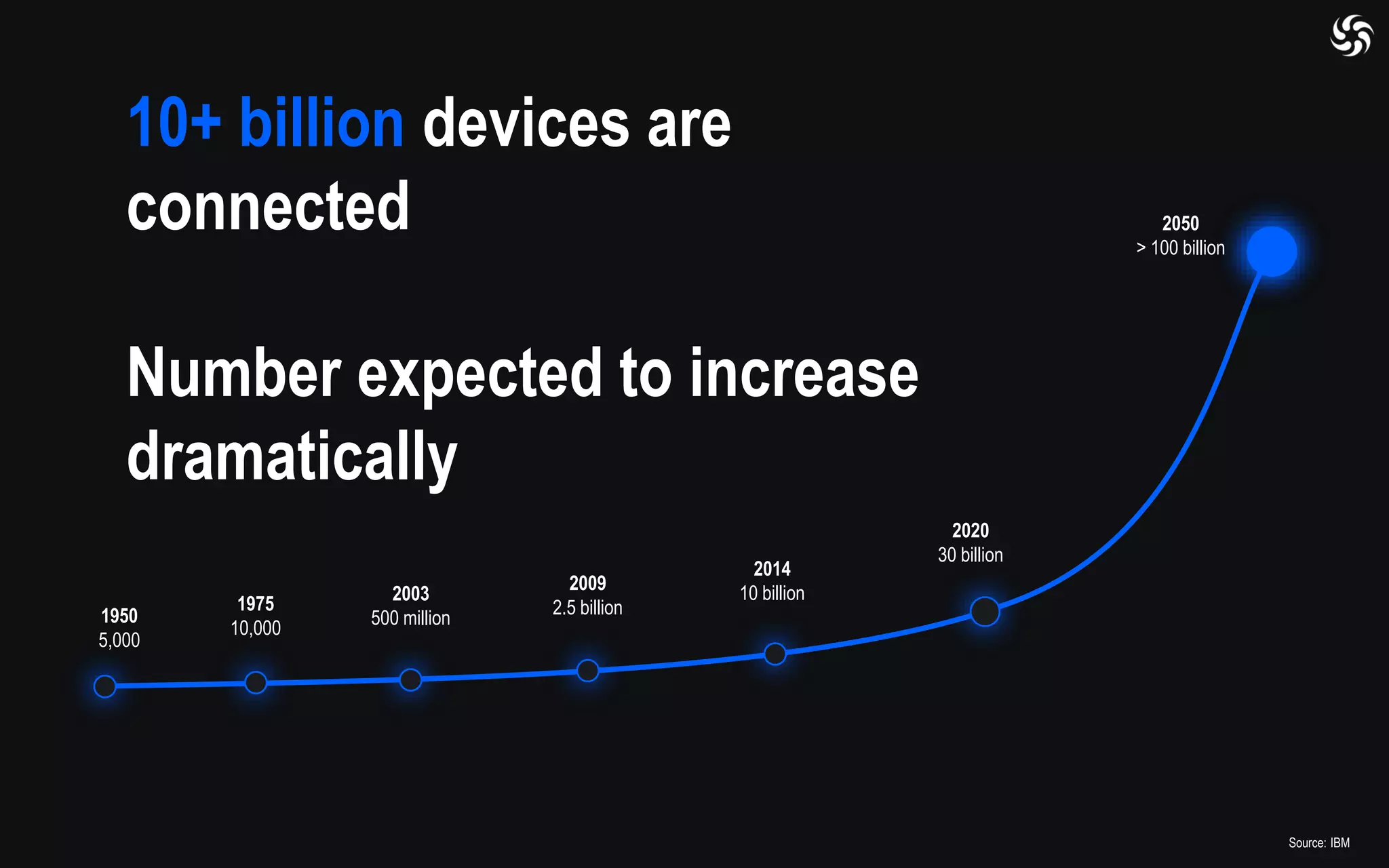

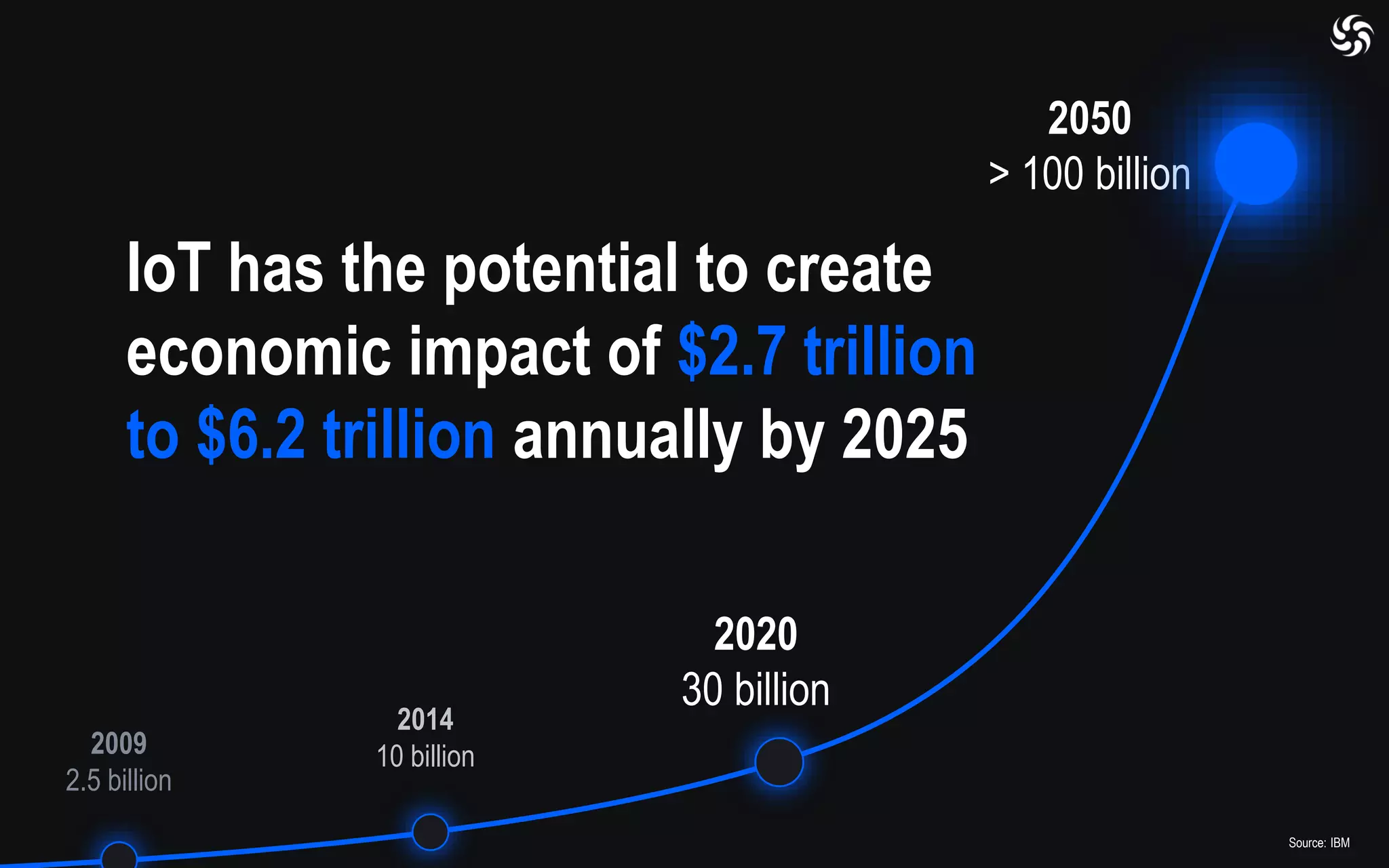

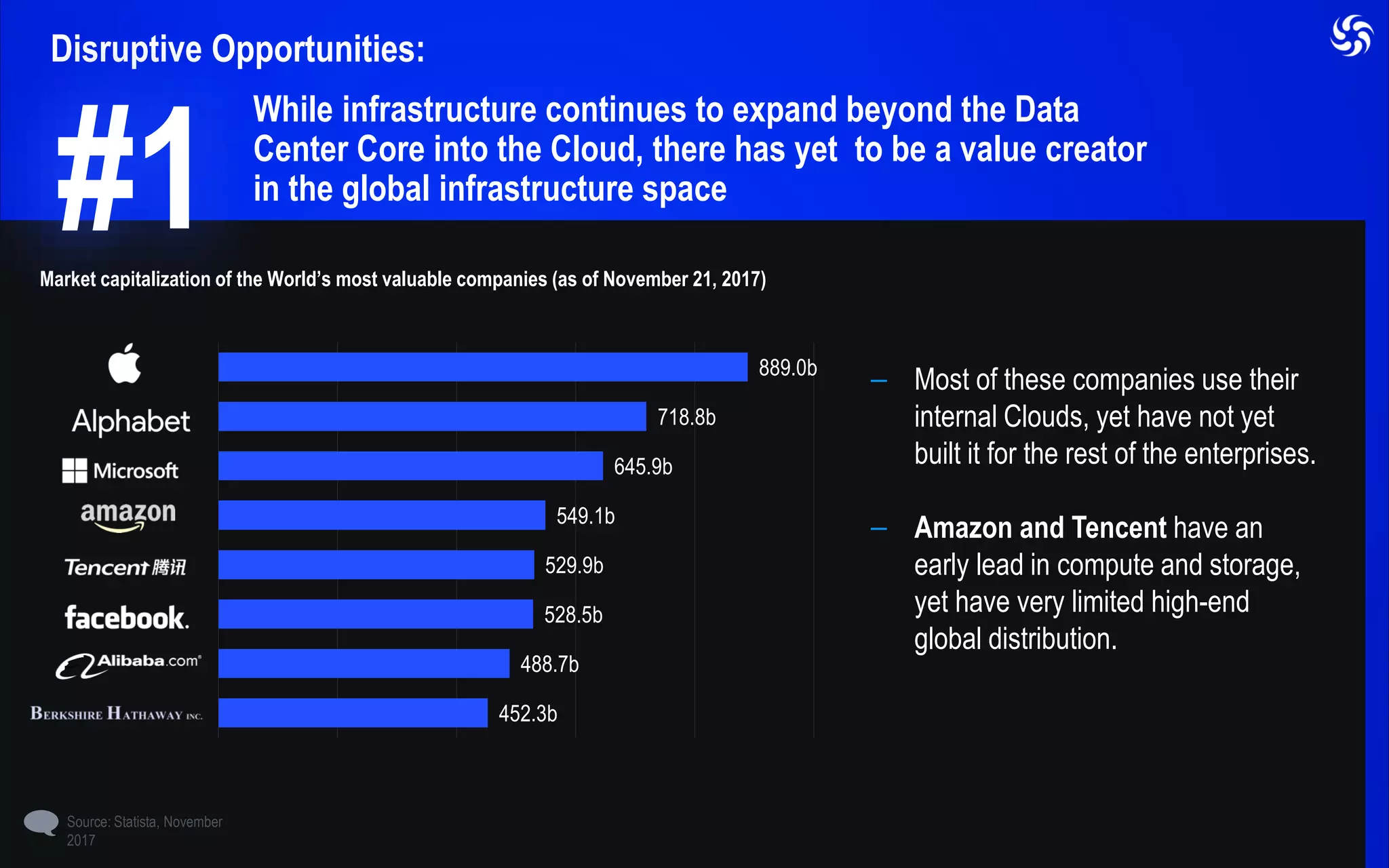

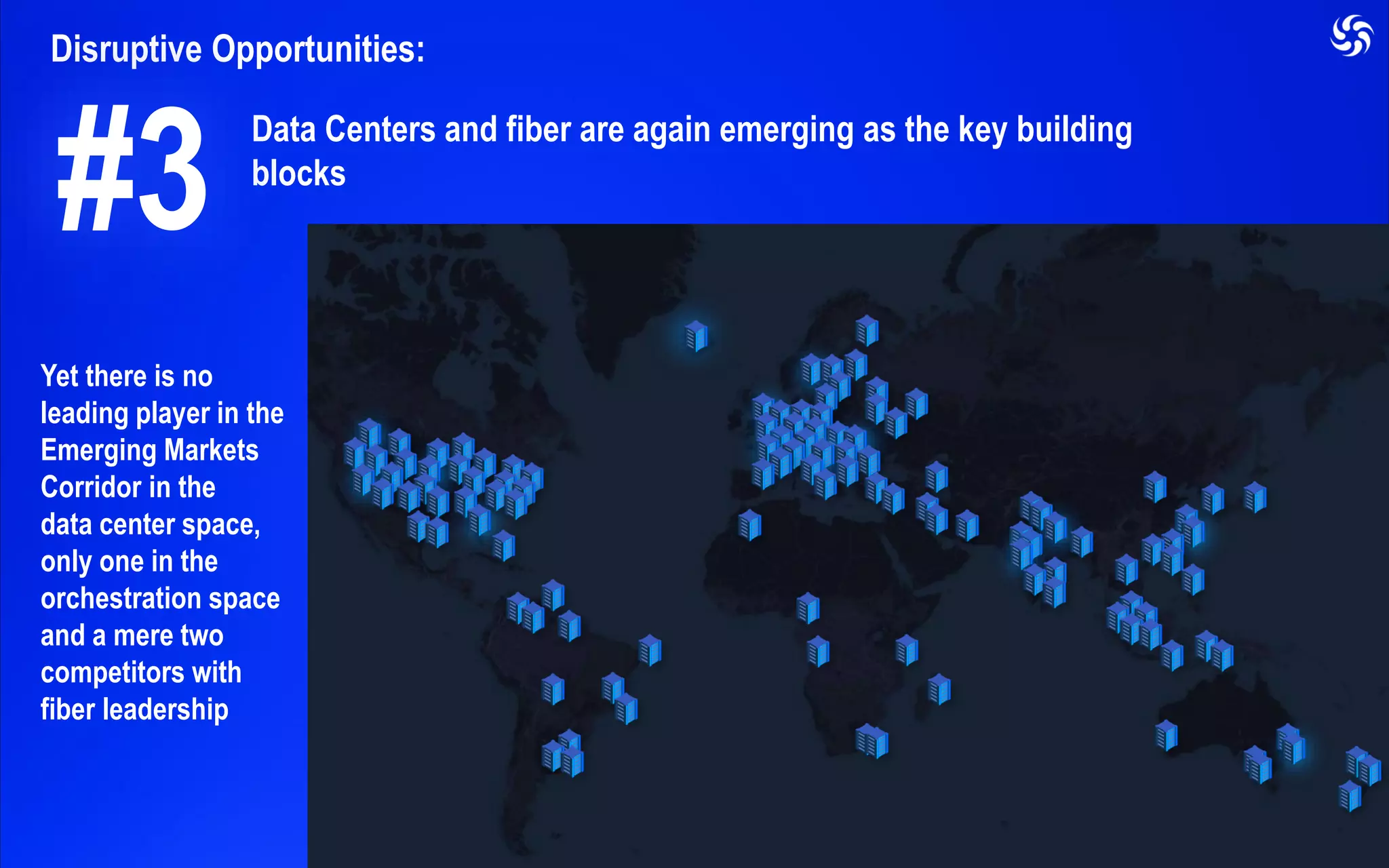

Bill Barney, CEO of Reliance Communications, discusses the future of technology infrastructure at Datacloud Asia in 2018, emphasizing the importance of digital transformation and the rapid growth of connected devices. He highlights disruptive opportunities in emerging markets and the challenges faced by CIOs in managing complex enterprise networks. The document concludes that success will hinge on mastering cloud orchestration, fiber connectivity, and accessible computing resources.