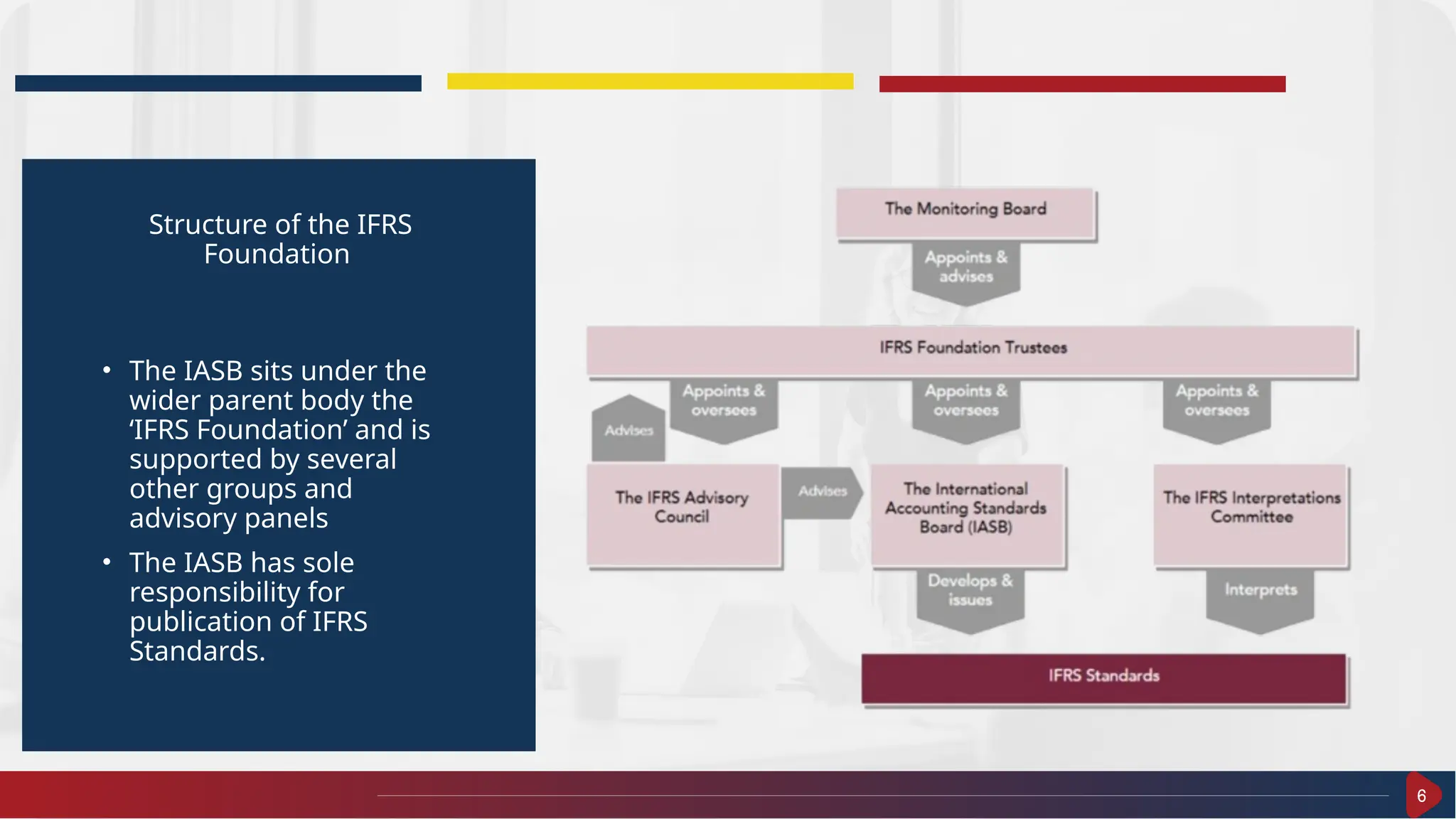

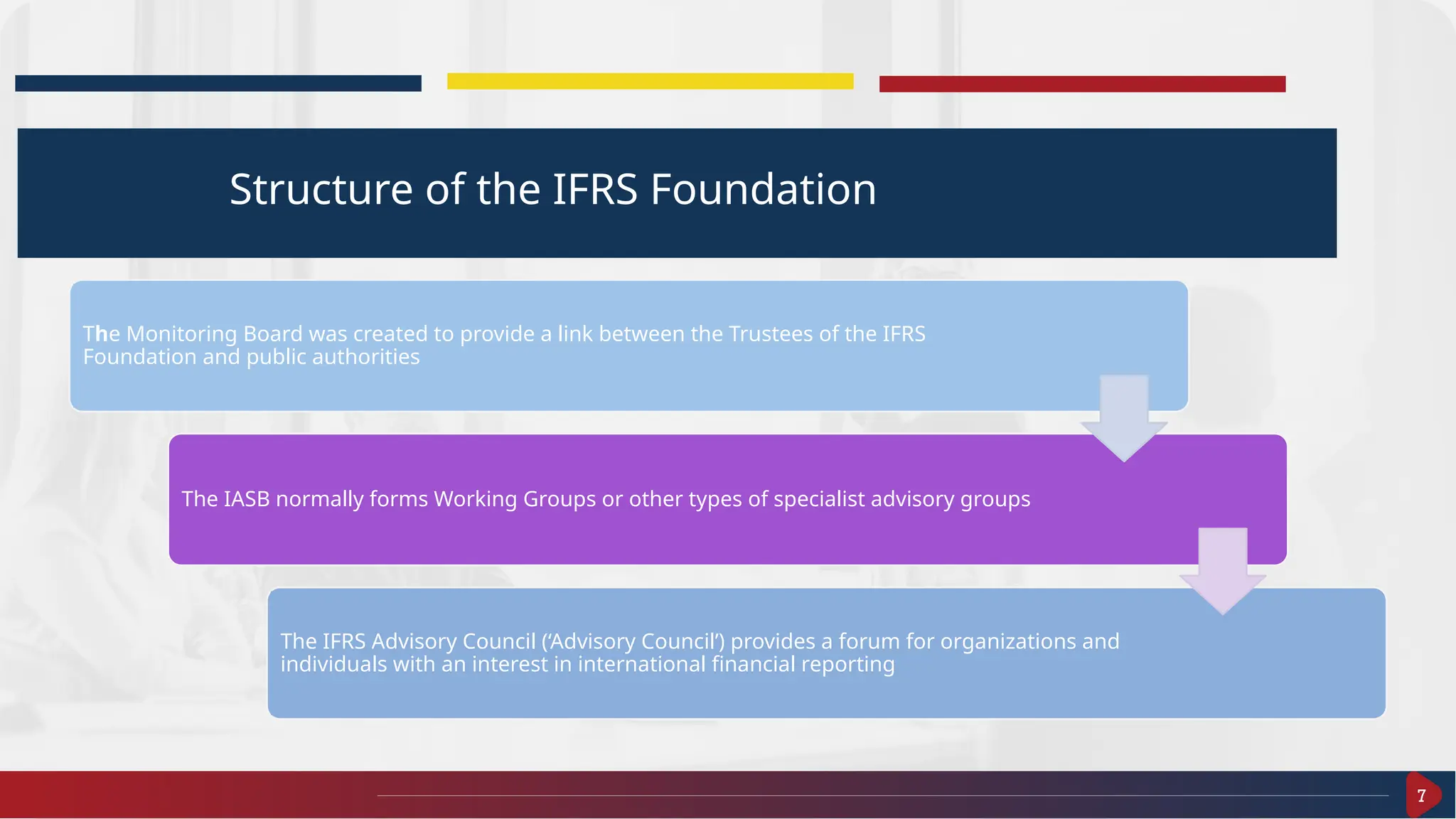

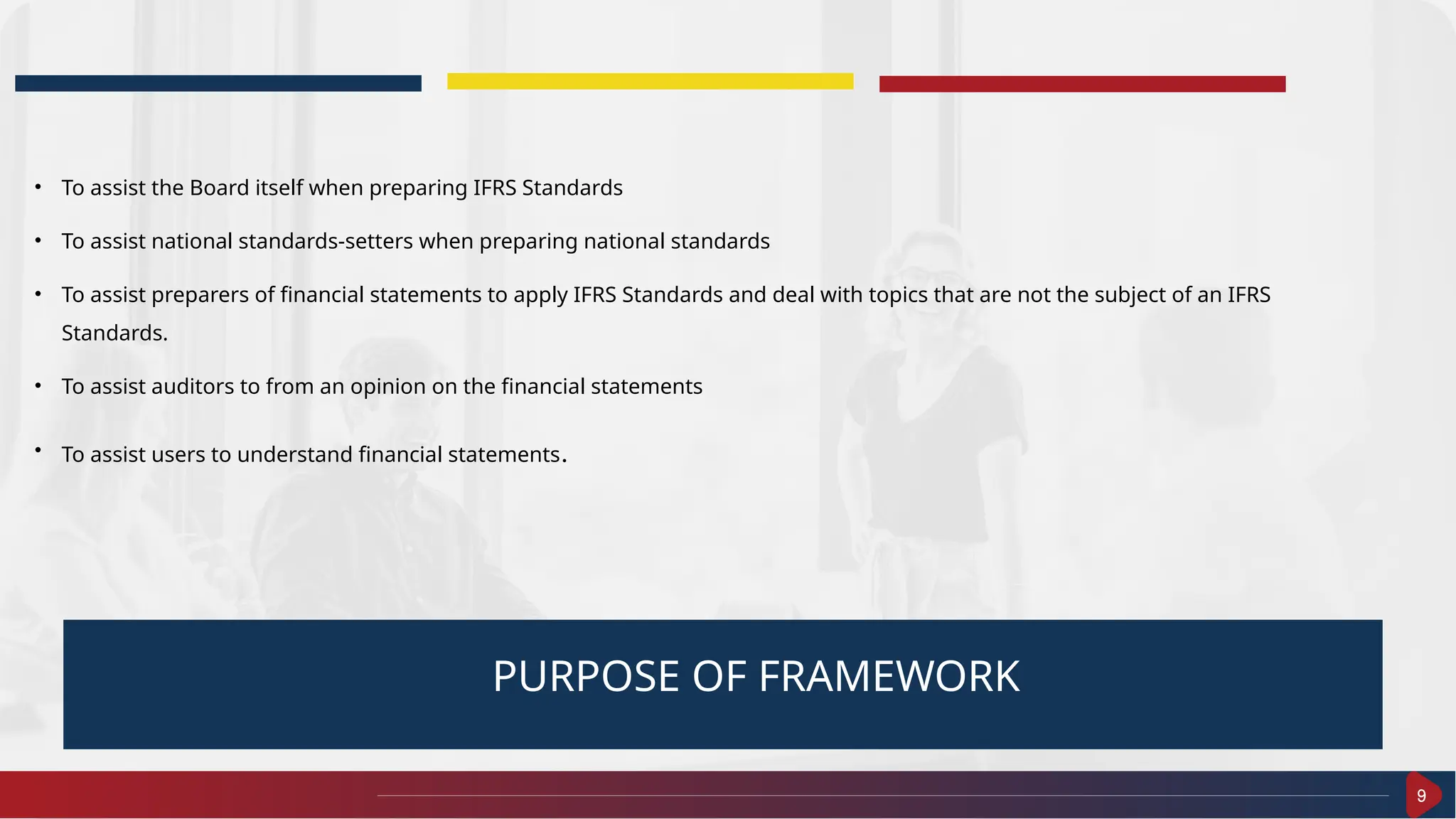

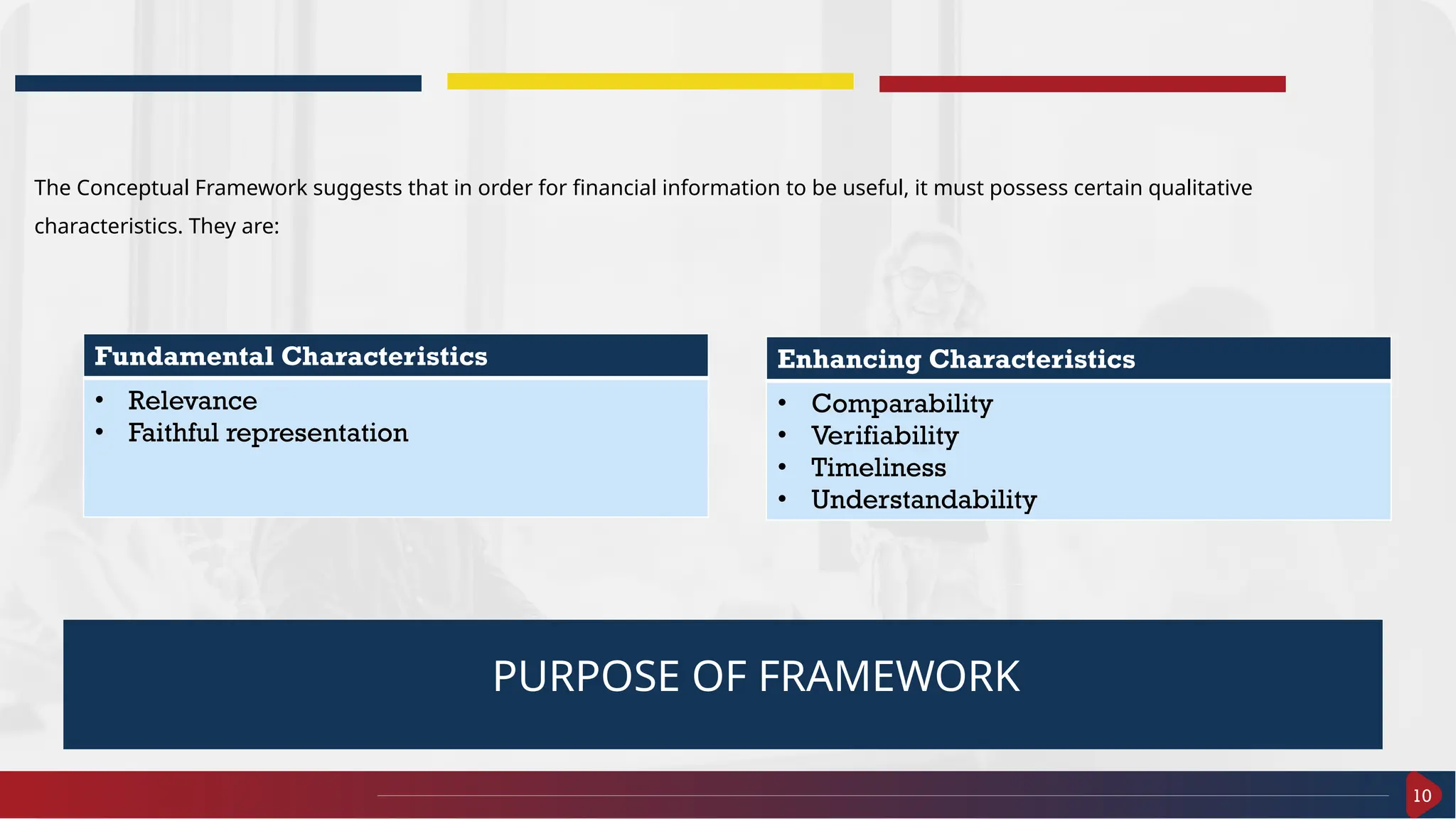

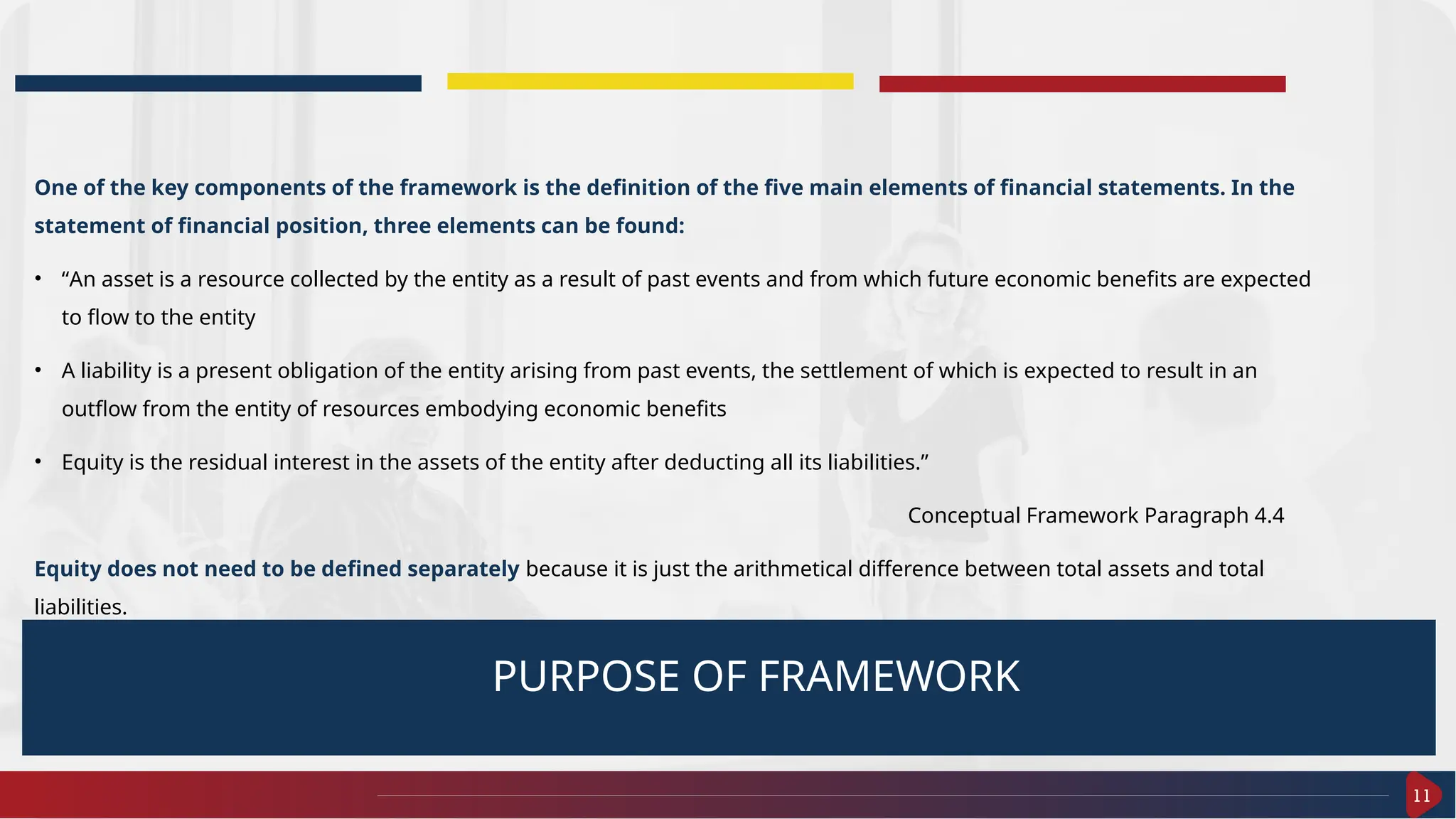

The document outlines a training session on International Financial Reporting Standards (IFRS) scheduled for November 8, 2024, detailing various topics such as the conceptual framework, key accounting standards, and qualitative characteristics of financial information. It includes energizing questions to engage participants and quizzes to test their understanding of IFRS principles regarding revenue recognition, materiality, and going concern assumptions. The document emphasizes the importance of accurate financial reporting that aids decision-making for users like investors and creditors.