Download to read offline

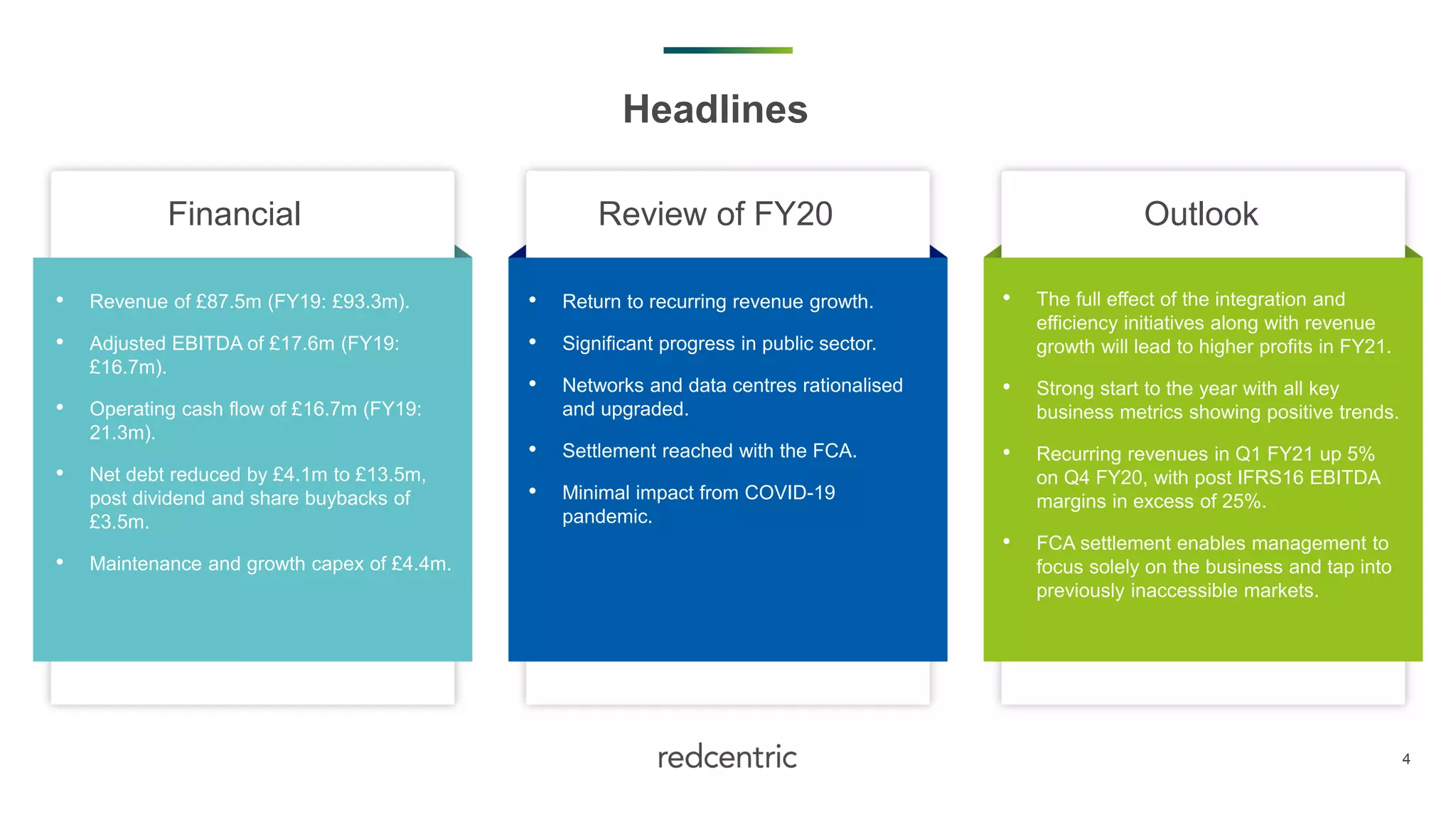

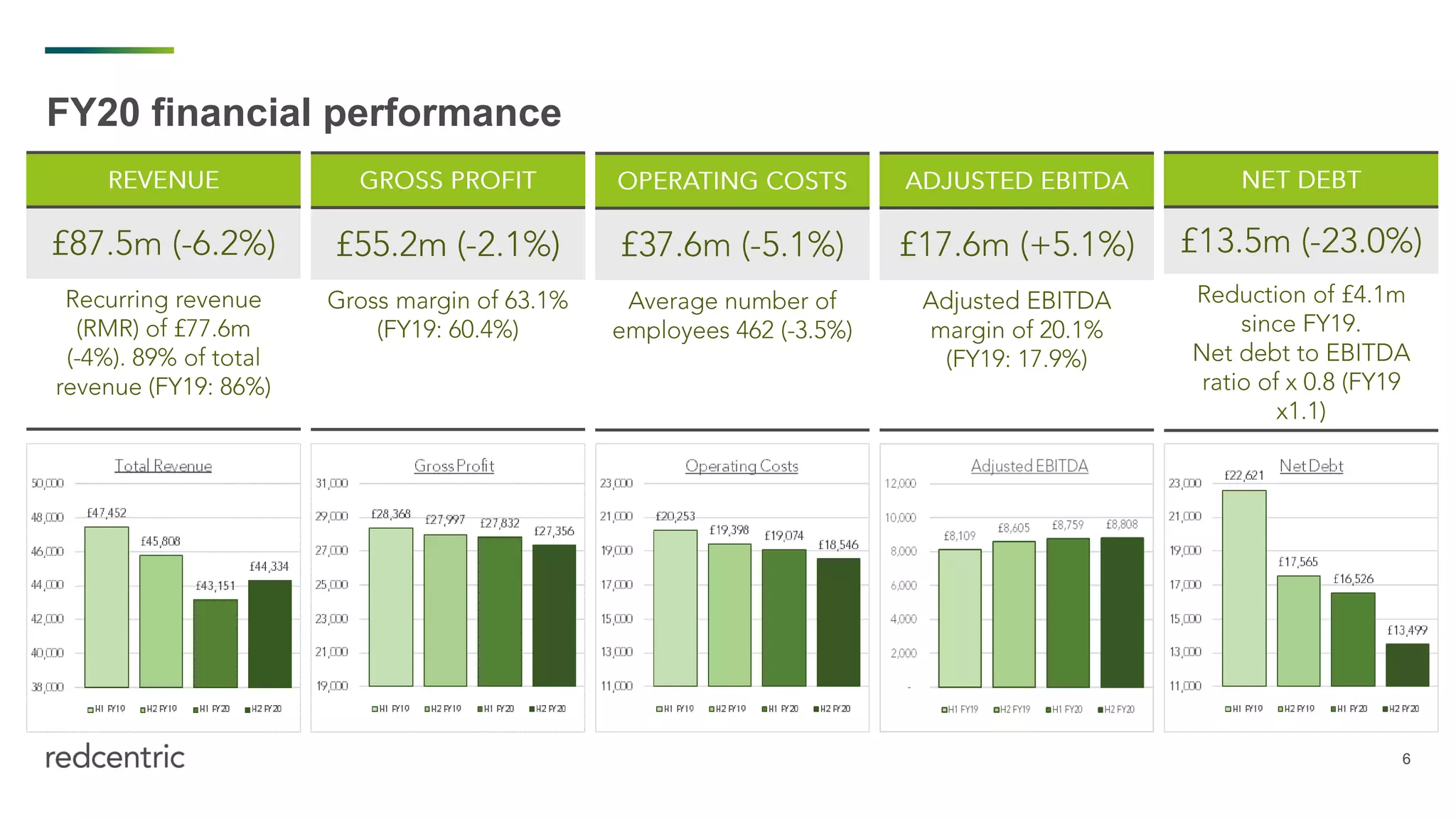

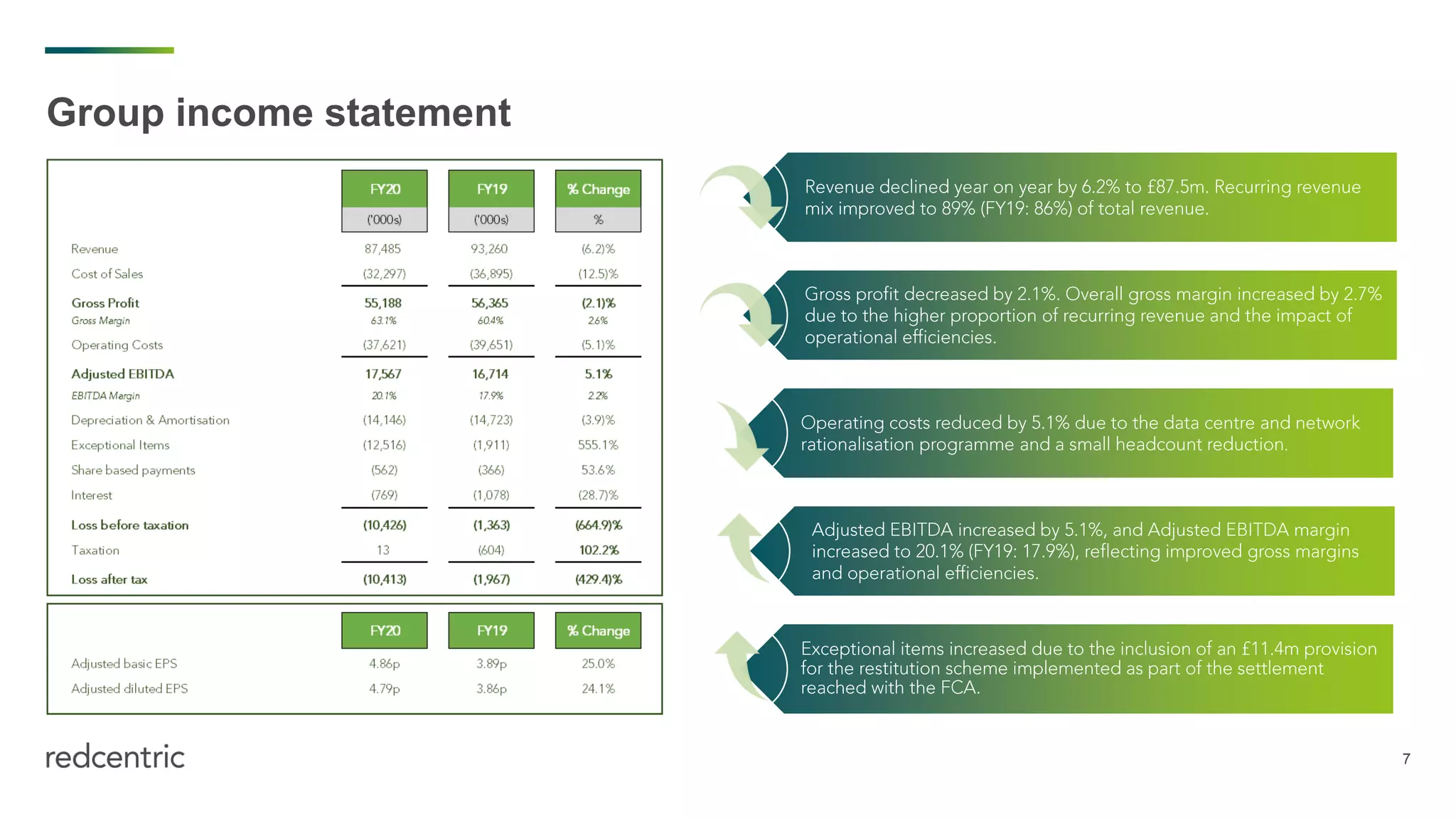

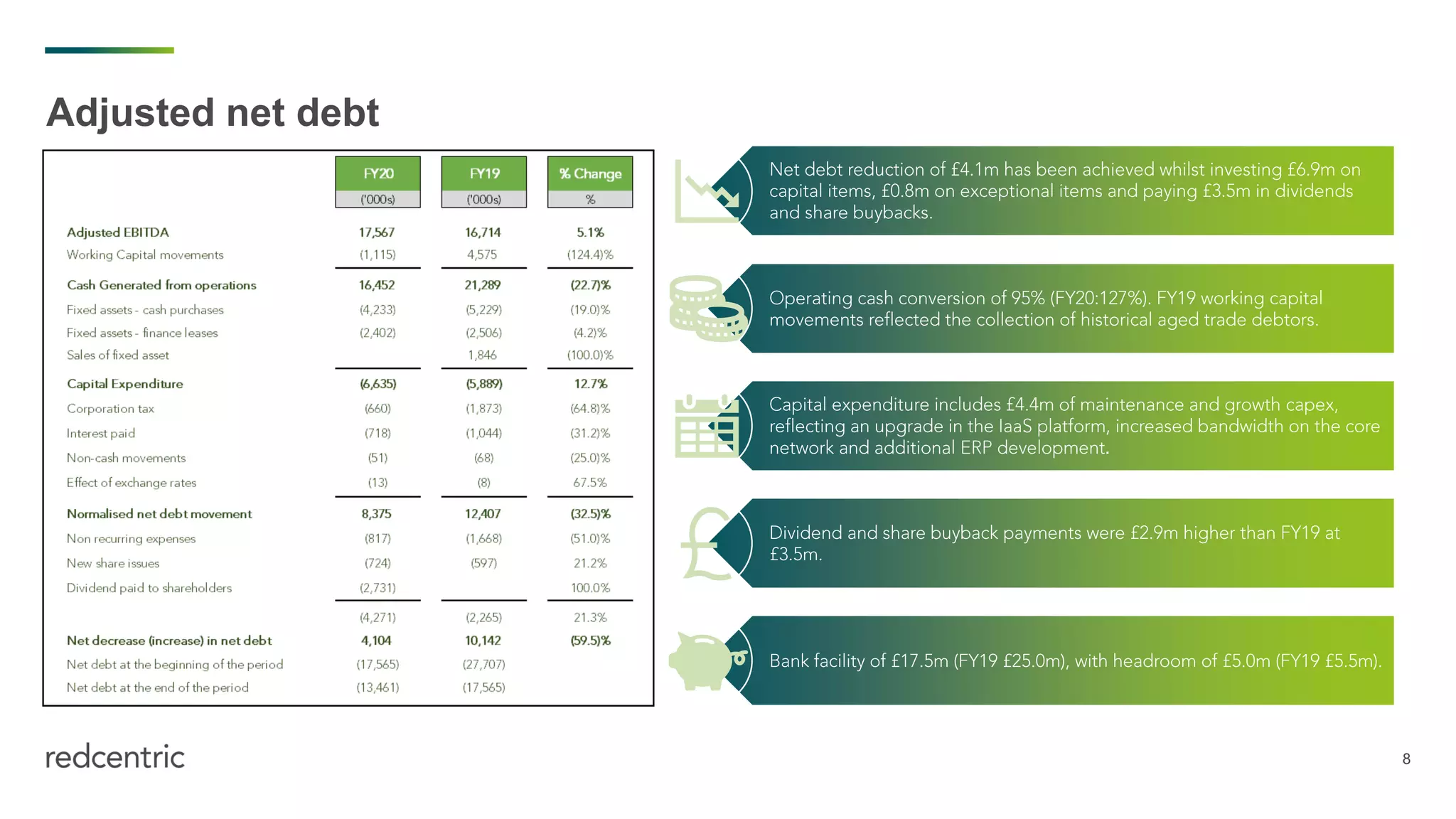

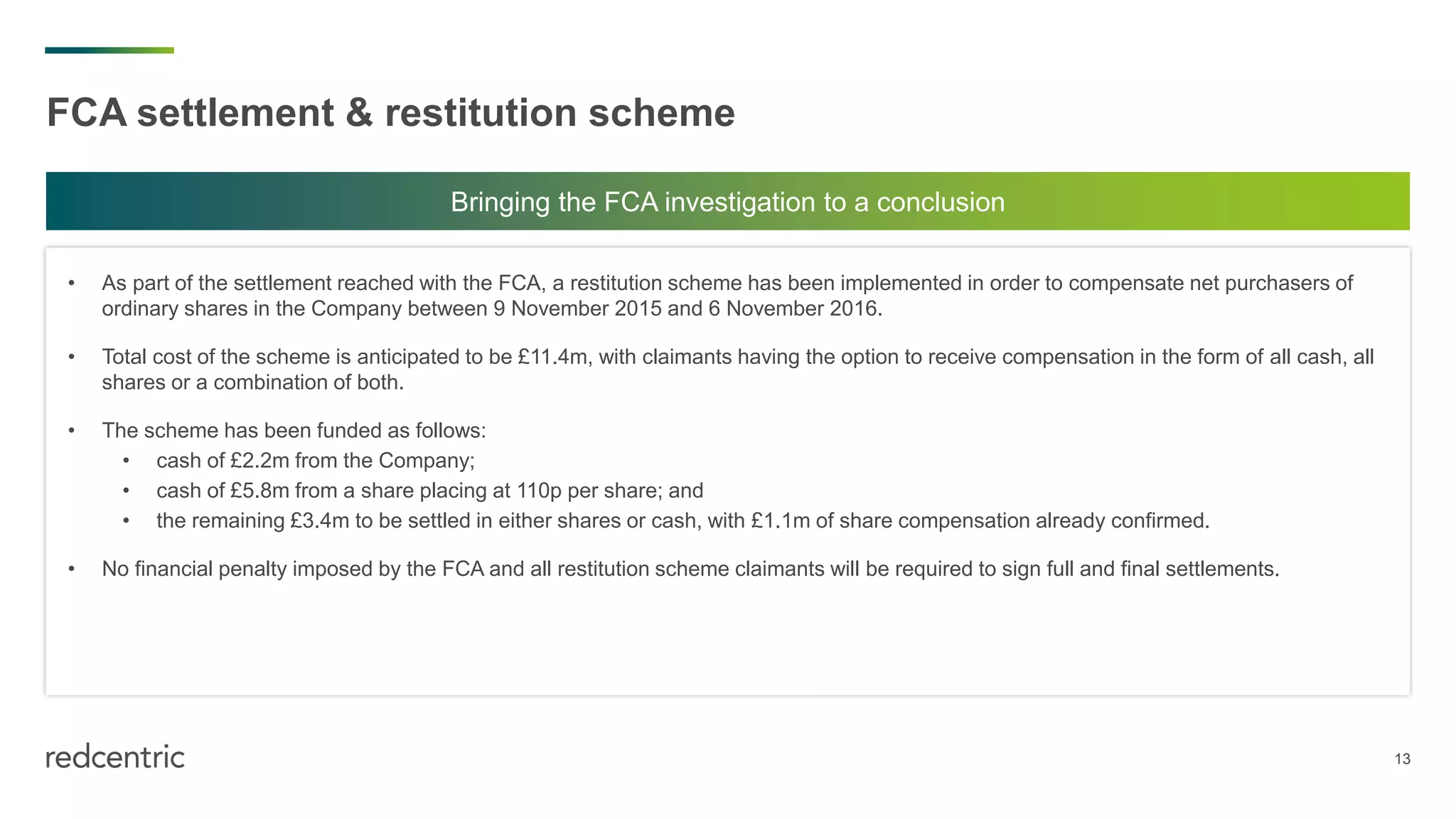

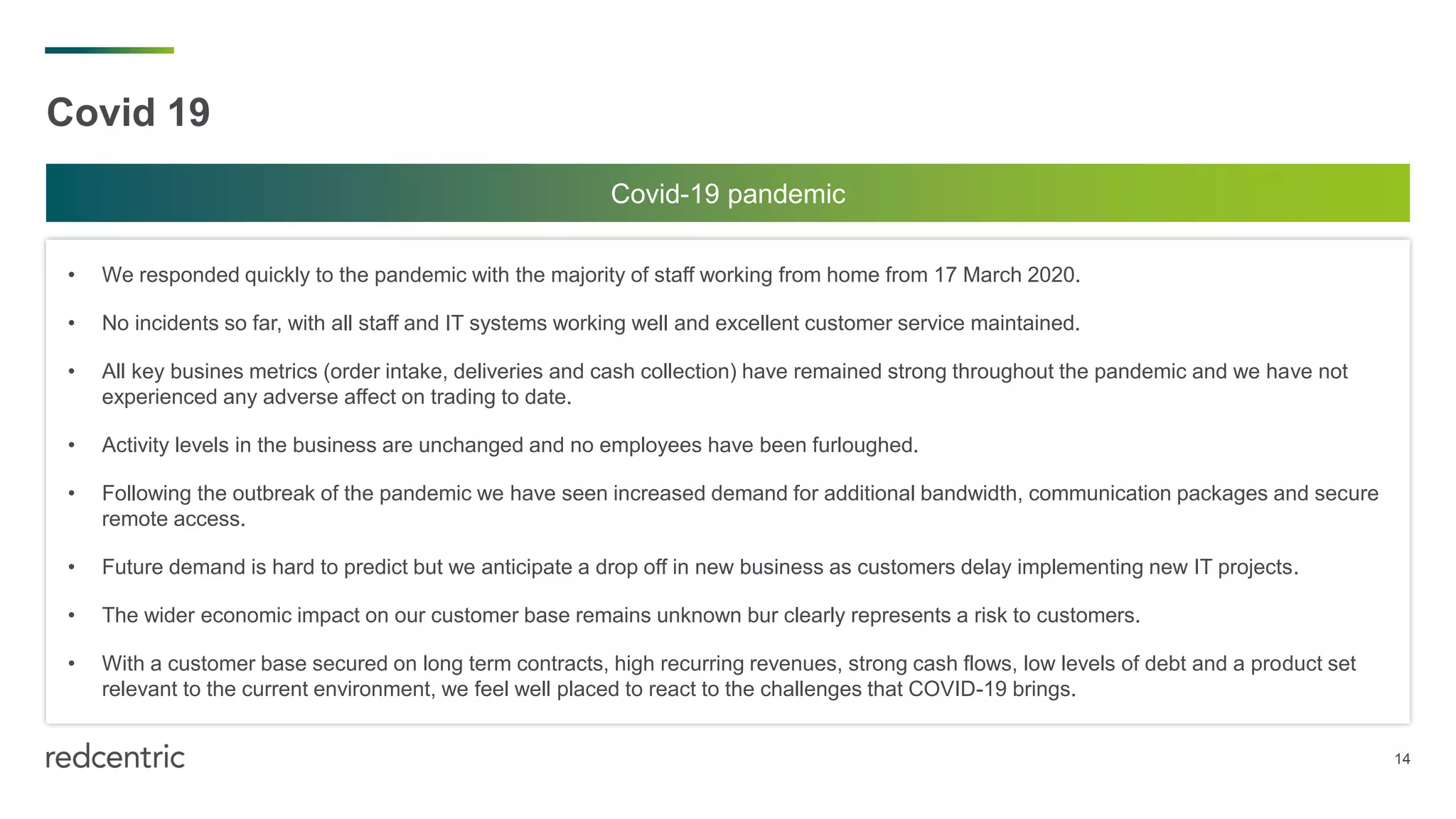

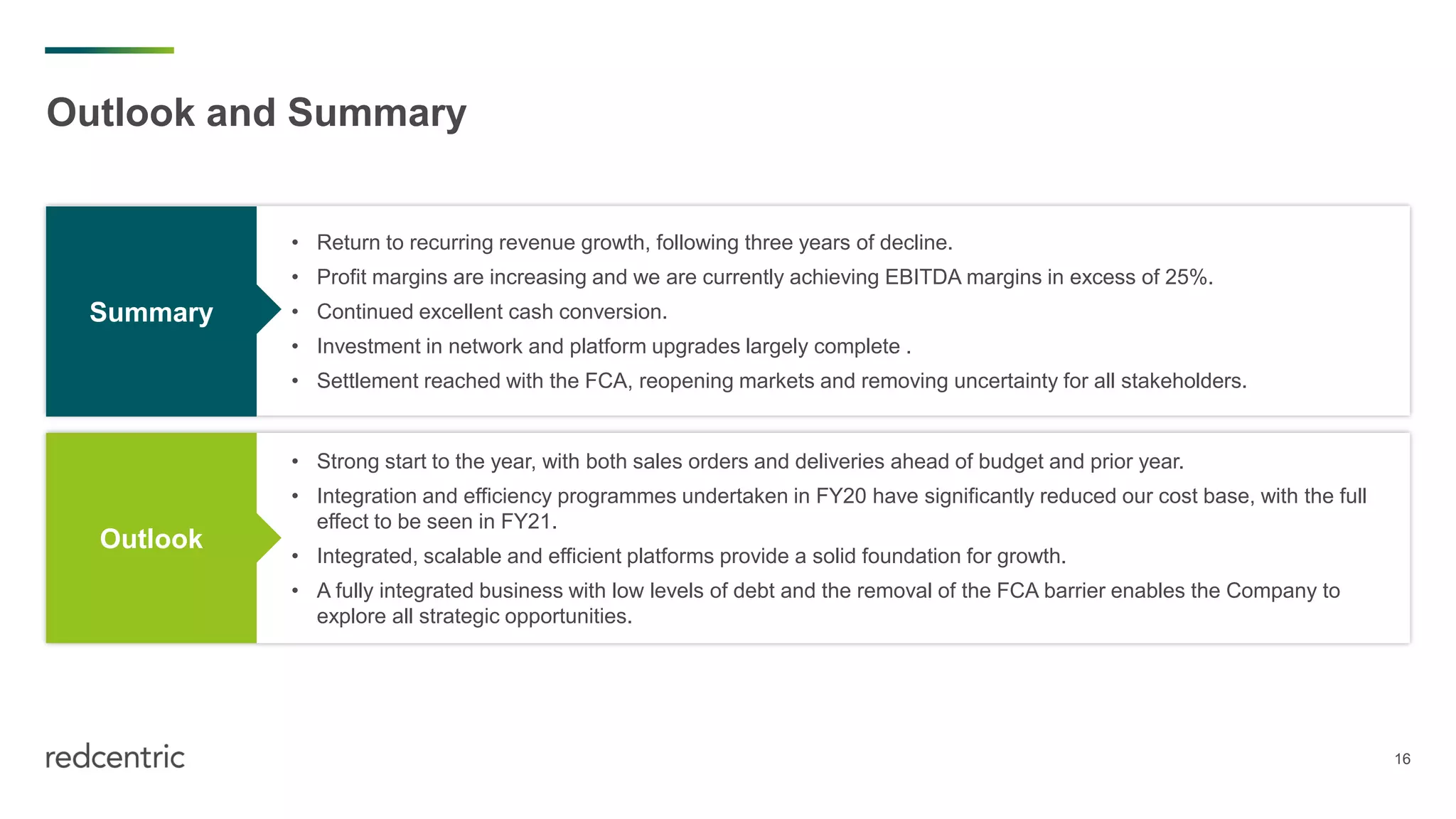

- Revenue for the year ended 31 March 2020 was £87.5 million, down 6% from the previous year. Adjusted EBITDA was £17.6 million, up 5% from the previous year. - Operational efficiencies and network upgrades were completed during the year to improve margins. Recurring revenues returned to growth in the second half after declines in previous years. - A settlement was reached with the FCA regarding past conduct, to be funded with £11.4 million to compensate shareholders. Minimal financial impact was seen from the COVID-19 pandemic.