Downloaded 99 times

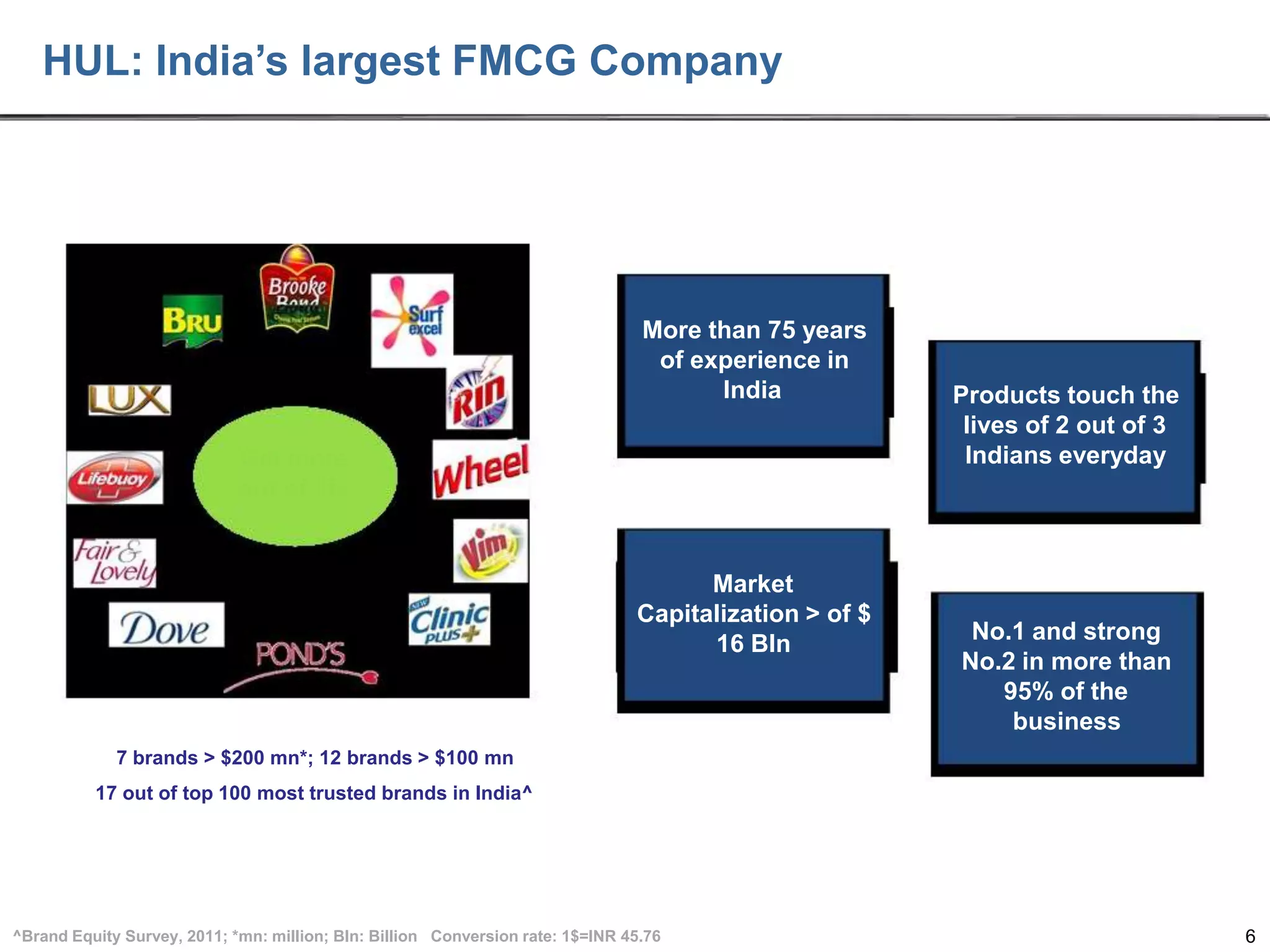

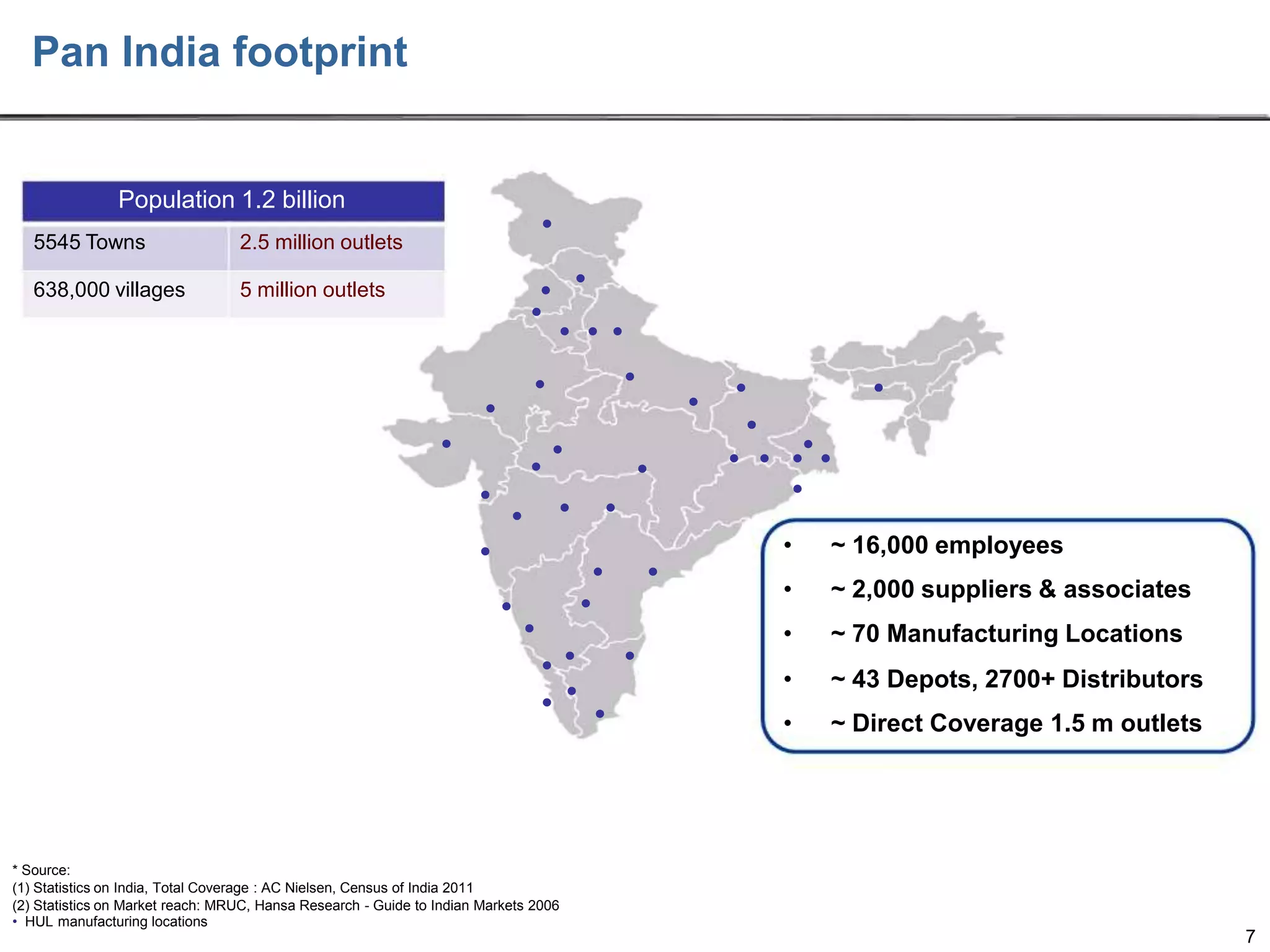

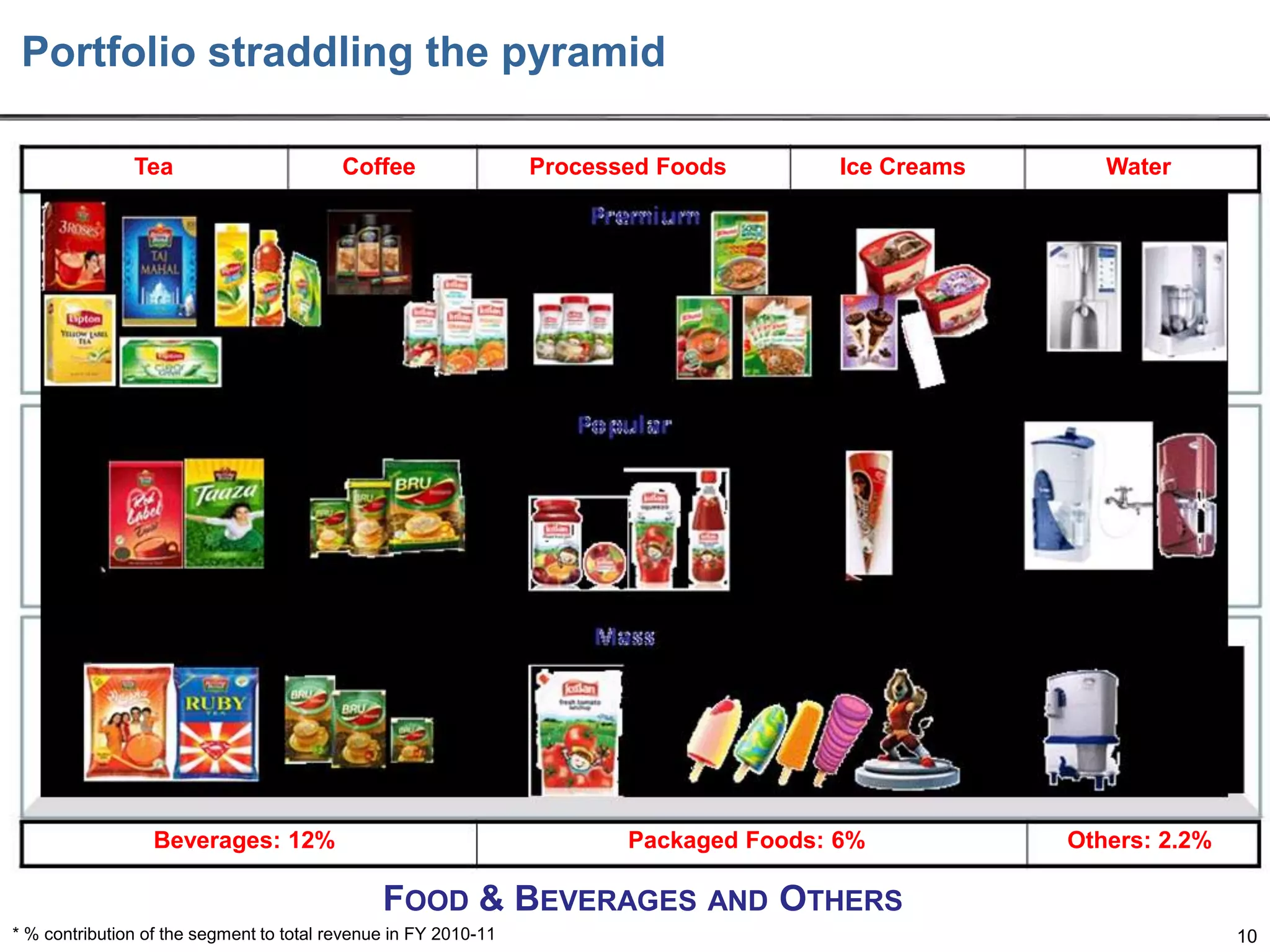

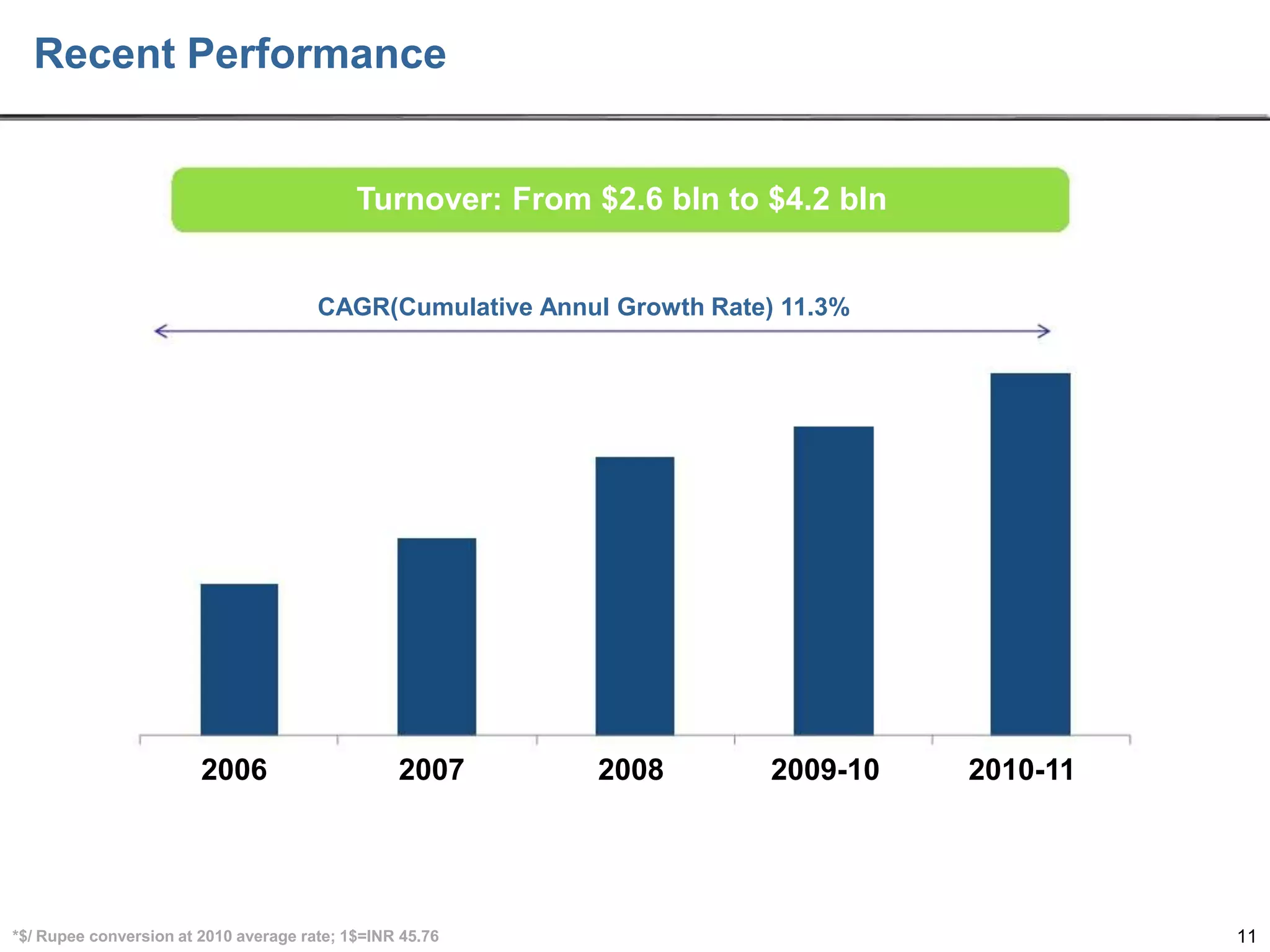

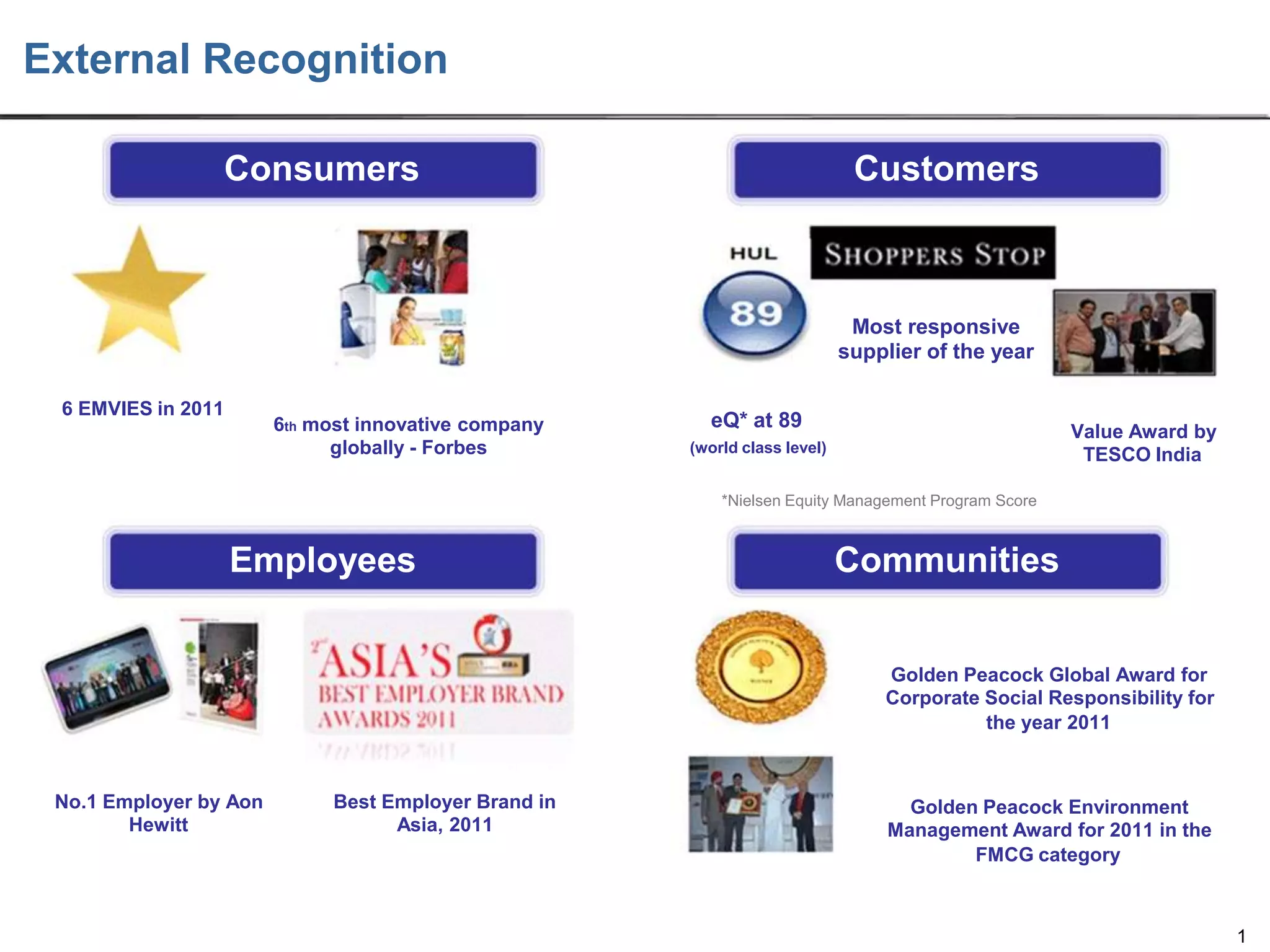

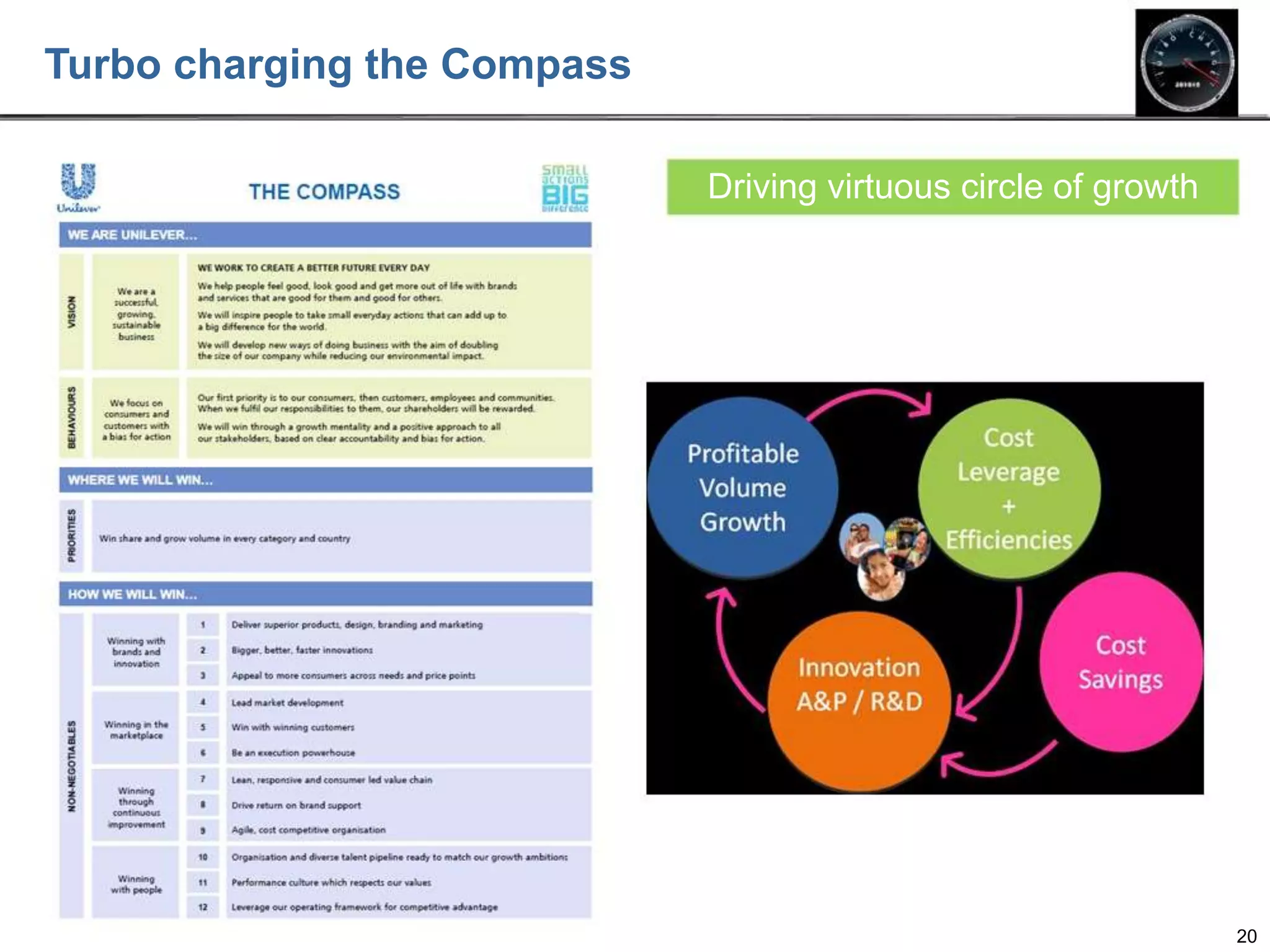

HUL is India's largest fast-moving consumer goods (FMCG) company with over 75 years of experience in India. It has a pan-India footprint with products that touch the lives of 2 out of 3 Indians daily. HUL holds the number 1 or strong number 2 position in over 95% of the business categories. The company aims to double its size while reducing environmental impact by inspiring small everyday actions. It has demonstrated consistent growth, achieving an 11.3% CAGR from 2006 to 2010-2011. HUL also has strong brands, market leadership positions, talented employees, and global leverage that position it well to capitalize on growth opportunities in India.

![Qcl 15-v4 [challenge-no 5 ]_[imnu]_[shubham gupta]](https://cdn.slidesharecdn.com/ss_thumbnails/qcl-15-v4challengeno5imnushubhamgupta-150427090717-conversion-gate02-thumbnail.jpg?width=640&height=640&fit=bounds)