Downloaded 39 times

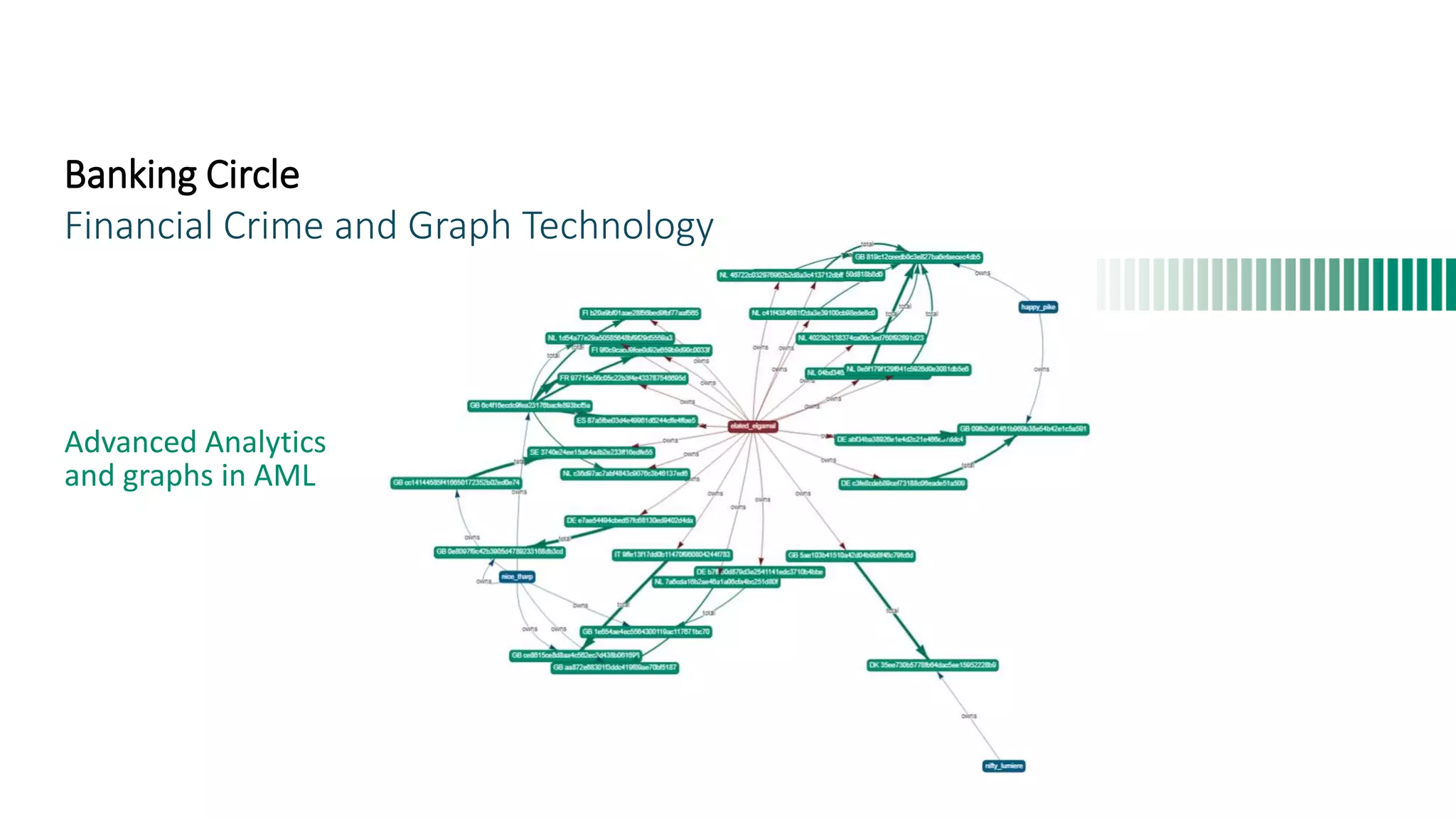

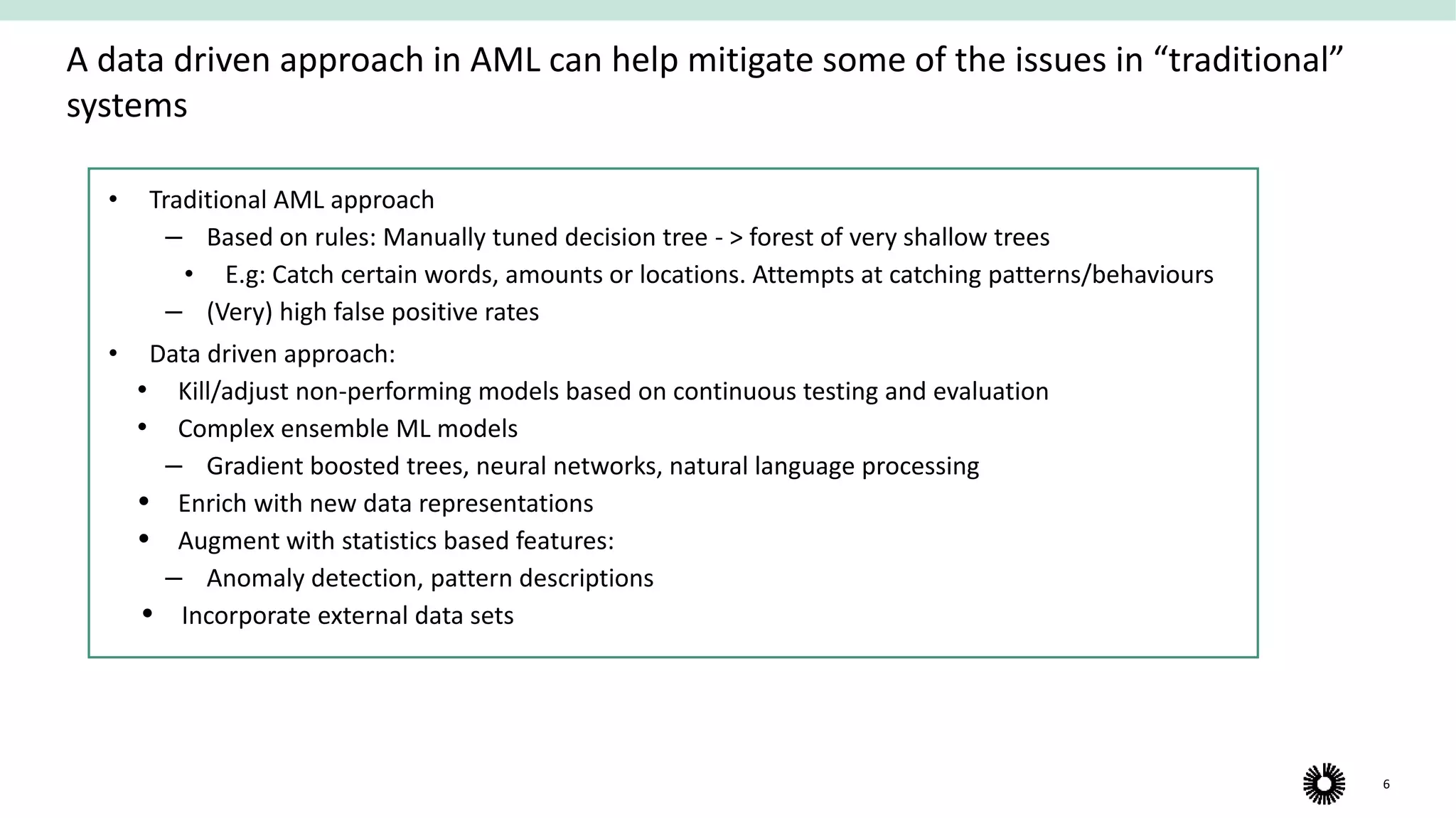

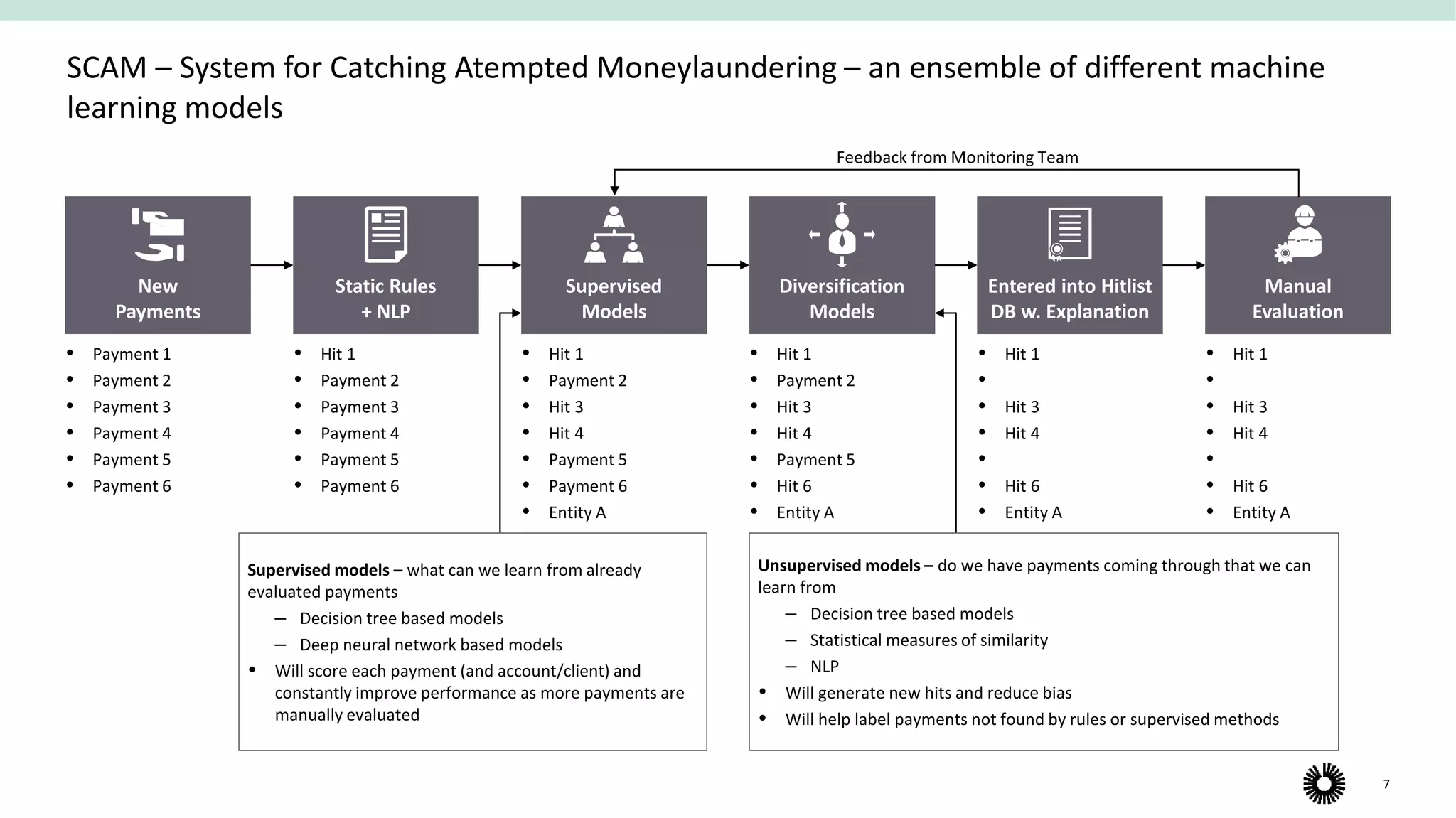

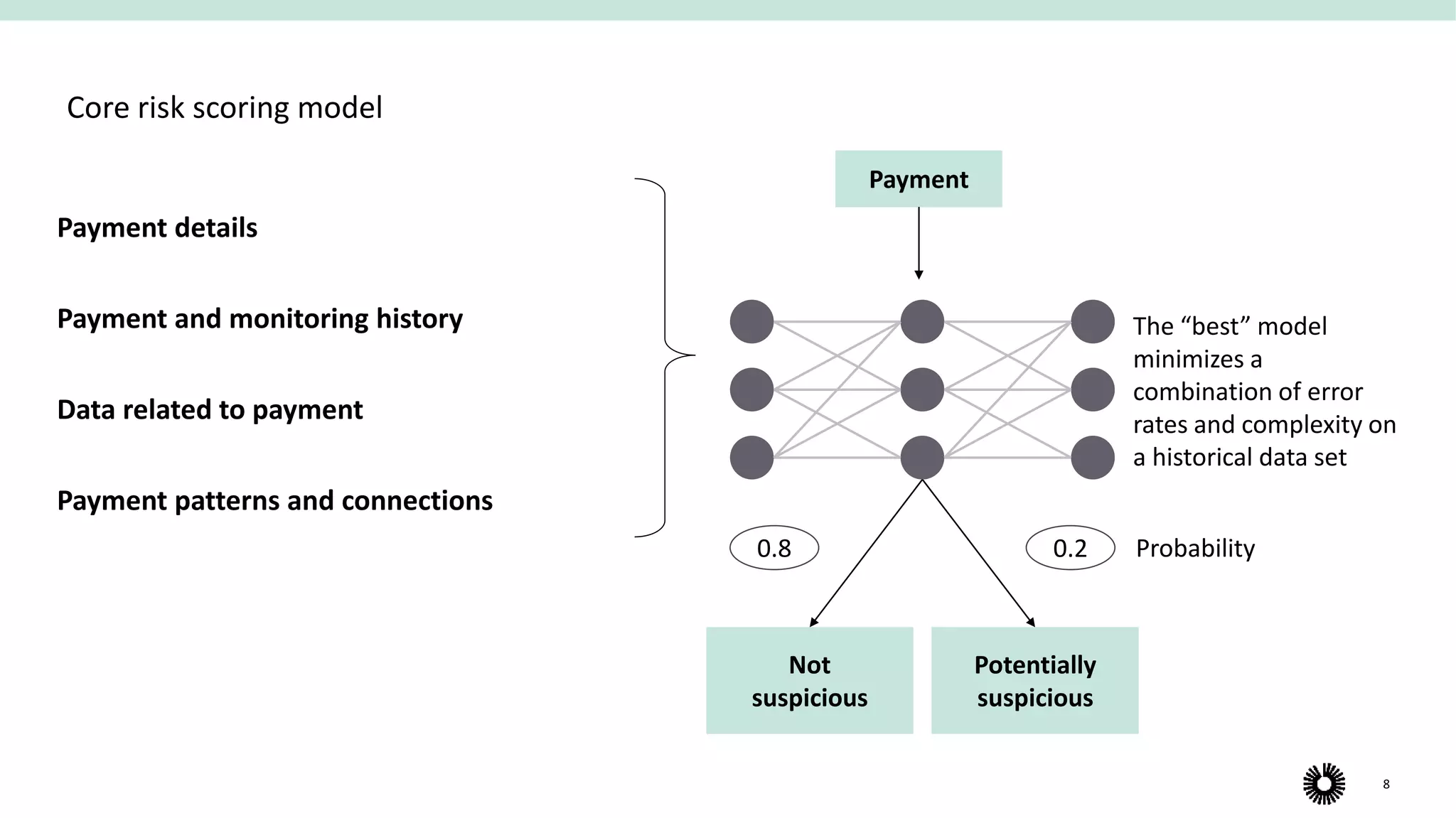

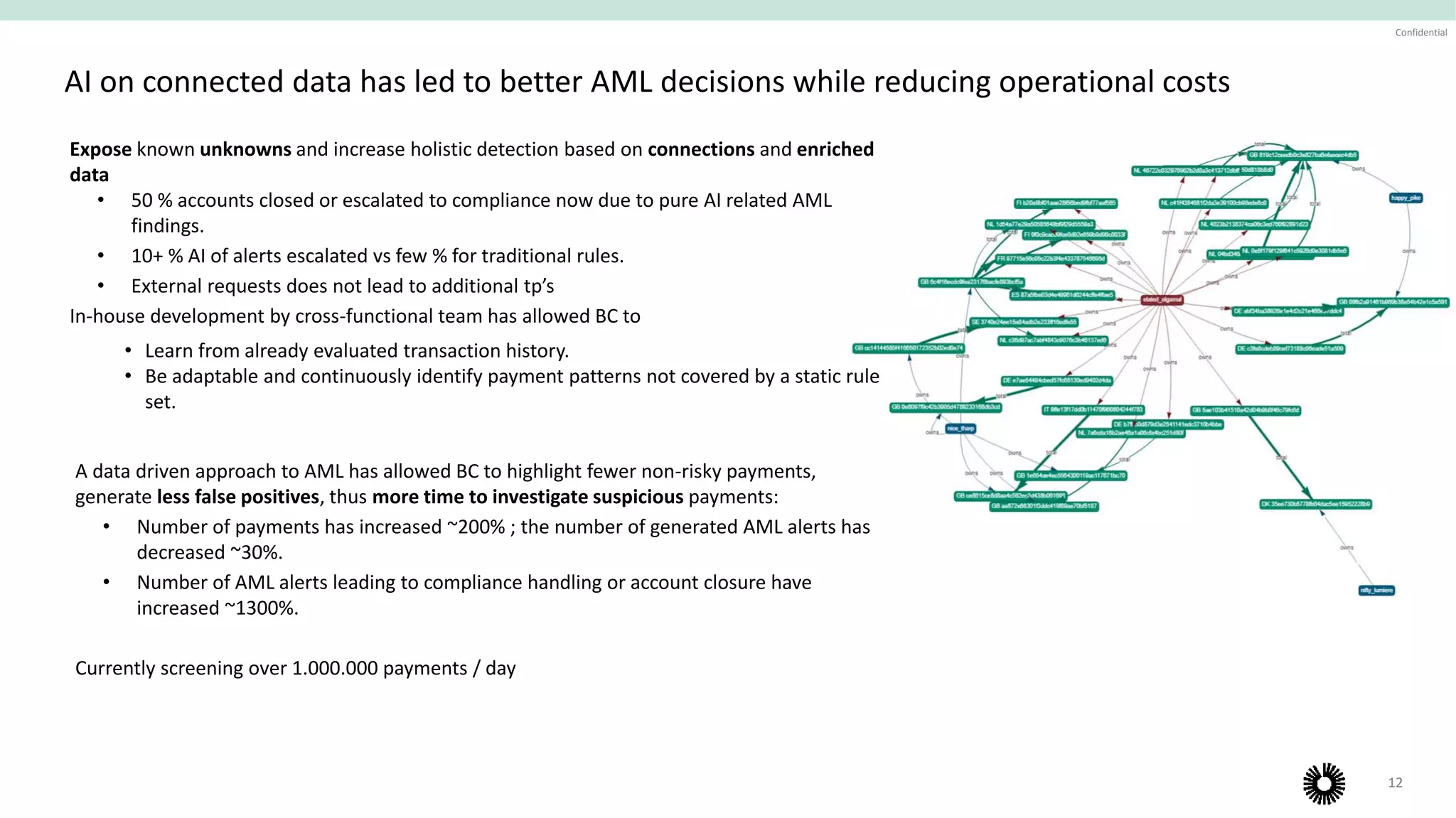

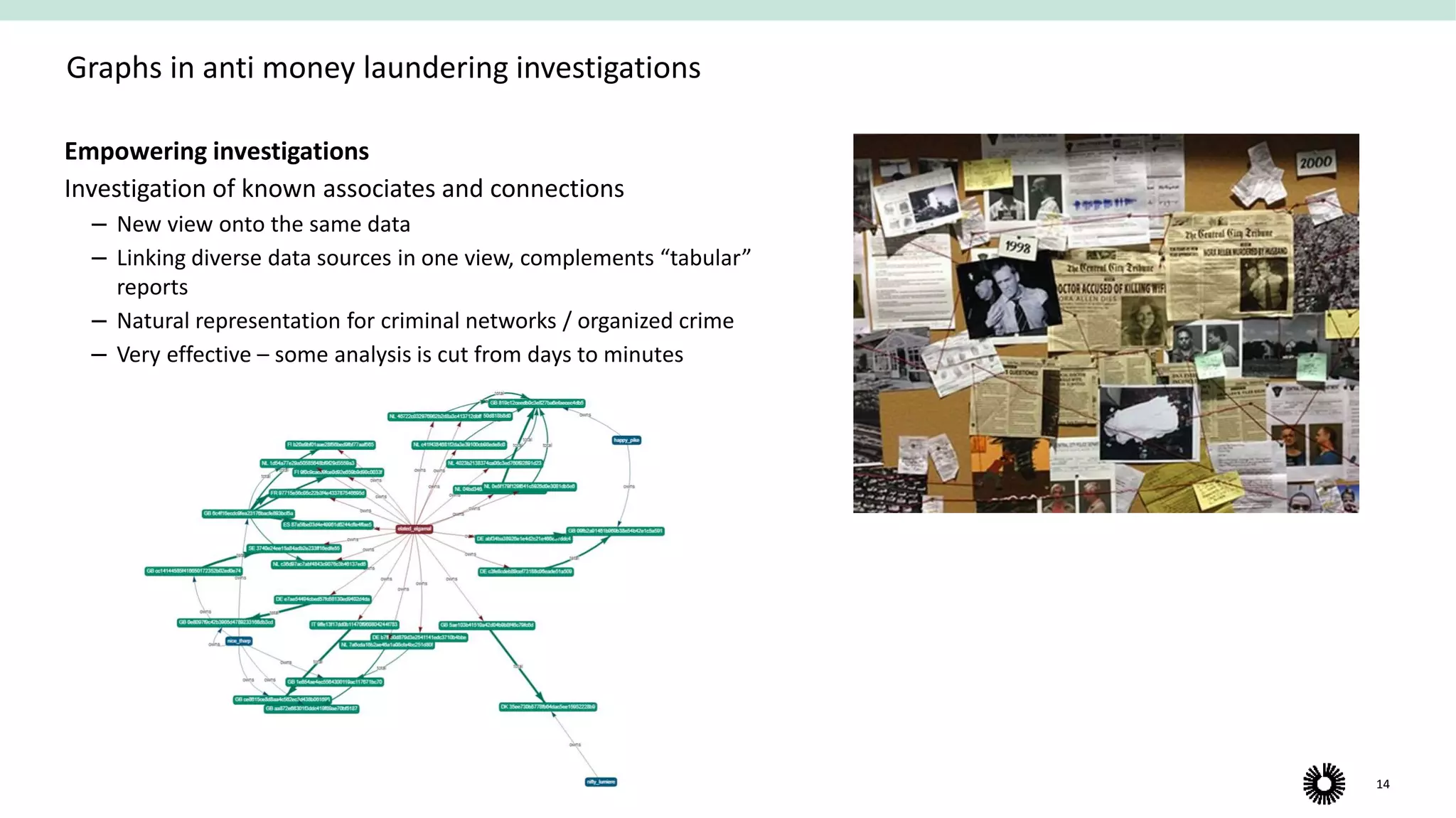

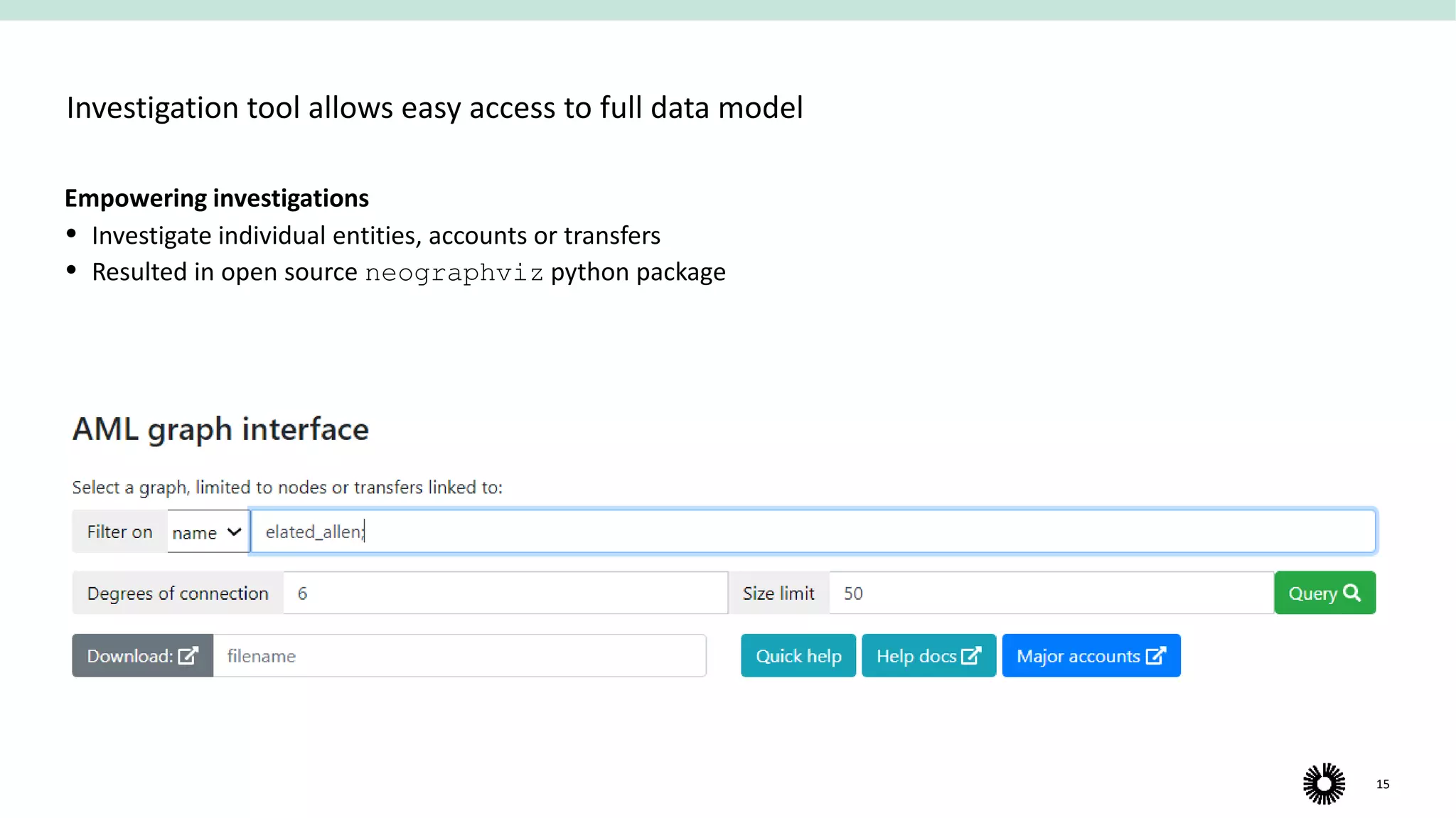

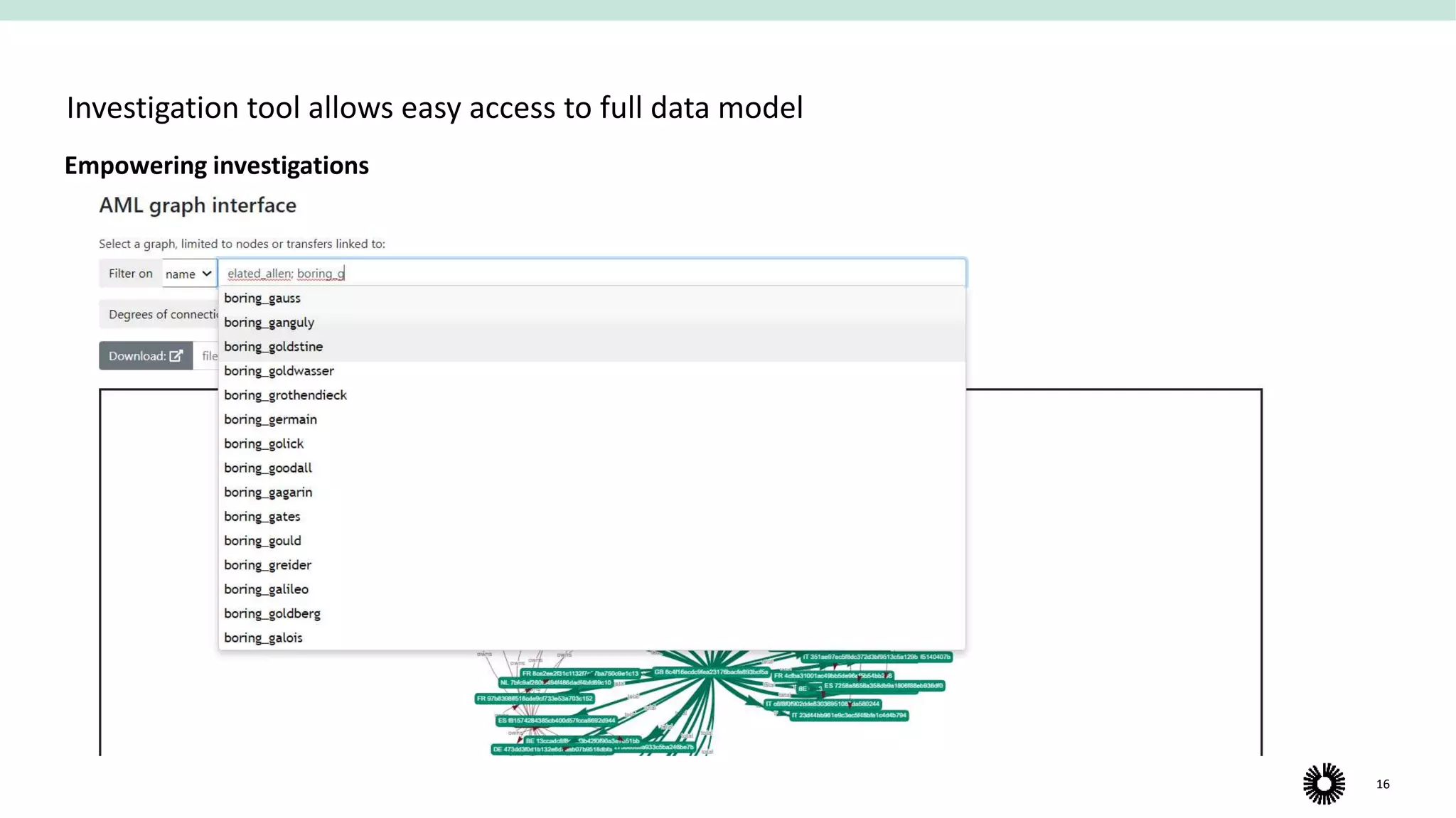

The document discusses Banking Circle's use of graph technology and a data-driven approach to improve its anti-money laundering efforts. It represents payment data as a network to extract features for machine learning models that detect suspicious activity. This approach generates fewer false alarms than rules-based systems while identifying more high-risk payments and accounts. Network-based investigations also help analysts explore connections more efficiently. The new system screens over 1 million payments daily and has increased alerts leading to compliance actions by 1300% while reducing total alerts by 30%.

![[DSC Europe 22] Anti-Money Laundering ML Modeling approach - Gizem Akar](https://cdn.slidesharecdn.com/ss_thumbnails/gizemakarantimoneylaunderingmlmodel-221130080718-afd93383-thumbnail.jpg?width=640&height=640&fit=bounds)