Download as PDF, PPTX

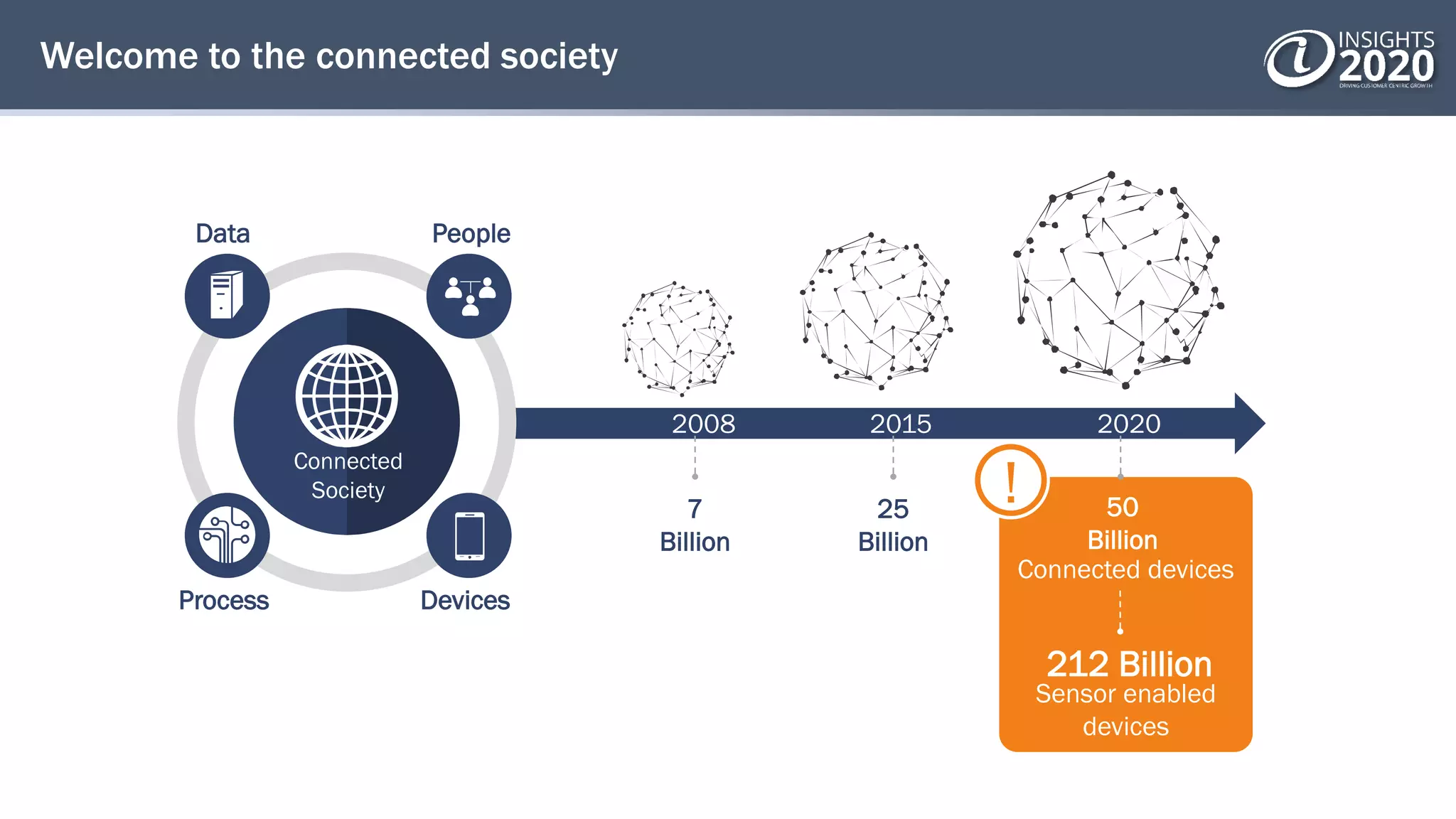

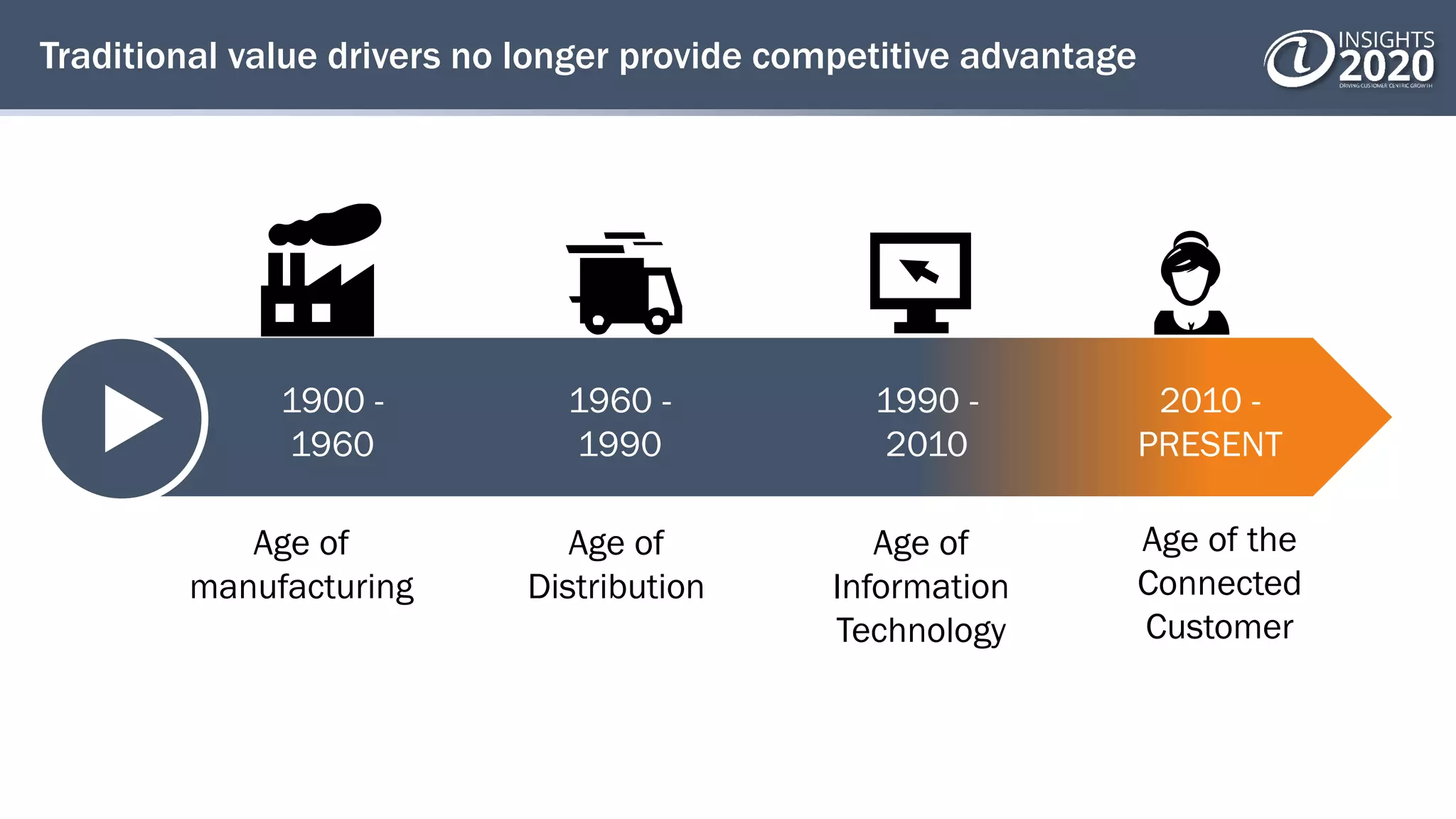

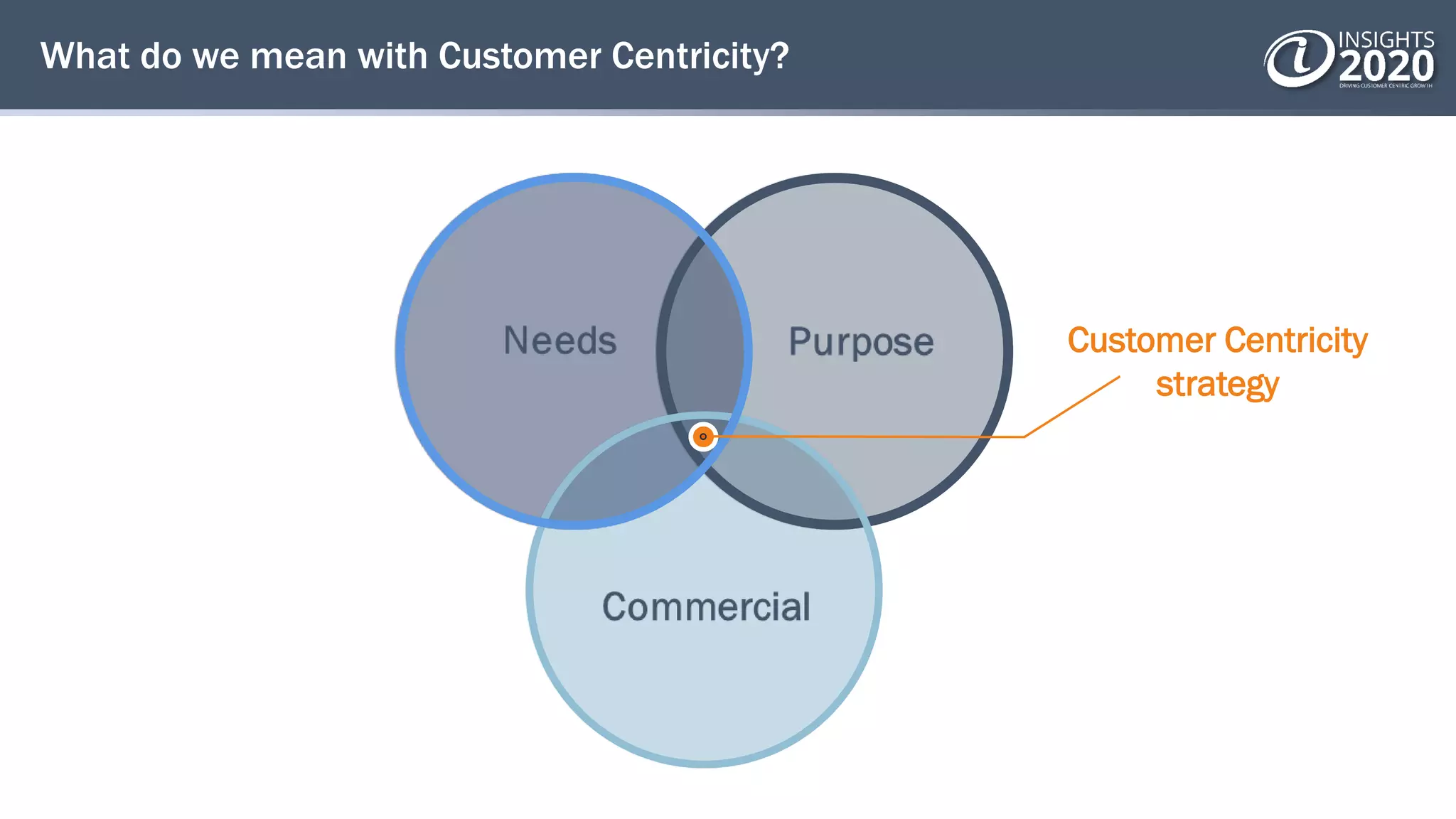

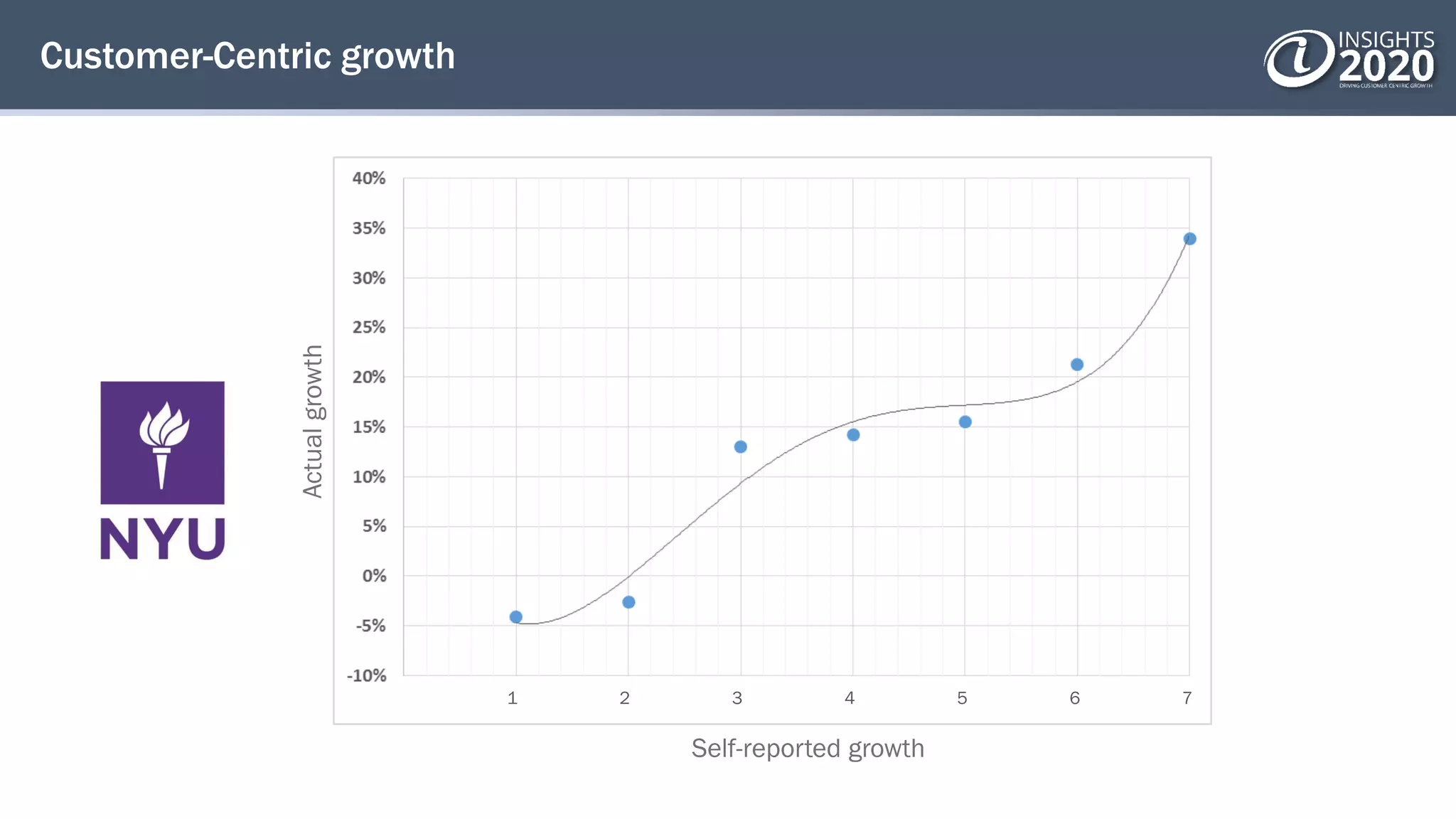

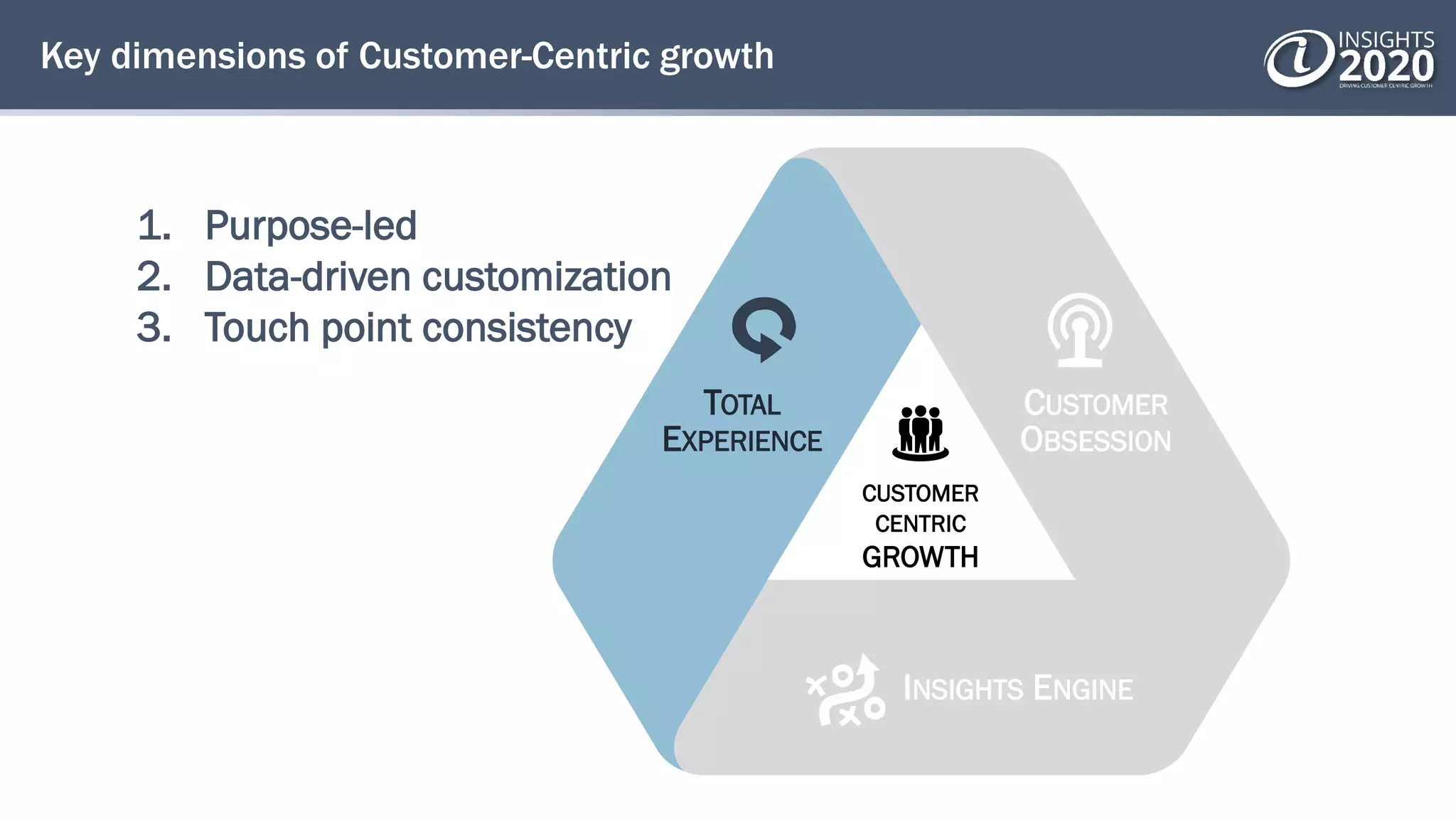

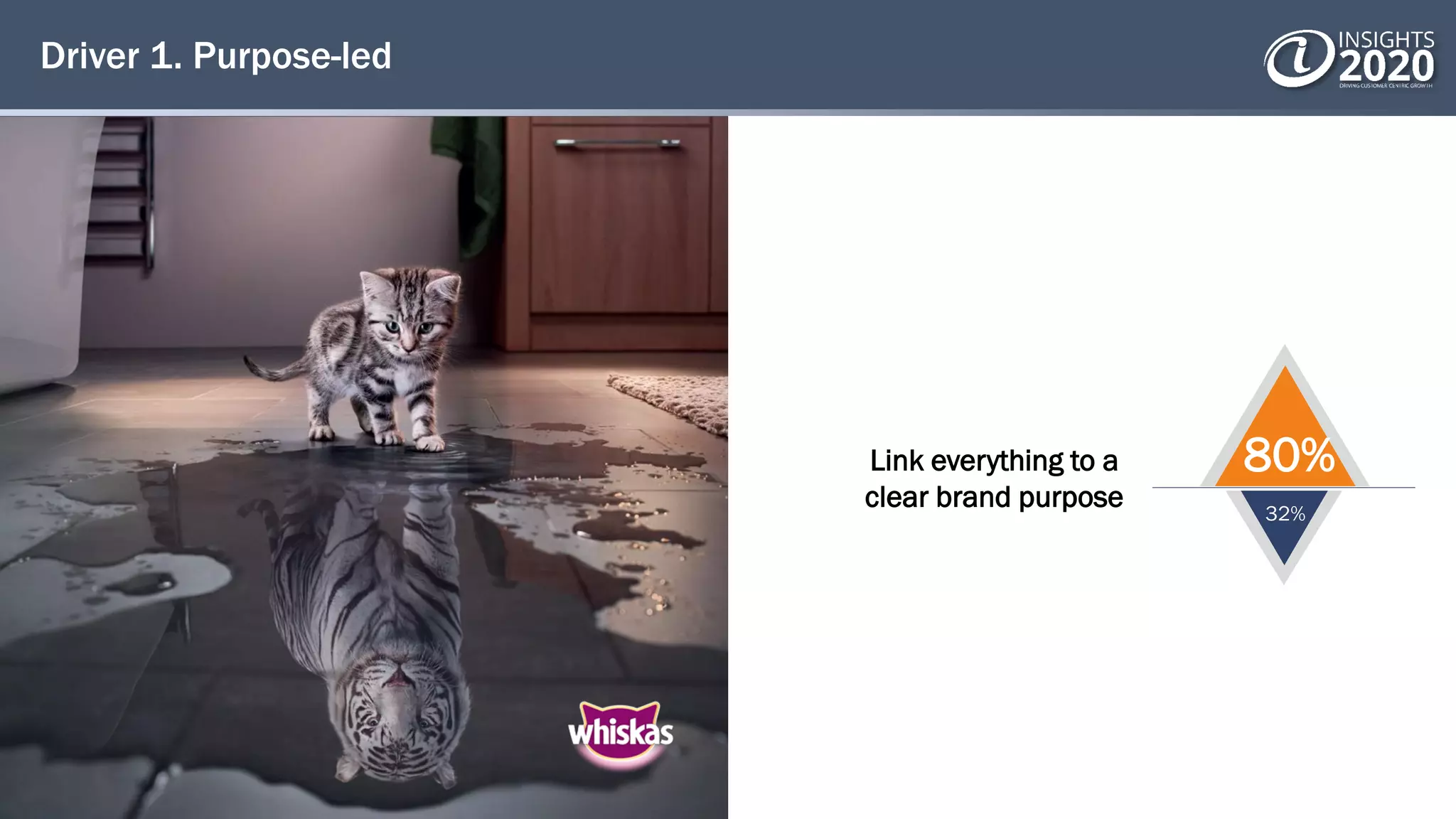

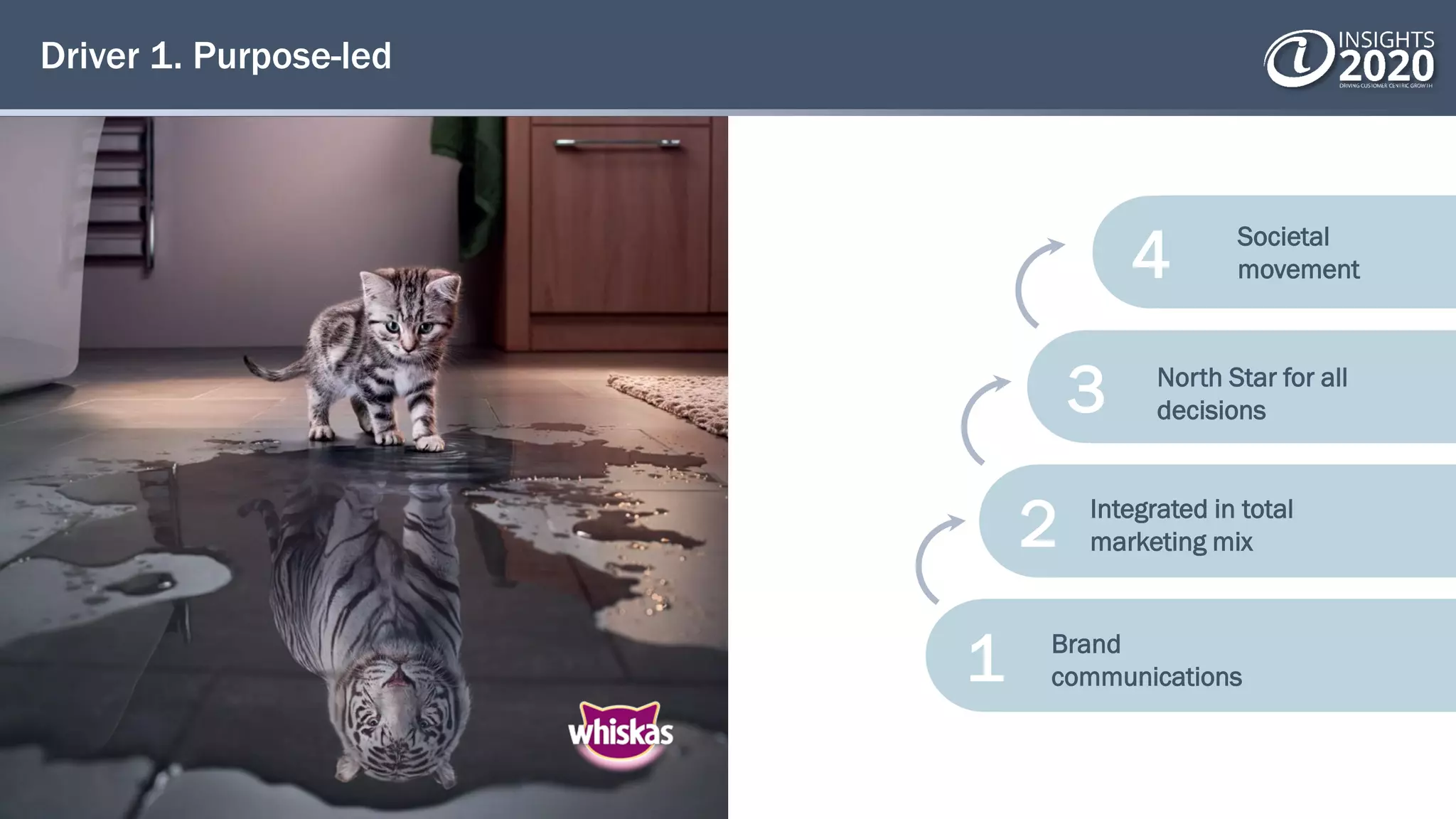

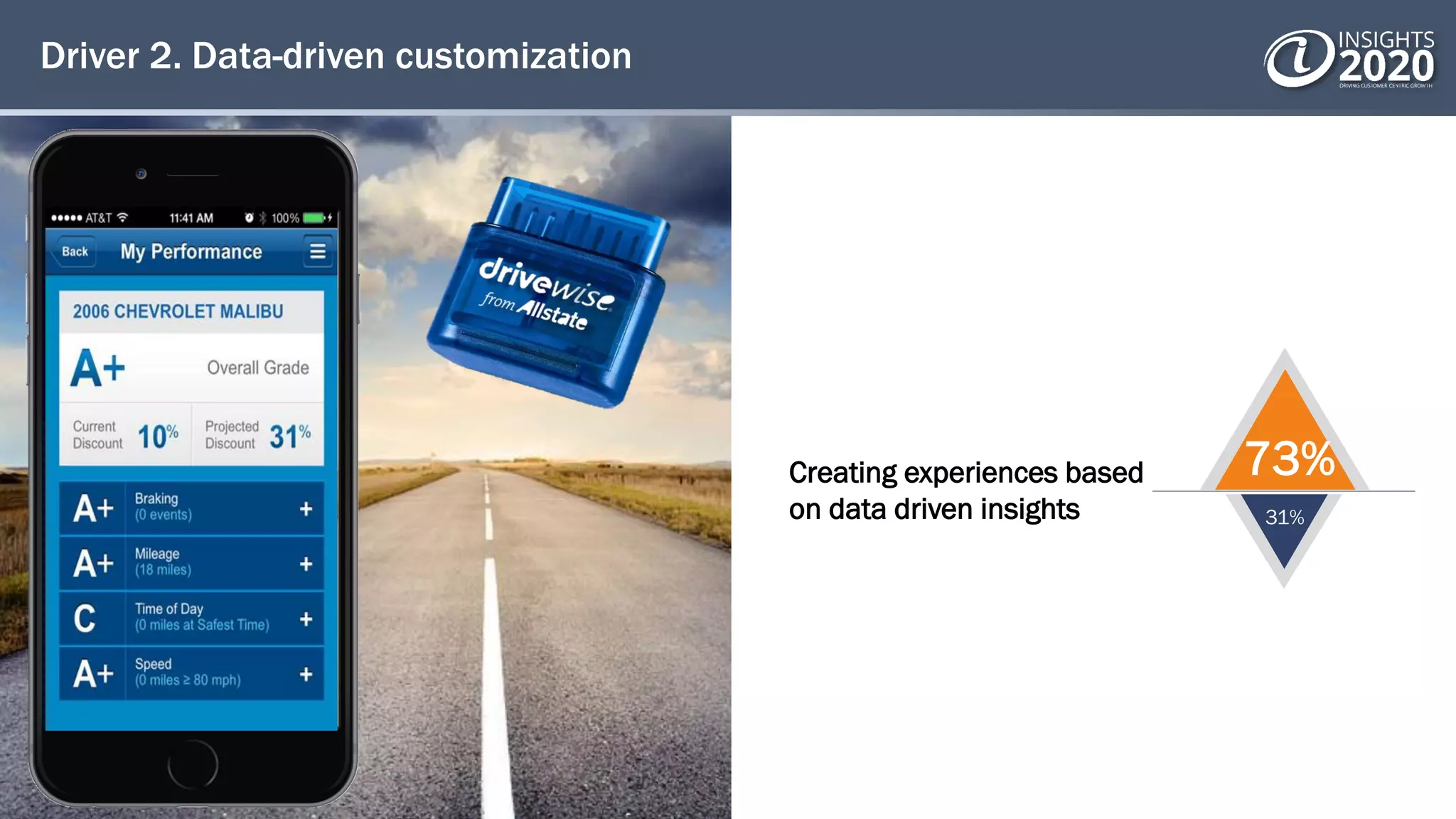

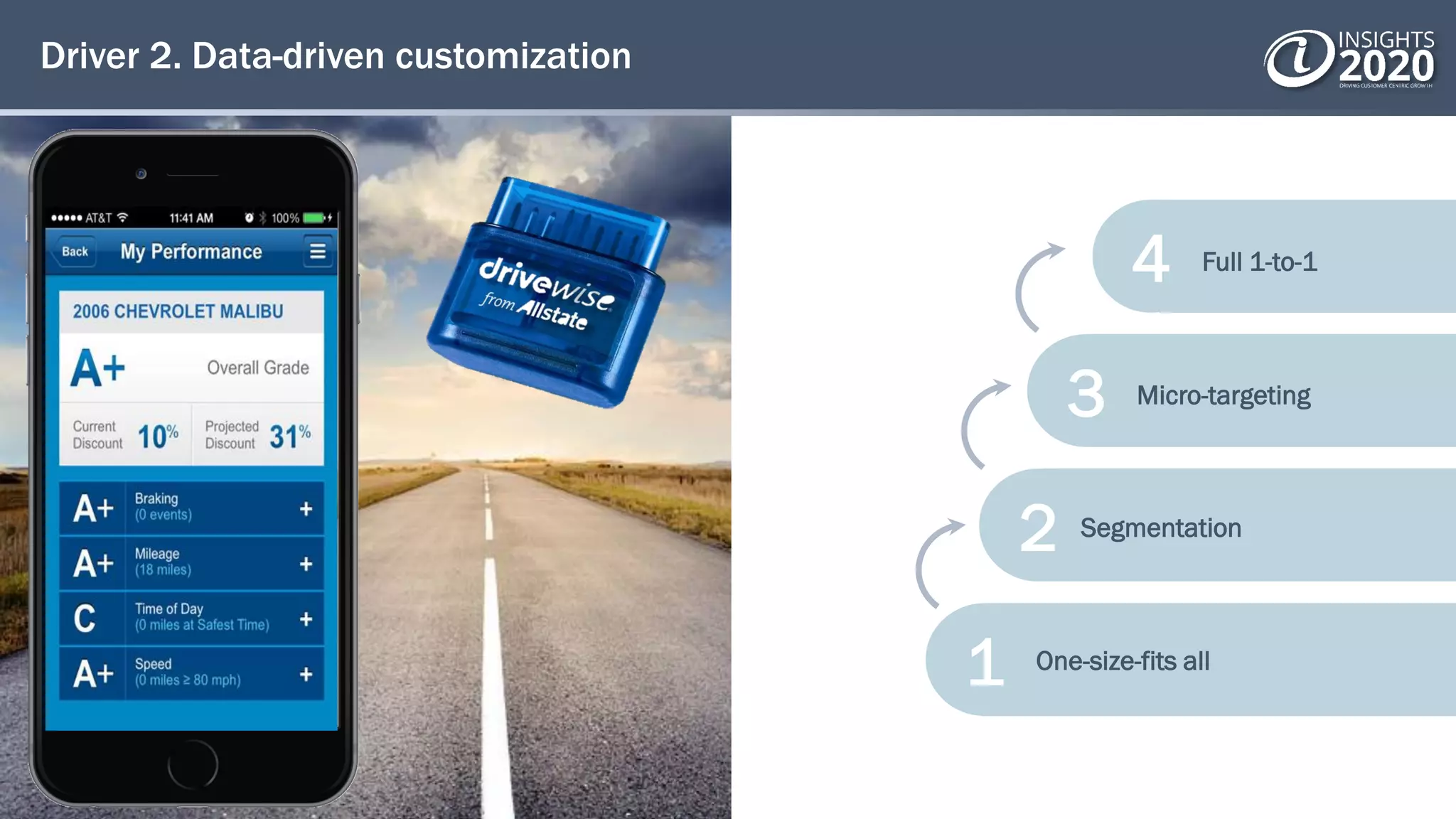

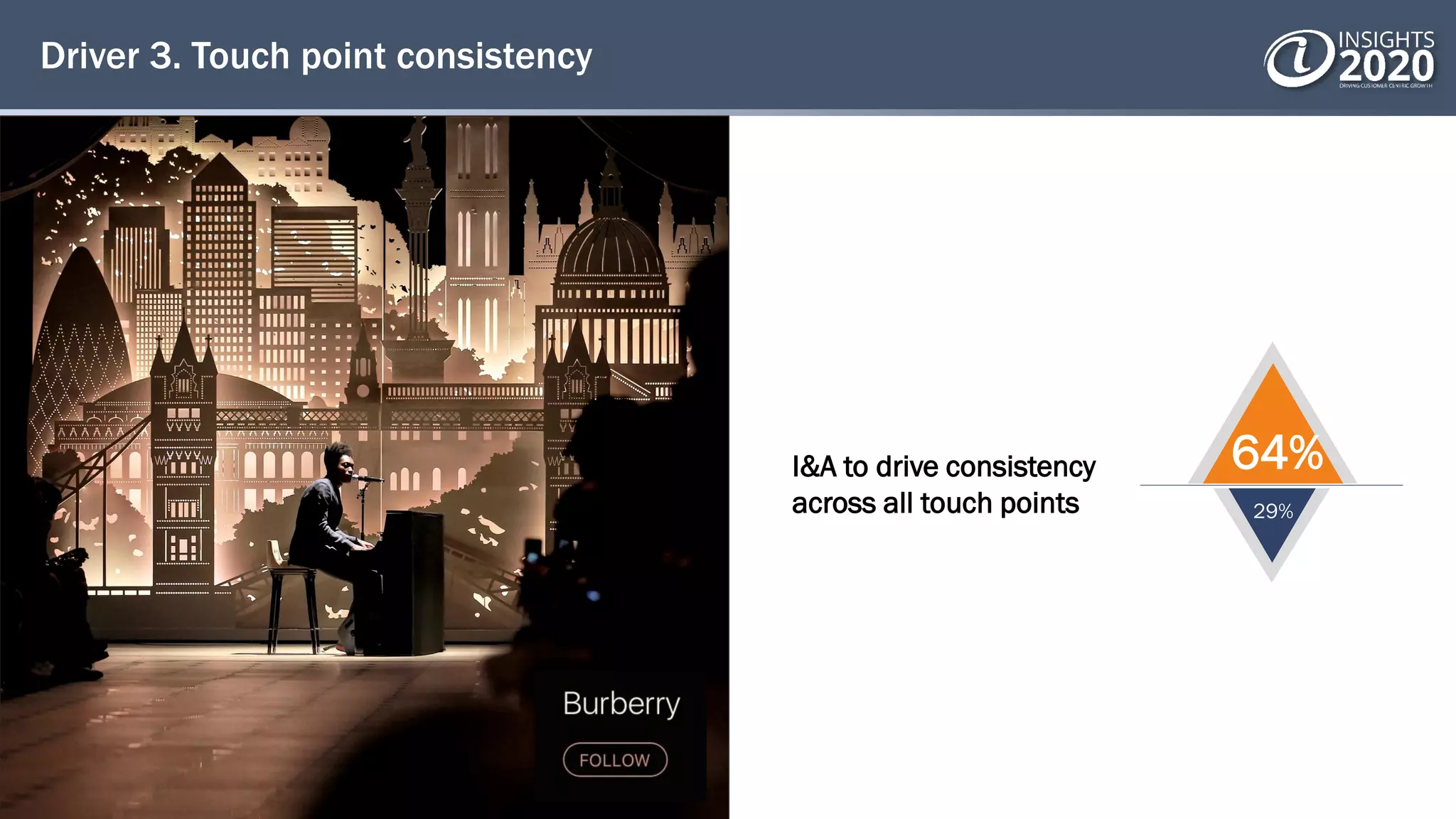

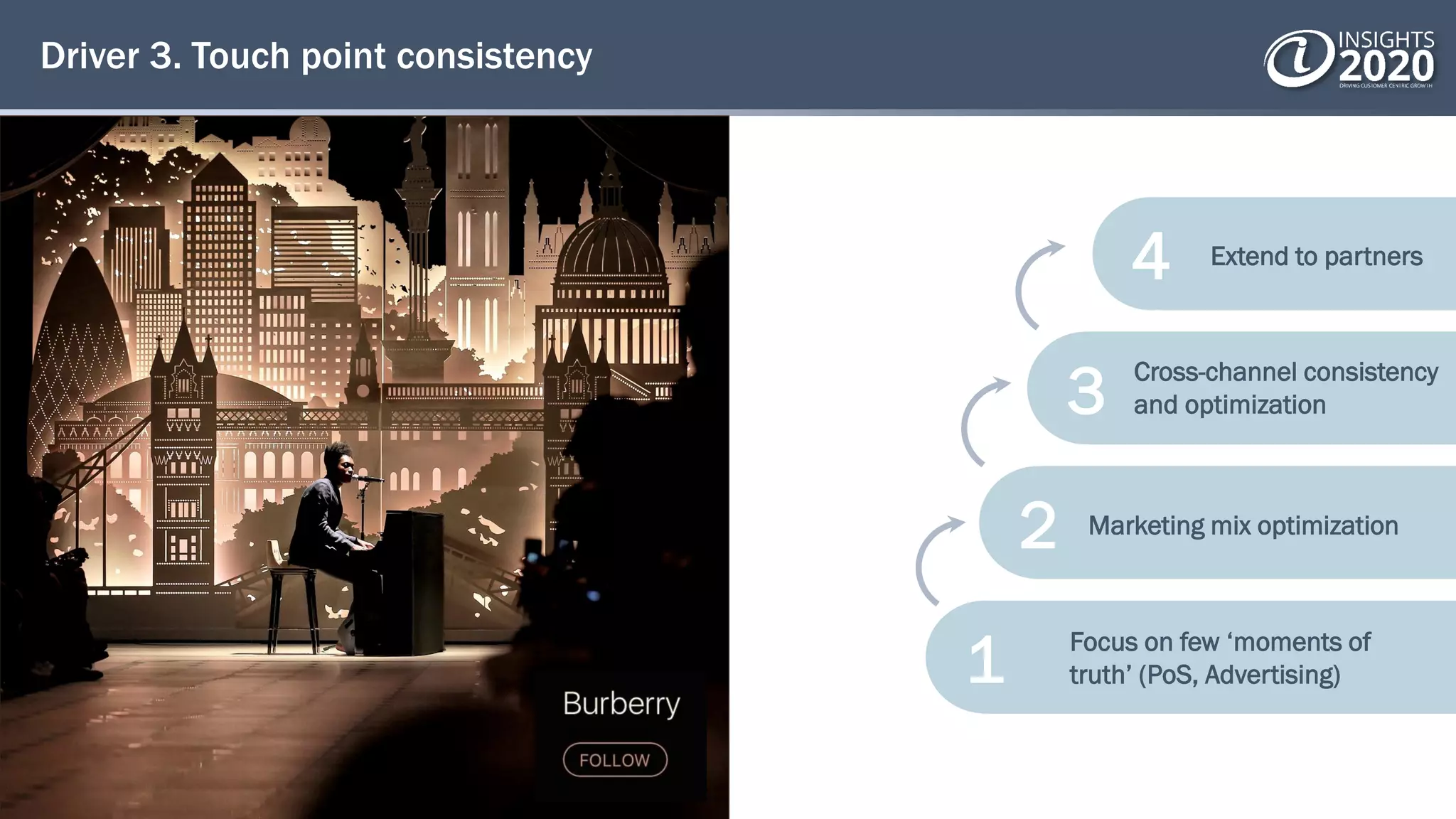

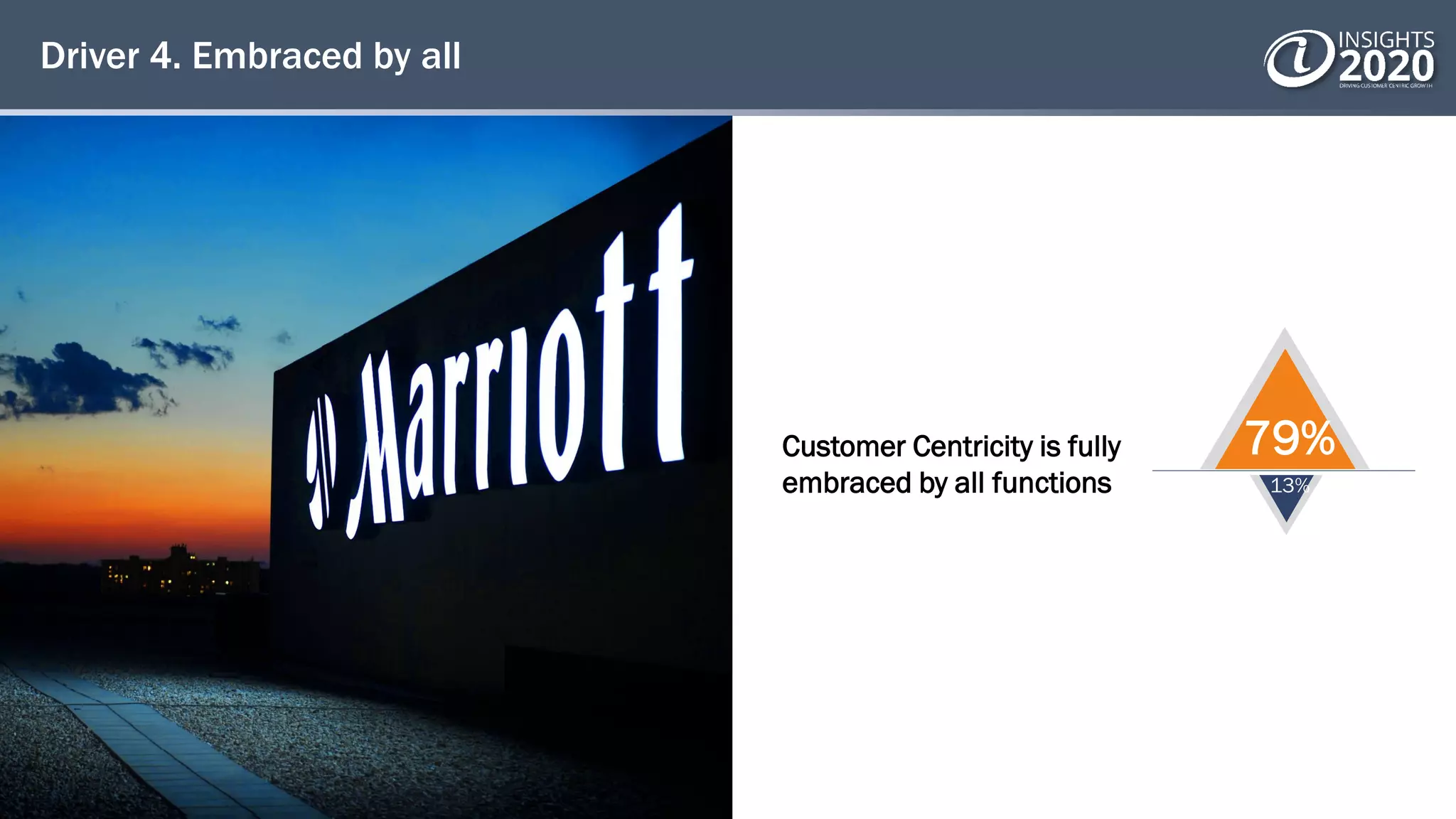

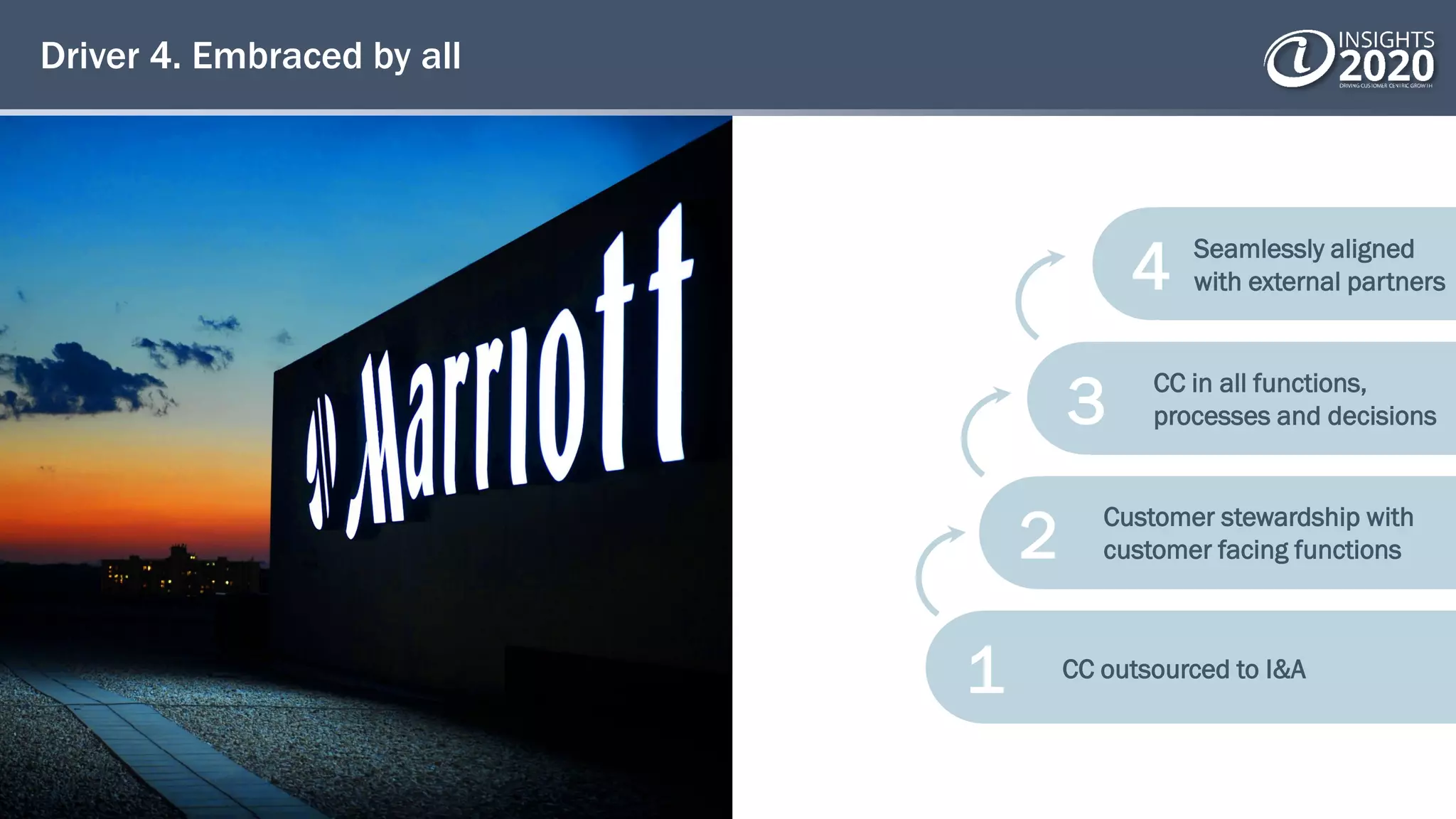

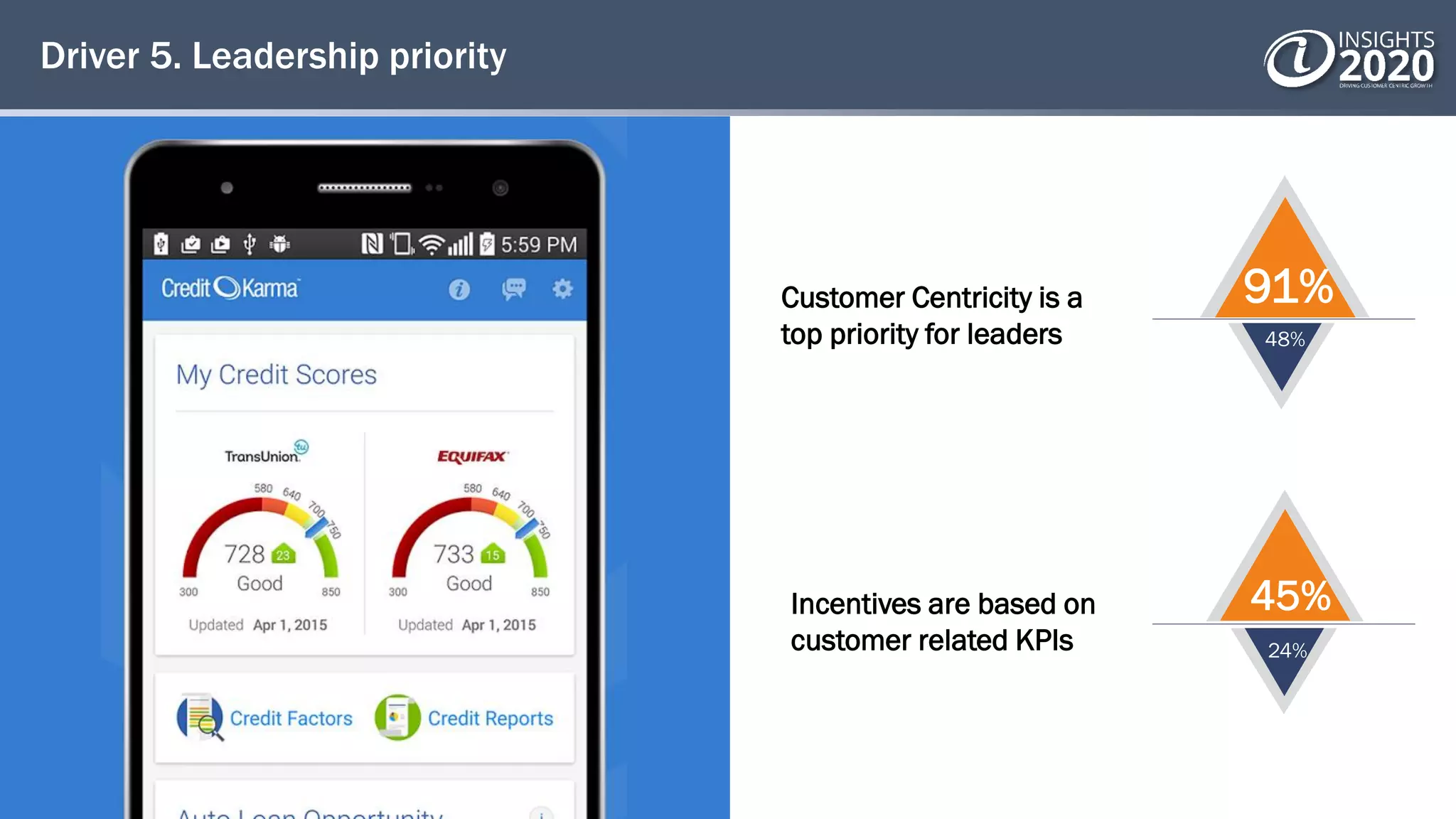

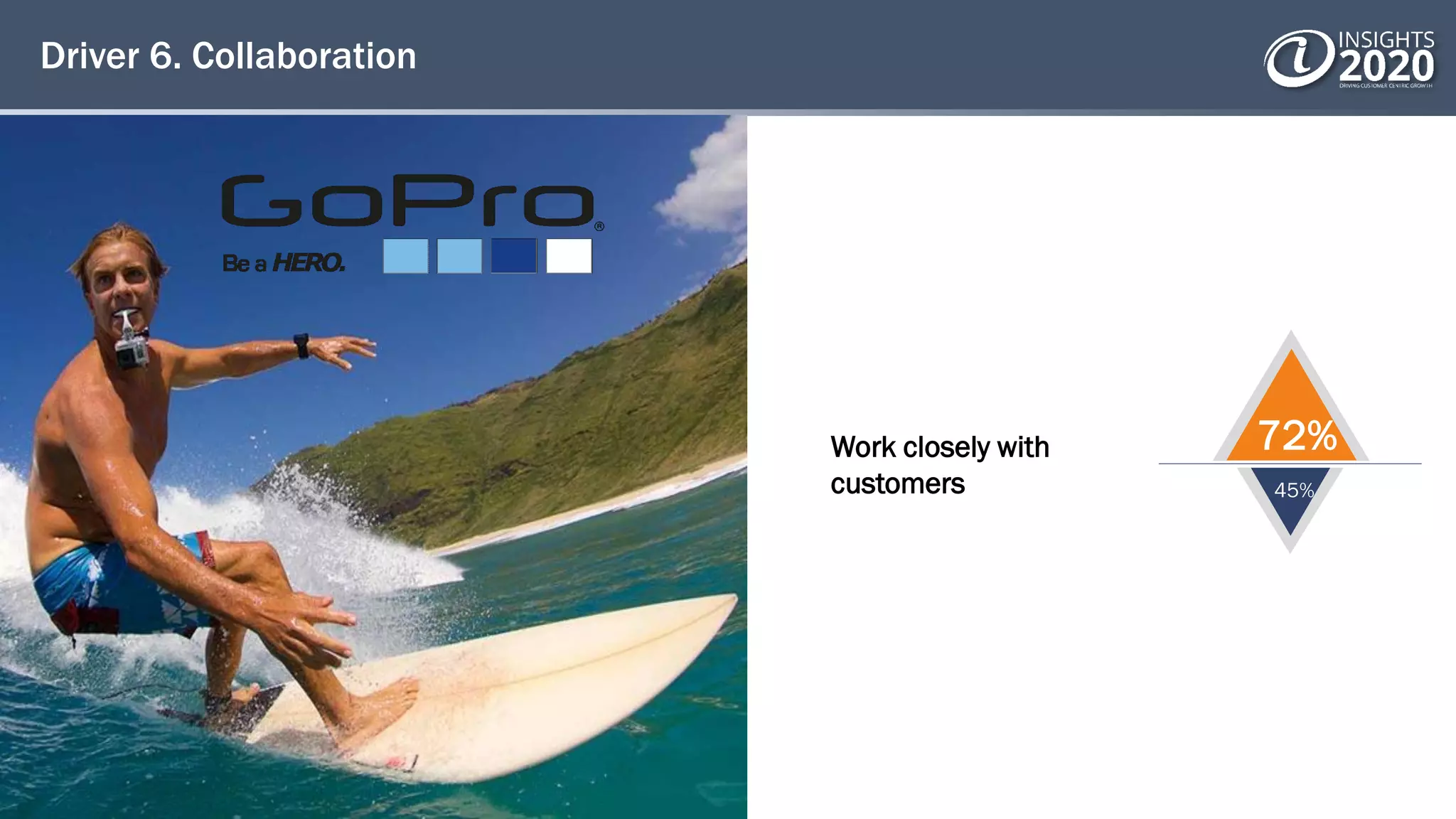

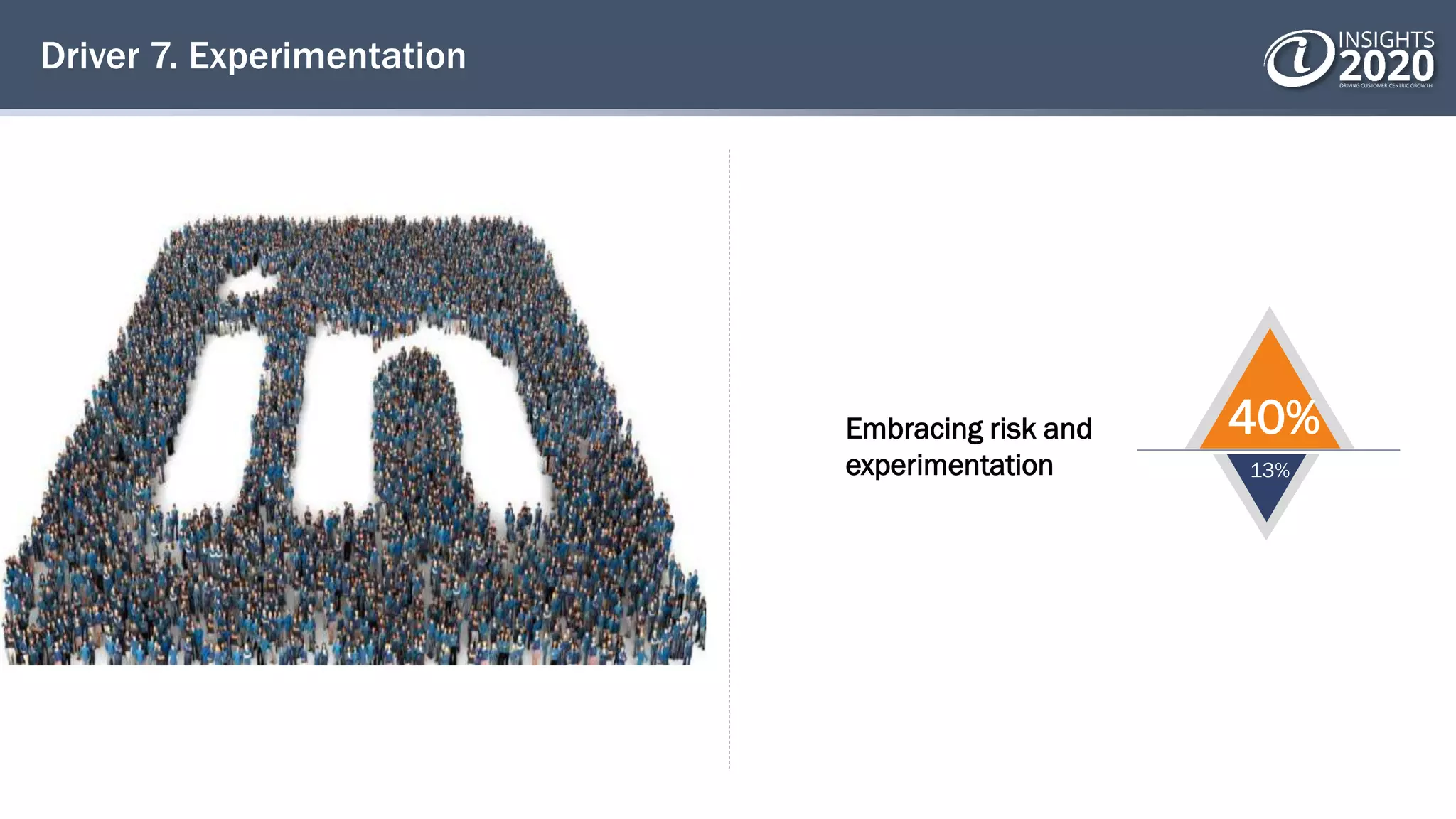

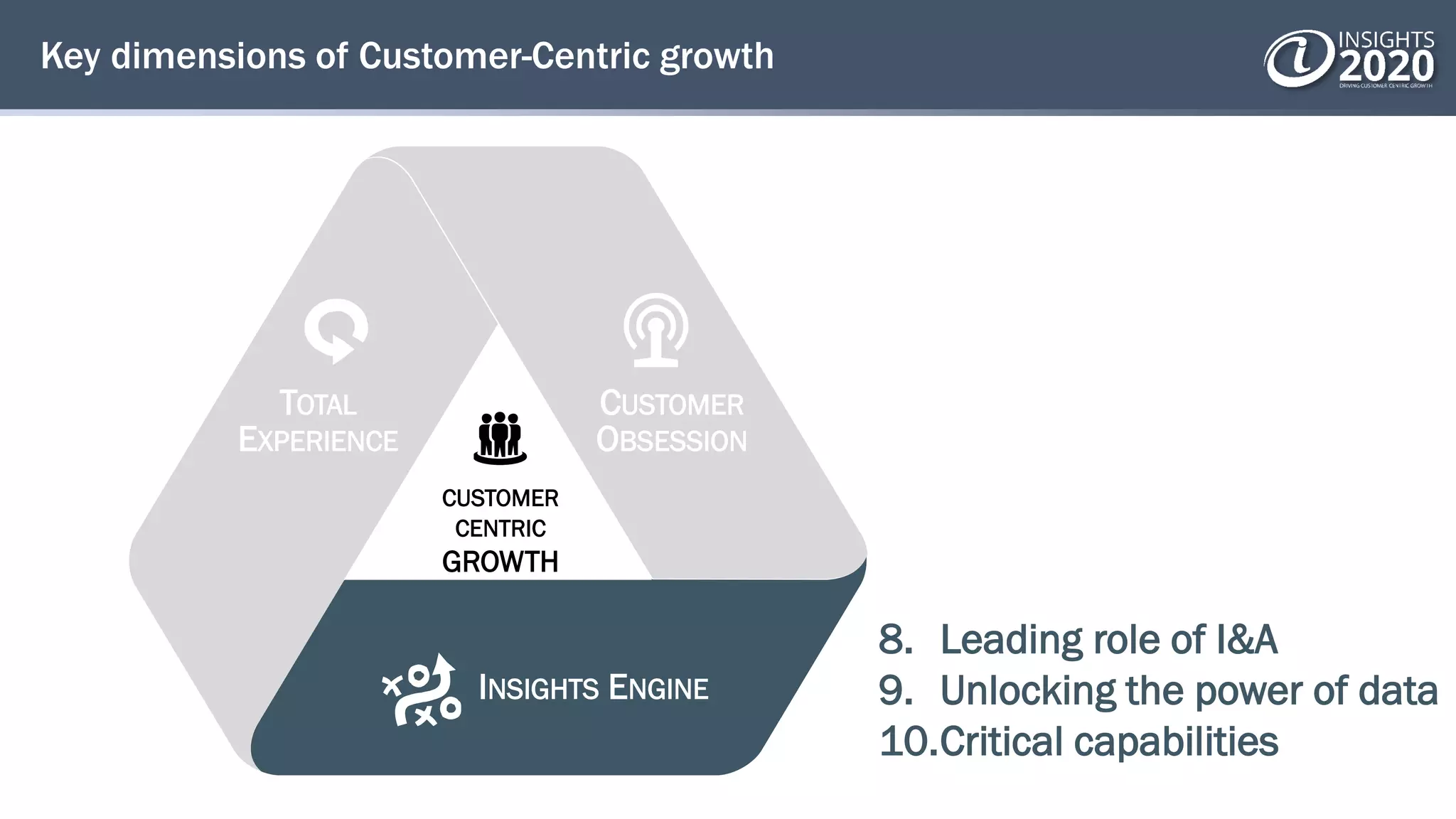

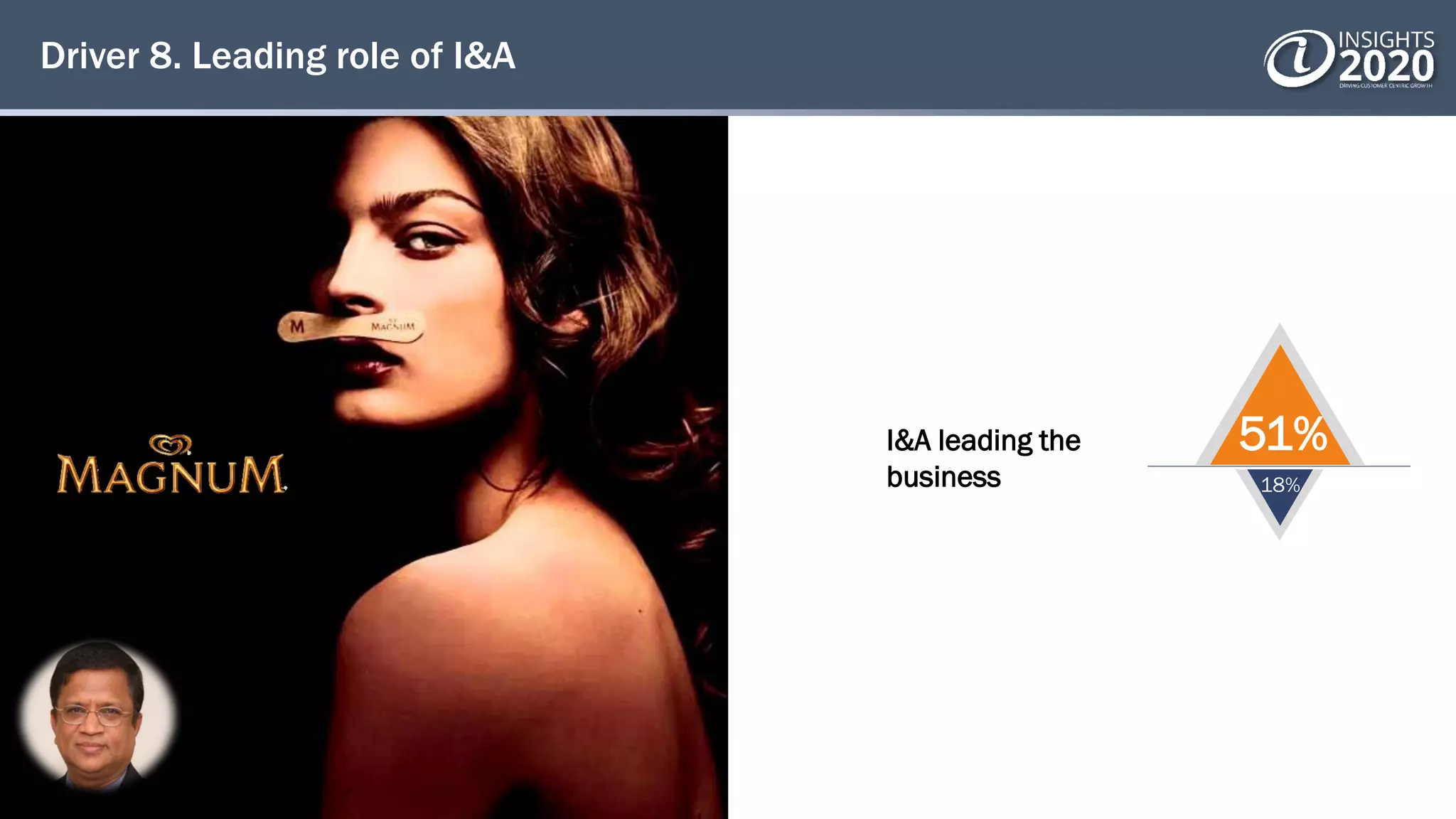

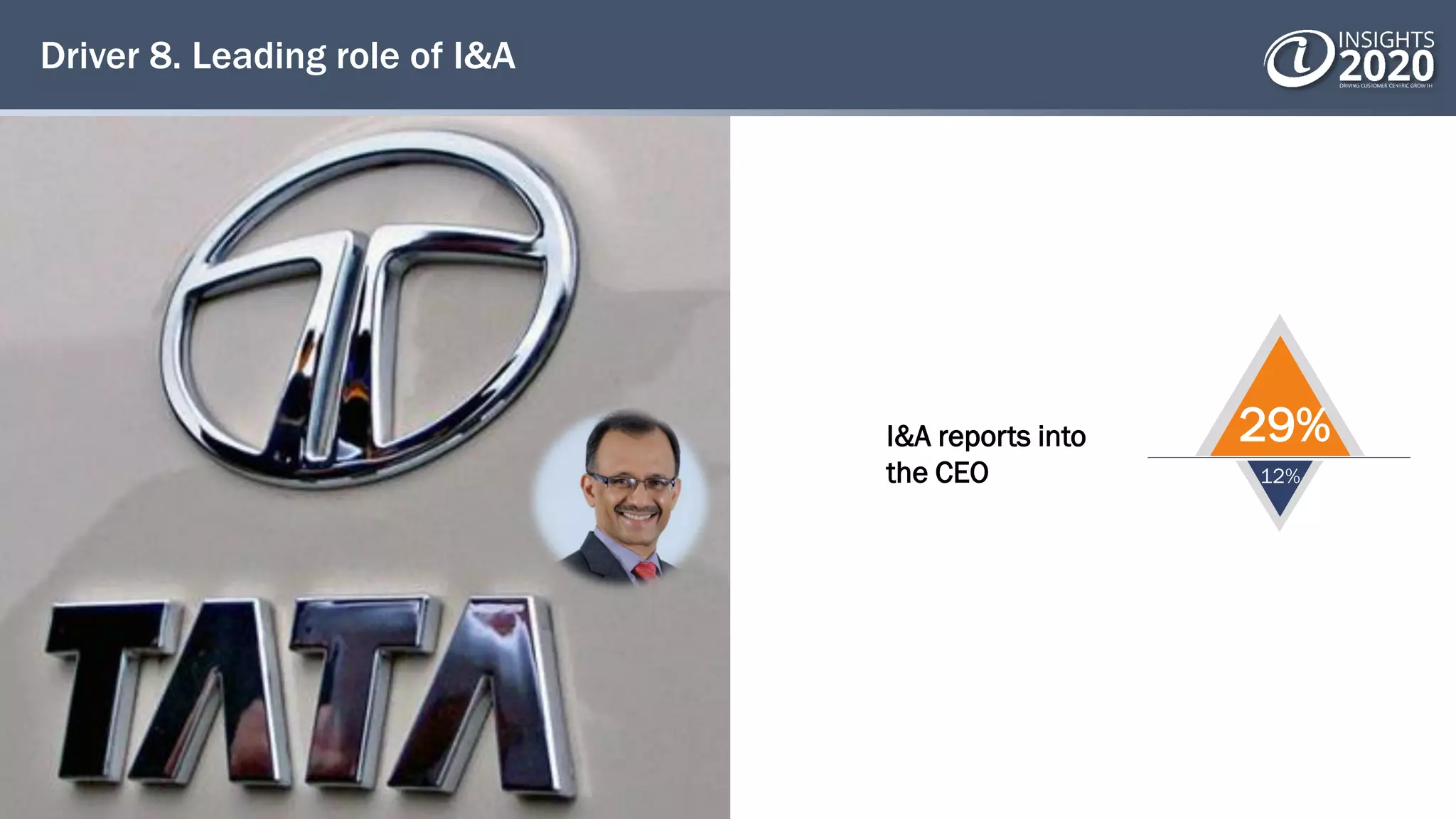

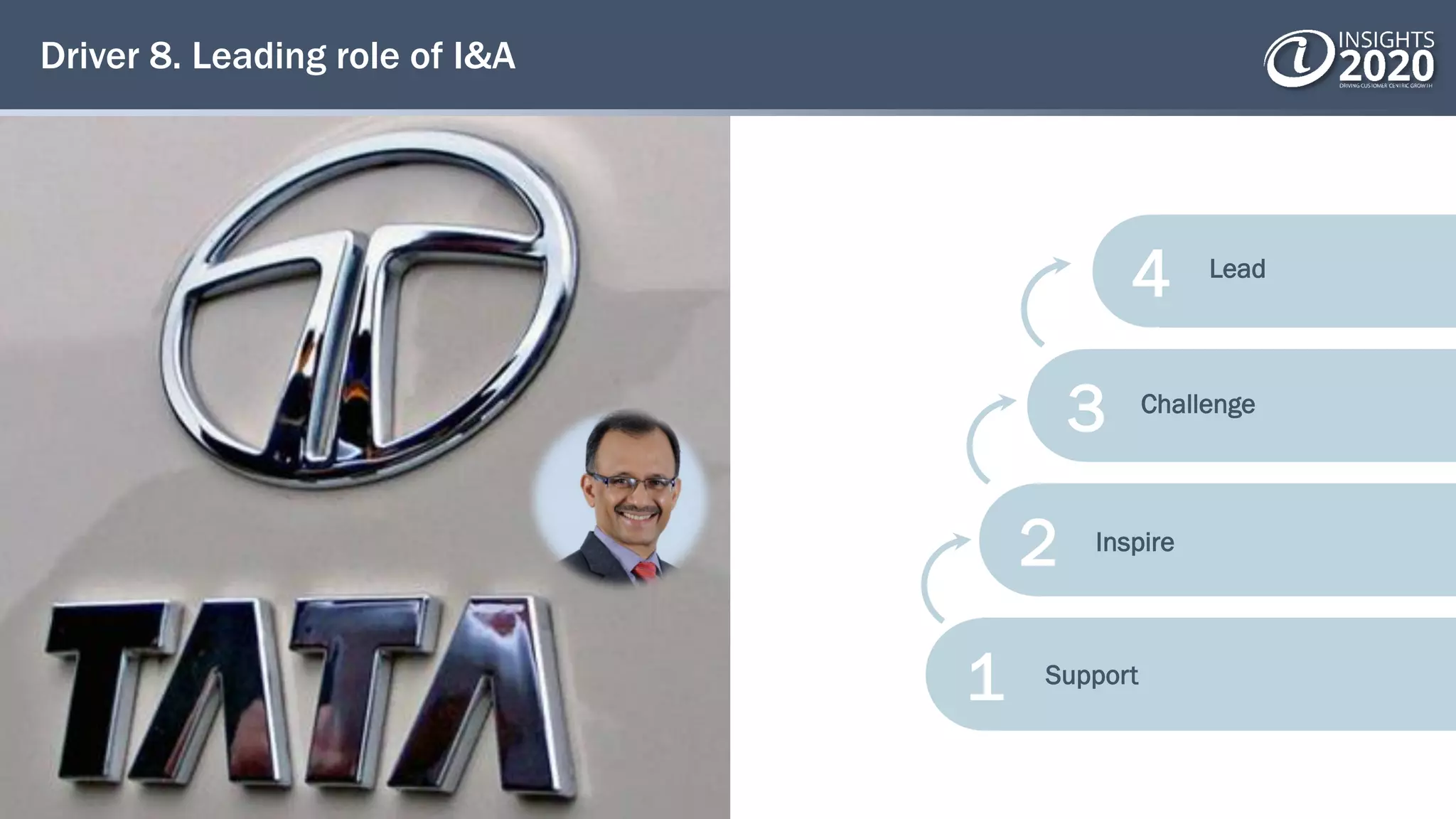

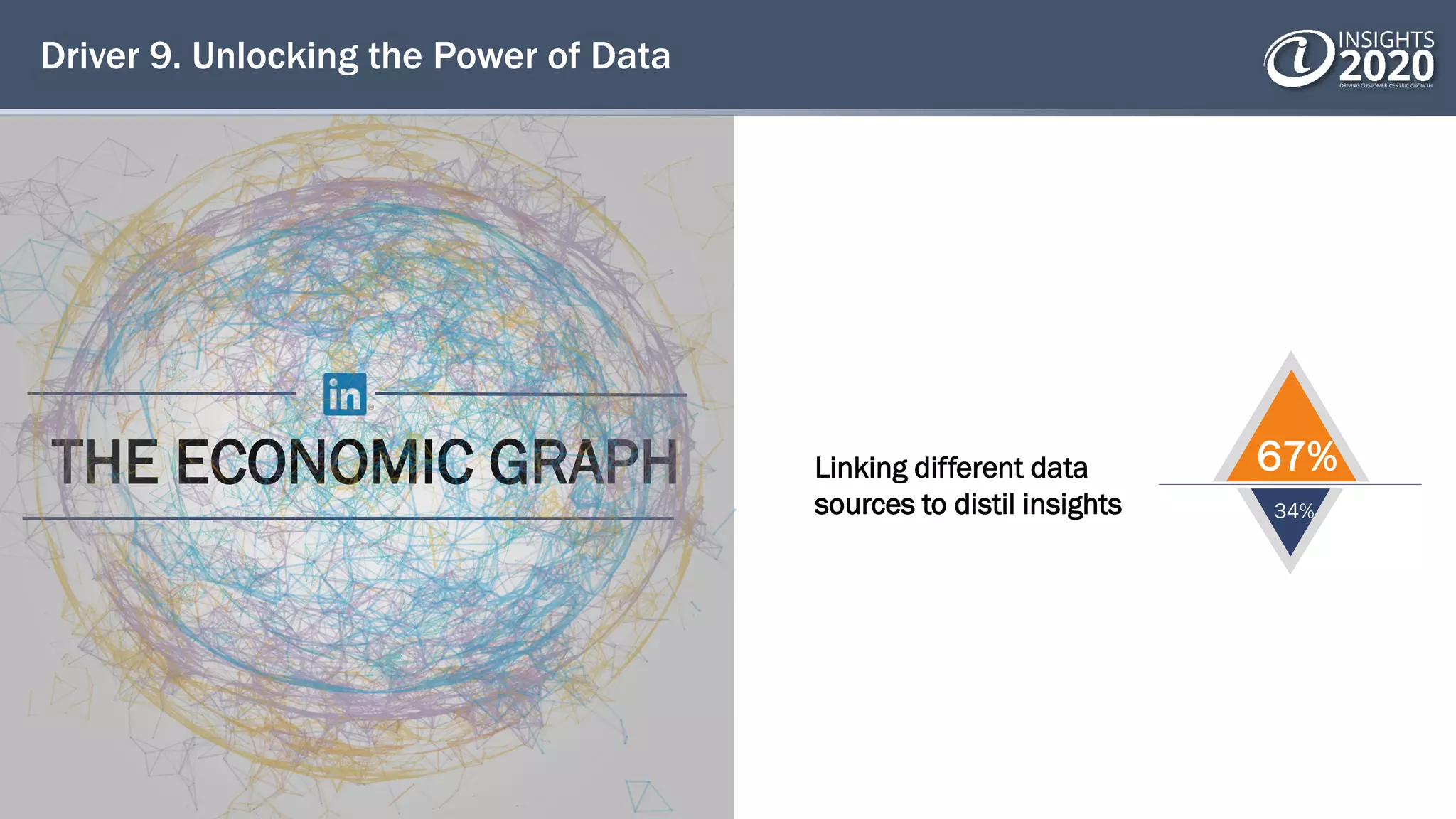

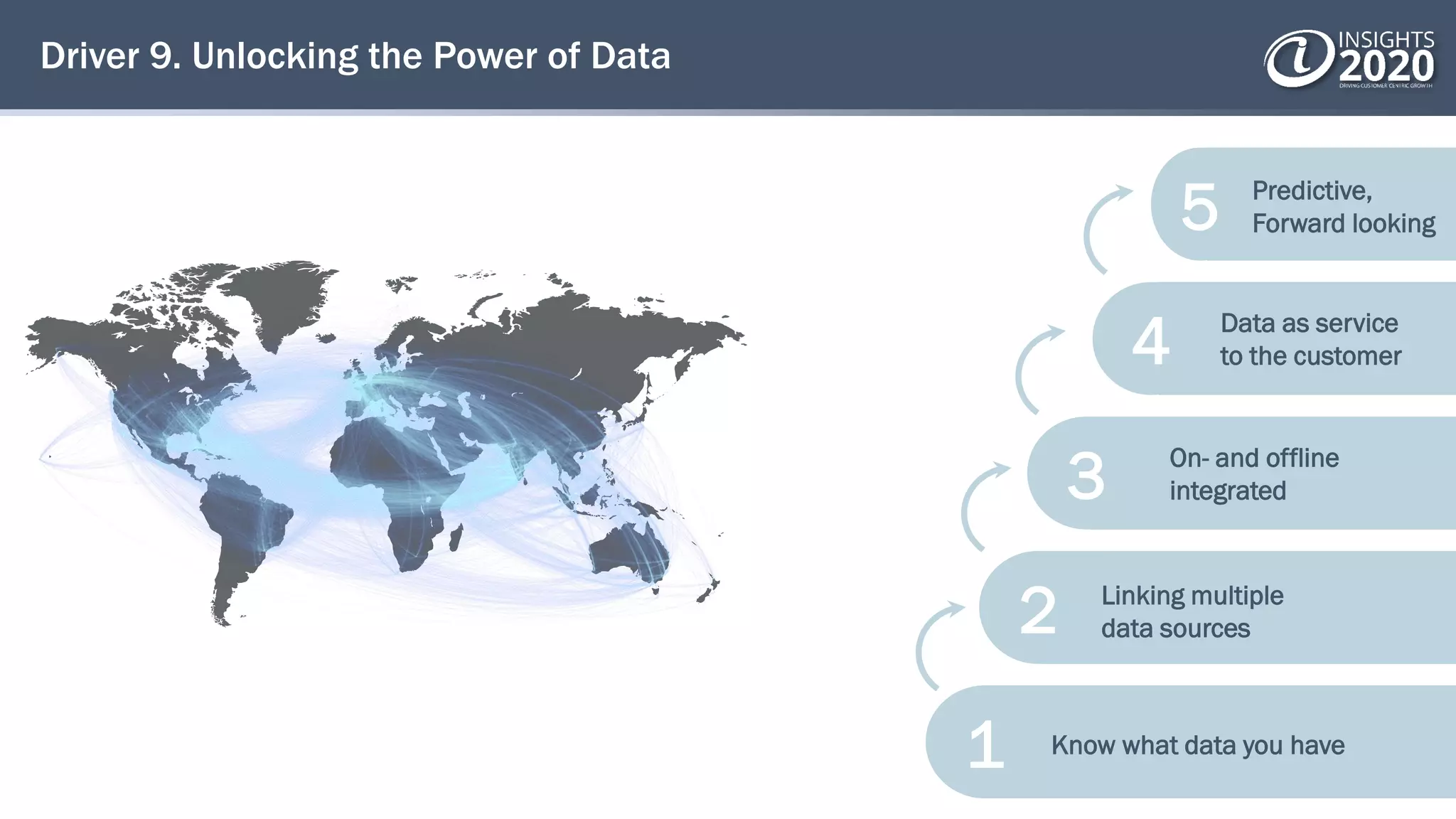

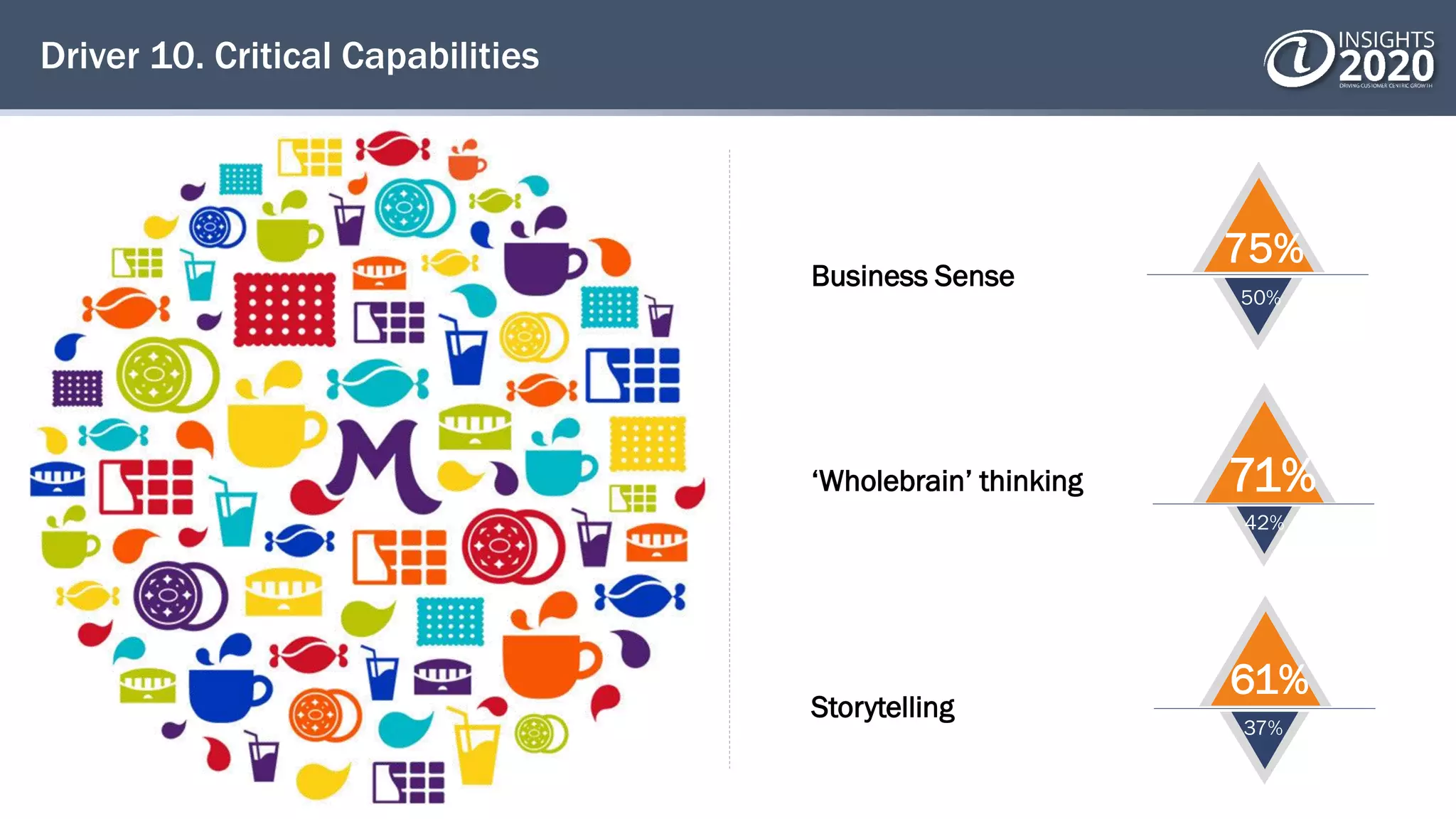

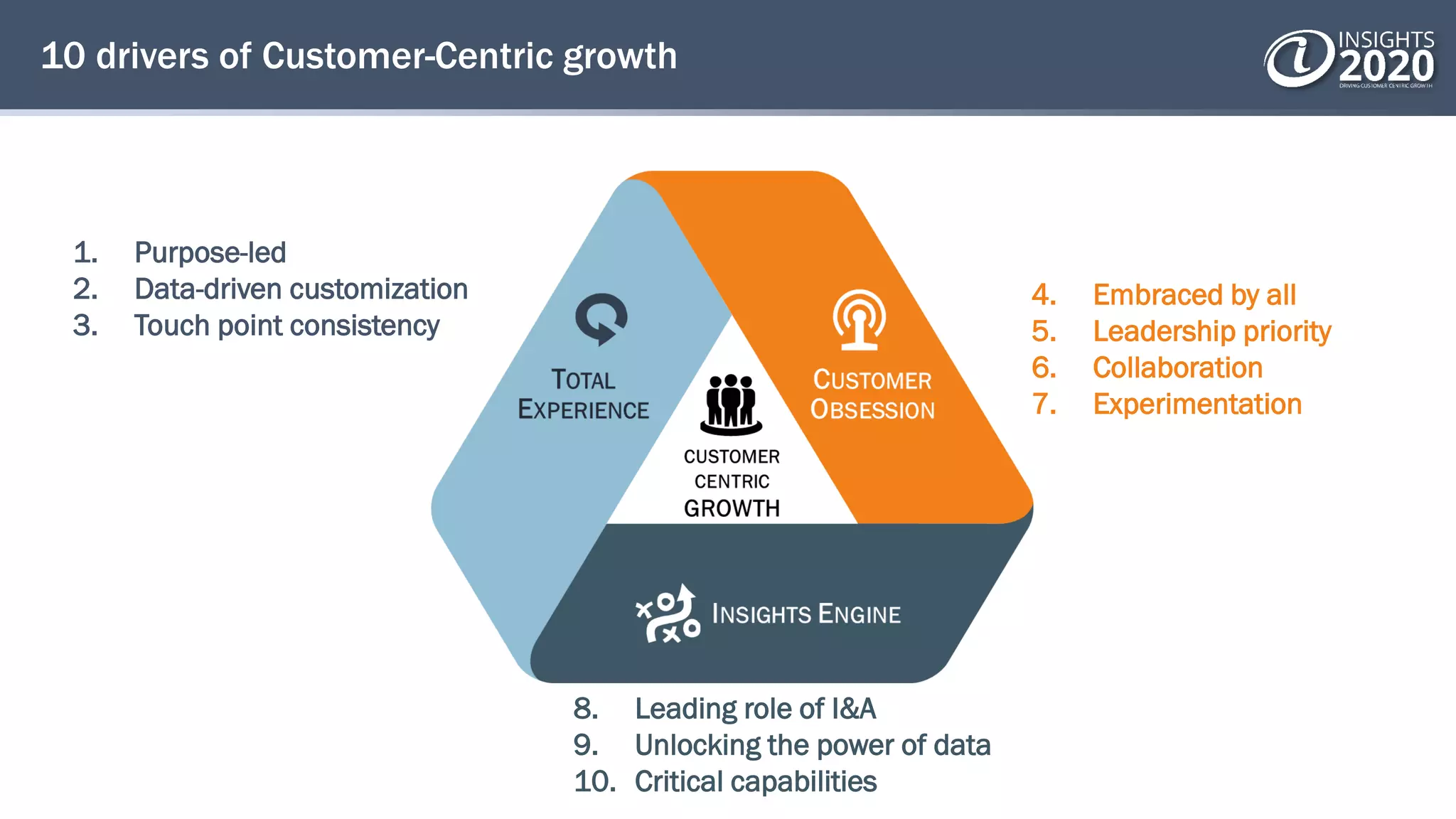

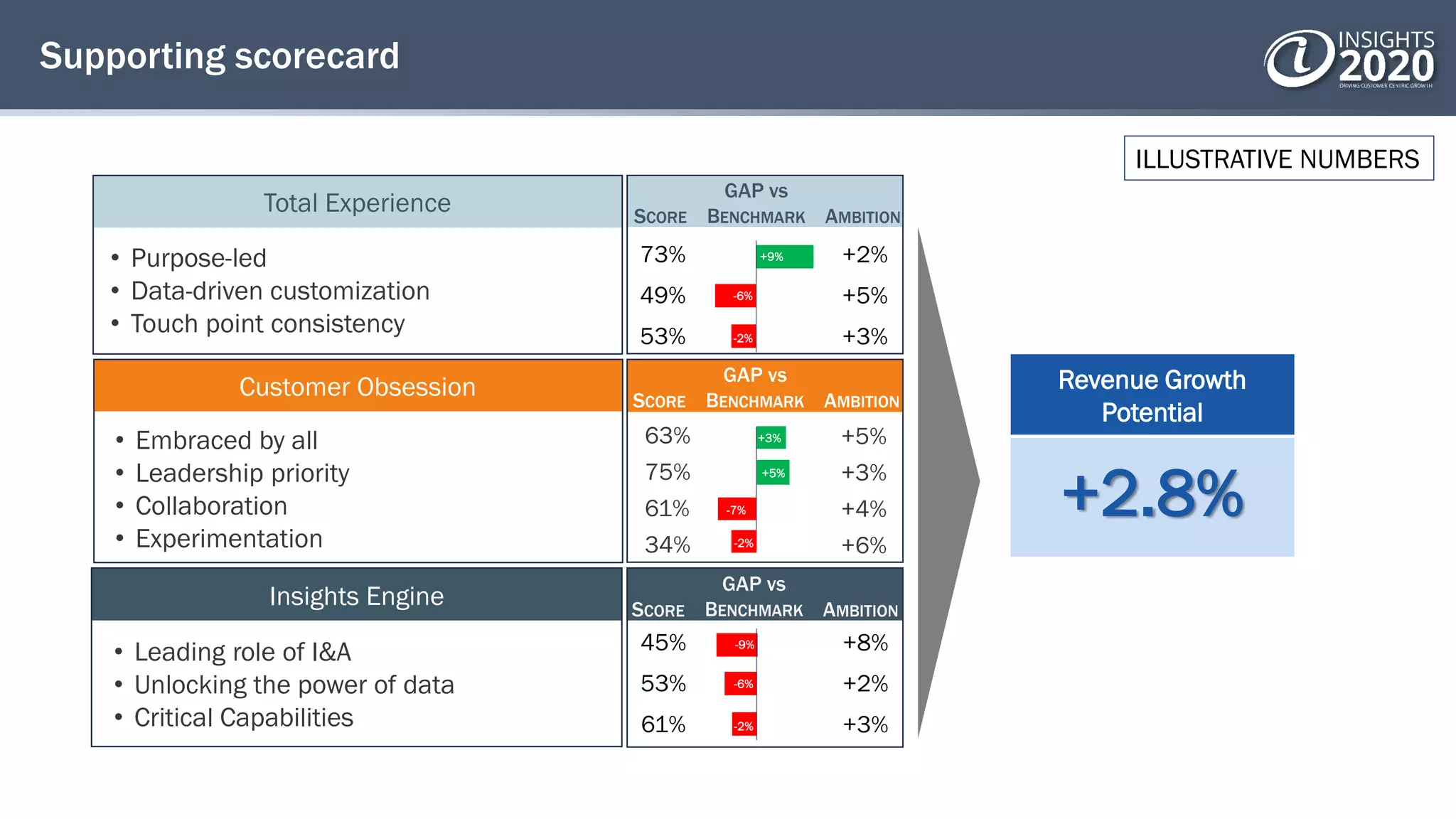

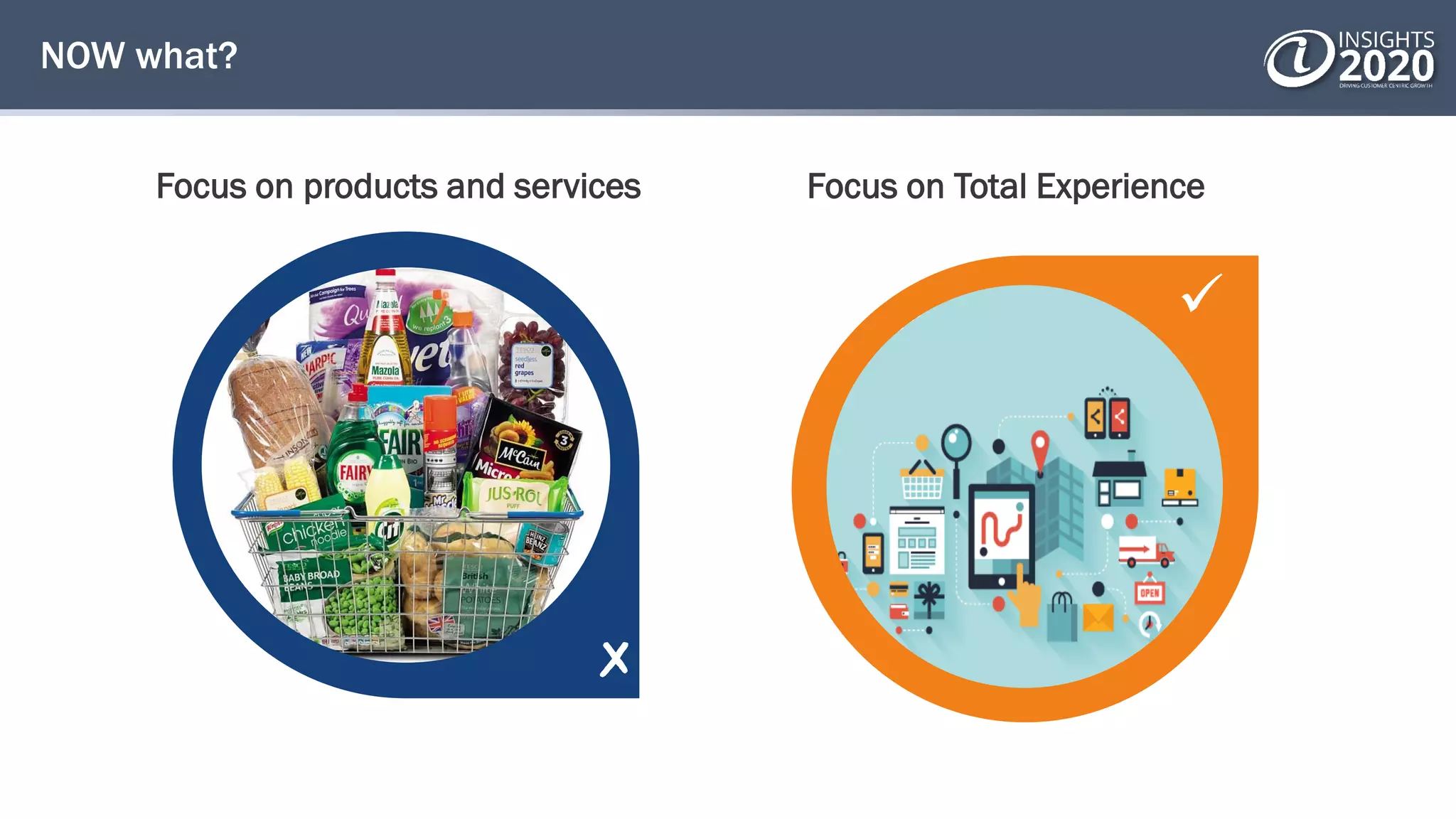

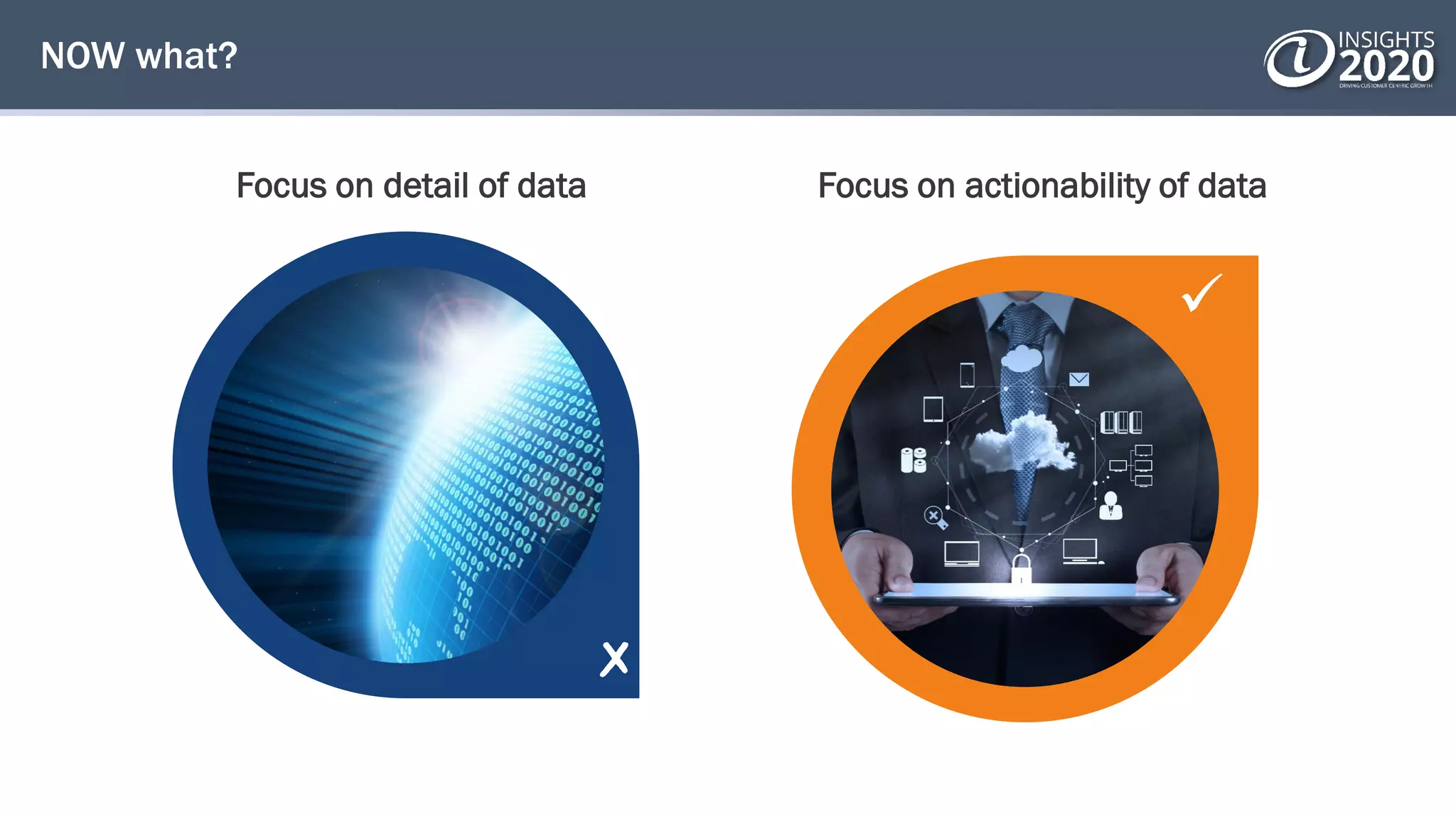

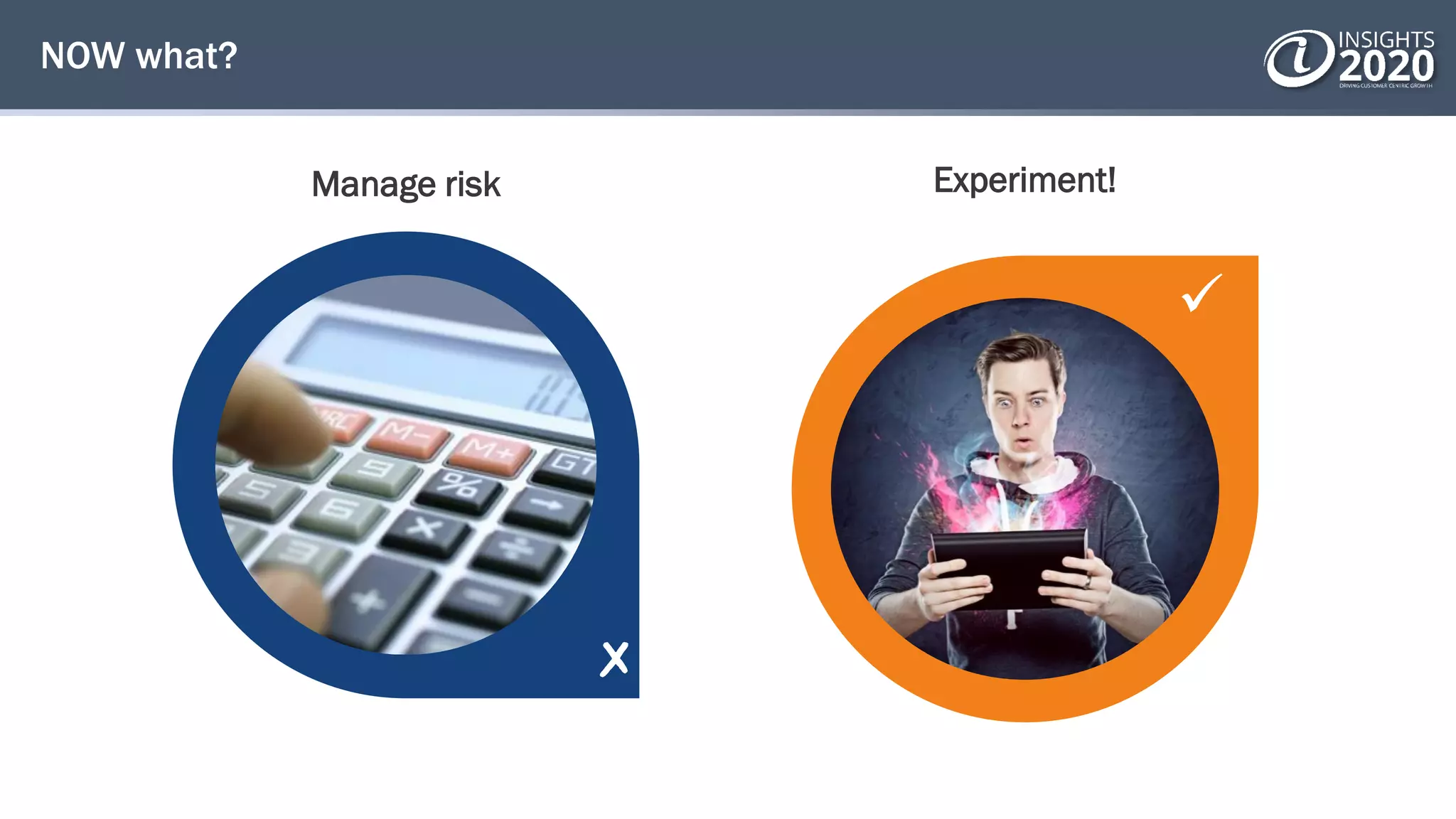

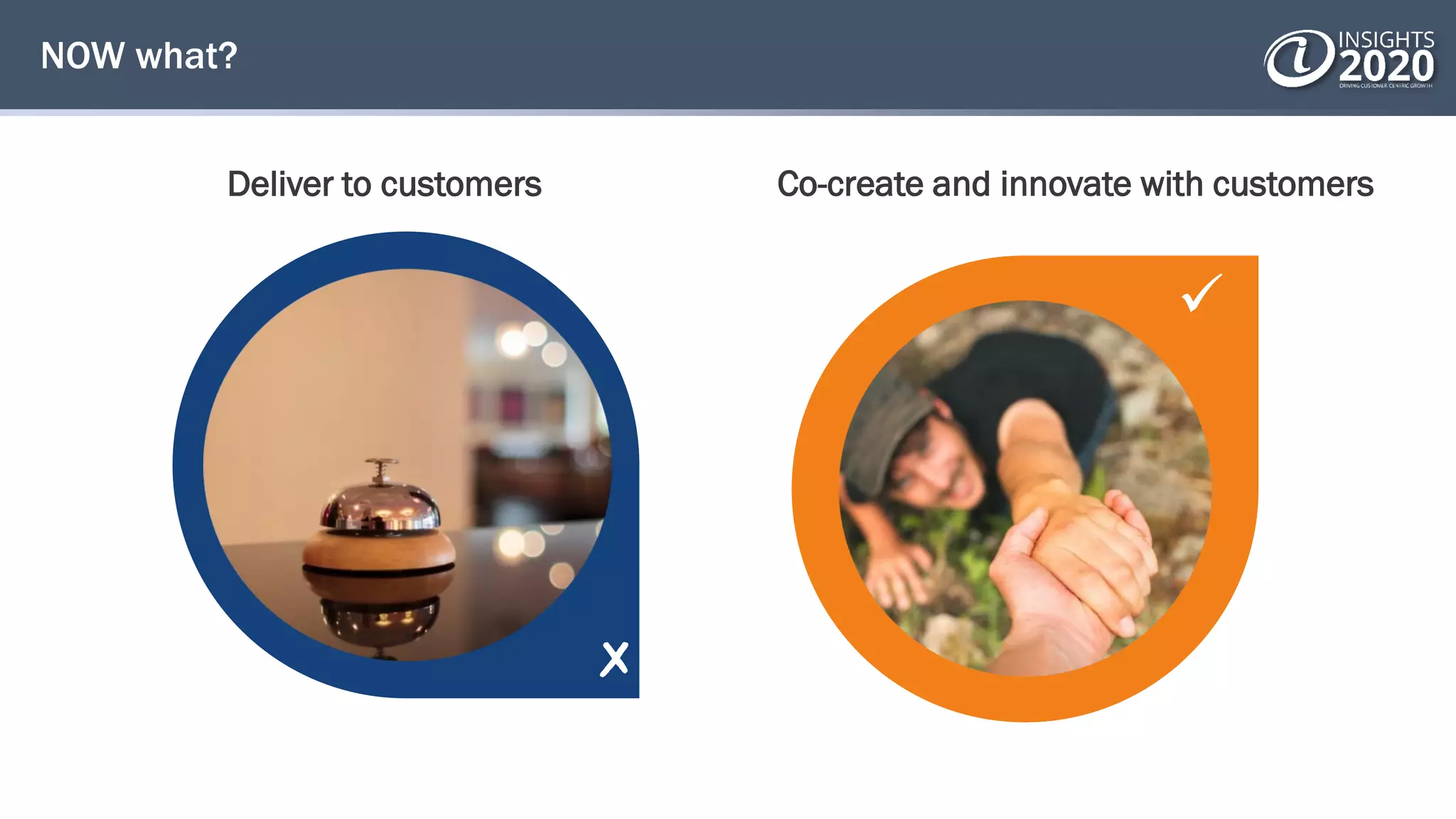

This document discusses driving customer-centric growth through connected experiences. It notes that traditional value drivers no longer provide competitive advantage in today's connected world. The document reports on a large global study examining how to achieve true customer centricity. It identifies 10 key drivers of customer-centric growth: having a clear brand purpose, data-driven customization, touchpoint consistency, company-wide embrace, leadership priority, collaboration, experimentation, the leading role of insights and analytics, unlocking data's power, and developing critical capabilities like storytelling. Achieving these 10 drivers can boost revenue growth by focusing on total customer experience.

![[Skale] an HR centric Scrum Process](https://cdn.slidesharecdn.com/ss_thumbnails/skalepublicationv22-110211081128-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Improving CX with AI: Microsoft Case Study [SiriusDecisions Summit 2017]](https://cdn.slidesharecdn.com/ss_thumbnails/improvingcxwithai-microsoftcasestudysiriusdecisionssummit2017-170523005614-thumbnail.jpg?width=640&height=640&fit=bounds)

![2014 bz lat_am report_final[1]](https://cdn.slidesharecdn.com/ss_thumbnails/2014bzlatamreportfinal1-140925232324-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)