Download to read offline

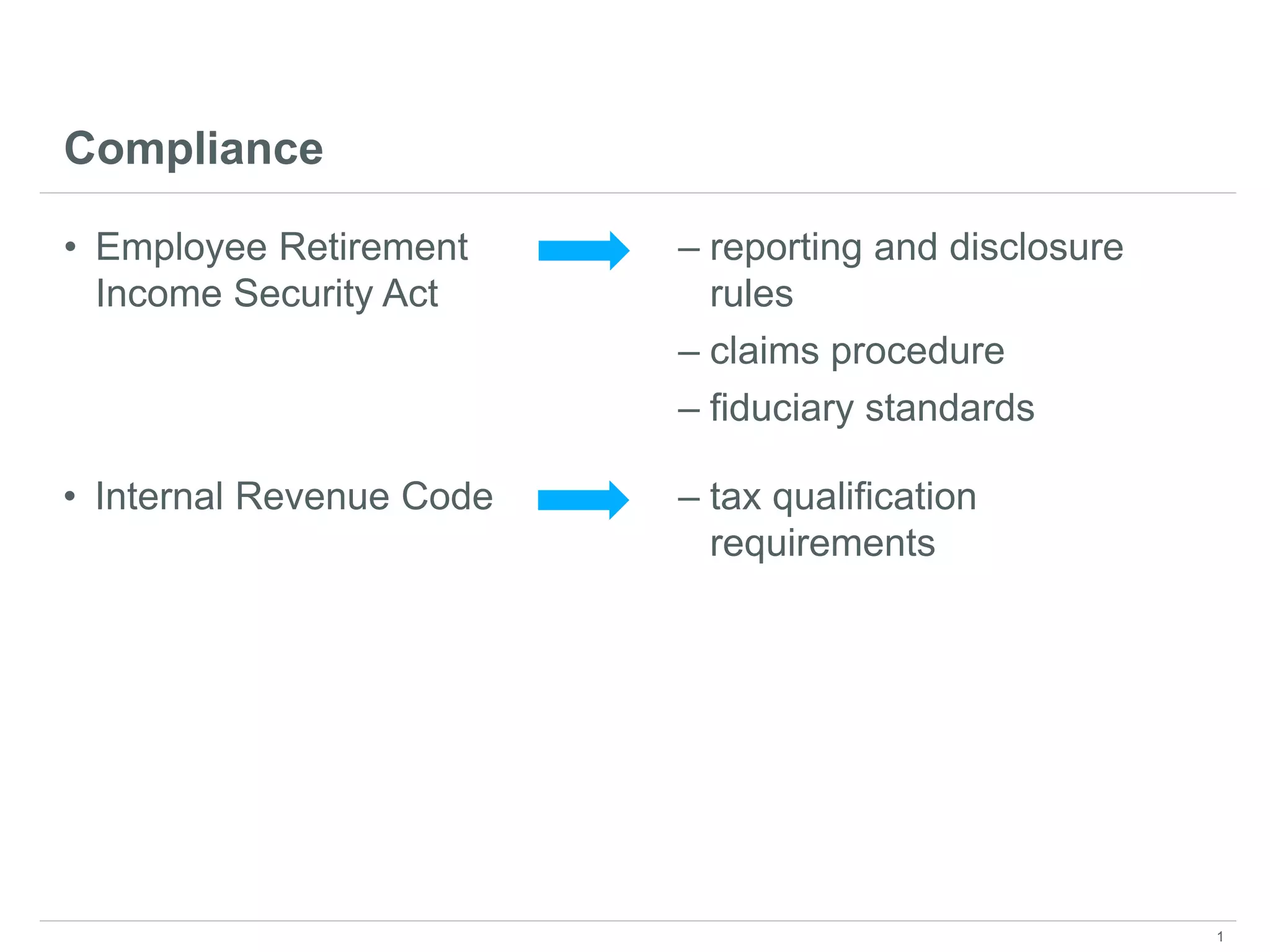

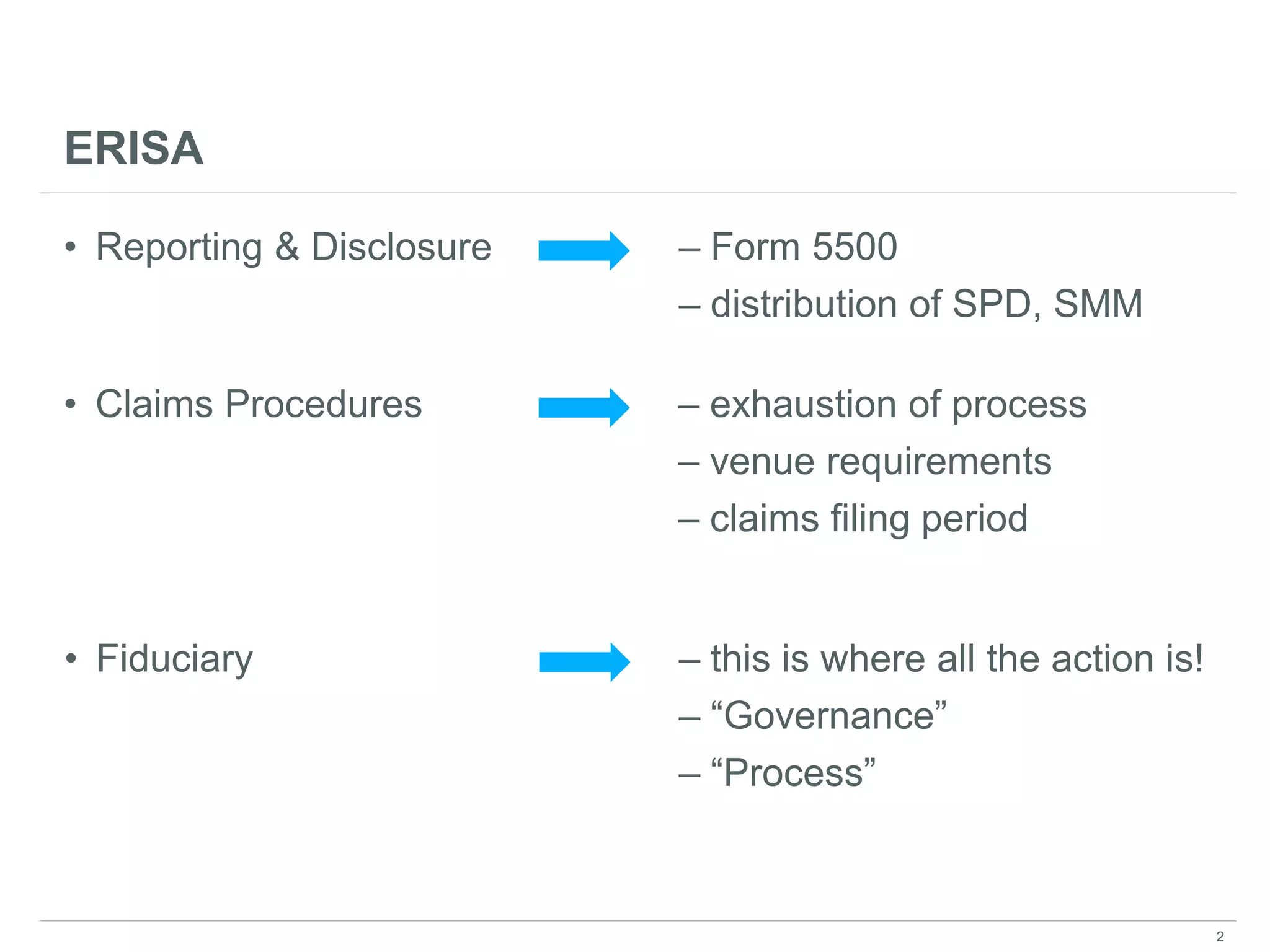

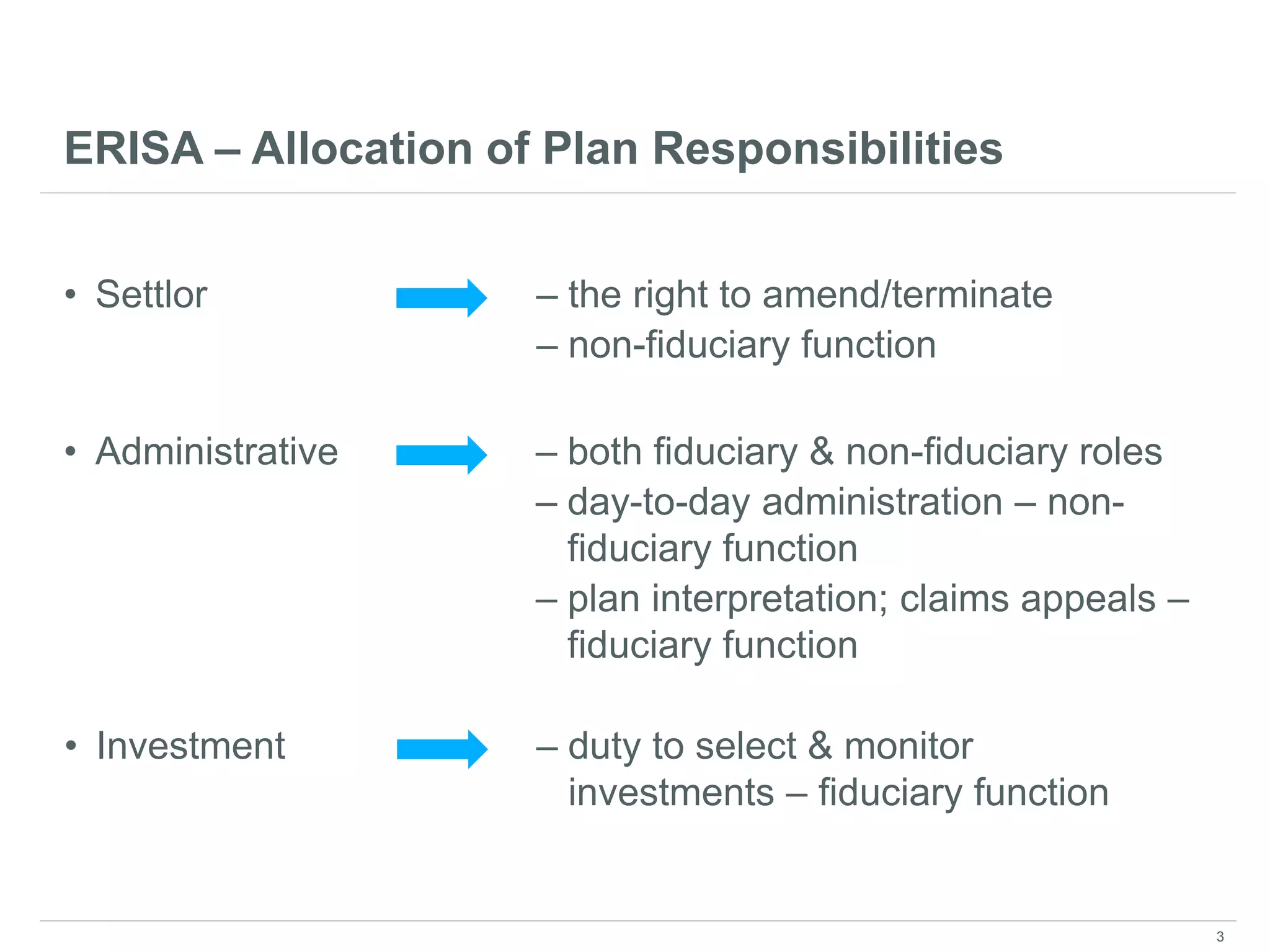

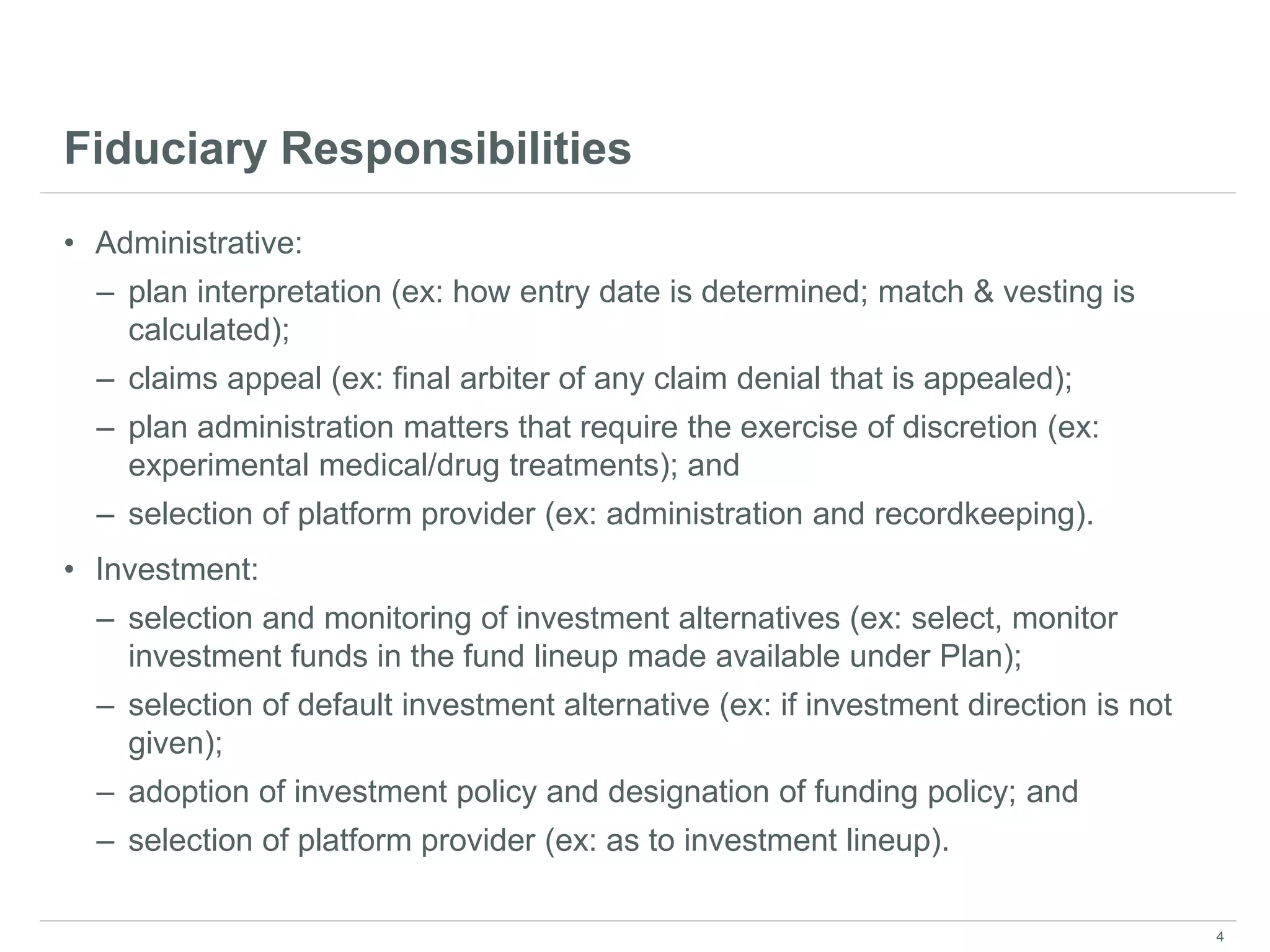

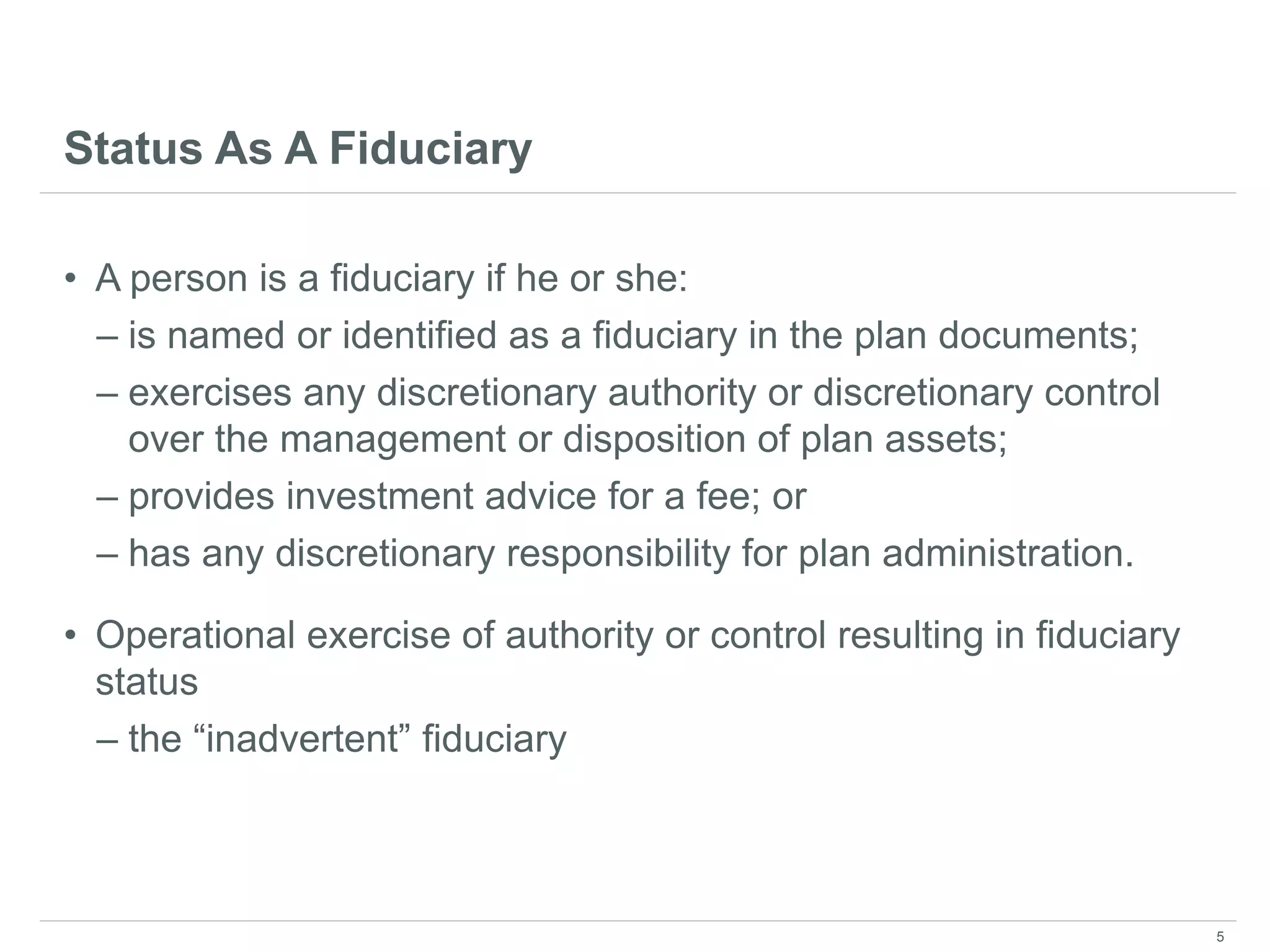

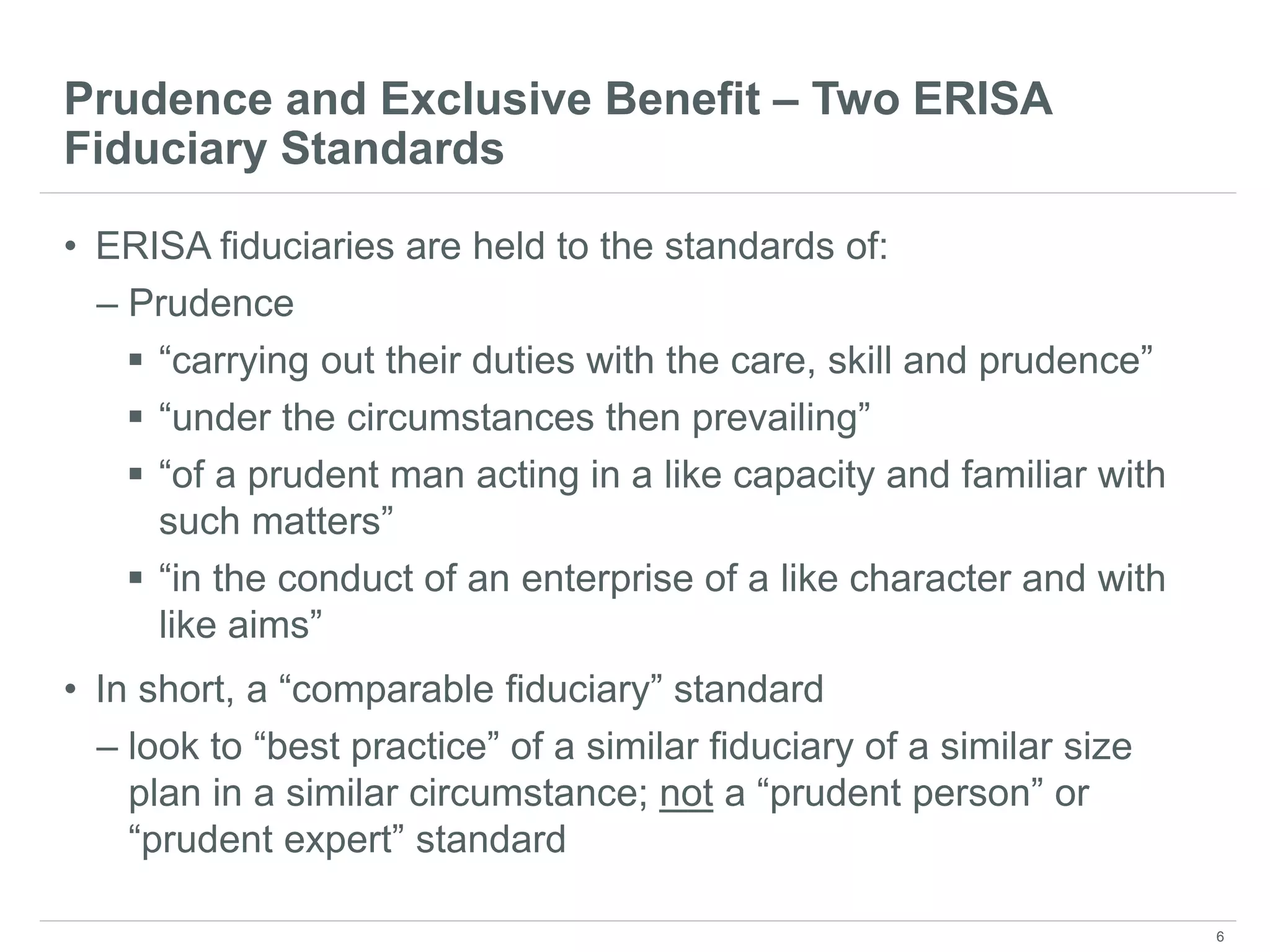

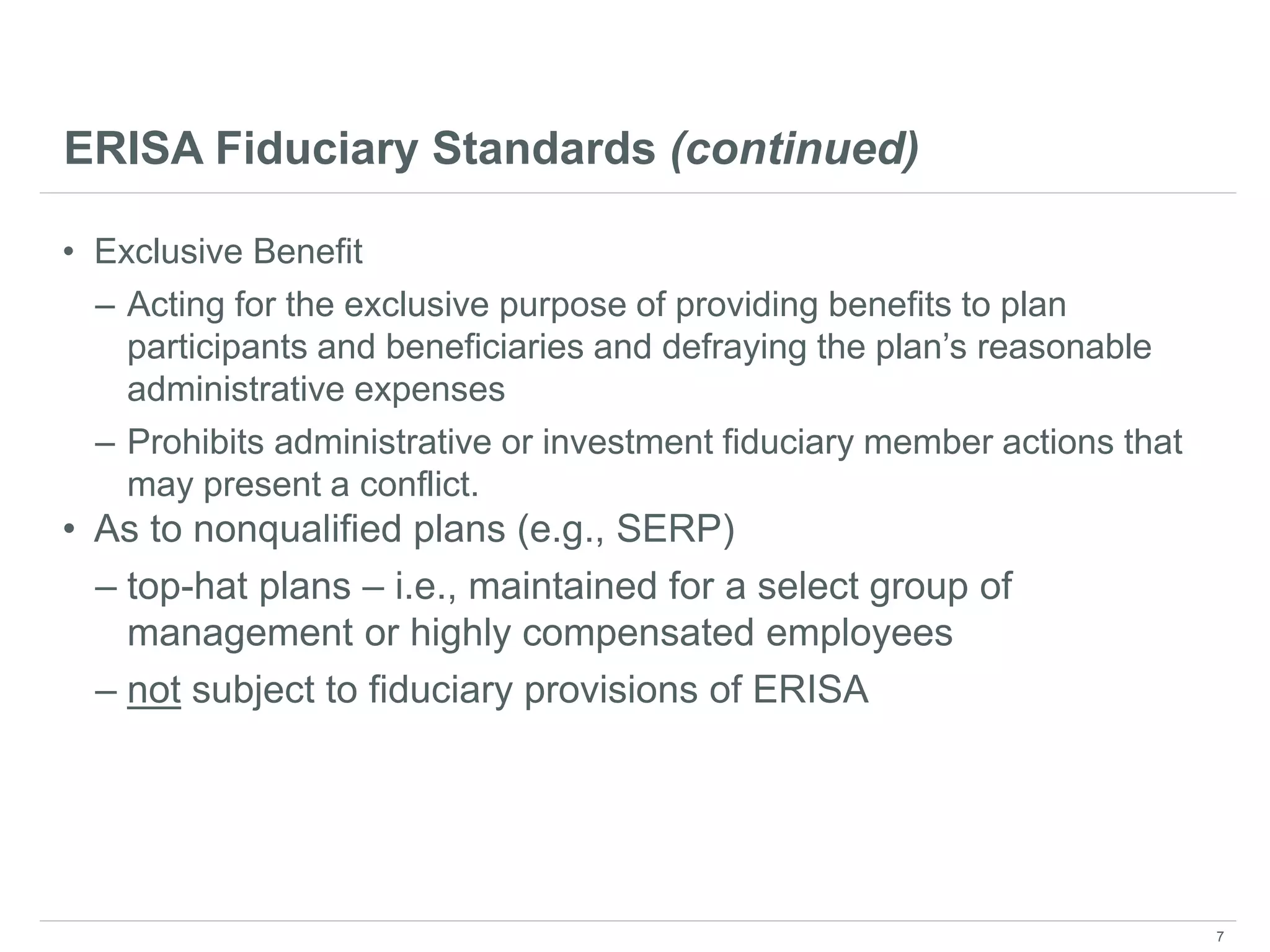

This document summarizes key compliance requirements for qualified retirement plans in 2017, including ERISA and Internal Revenue Code rules. It discusses fiduciary responsibilities under ERISA, such as acting prudently and for the exclusive benefit of participants. It also covers new fiduciary regulations defining investment advice, exceptions, and class exemptions. The document concludes with an overview of plan document and operational compliance requirements under the Internal Revenue Code.

![Szw Pp Presentation Cai Version[1]](https://cdn.slidesharecdn.com/ss_thumbnails/szwpppresentationcaiversion1-12953614988461-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)