Download as PDF, PPTX

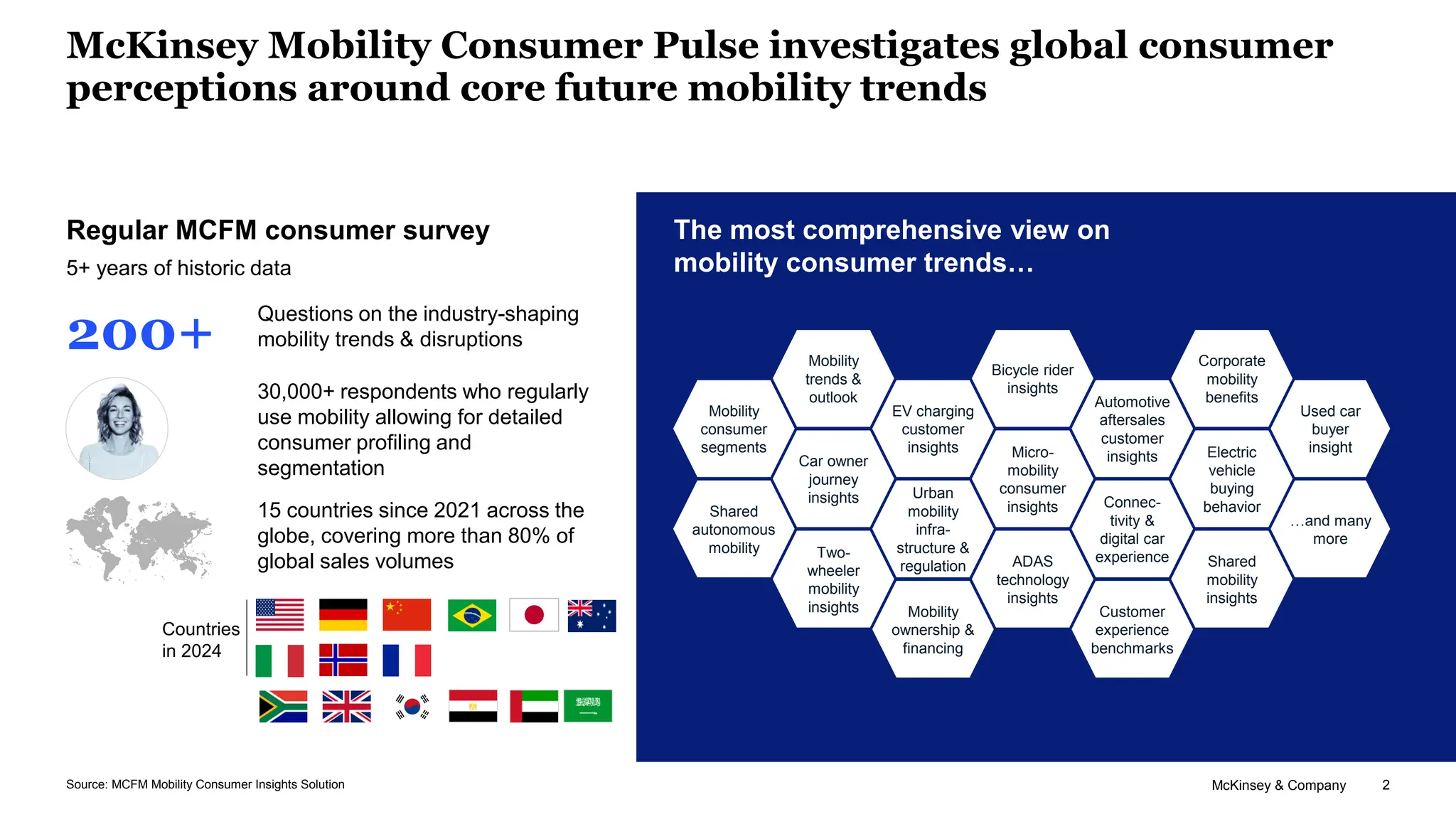

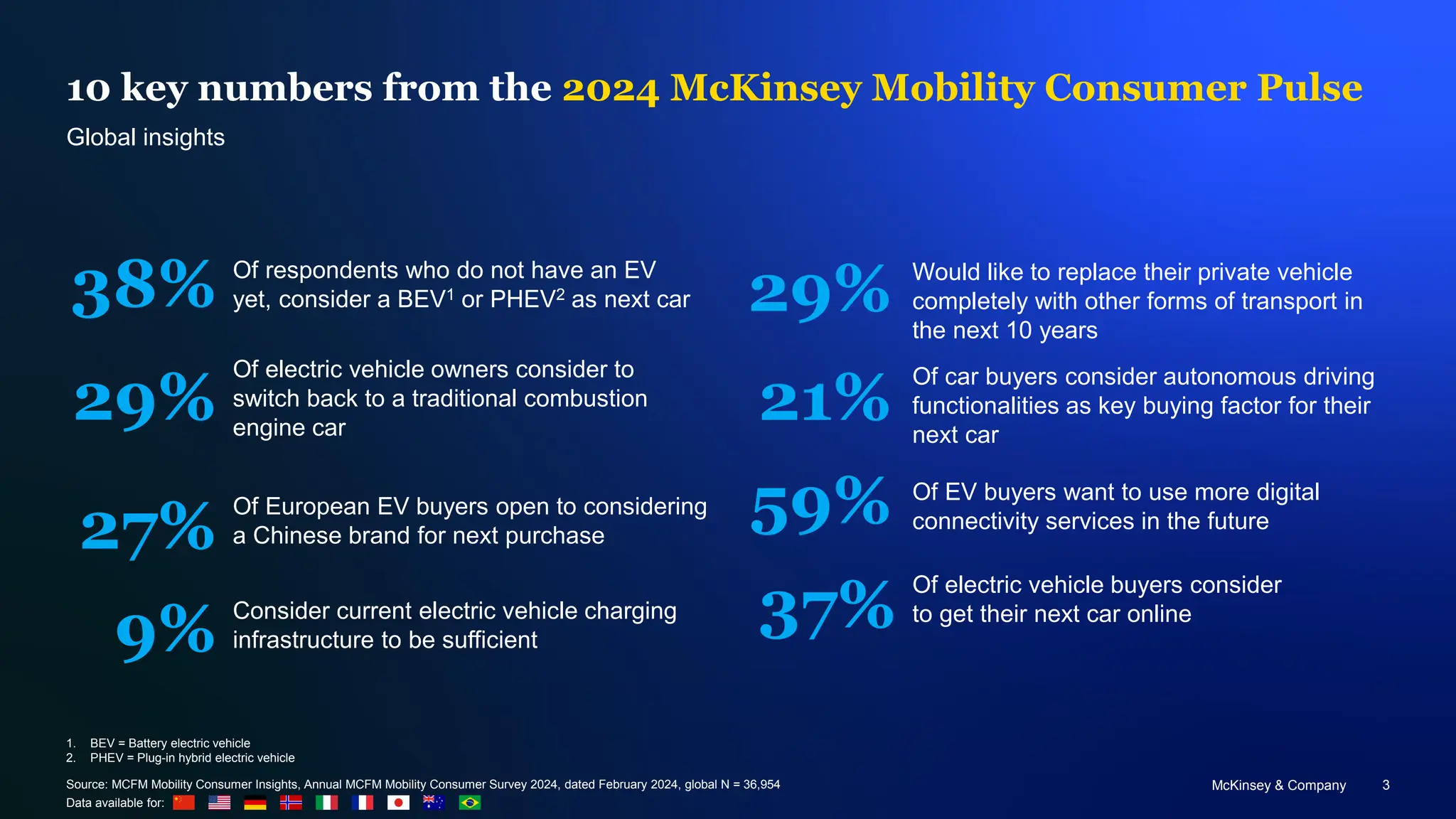

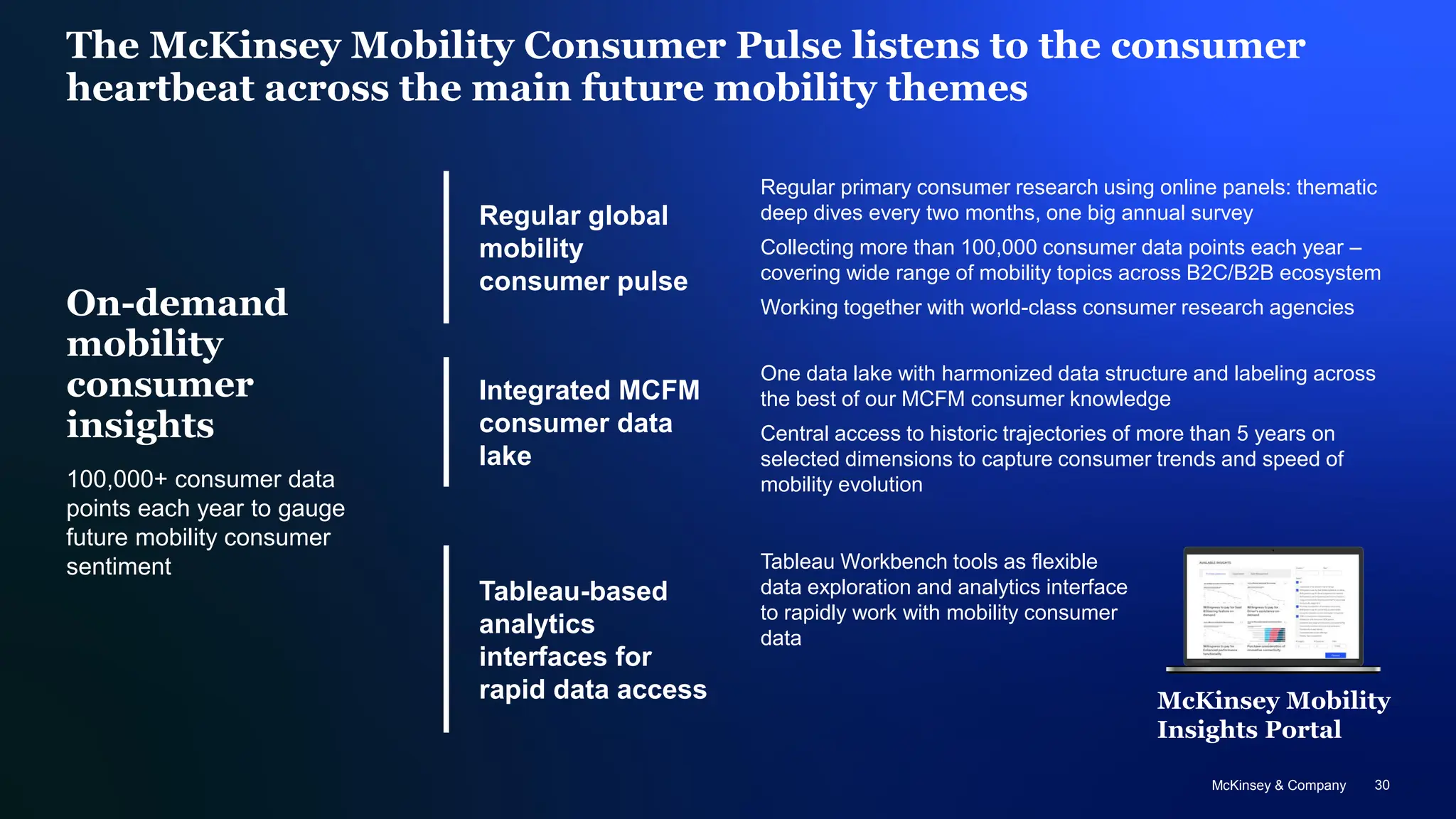

Uncover McKinsey’s Mobility Consumer Pulse 2024 with insights from 36,000+ consumers across 15 countries. Explore trends in electric vehicles, shared mobility, autonomous tech, and evolving consumer preferences shaping the future of mobility.

![Copy of Presentation - [Your Organization Name]_20250924_181258_0000.pdf](https://cdn.slidesharecdn.com/ss_thumbnails/copyofpresentation-yourorganizationname202509241812580000-251117131601-9744dd2d-thumbnail.jpg?width=640&height=640&fit=bounds)