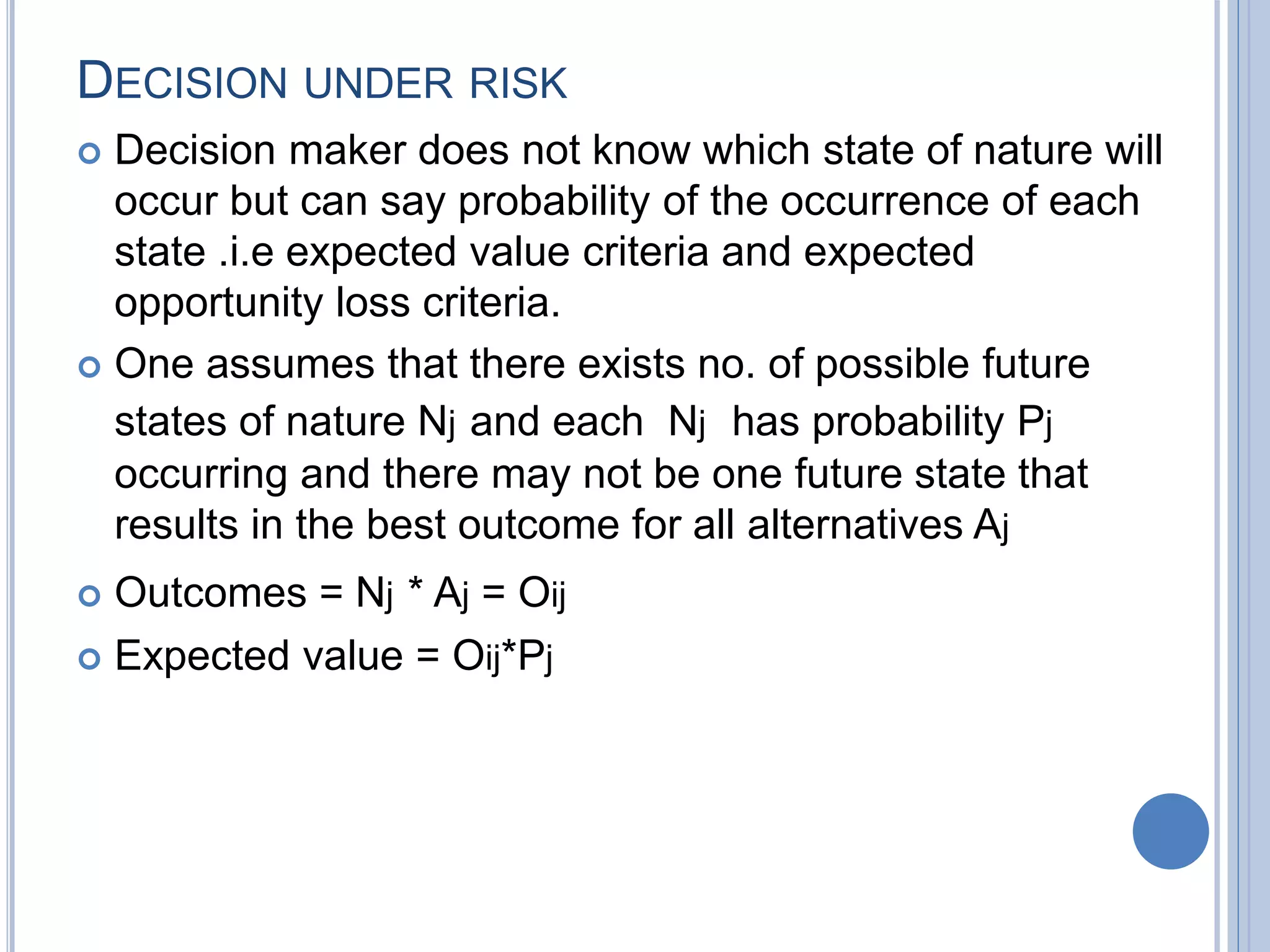

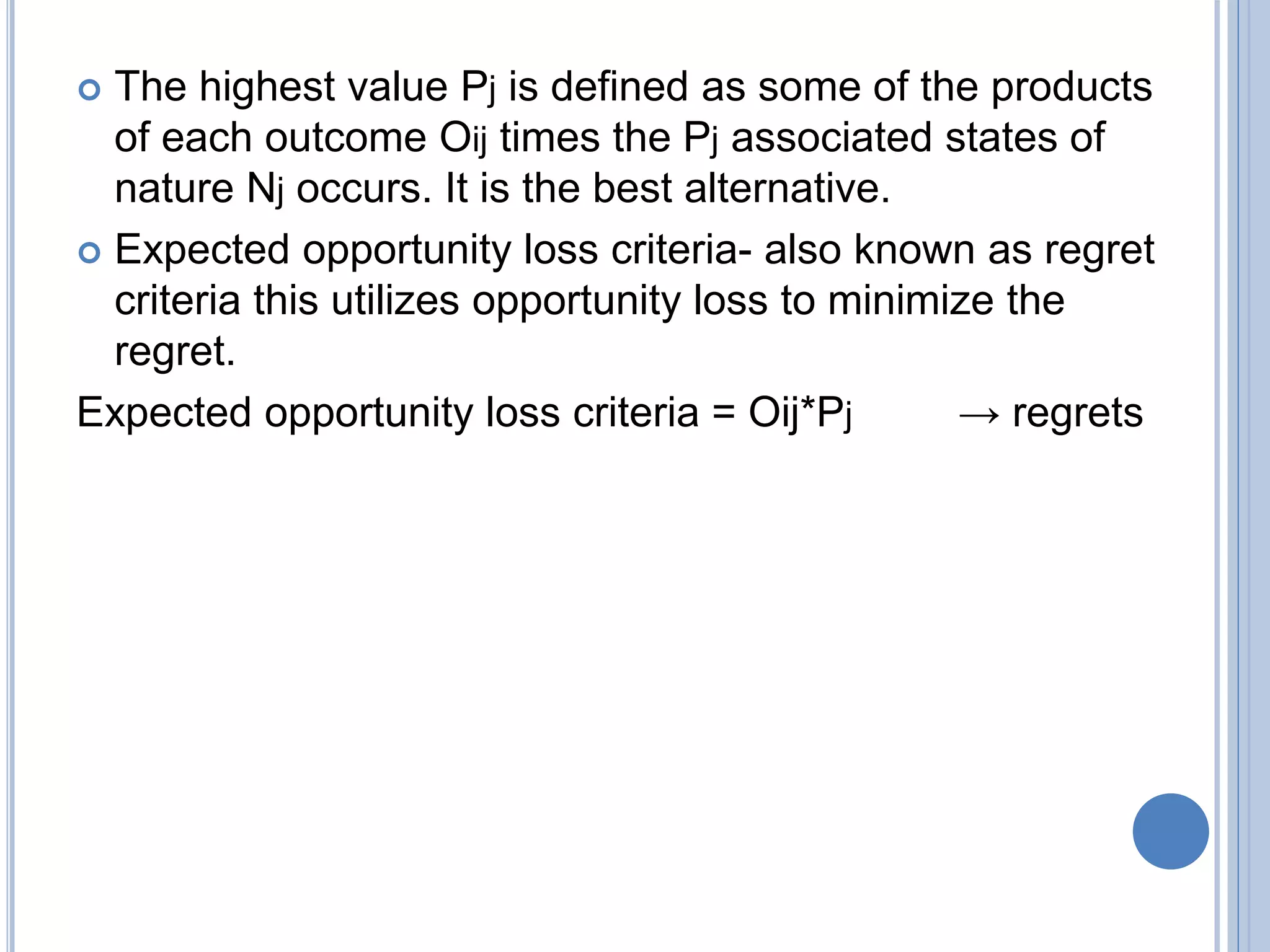

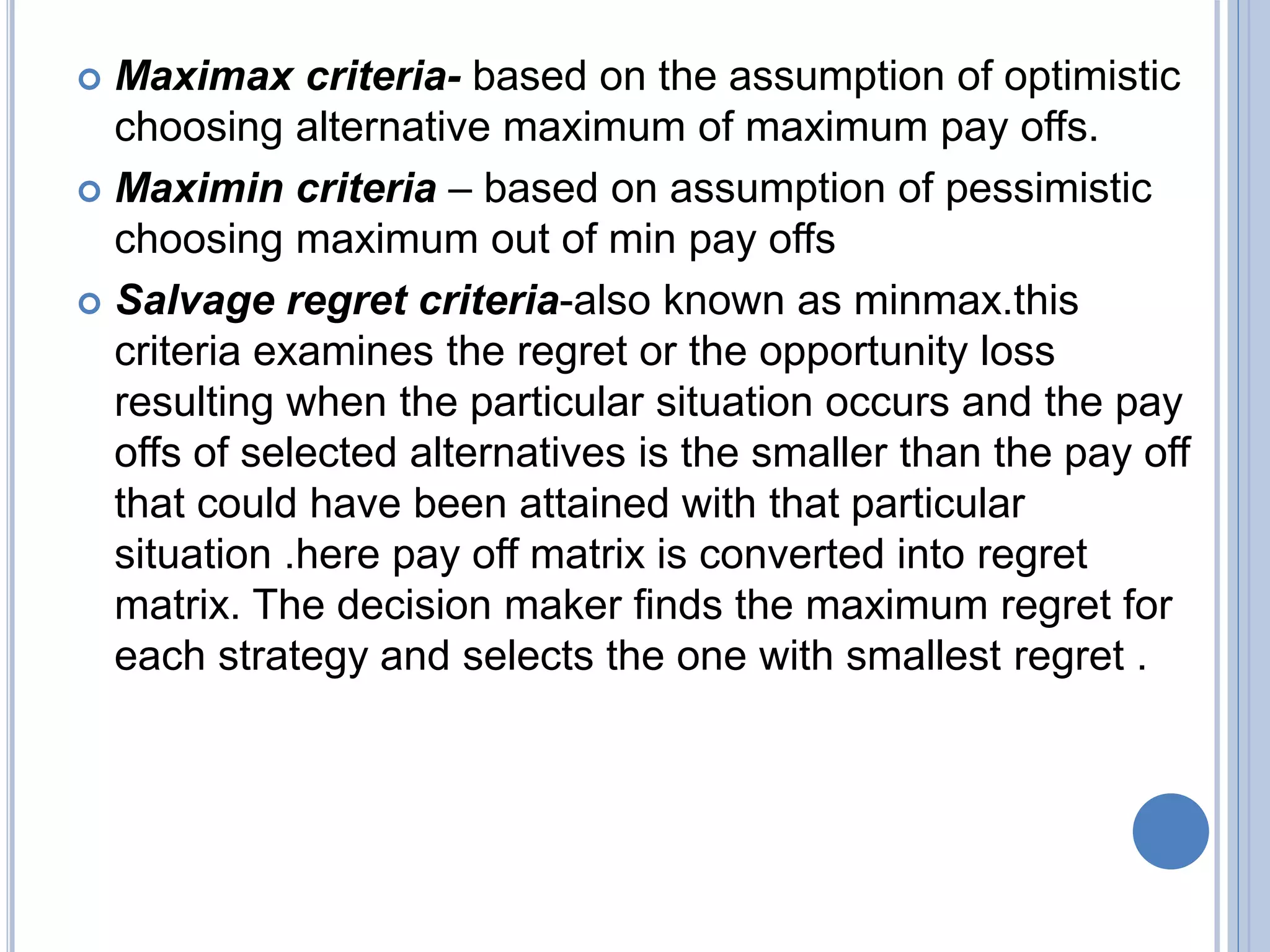

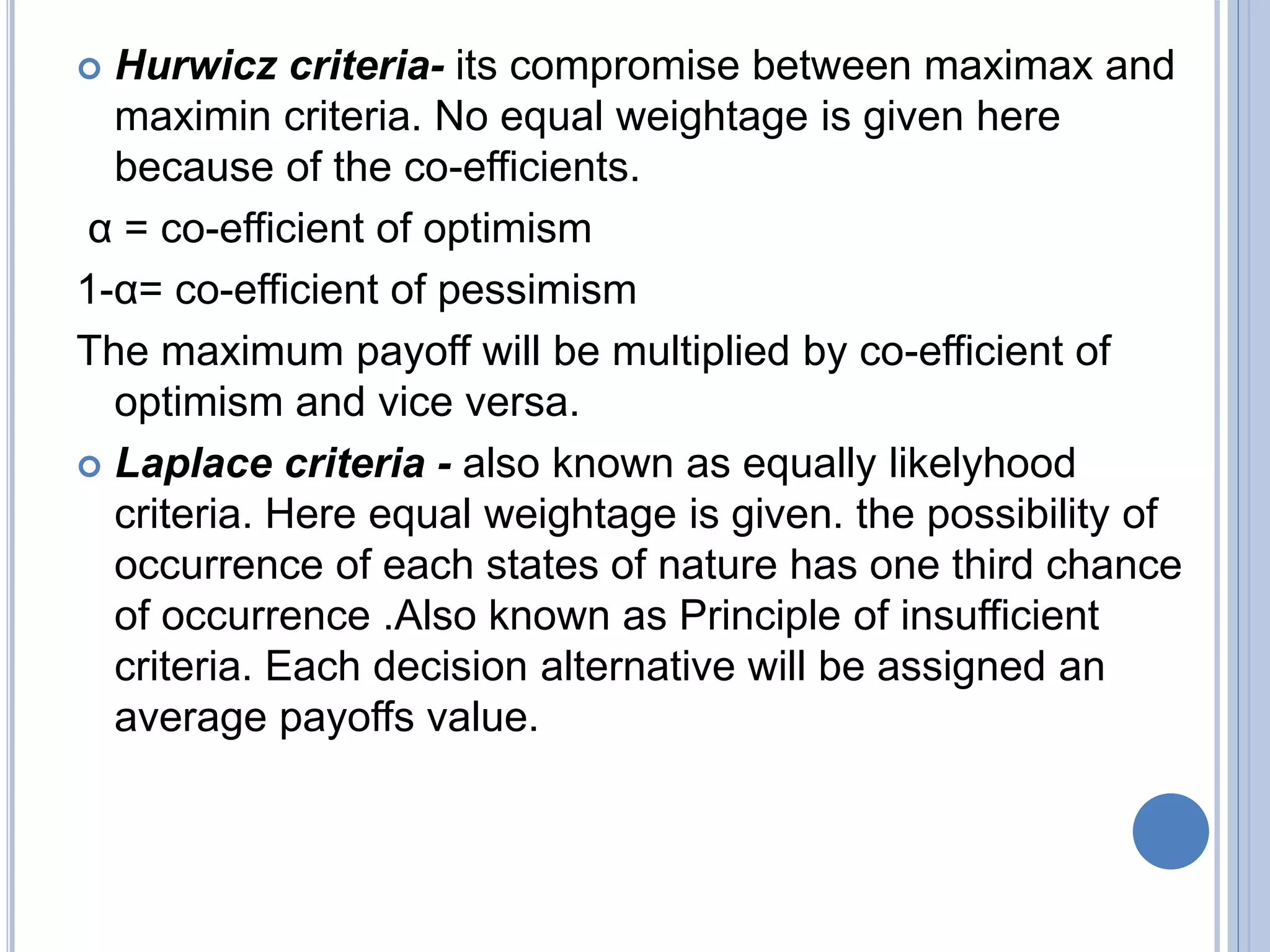

This document discusses different types of decision making environments including certainty, risk, uncertainty, and conflict. It defines key concepts in decision theory like courses of action, states of nature, and payoffs. It also describes different types of decisions and provides details on decision making under certainty, risk, and uncertainty. Decision making under uncertainty involves criteria like maximax, maximin, salvage regret, Hurwicz, and Laplace criteria.