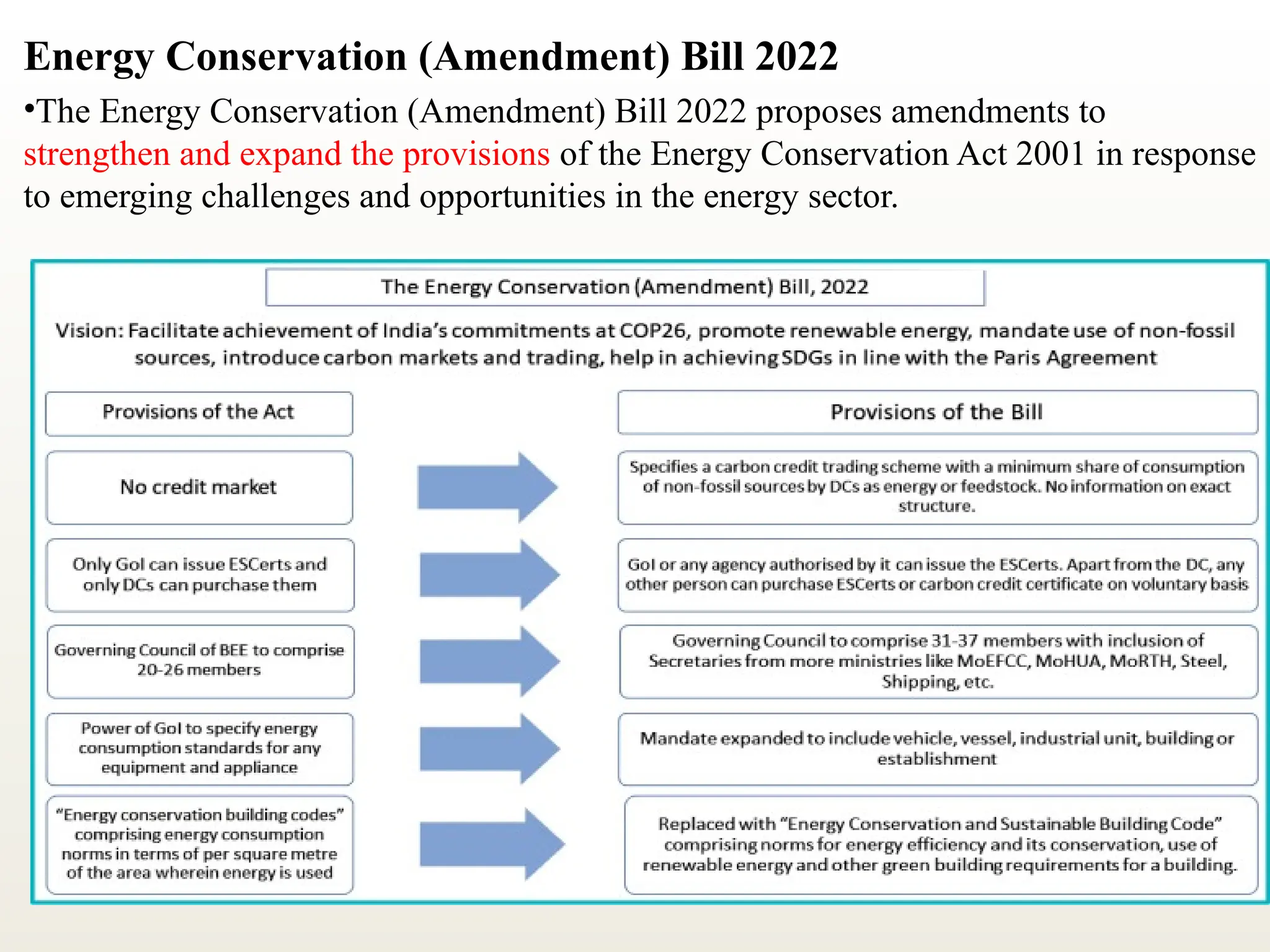

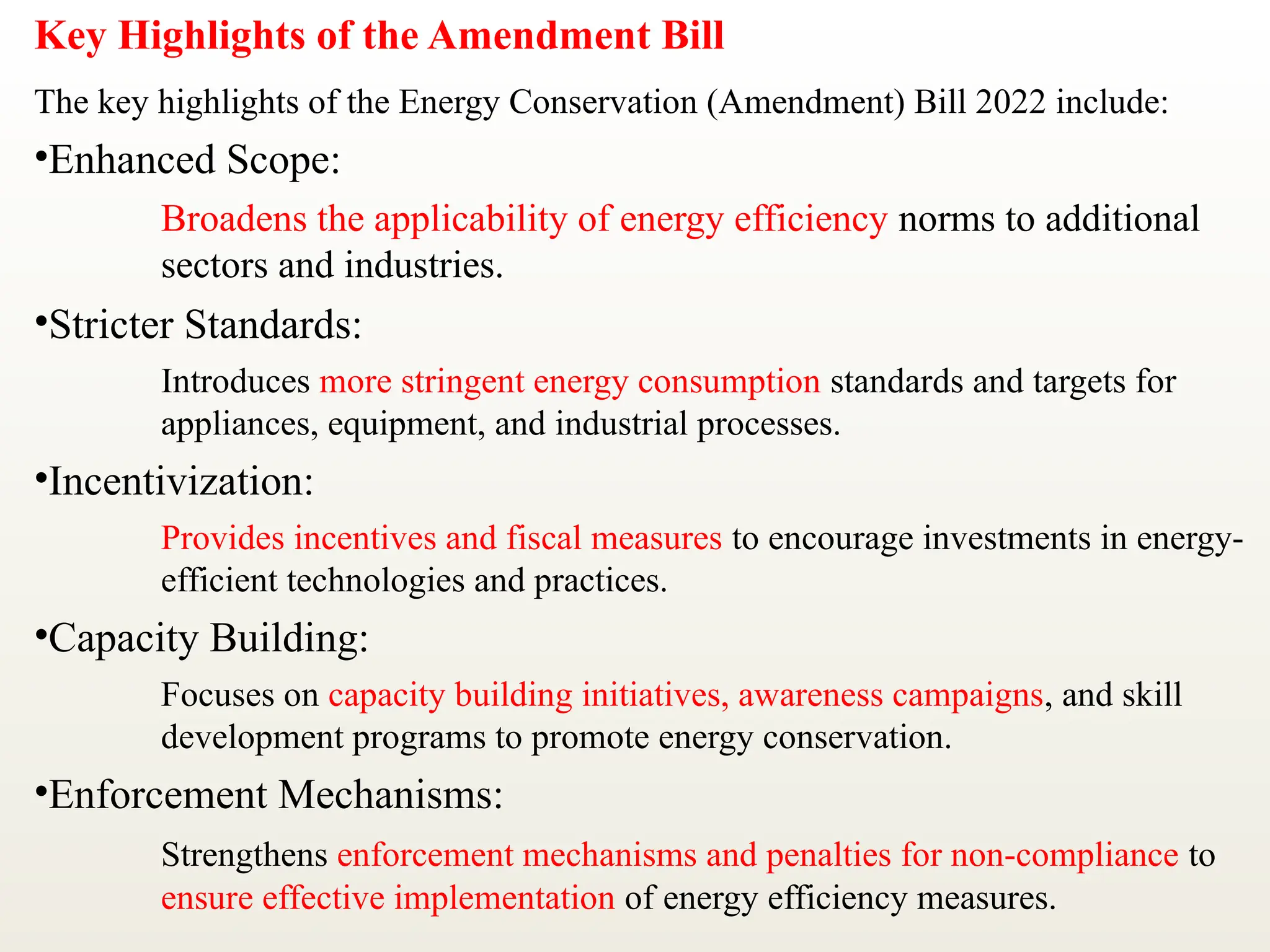

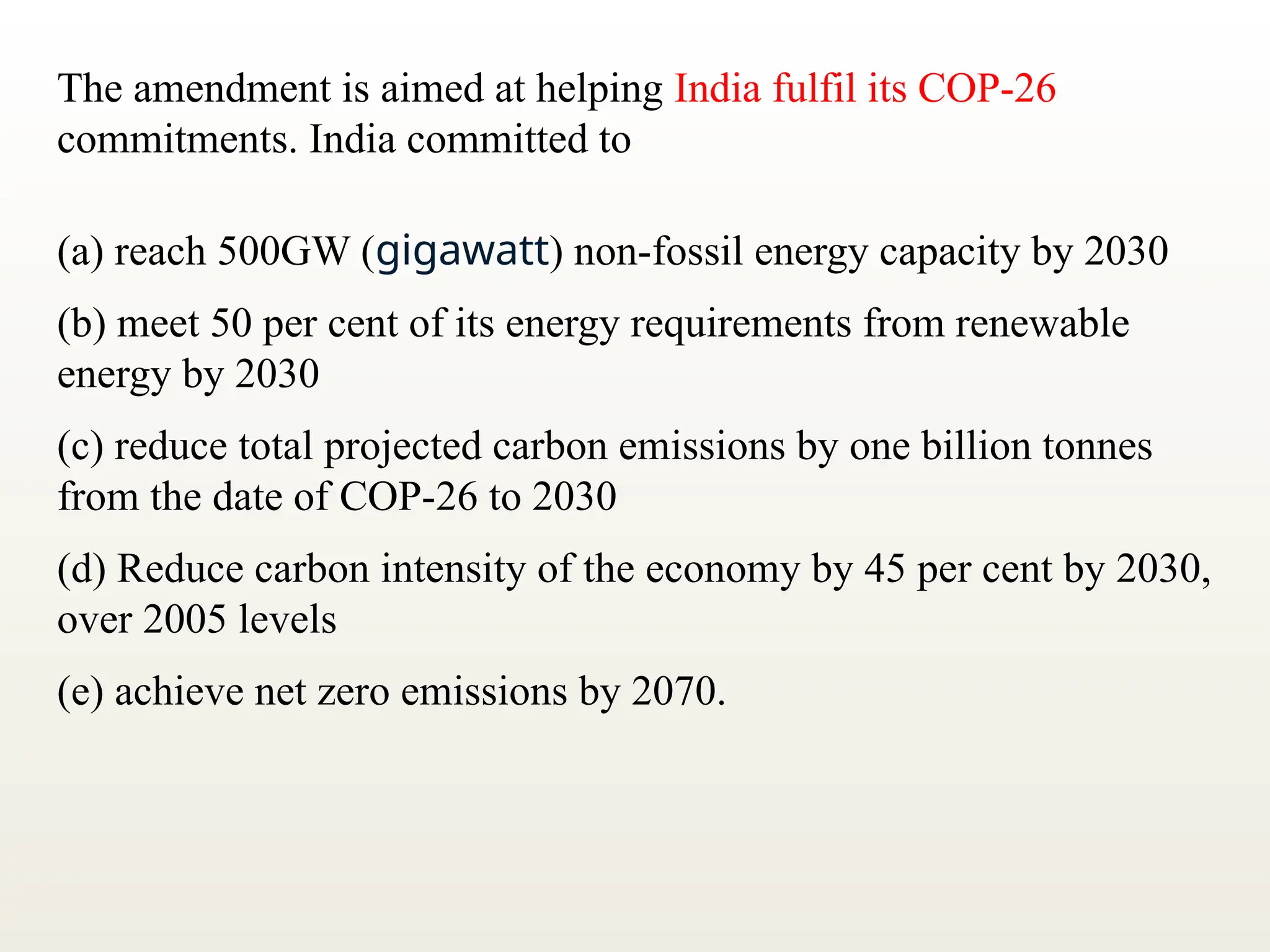

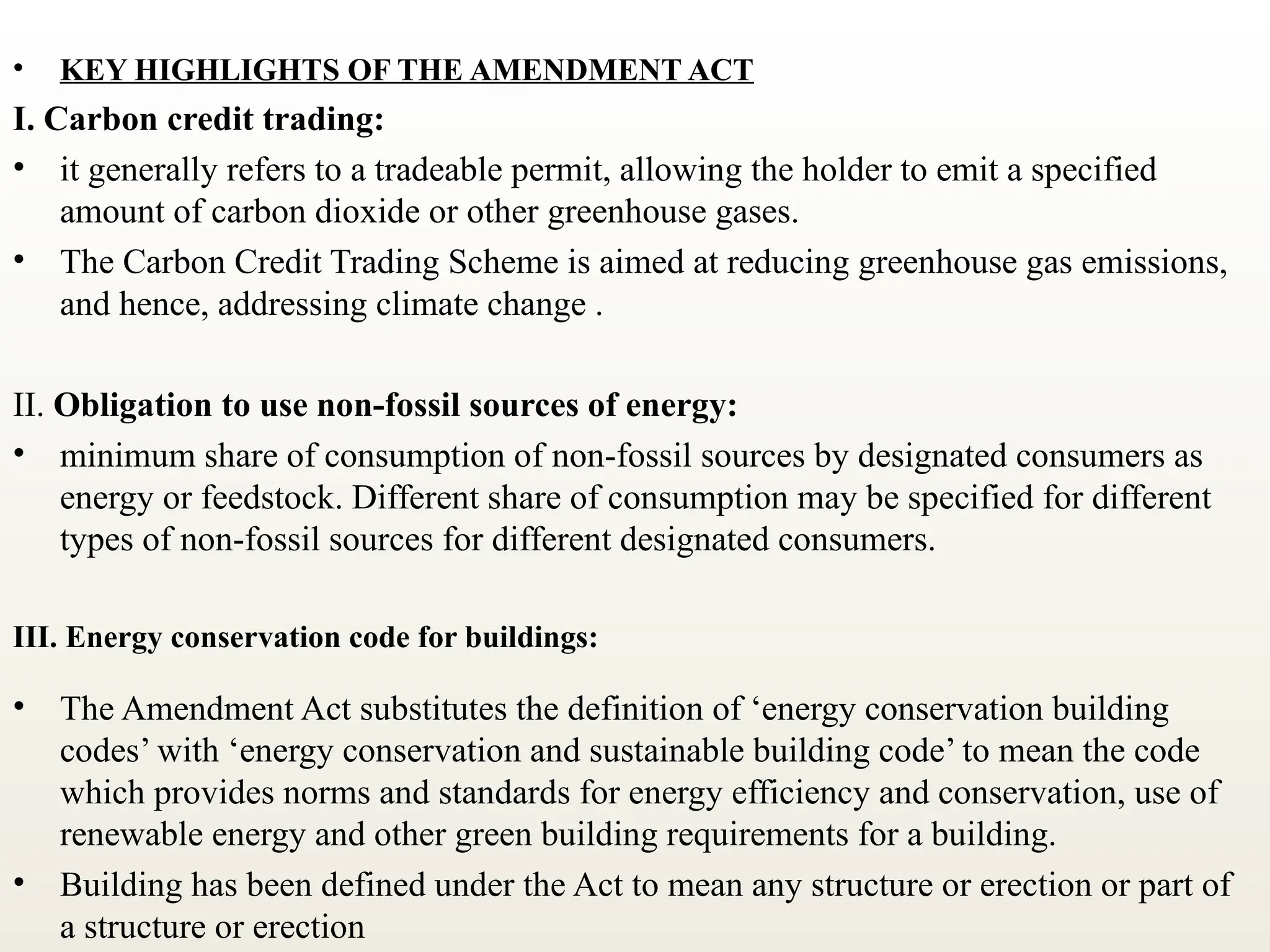

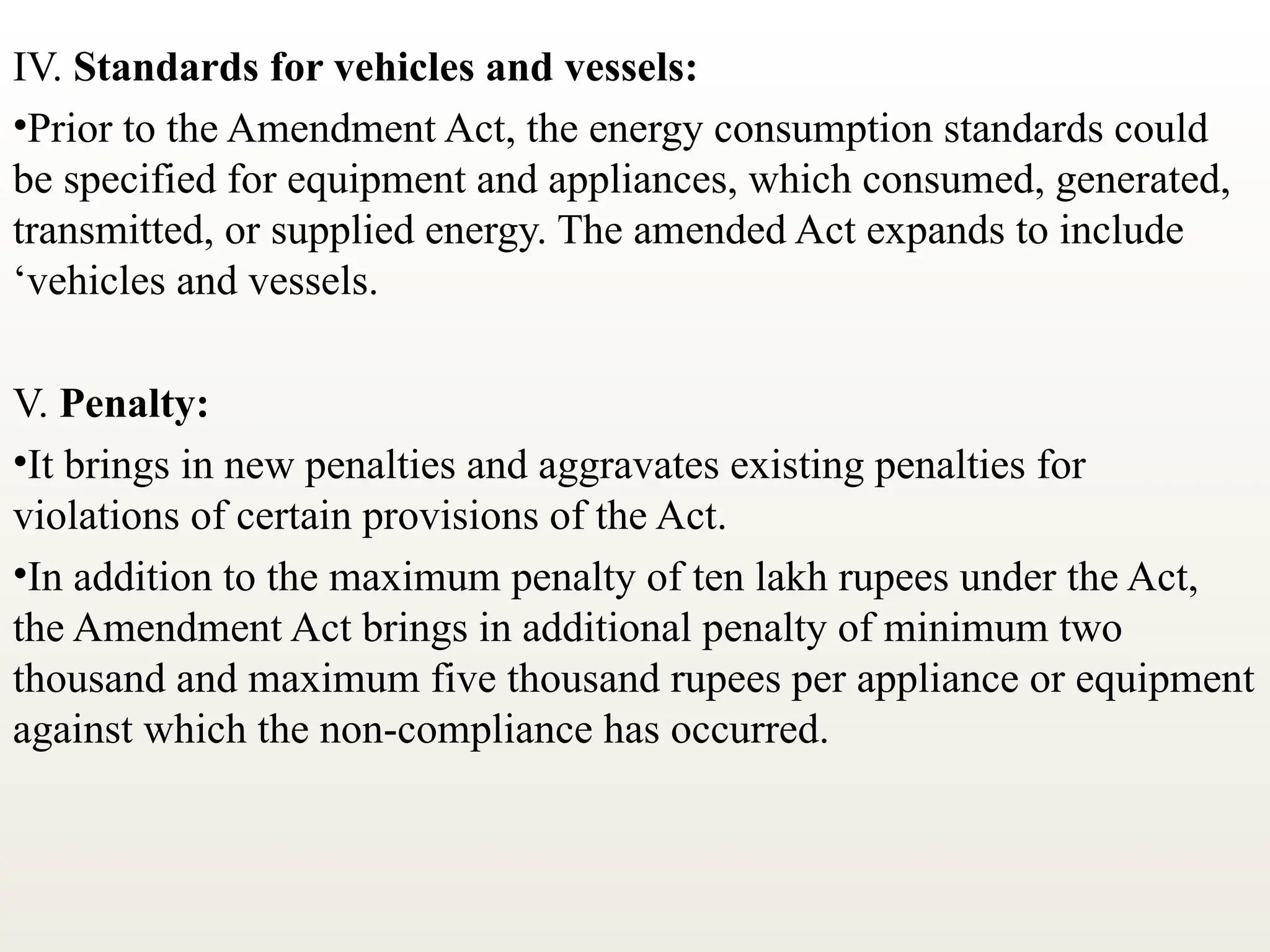

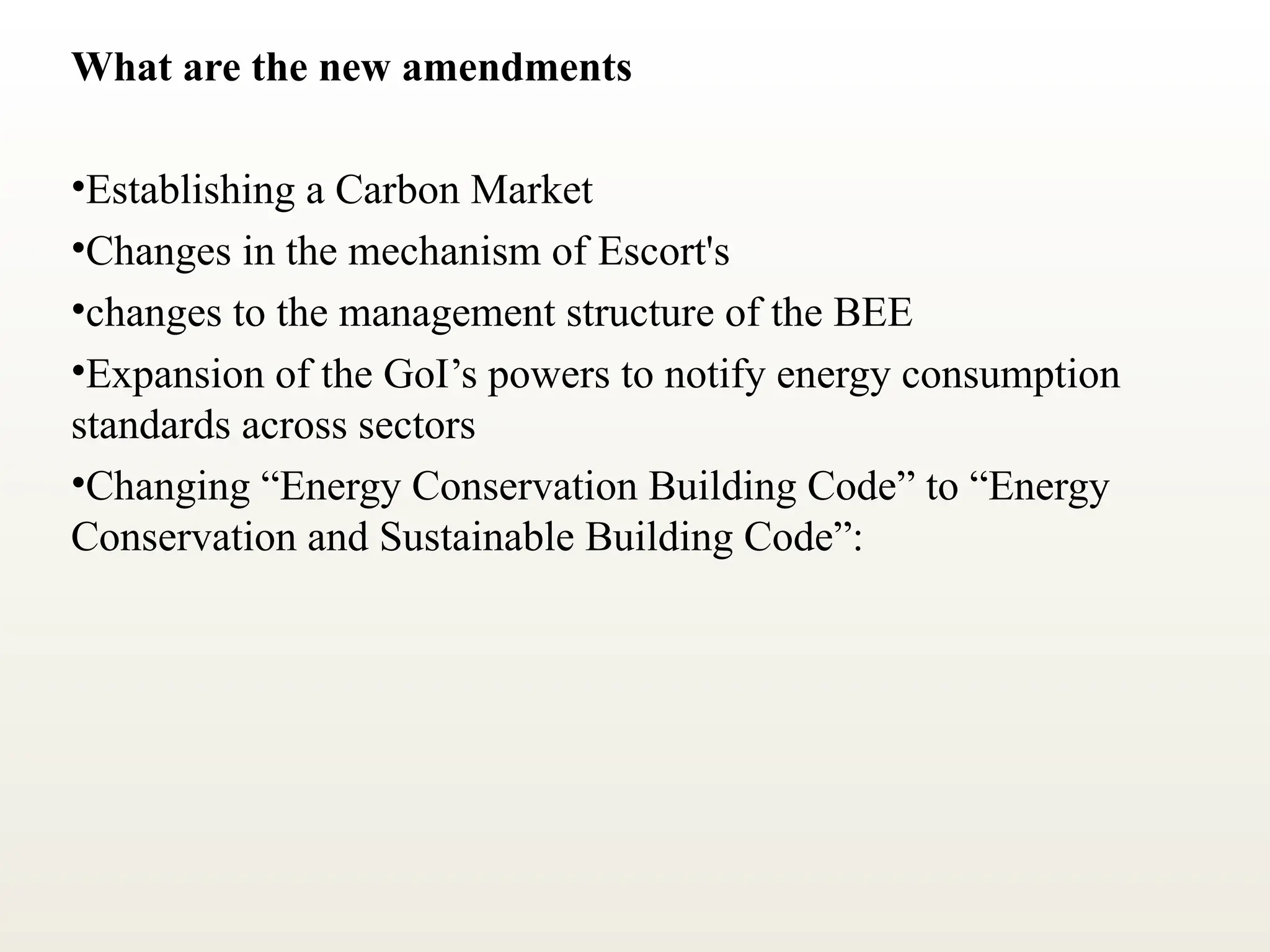

Current Energy Conservation Act and Electricity Act and its features