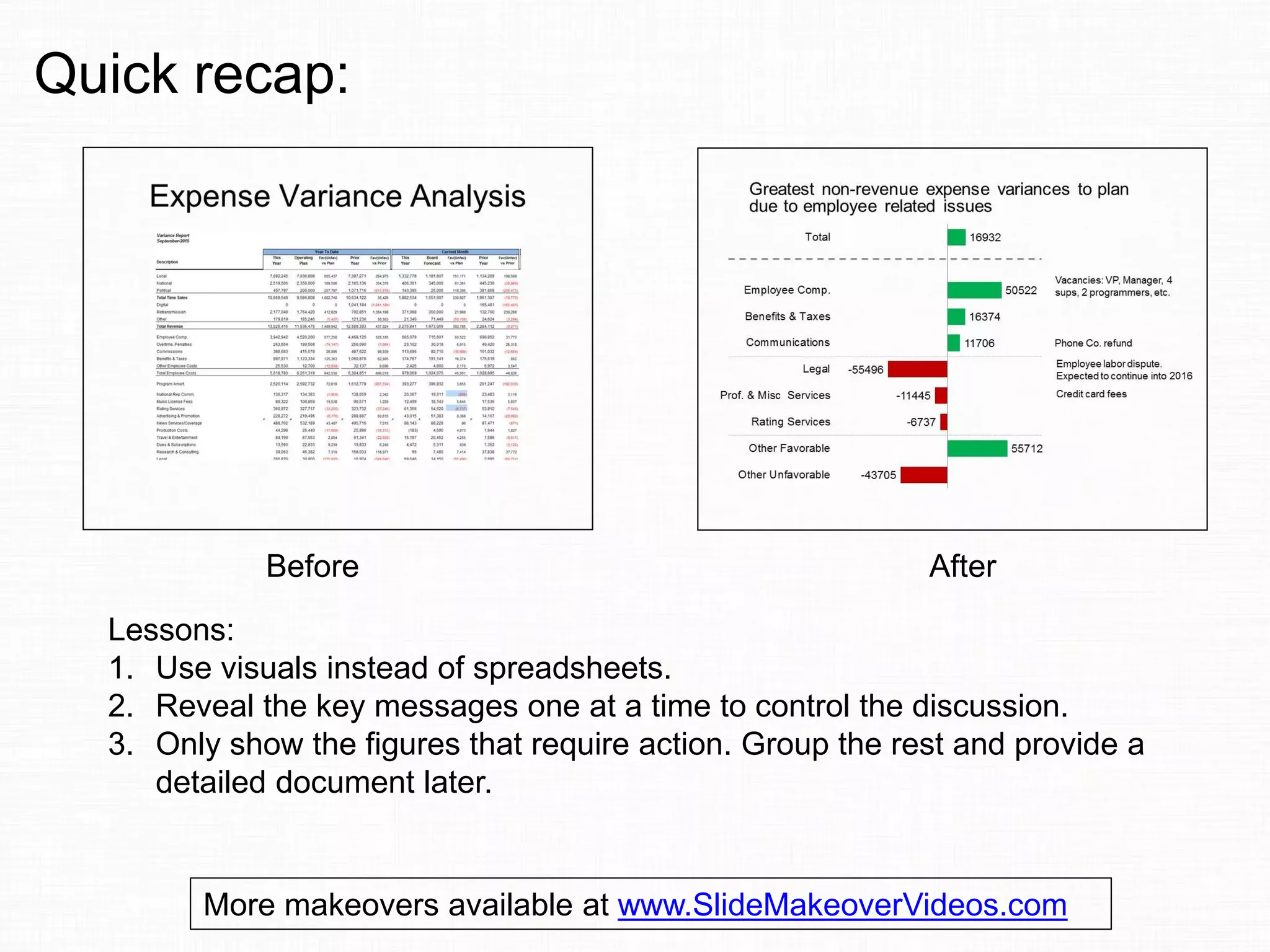

The document discusses effective presentation techniques for variance analysis, emphasizing the use of visuals over spreadsheets to enhance audience focus. It outlines methods for presenting key variances—both favorable and unfavorable—by revealing information gradually and selectively. The advice includes showing only essential figures and providing detailed data in supplementary documents to maintain clarity and control the discussion.

![Creating a powerful_presentation[1]](https://cdn.slidesharecdn.com/ss_thumbnails/creatingapowerfulpresentation1-100604185446-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)