Download to read offline

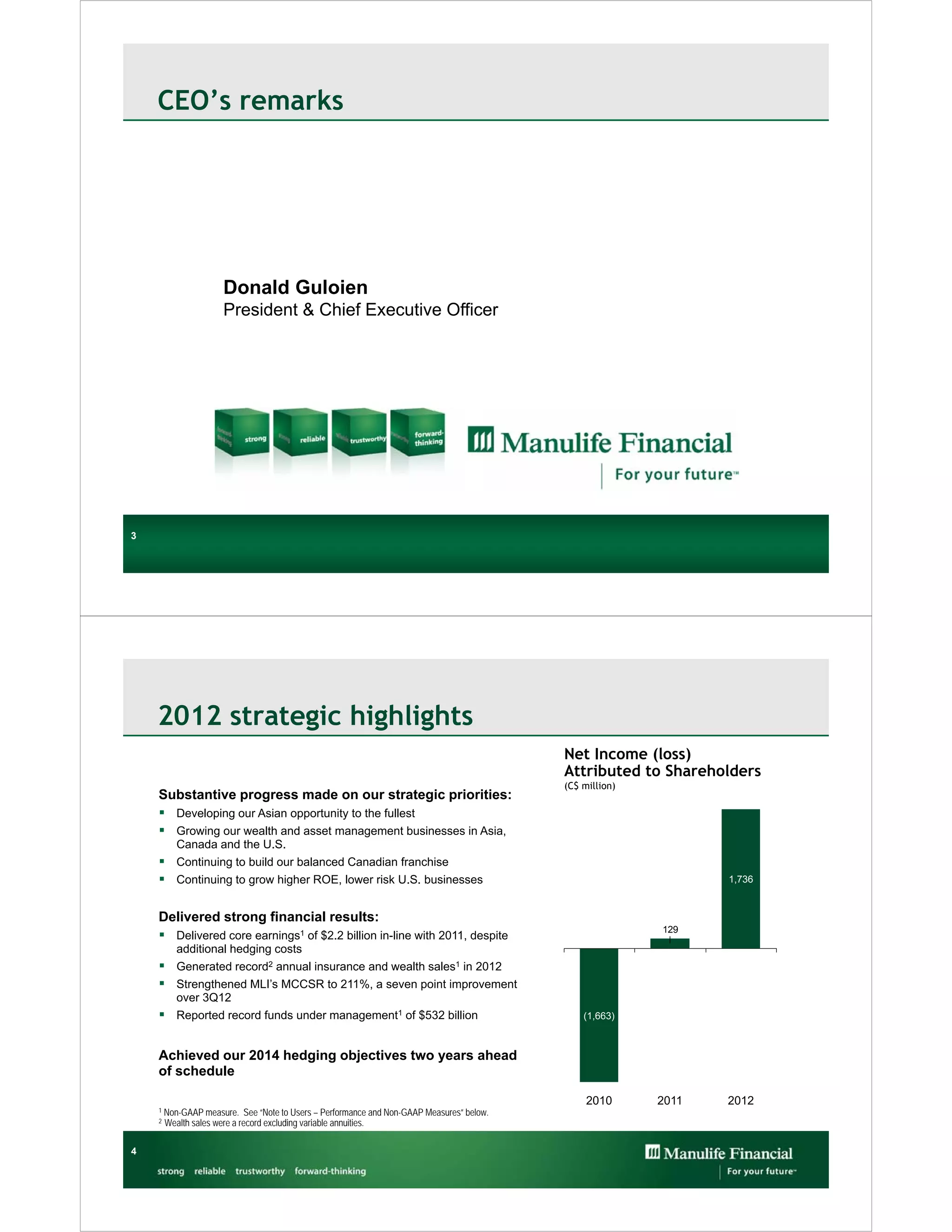

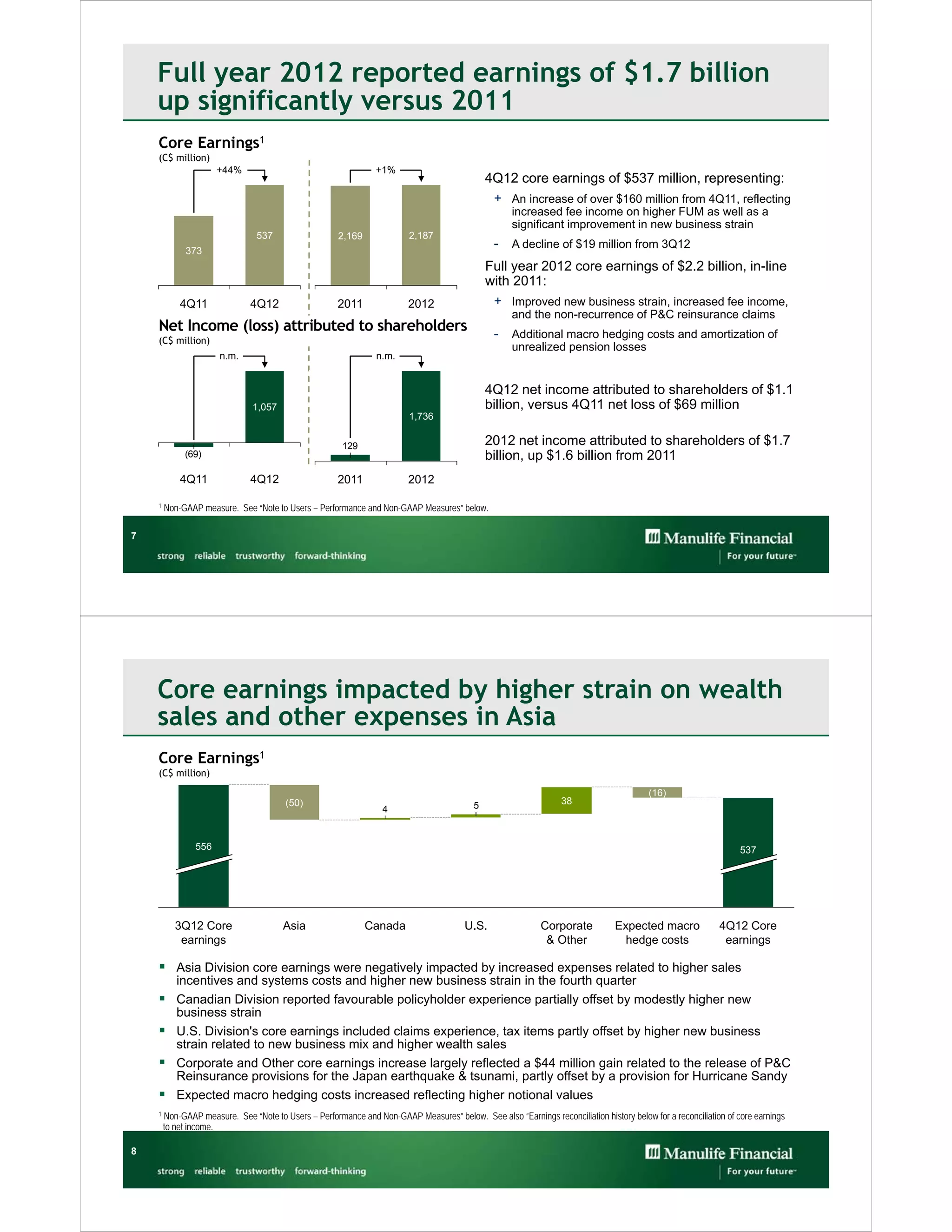

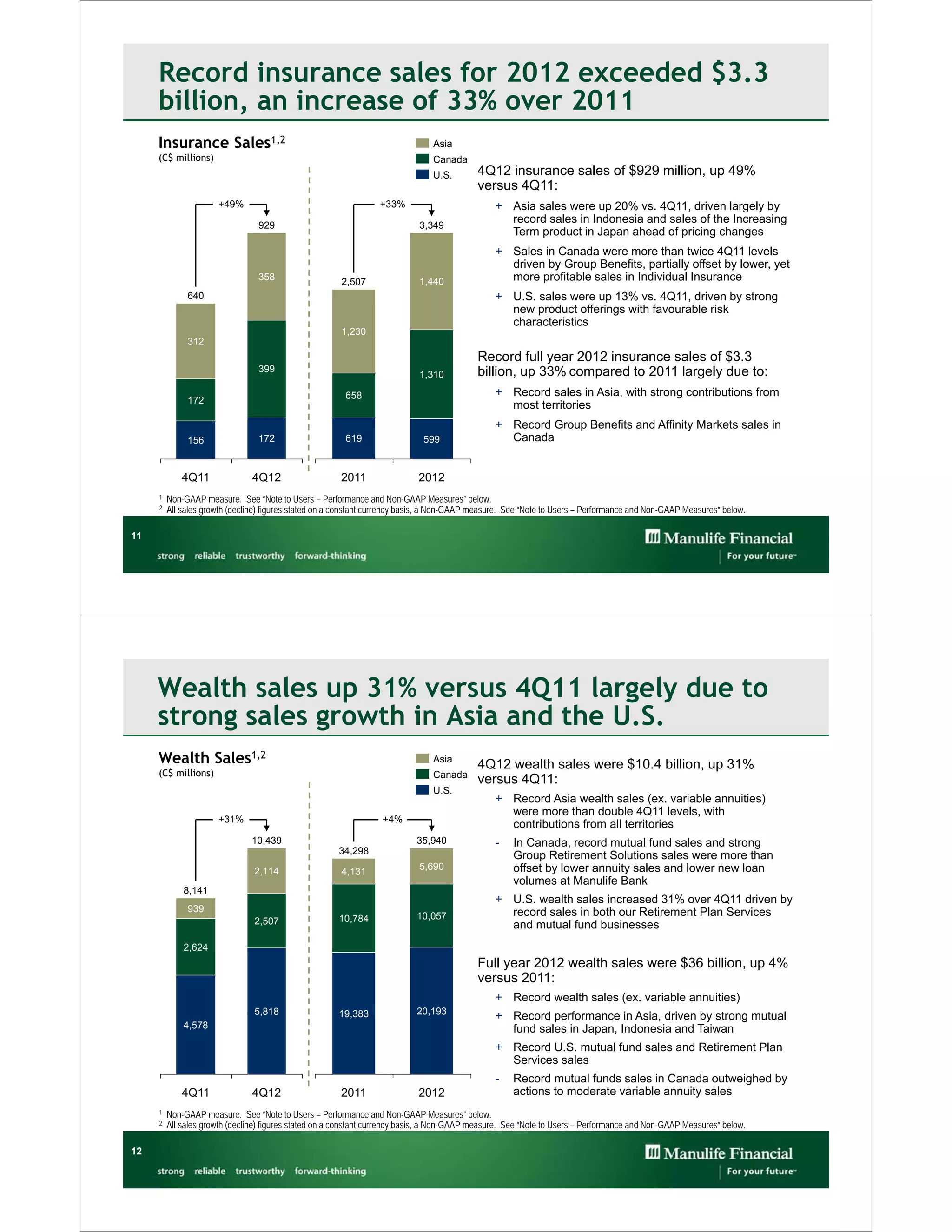

Manulife reported its financial results for the fourth quarter and full year of 2012. Some key highlights include: - Core earnings of $537 million for Q4 2012 and $2.2 billion for the full year of 2012, in line with 2011 results. - Record insurance sales of $3.3 billion for 2012, a 33% increase over 2011, driven by strong growth in Asia. Wealth sales also increased with Q4 2012 sales reaching $10.4 billion, up 31% from Q4 2011. - Net income attributed to shareholders was $1.057 billion for Q4 2012 and $1.736 billion for the full year, up significantly from 2011 results. So