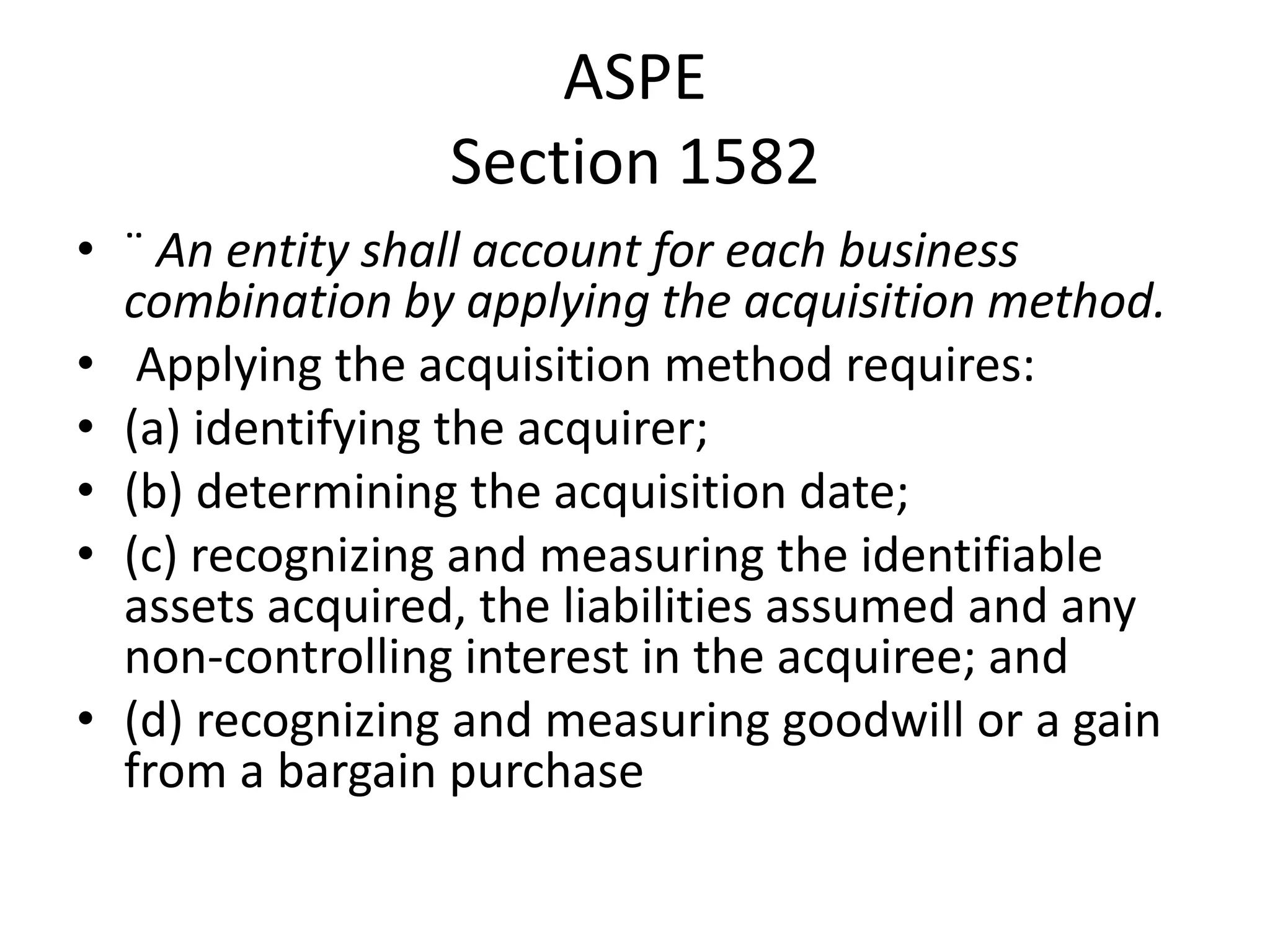

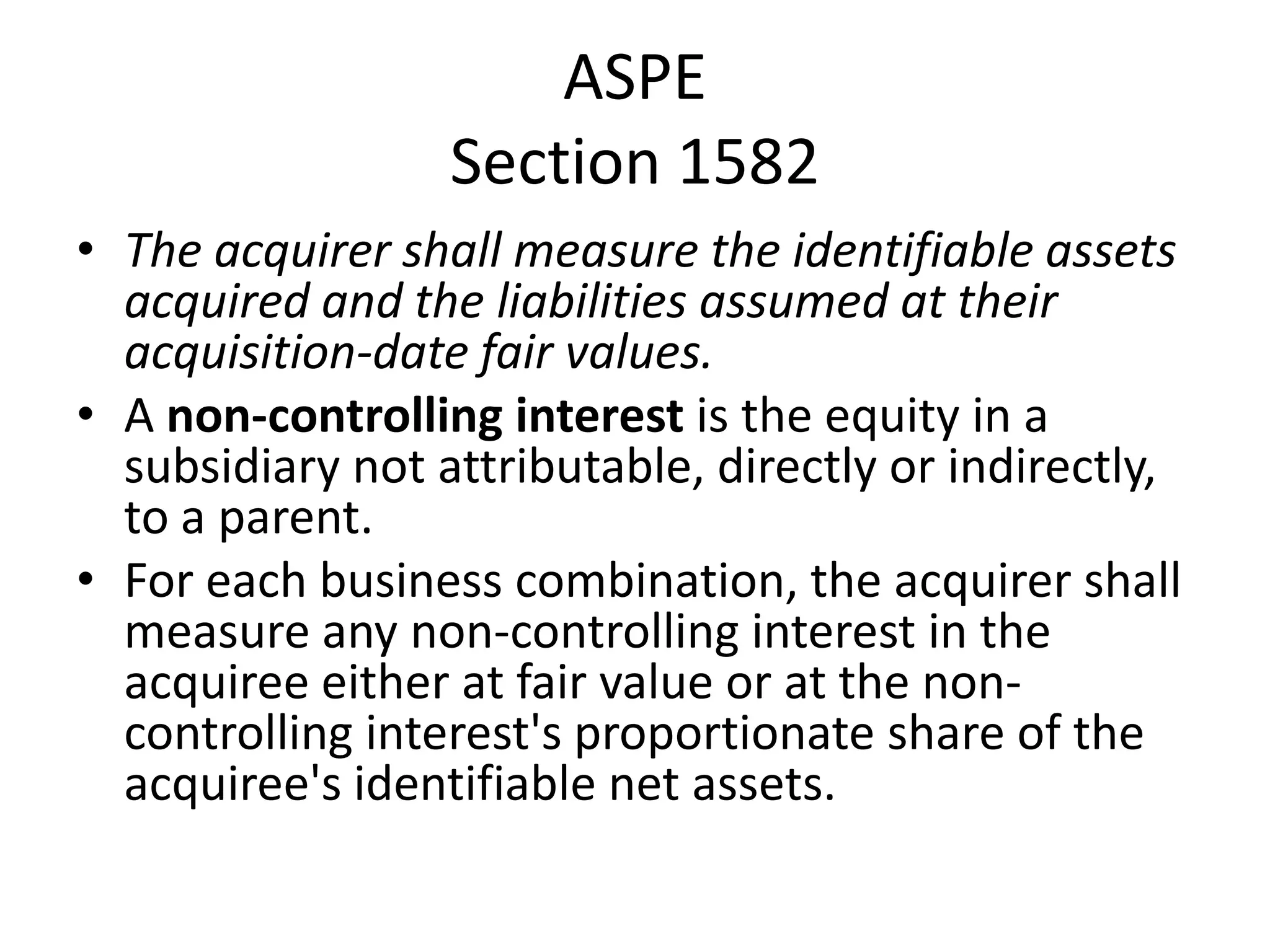

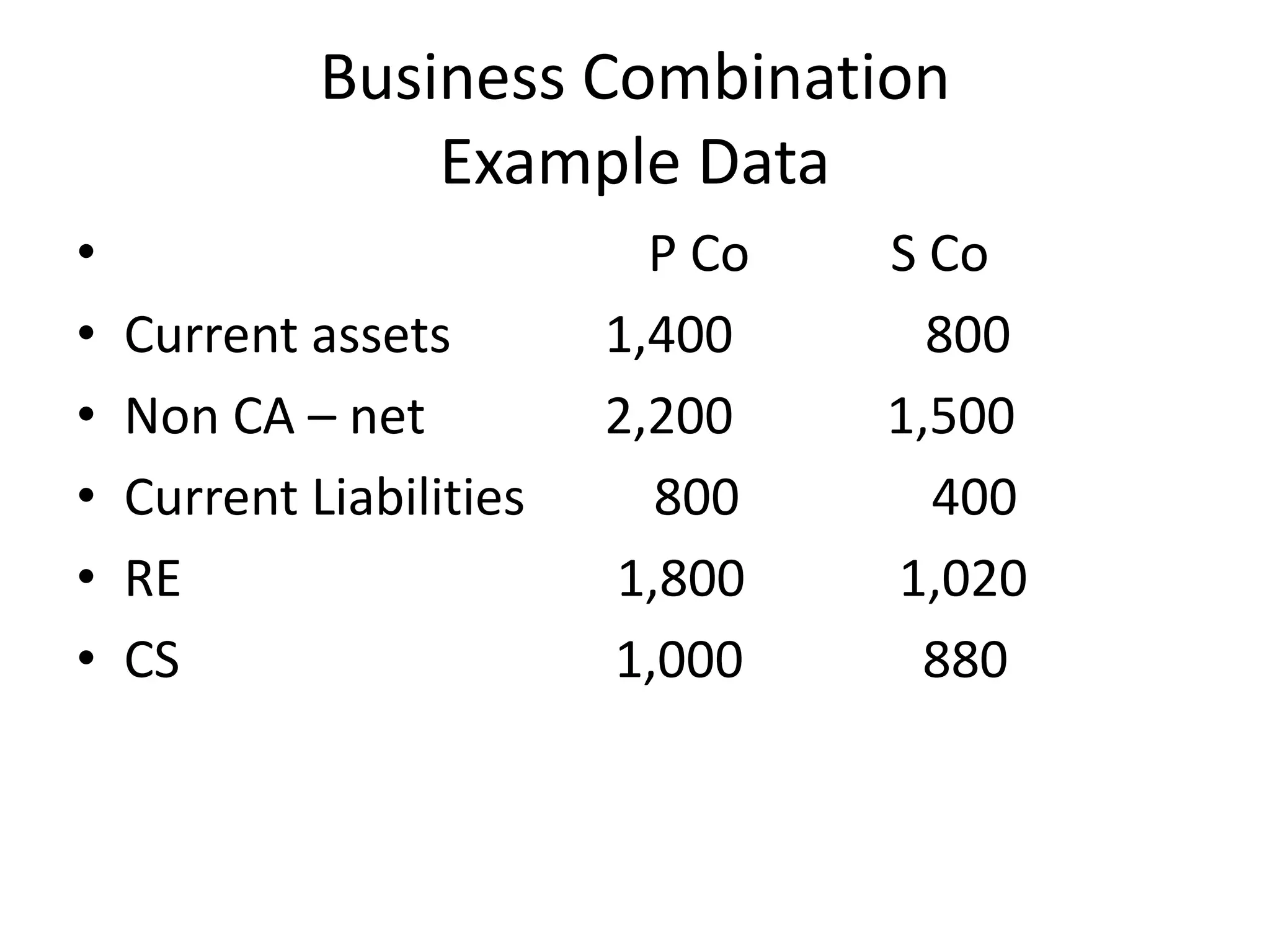

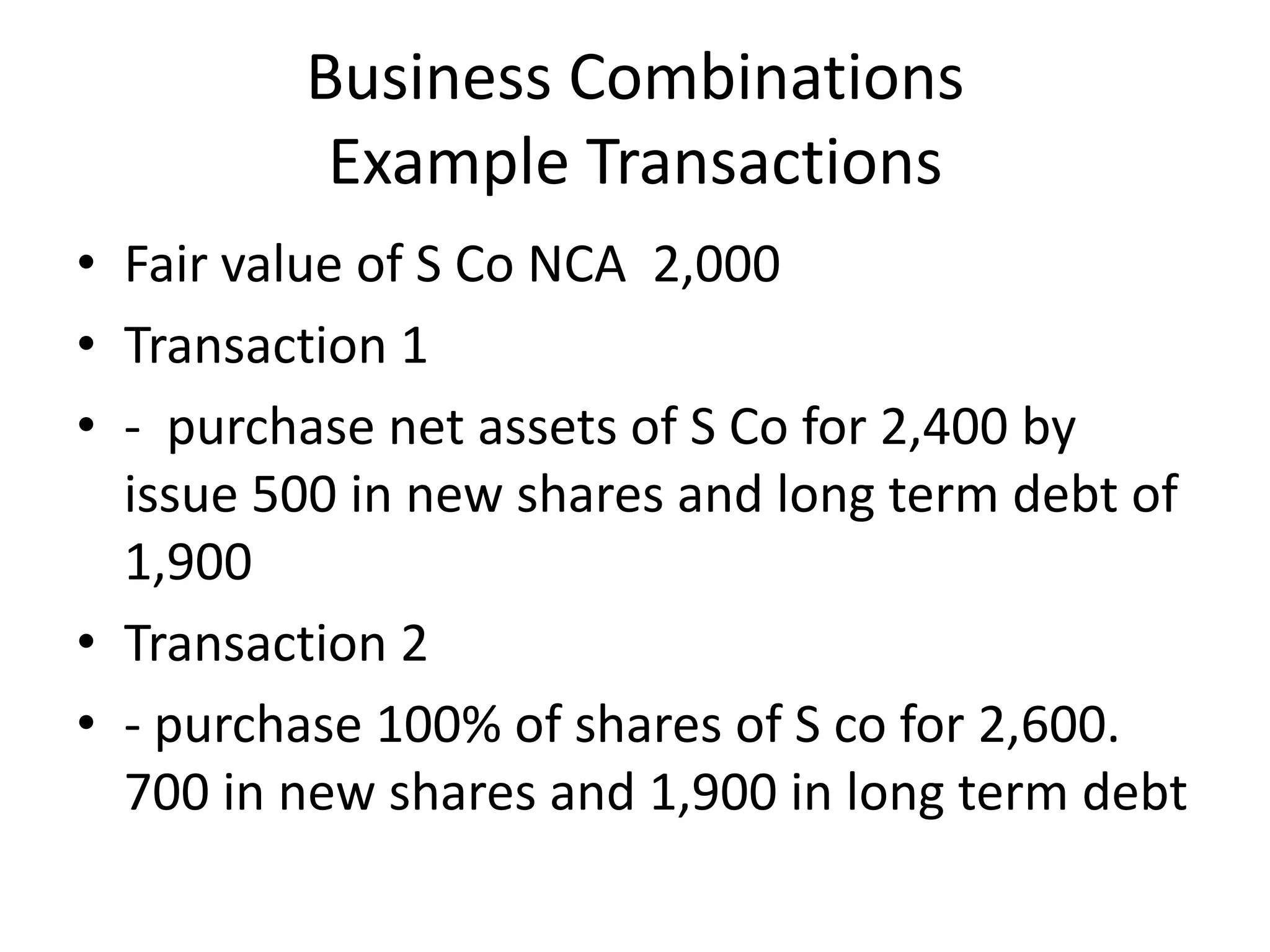

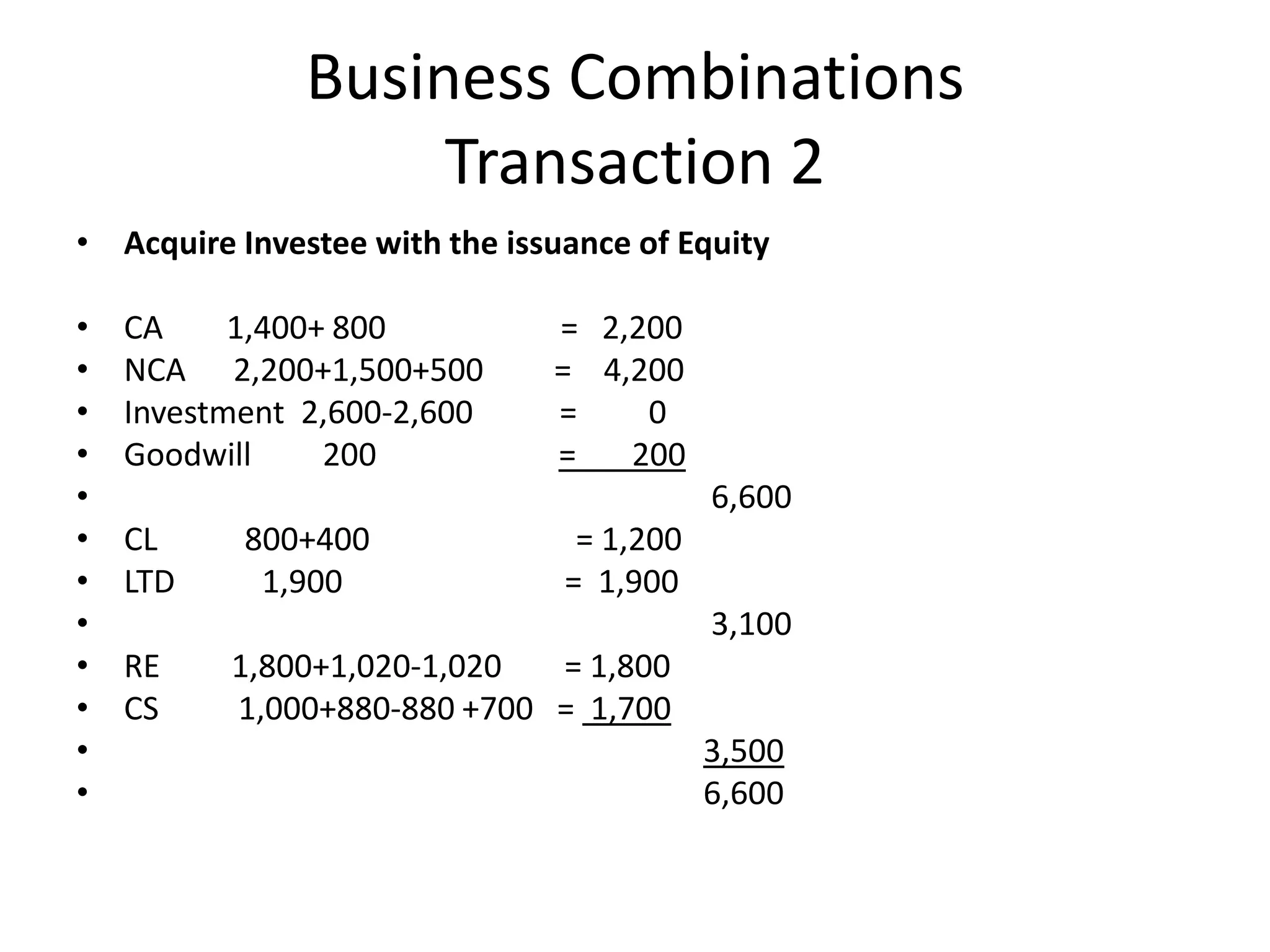

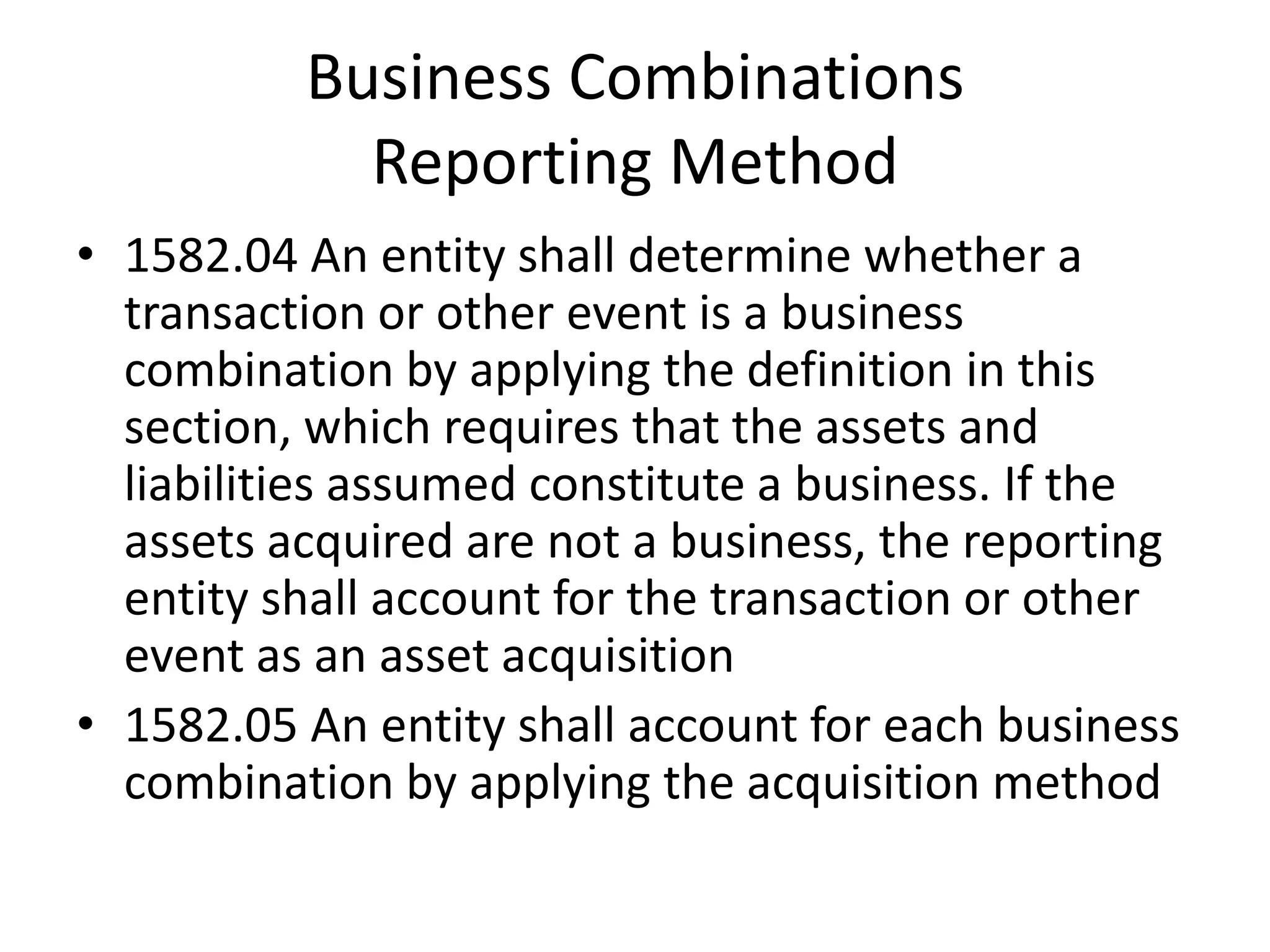

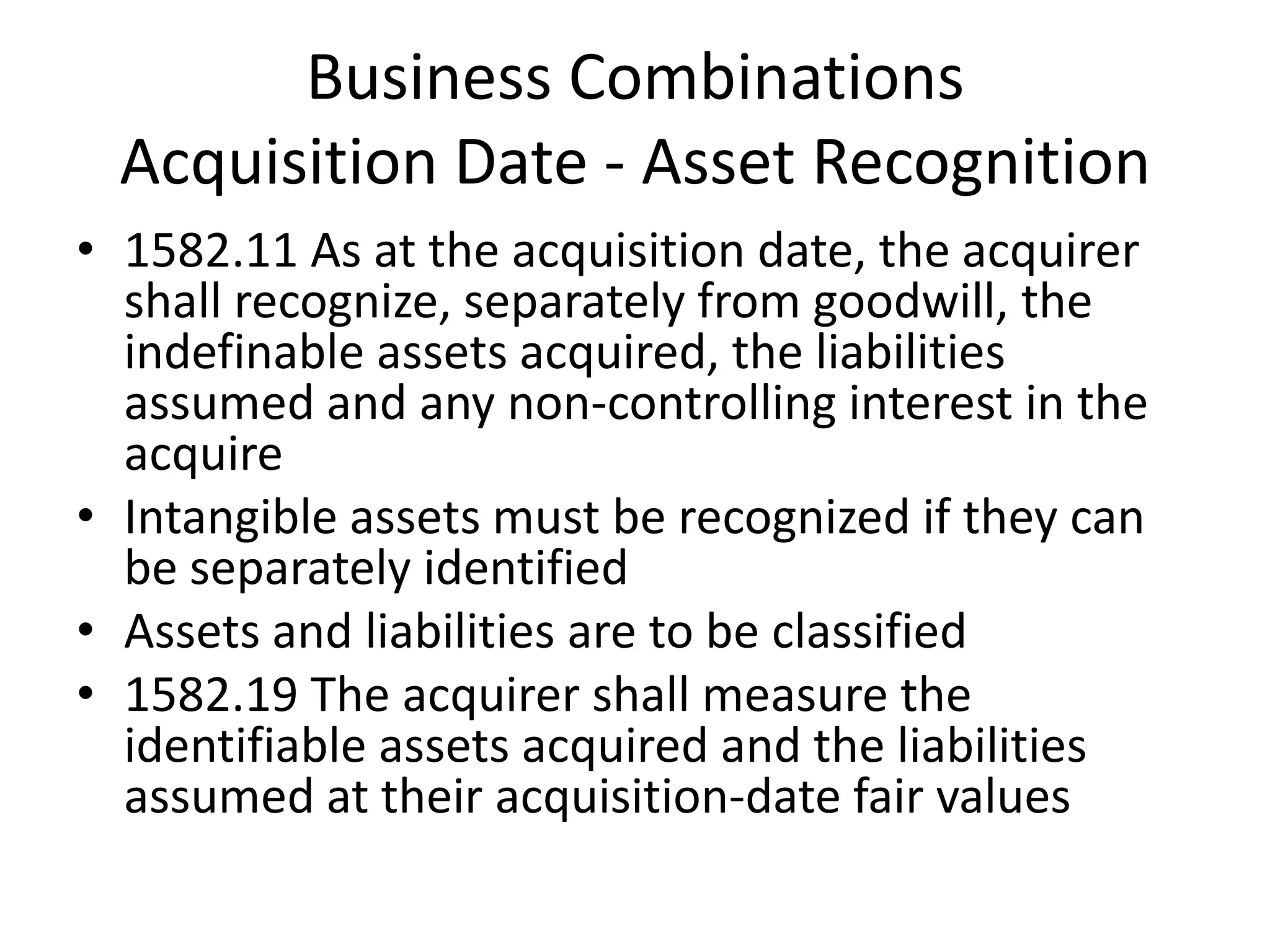

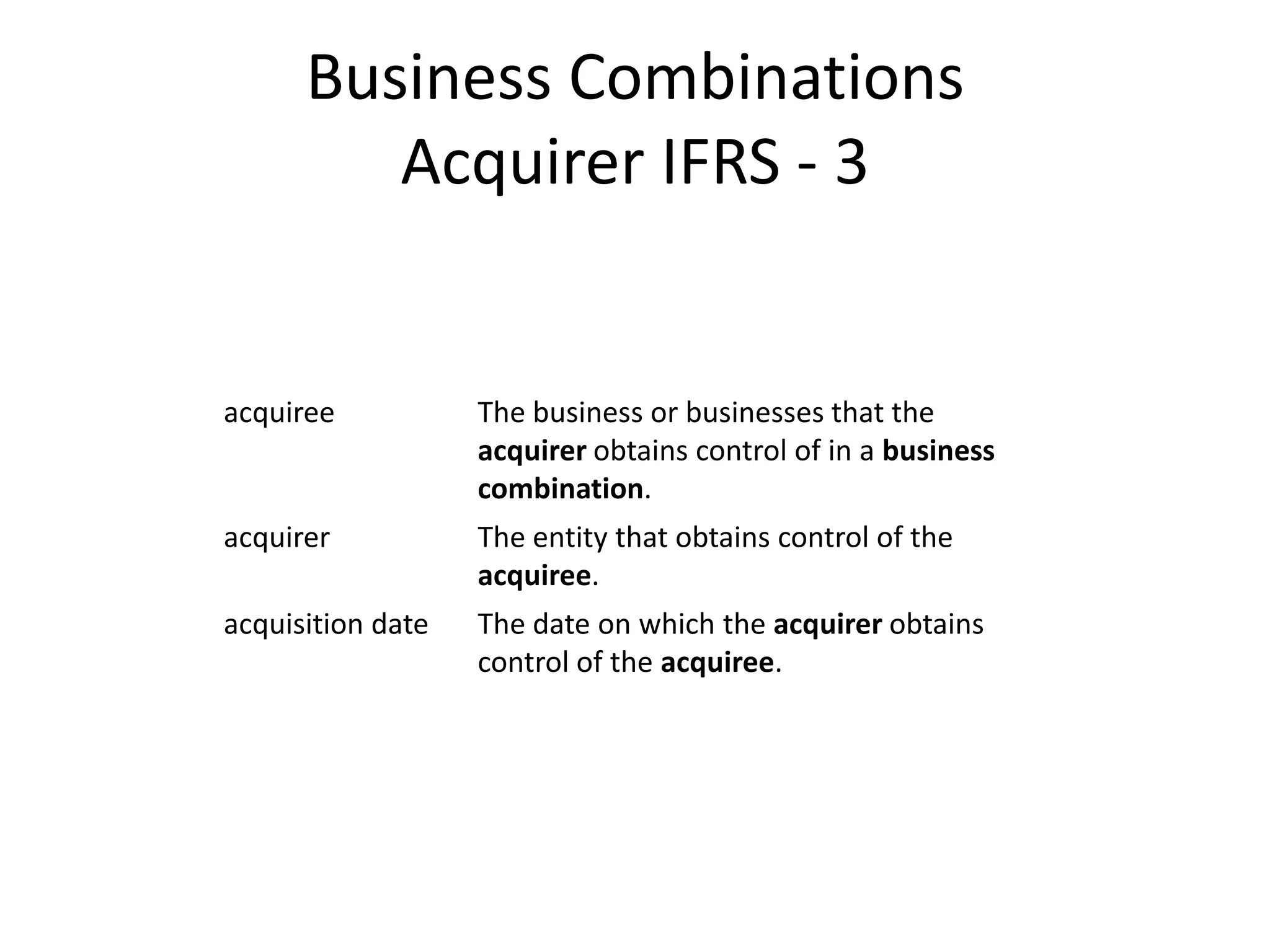

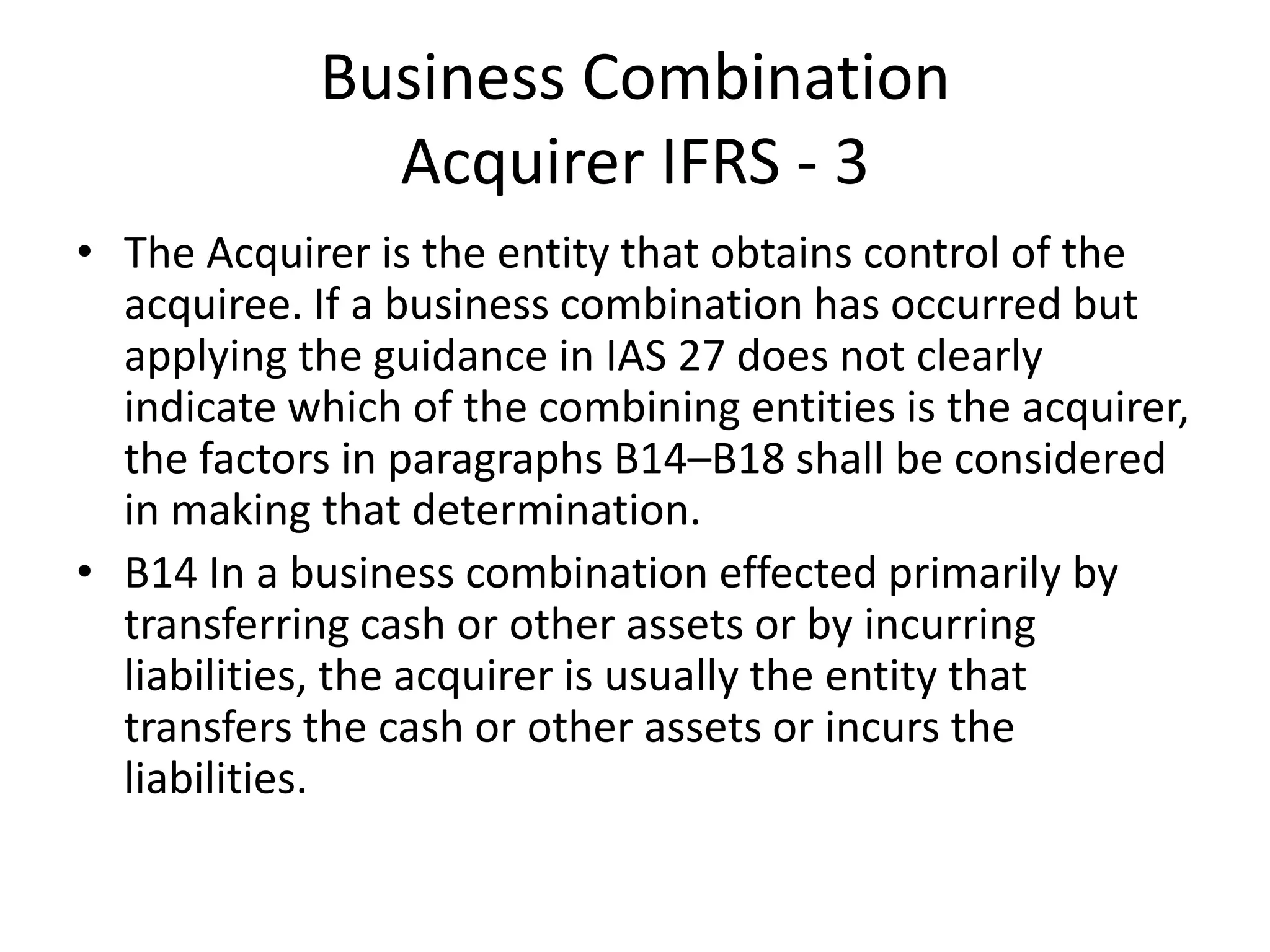

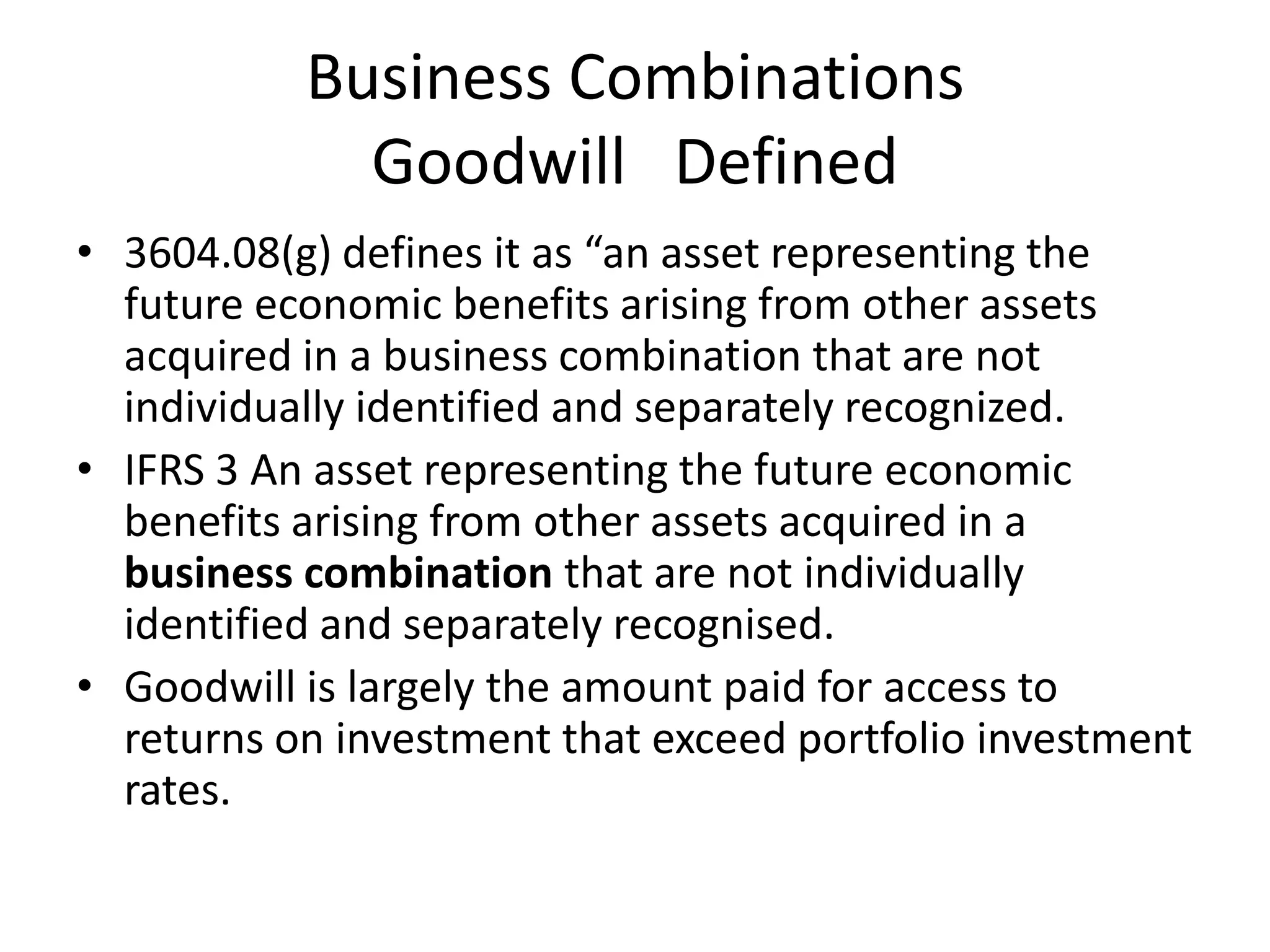

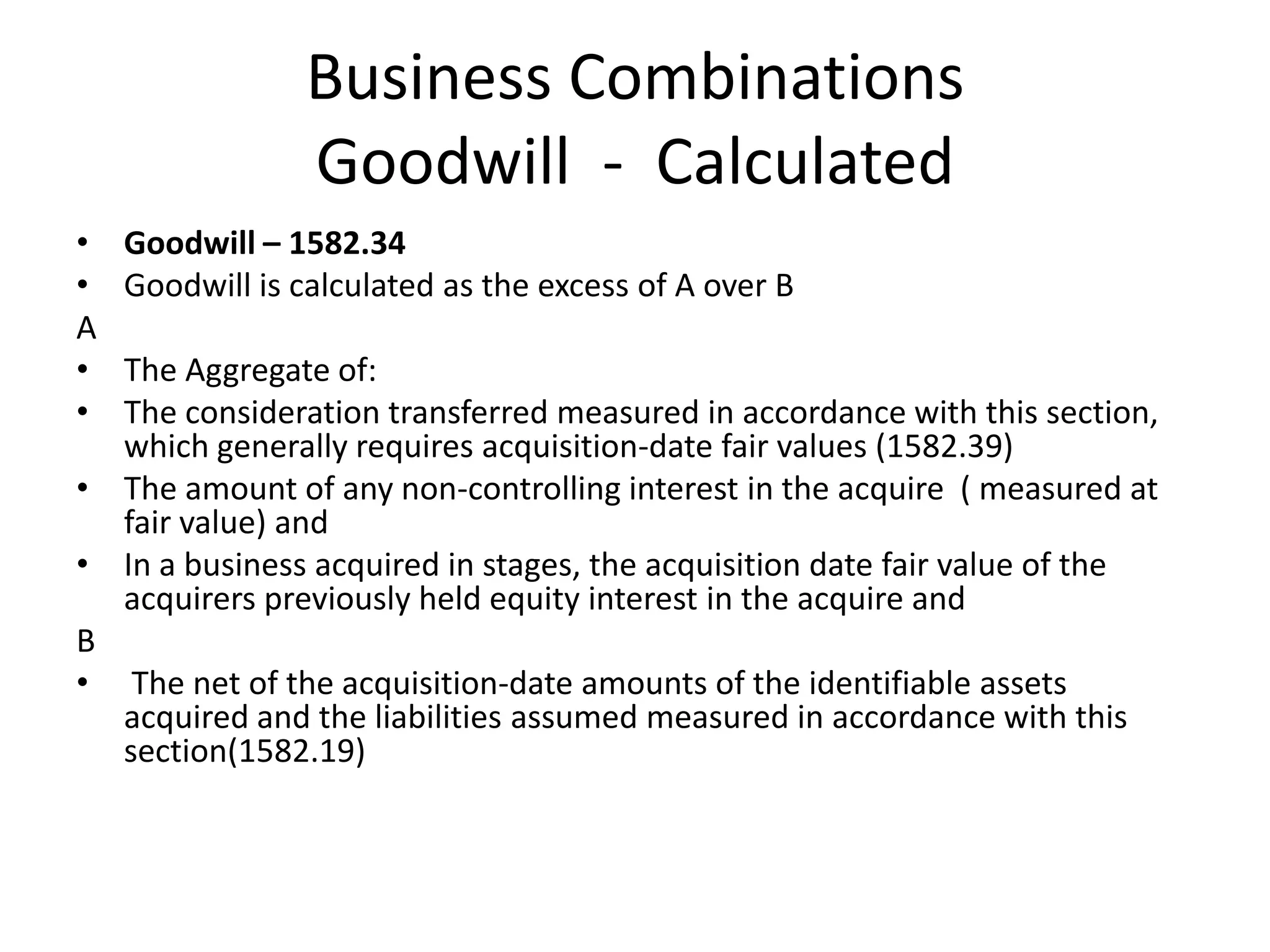

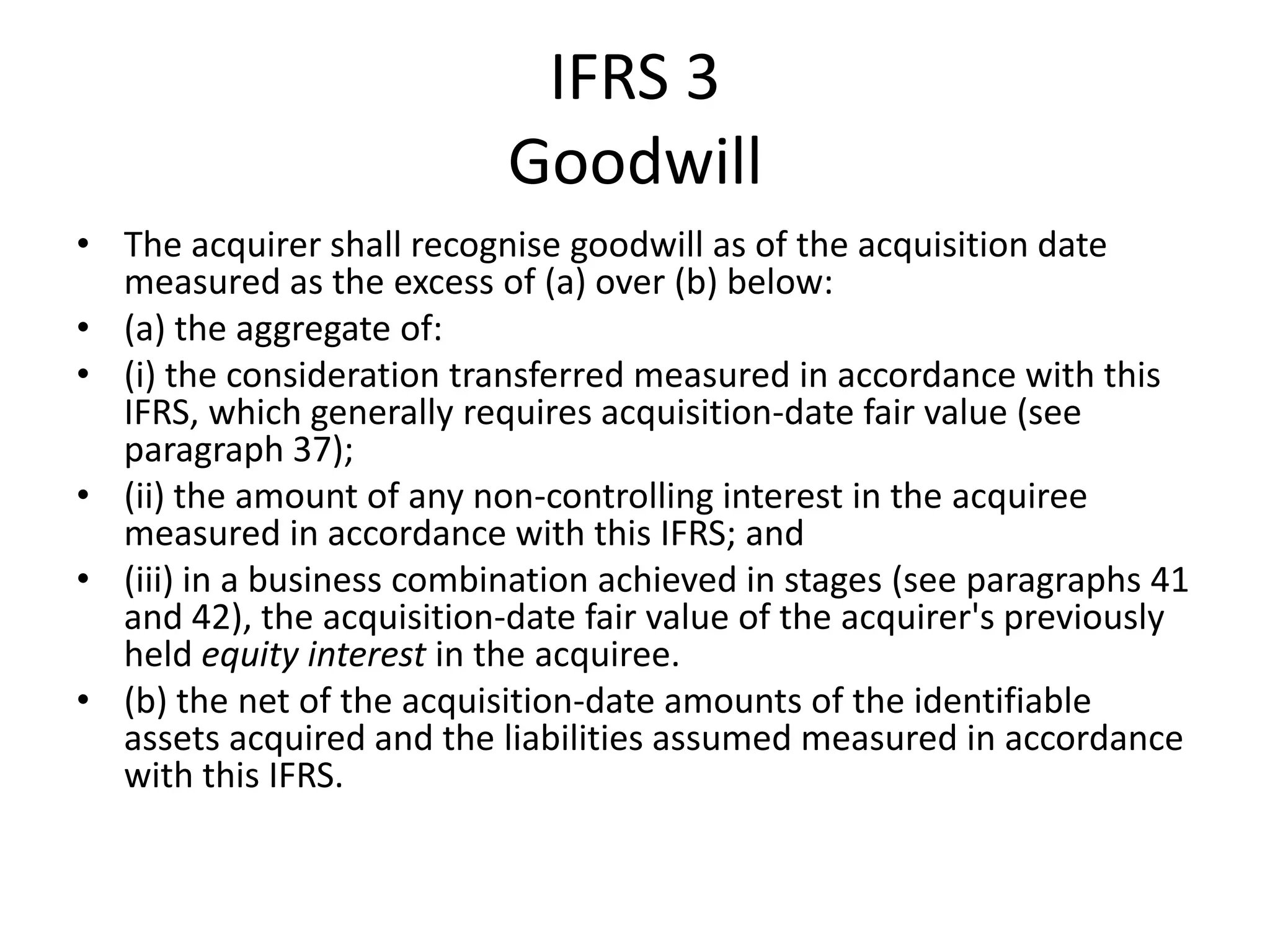

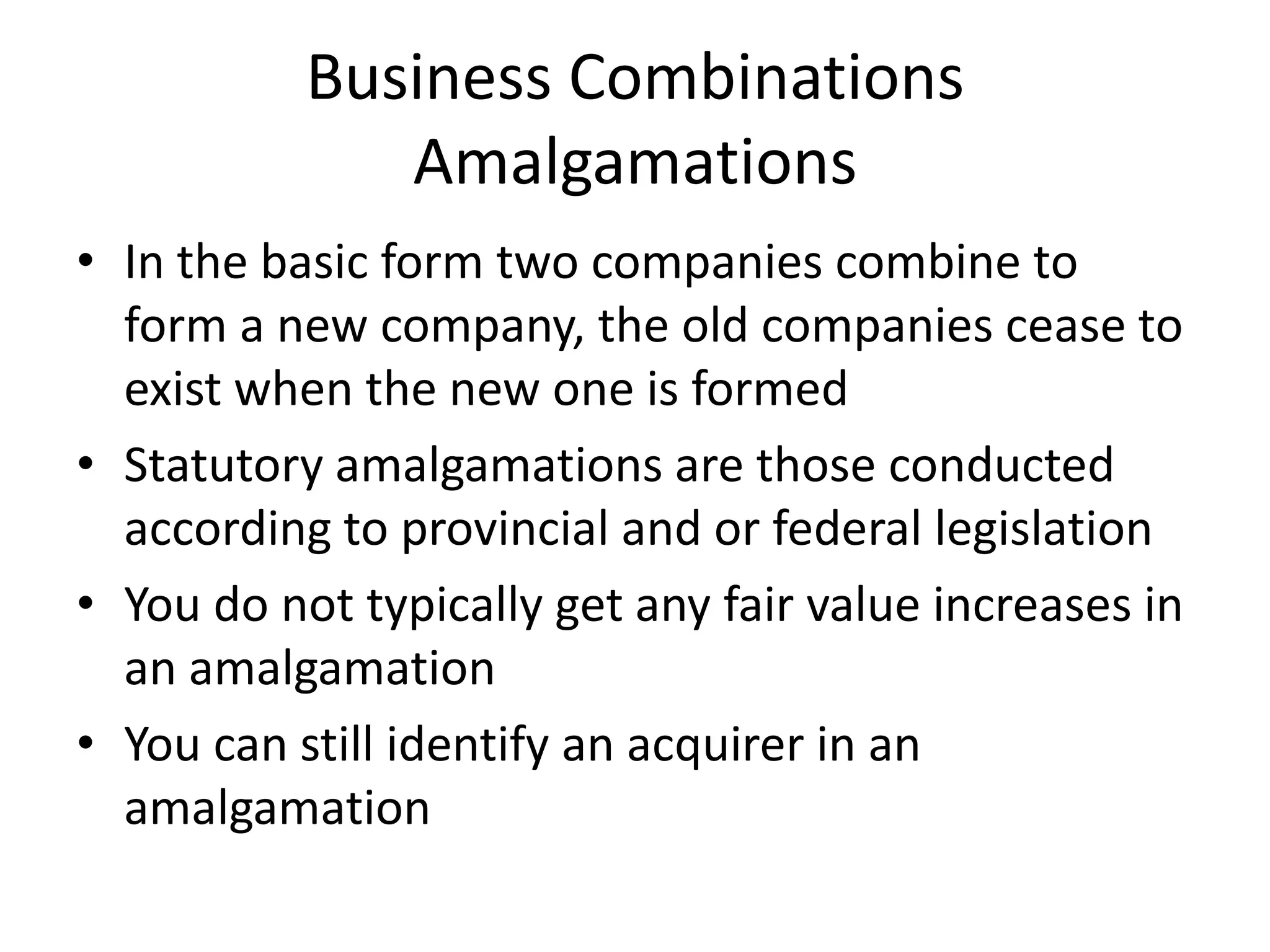

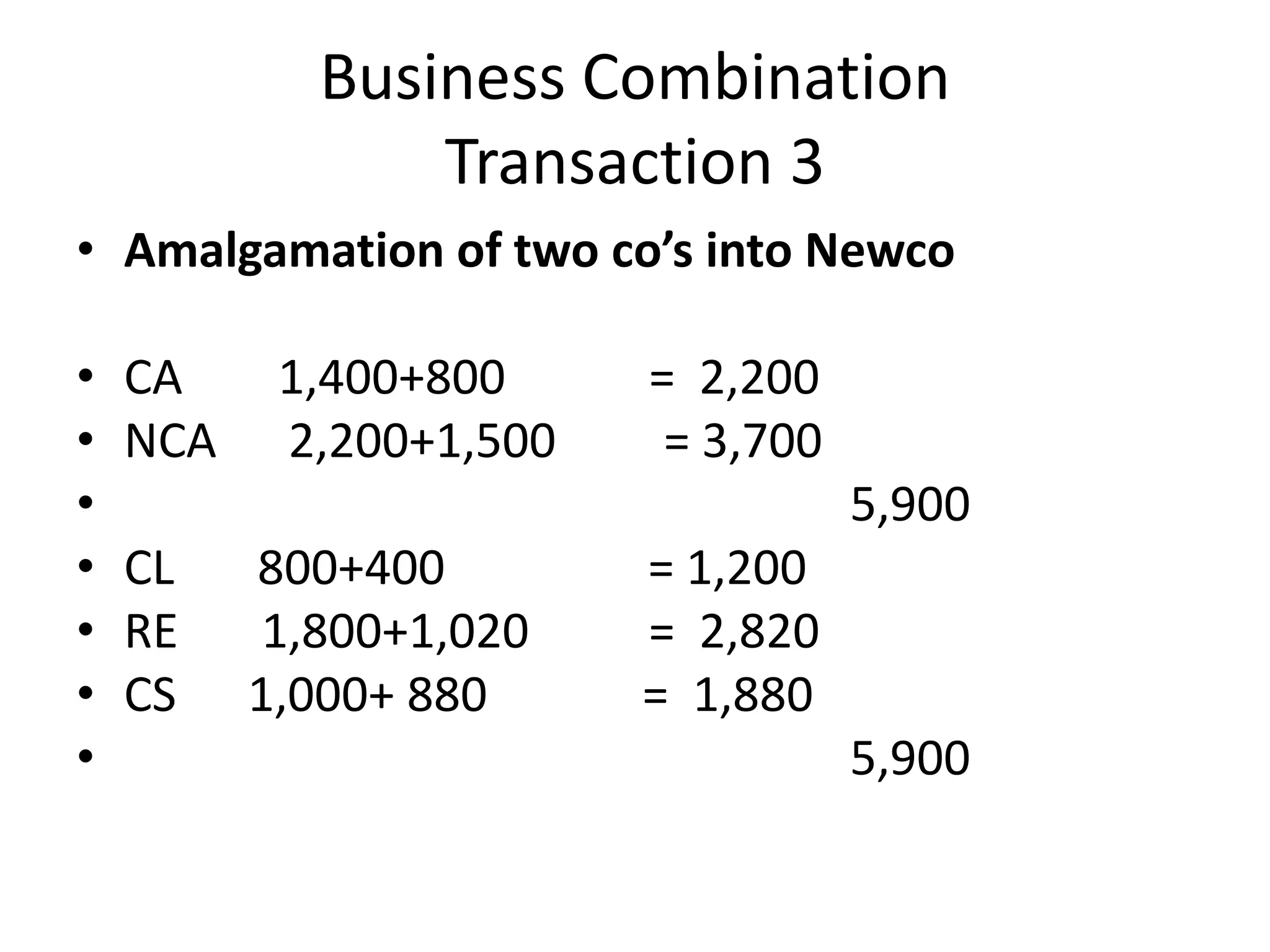

This document discusses key concepts related to business combinations, including defining a business combination, applying the acquisition method, determining goodwill, assessing goodwill impairment, and identifying the acquirer. It provides learning objectives and definitions from IFRS 3 and ASPE related to business combinations. Examples are provided to illustrate accounting for asset acquisitions, share acquisitions, and amalgamations. The calculation and subsequent accounting for goodwill and non-controlling interests are also summarized.