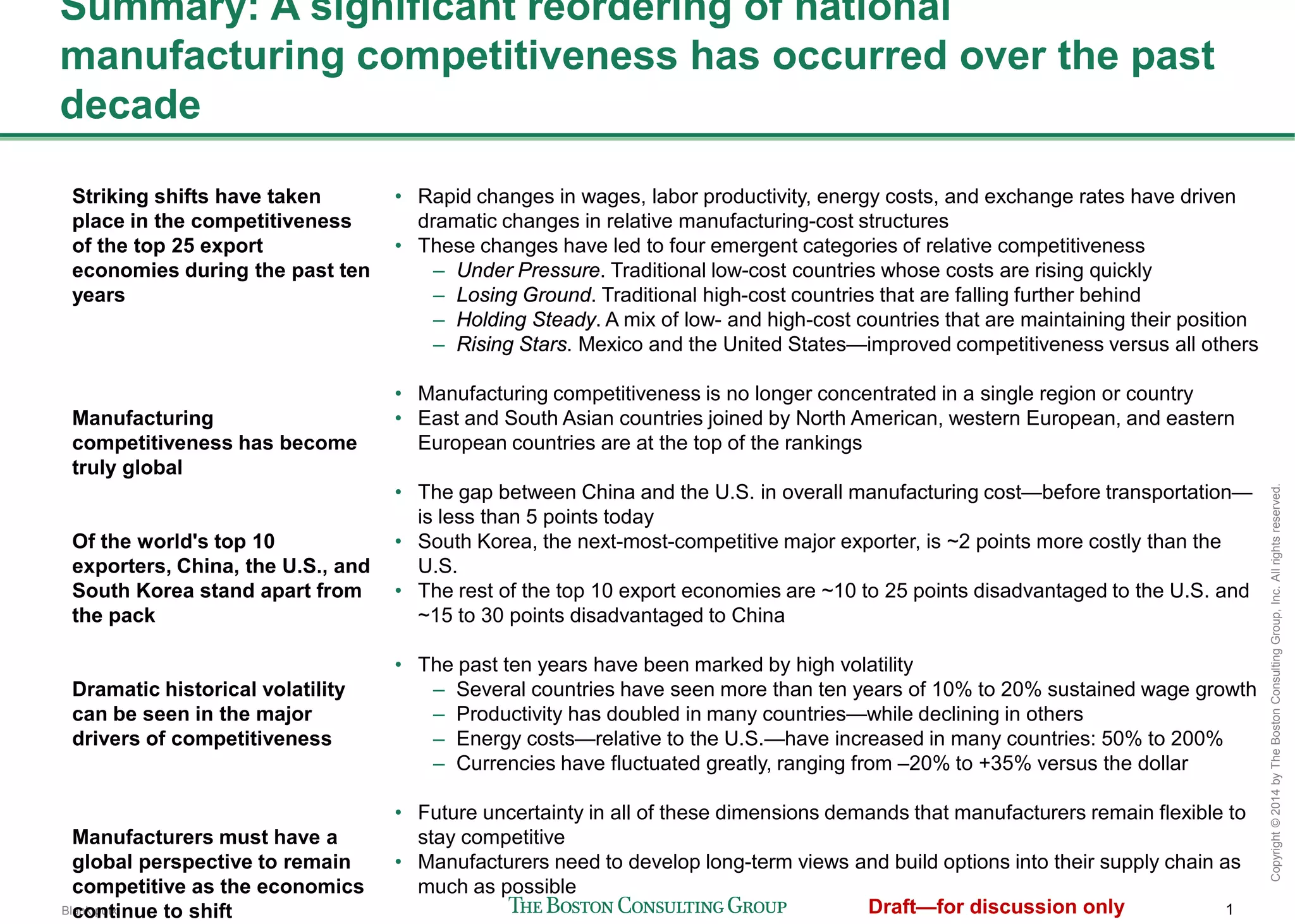

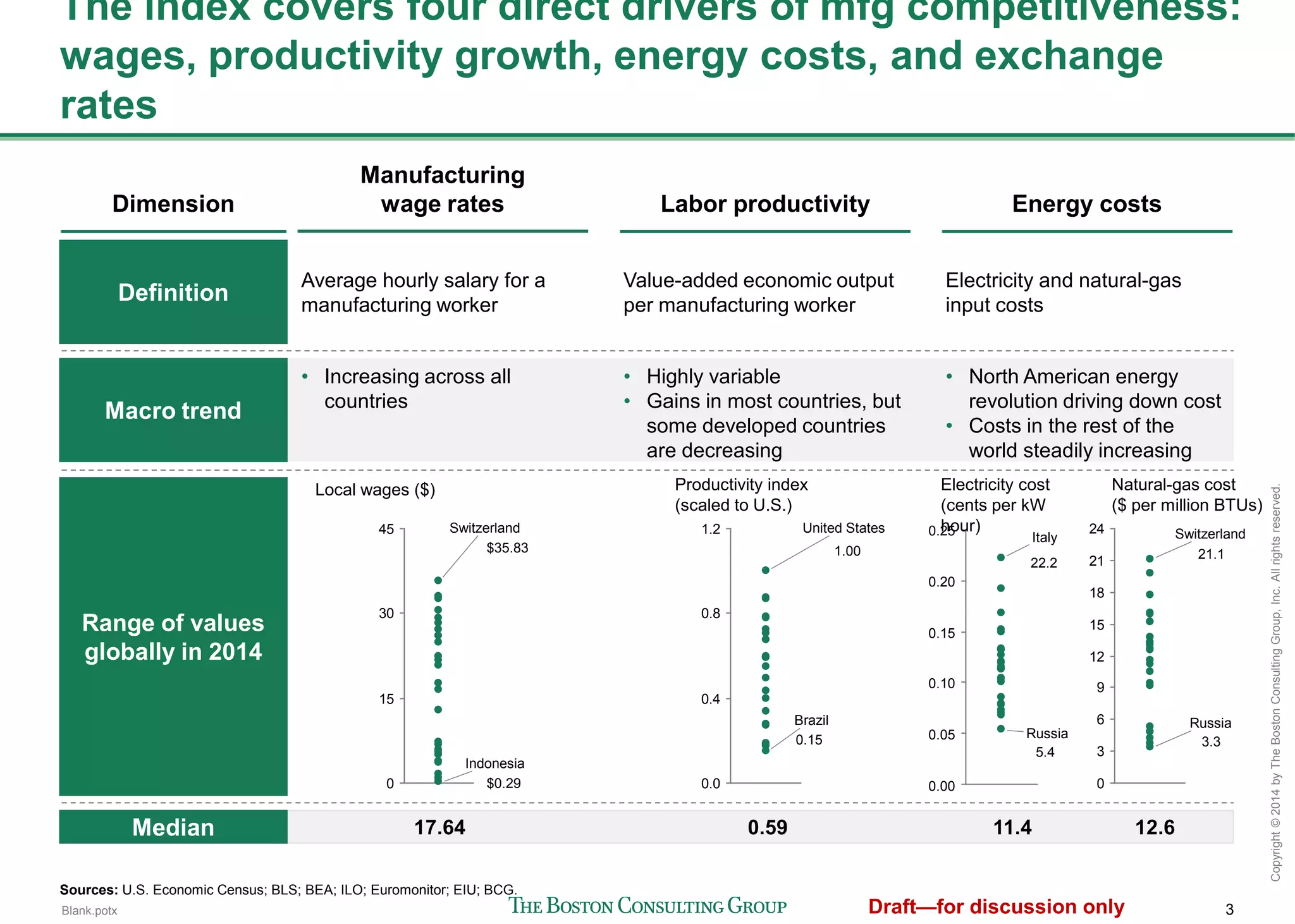

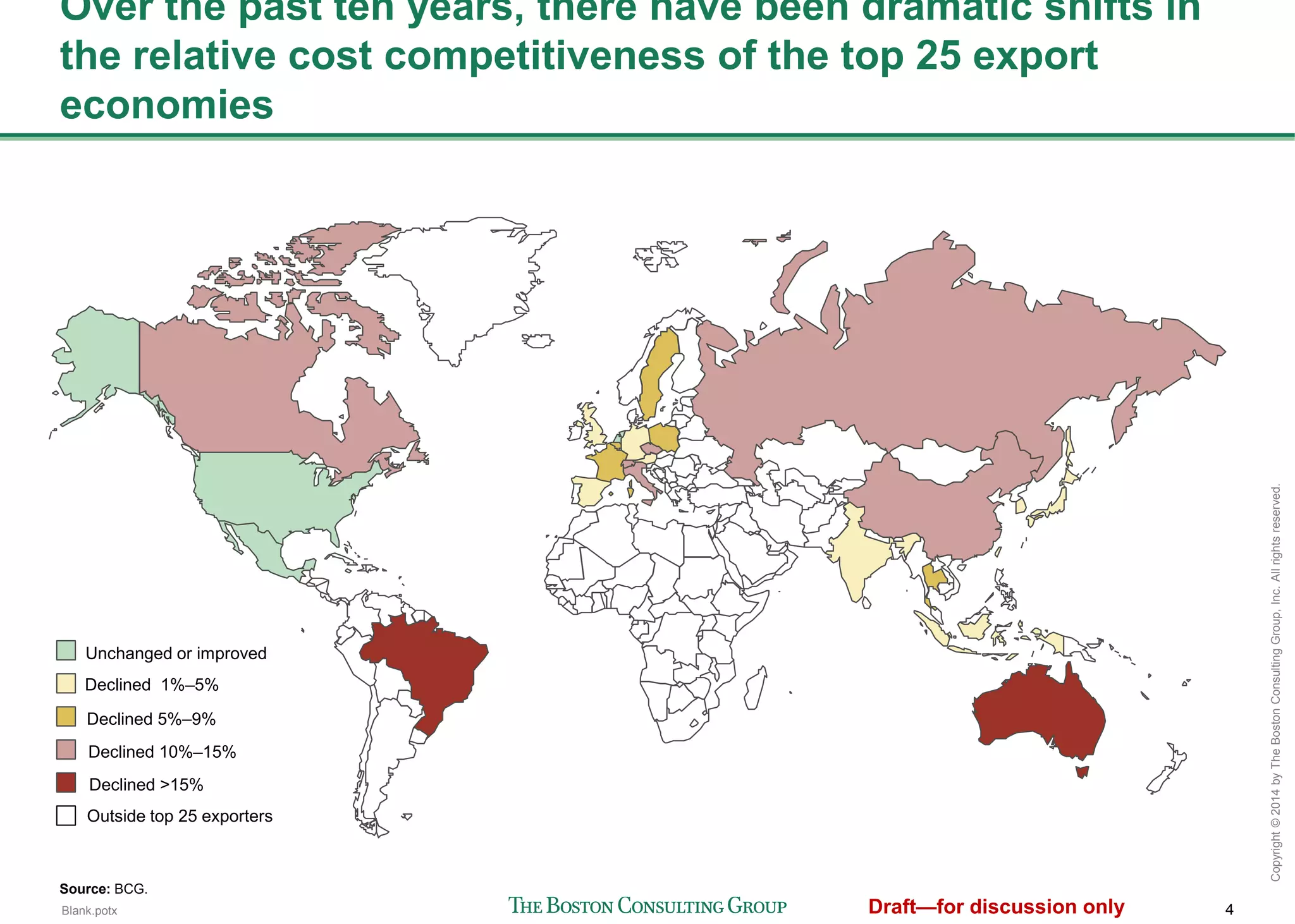

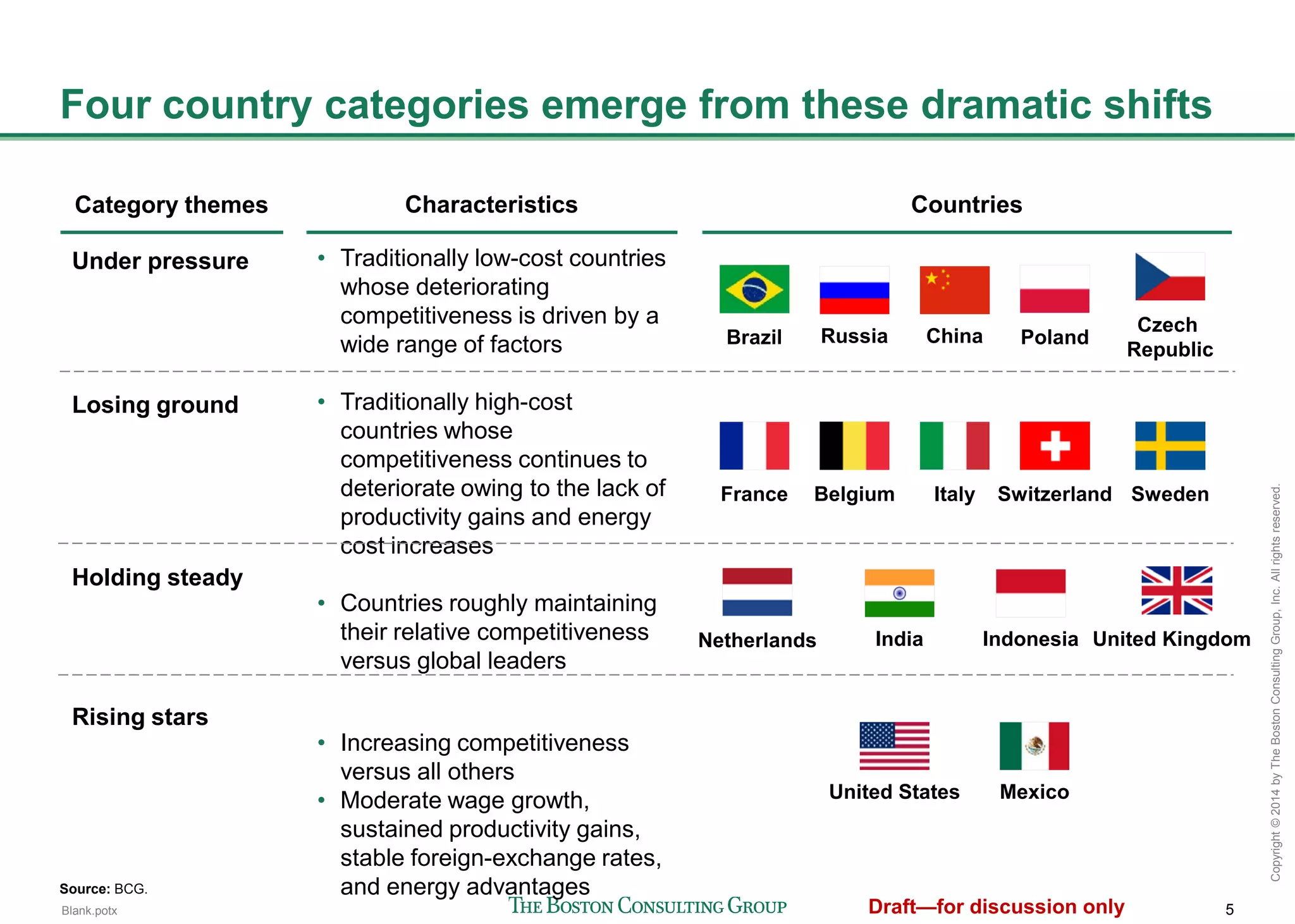

This document analyzes shifts in manufacturing competitiveness among the top 25 export economies over the past decade. It finds that dramatic changes in wages, productivity, energy costs, and exchange rates have led to four categories of countries in terms of competitiveness: under pressure, losing ground, holding steady, and rising stars like the US and Mexico. While China remains the most competitive overall, its lead over the US is shrinking and other countries like South Korea are also highly competitive. Future uncertainty in economic drivers means manufacturers must have flexibility to remain competitive as conditions continue changing globally.