Downloaded 552 times

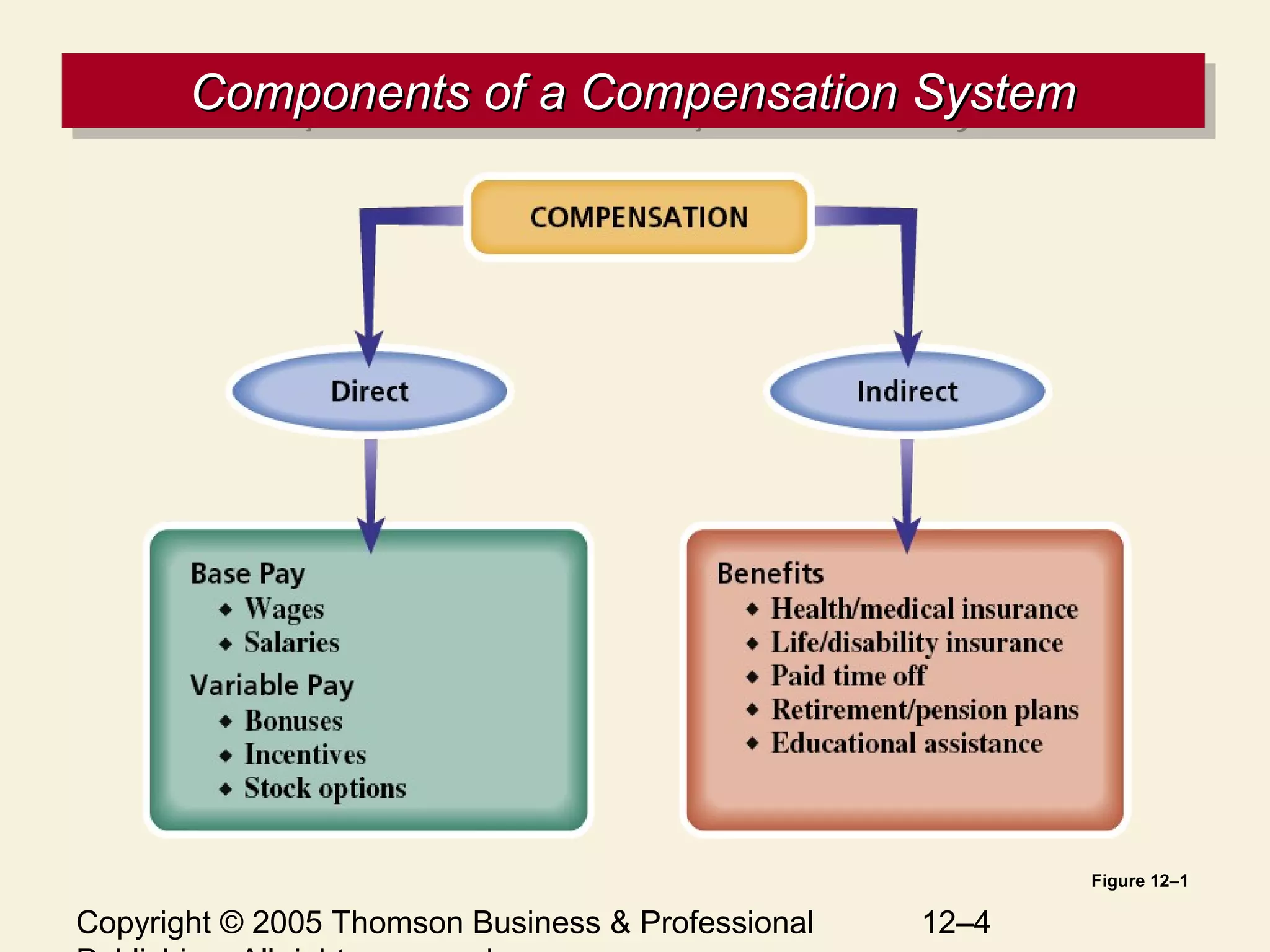

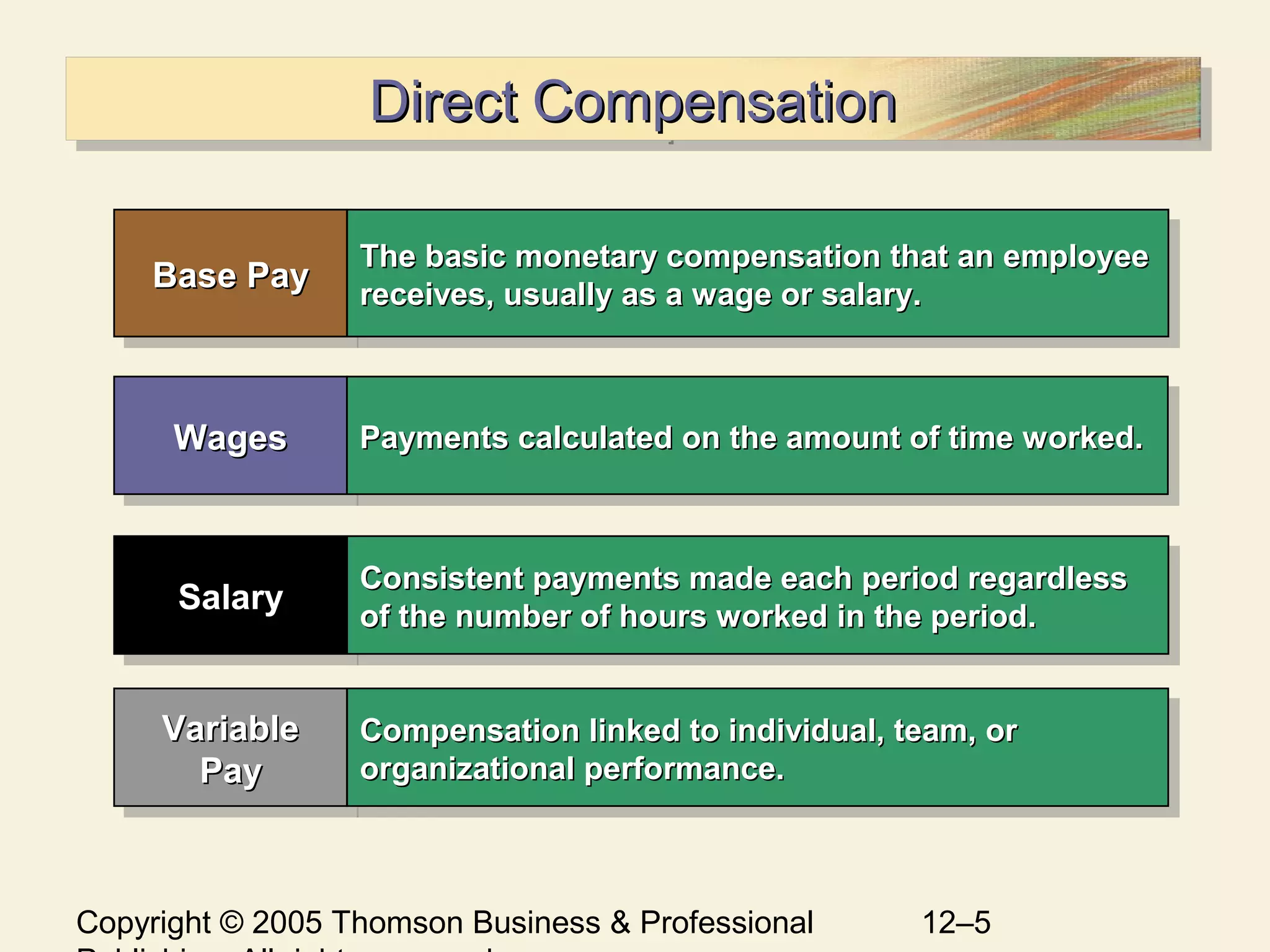

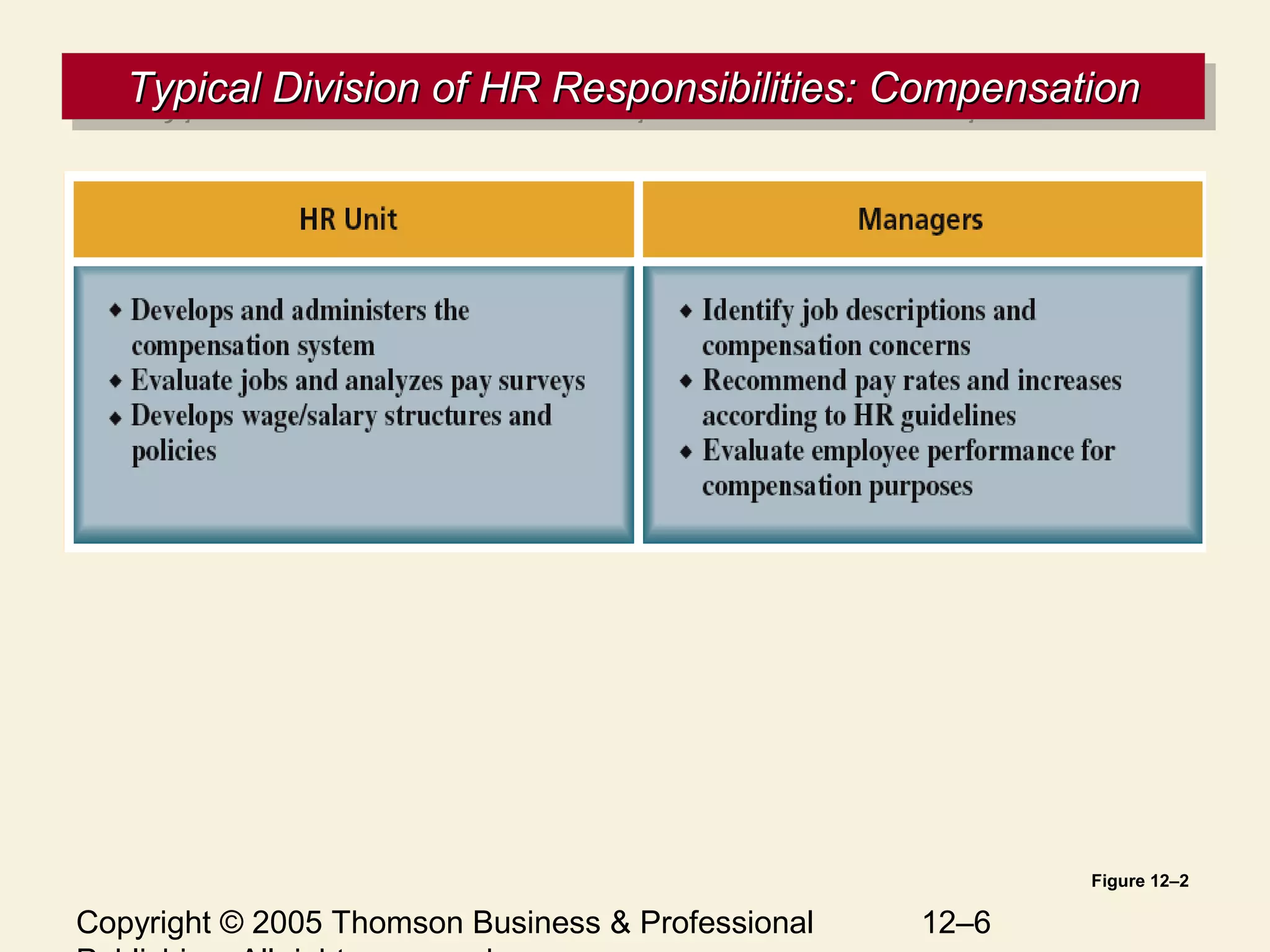

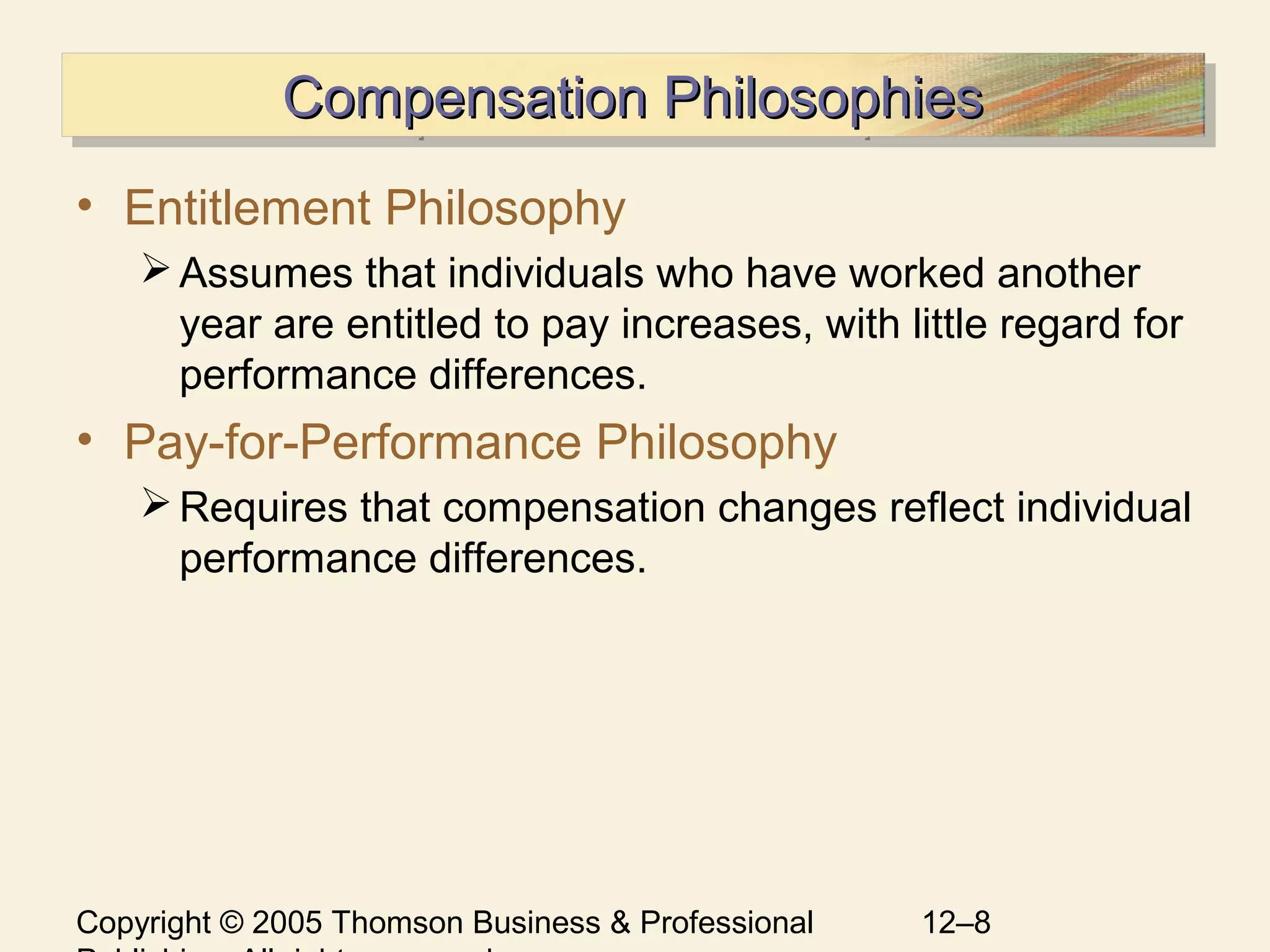

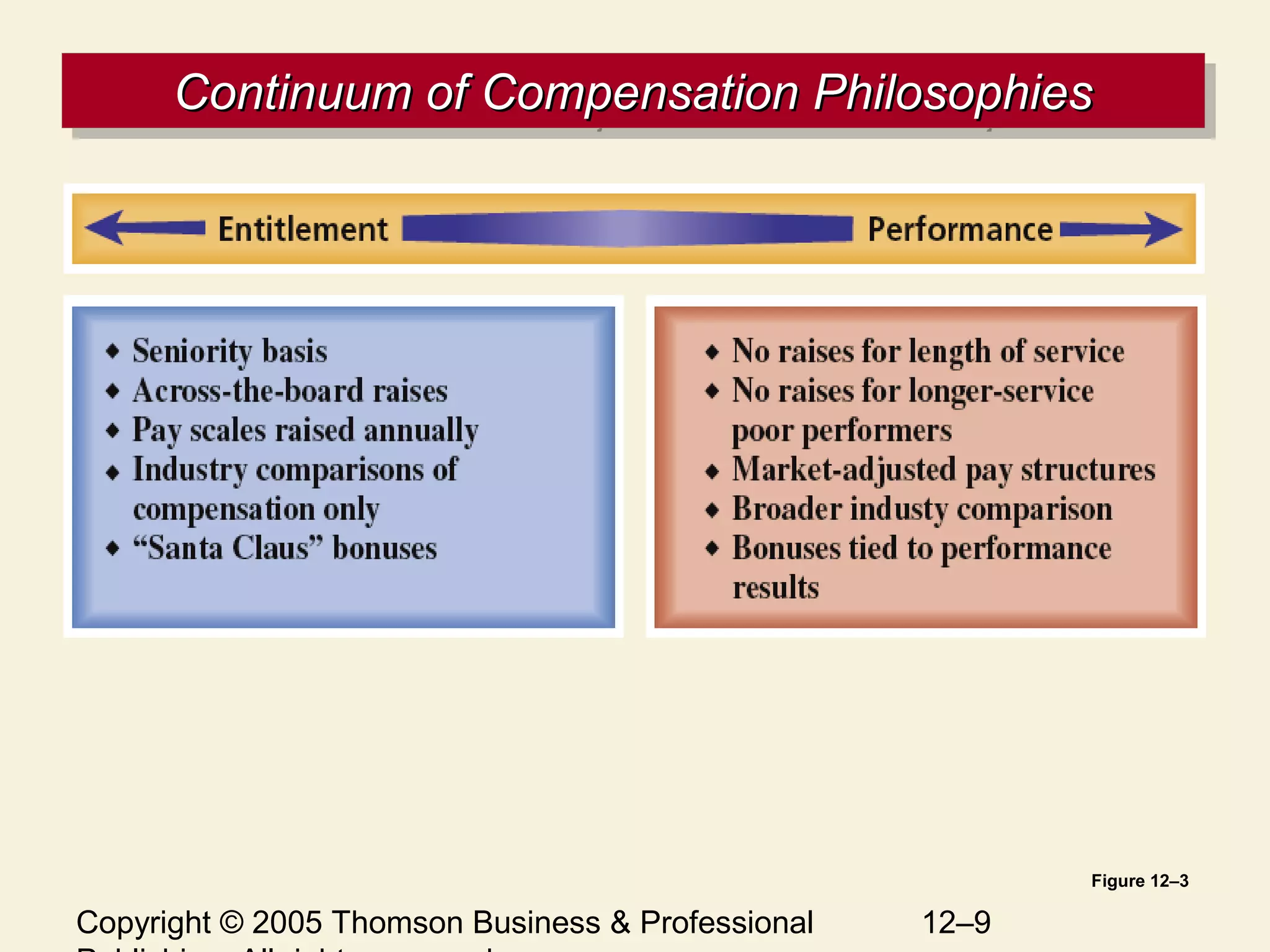

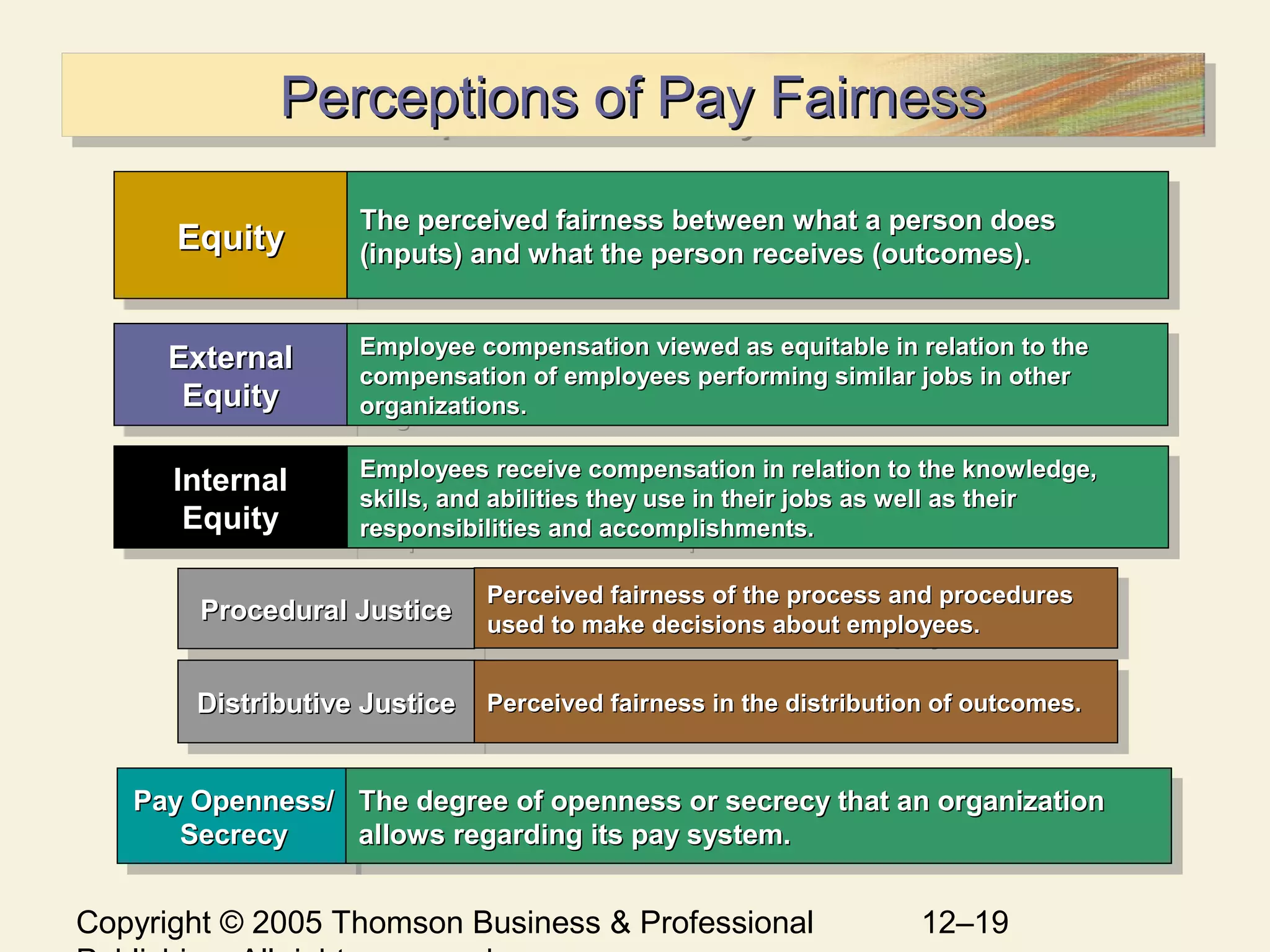

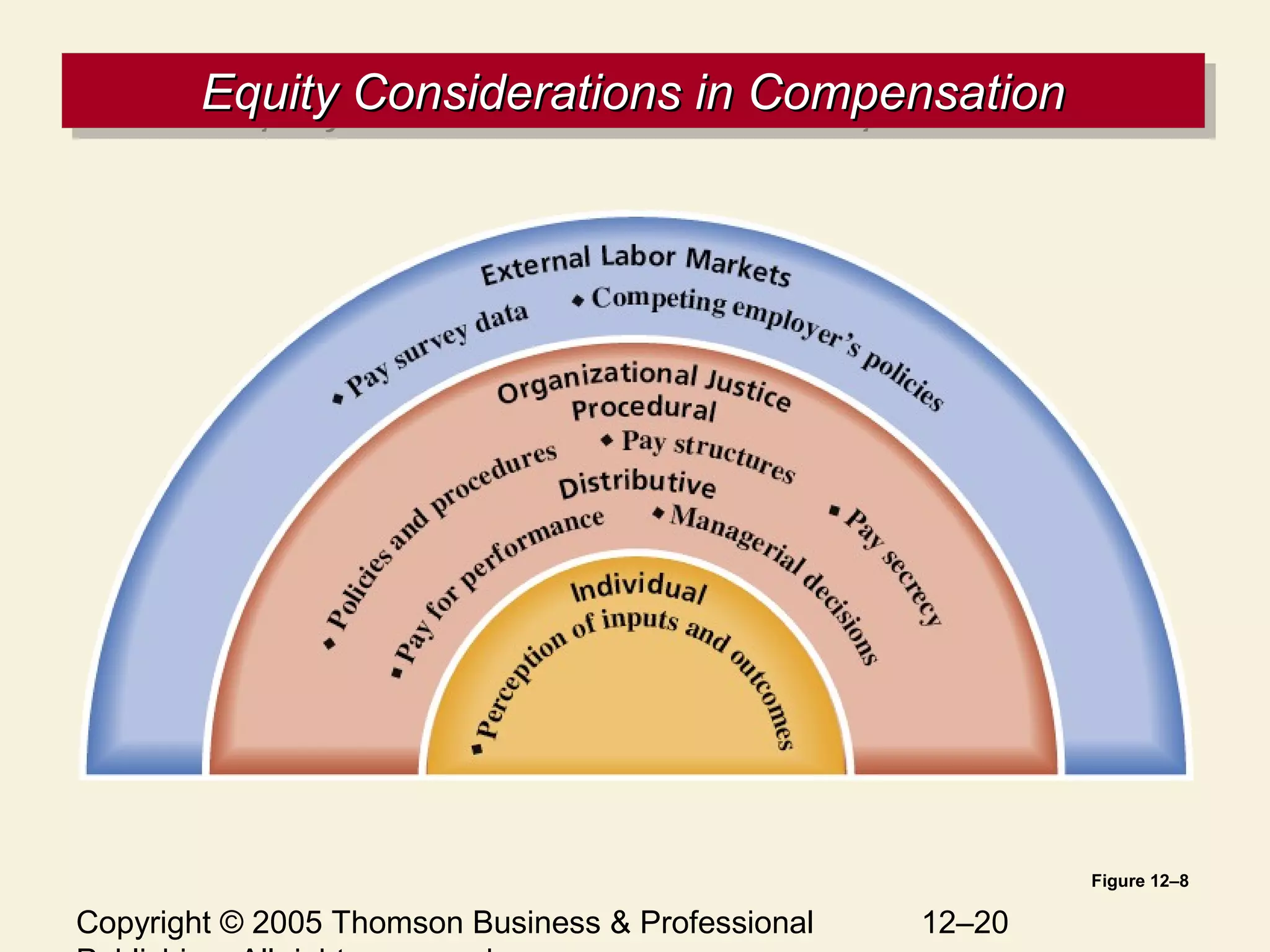

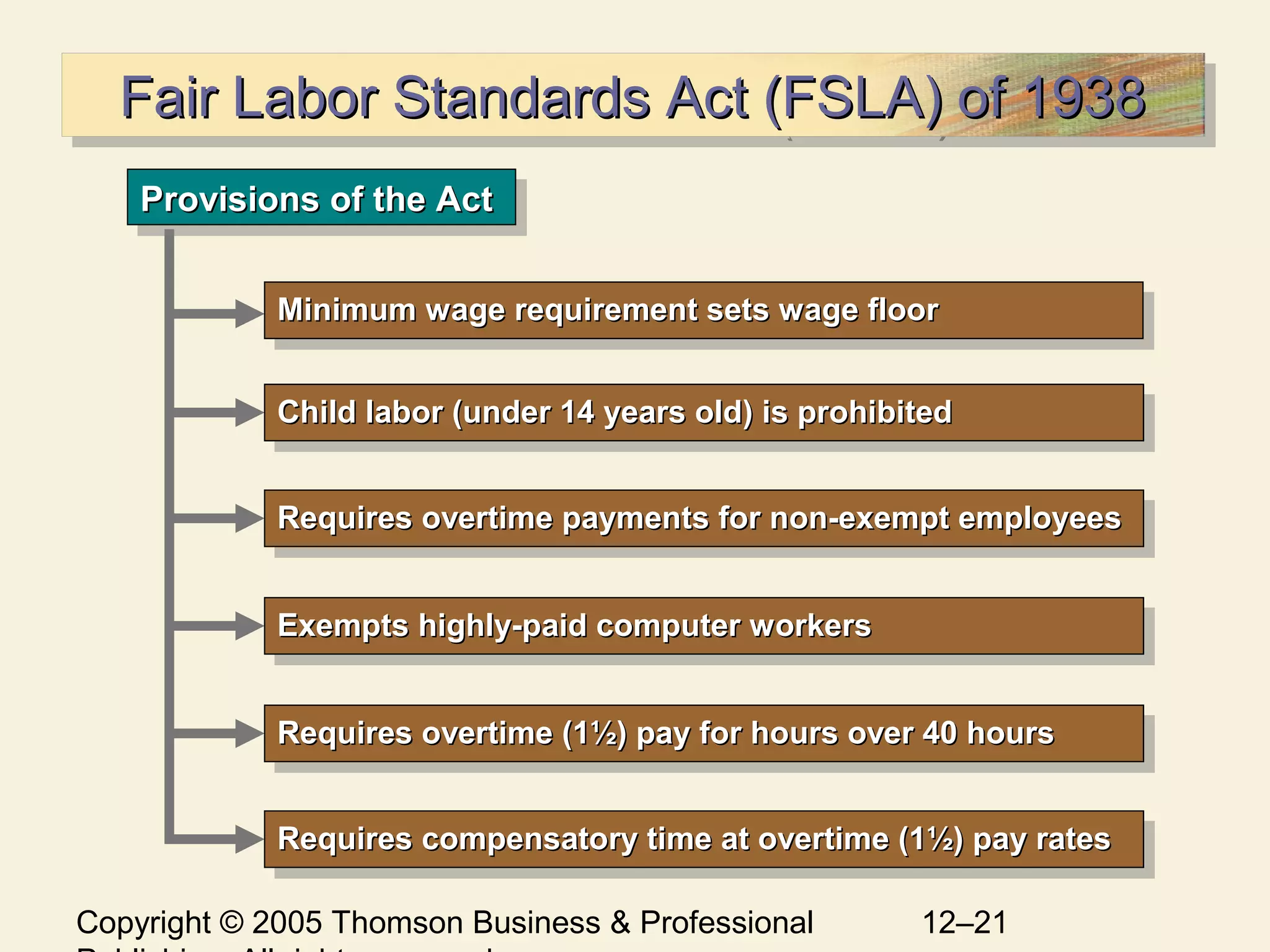

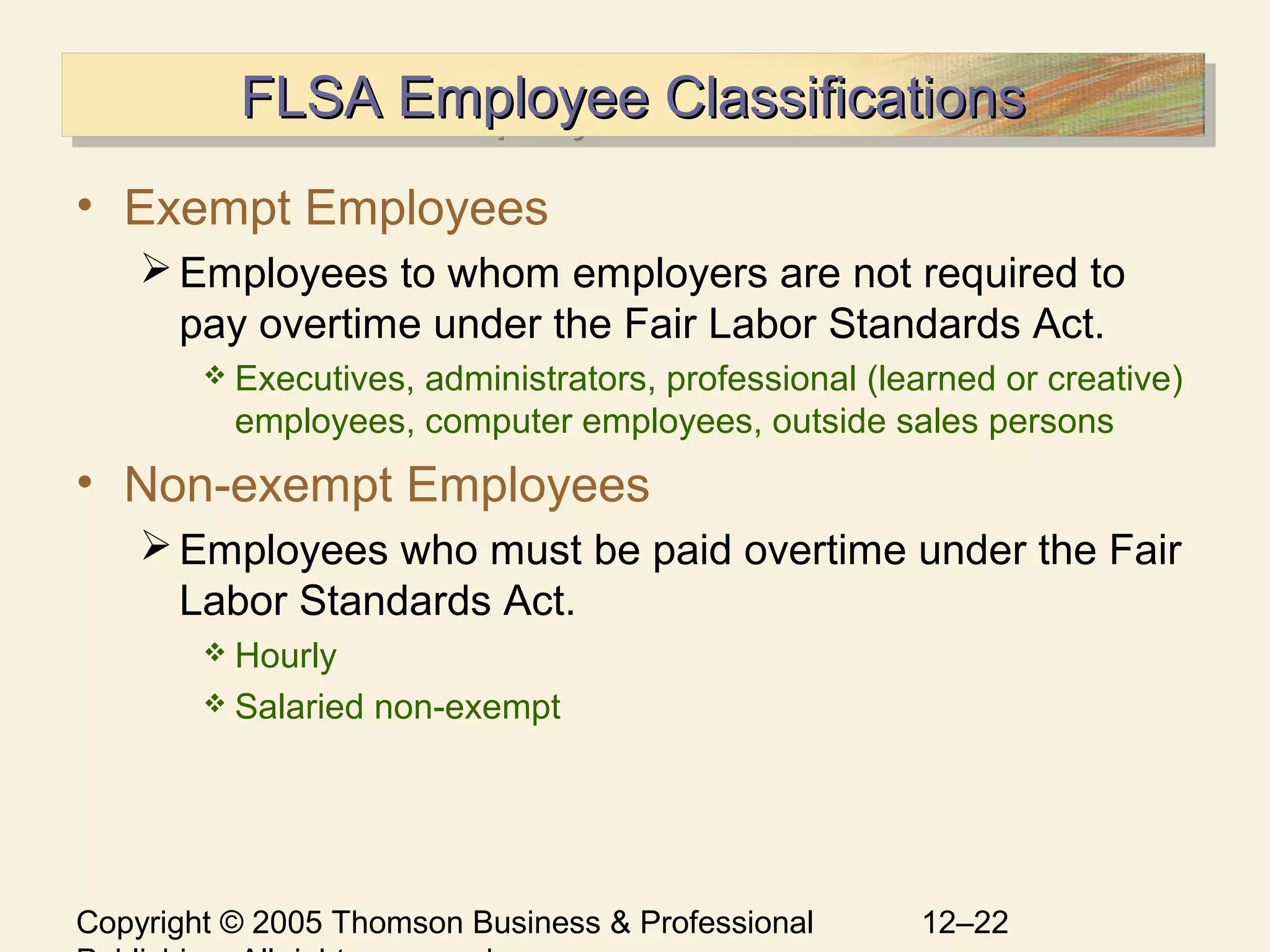

This document provides an overview of compensation strategies and practices for human resources. It discusses the two types of compensation as direct and indirect. Direct compensation includes base pay such as salary and wages, as well as variable pay linked to performance. Indirect compensation includes employer-provided benefits. The document outlines the components of a compensation system and considerations for strategic compensation design, including compensation philosophies, approaches, and ensuring pay fairness.